GTX - Dana Incorporated: Recent Share Weakness Unjustly Overshadows Value

2023-05-16 18:47:39 ET

Summary

- Dana Incorporated, a vehicle servicing company, has seen its stock underperform lately, even as sales grow.

- The company's sales continue to climb, but margins have been mixed.

- Despite this, Dana Incorporated's shares look cheap on an absolute basis and fairly valued compared to similar firms, making it a decent "buy" candidate.

When it comes to value stocks, the market can be rather stubborn. It can spend weeks, months, or even longer, holding a stock down or pushing it even lower, despite your conviction that the stock should move higher.

A really good example of this can actually be seen when looking at Dana Incorporated ( DAN ), a company that's dedicated to servicing different types of vehicles such as commercial vehicles and off-highway equipment, by providing them with axles, transmissions, drivetrain components, and more. Even though shares of the company look incredibly cheap on an absolute basis and are probably fairly valued when stacked against similar firms, the stock has pulled back over the past several months. Though disappointing, I do believe that this affords investors an interesting opportunity that they can capitalize on. In all, I believe that the company makes for a decent "buy" prospect at this time.

Driving in the wrong direction

Nearly a year ago, in June of 2022, I ended up revisiting Dana to see what kind of upside potential, if any, the company offered. Over the prior few months, shares the business had achieved rather poor performance even though top line and bottom line results were generally positive year over year. Even though 2022 was slated to be a difficult year for the business, management remained optimistic and shares of the company looked attractively priced. This all led me to rate the business a "buy" to reflect my view at the time that the stock should outperform the broader market moving forward. Since then, Dana has sadly underperformed. While the S&P 500 (SP500) is up 7.9%, it has seen downside of 8.3%.

{kind=link}

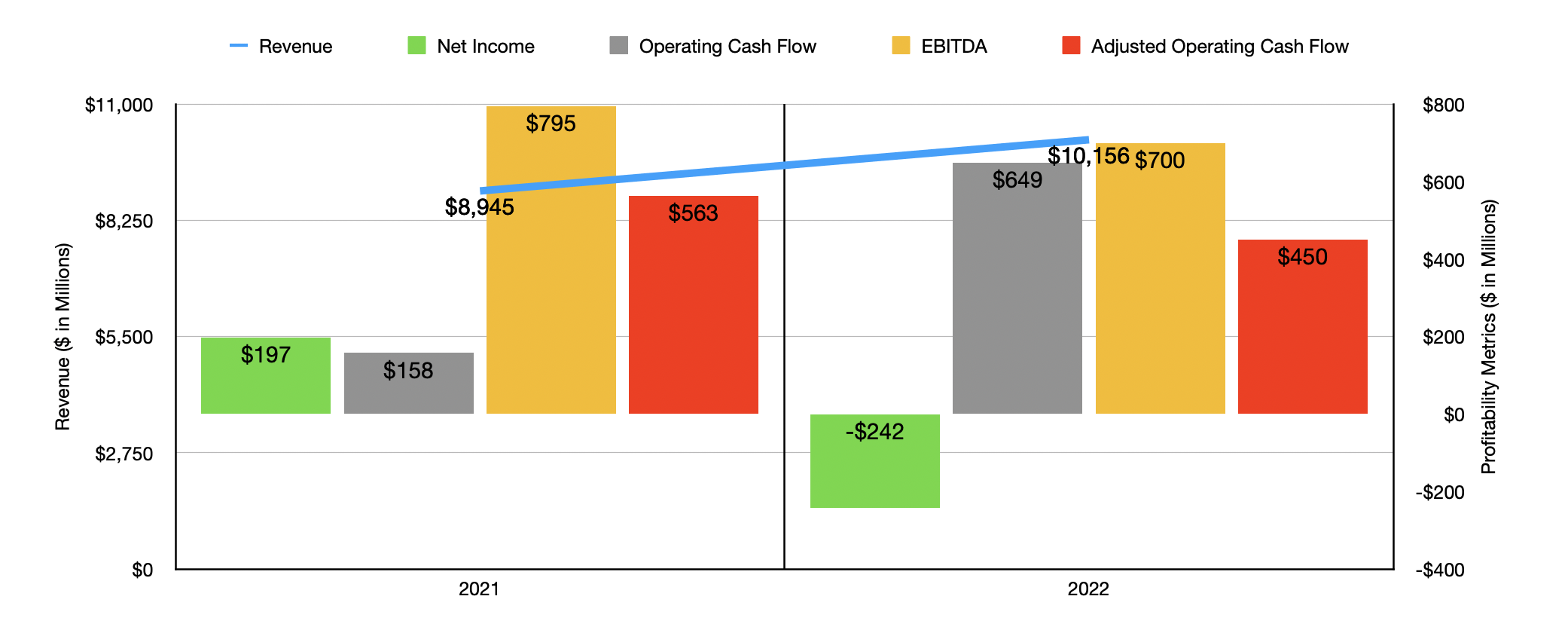

The big question is whether or not this return disparity is justified. In my view, the answer is no. But it's not just my opinion. It's also a question of fundamentals. Consider how the company performed during its 2022 fiscal year . Sales for that time came in at $10.16 billion. That represents an increase of 13.5% over the $8.95 billion the company reported one year earlier. The largest portion of this sales increase came from the company's operations in North America. Revenue there spiked from $4.23 billion to $4.92 billion. This was a roughly 16% rise, driven largely by stronger light, medium, and heavy-duty truck production volumes, higher light vehicle engine production levels, and management’s ability to work on addressing its growing backlog. Interestingly, sales for the company as a whole would have been higher to the tune of $420 million had it not been for foreign currency fluctuations. Most of that pain came from Europe.

On the bottom line, the picture was a bit different. The business went from generating a profit of $197 million to generating a loss of $242 million. Despite the nice increase in revenue, the company suffered from a decline in its gross profit margin from 9.4% to 7.5%, largely because of inflationary pressures centered around commodities, wages, and more. Other profitability metrics for the company were quite volatile. Operating cash flow, for instance, jumped from $158 million just $649 million. But if we adjust for changes in working capital, we would get a decline in the metric from $563 million to $450 million. Meanwhile, EBITDA for the company dropped from $795 million to $700 million.

{kind=link}

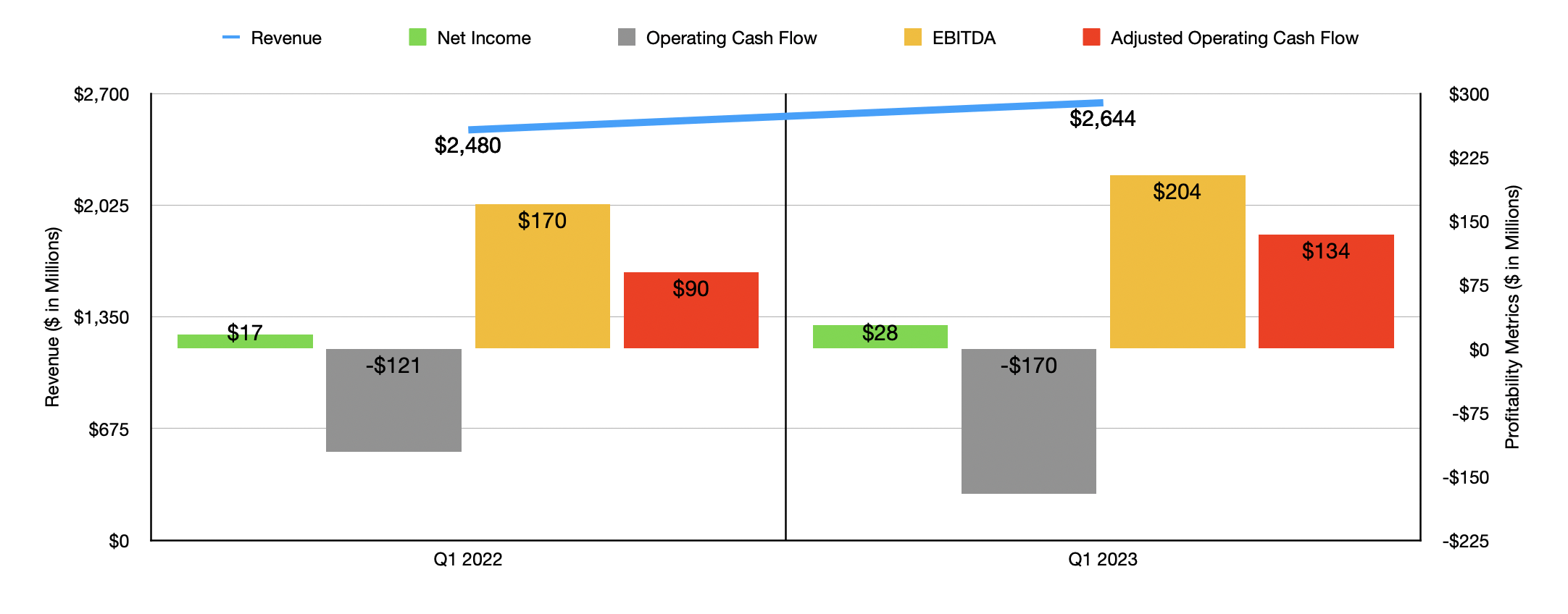

For the current fiscal year, results are similarly mixed, but mostly positive. Sales totaled $2.64 billion for the first quarter of the year . That's 6.6% above the $2.48 billion reported one year earlier. Unlike in the 2022 fiscal year, the strong spot for the company for the first quarter of 2023 was actually its operations in Europe. Even though the company faced A headwind of $47 million, revenue in Europe grew $119 million year over year from $801 million to $920 million. This rise, according to management, was driven by high demand and off-highway operations, strong construction and mining equipment demand, and other factors. On the bottom line, profits for the business shot up from $17 million to $28 million. Operating cash flow actually worsened from negative $121 million to negative $170 million. But on an adjusted basis, it went from $90 million to $134 million, while EBITDA expanded from $170 million to $204 million.

For the 2023 fiscal year in its entirety, management has some pretty high hopes. Overall vehicle sales so far in 2023 are looking pretty strong. For instance, the light vehicle market this year in the U.S. is forecasted to hit 14.5 million units. That would imply growth of between 10% and 12% compared to what we saw last year, though the company will likely see some weakness in the commercial and off-highway categories. Because of this, management expects revenue for the business to come in at between $10.35 billion and $10.85 billion. At the midpoint, that would translate to a 4.4% increase compared to what the company saw in 2022. Earnings per share are forecasted to be between $0.25 and $0.75. Management is also forecasting operating cash flow of between $510 million and $560 million, with EBITDA expected to come in at between $750 million and $850 million.

{kind=link}

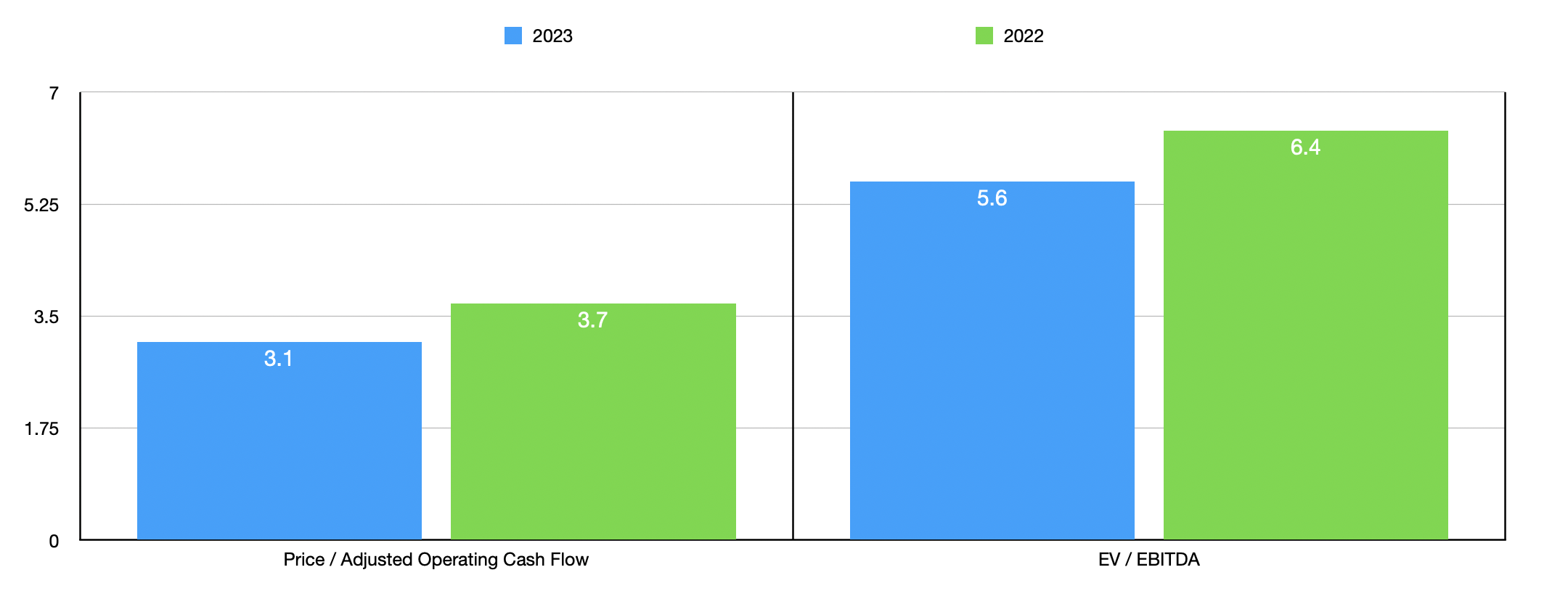

Based on these figures, we can easily value the company. As you can see in the chart above, shares are trading at a forward price to adjusted operating cash flow multiple of 3.1 and at a forward EV to EBITDA multiple of 5.6. These numbers represent an improvement over the readings that we would get using data from 2022. As part of my analysis, I also compared Dana to five similar firms on a price to operating cash flow basis, two of the three companies were cheaper than it. Using the EV to EBITDA approach, I found that three of the five companies were cheaper than our prospect.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Dana Incorporated |

| 3.7 |

| 6.4 |

| LCI Industries ( LCII ) |

| 4.6 |

| 5.5 |

| Patrick Industries ( PATK ) |

| 3.6 |

| 5.2 |

| Dorman Products ( DORM ) |

| 61.2 |

| 17.7 |

| Standard Motor Products ( SMP ) |

| 14.1 |

| 8.0 |

| Garrett Motion ( GTX ) |

| 1.3 |

| 2.1 |

Takeaway

I understand that Dana Incorporated has not exactly been a very popular prospect over the past several months. This much can be seen by looking at its share price performance. But from a purely fundamental perspective, the picture for the company is decent and shares look incredibly cheap on an absolute basis. They also look reasonably priced relative to similar enterprises. Given these factors, I would argue that Dana Incorporated makes for a decent "buy" candidate still.

For further details see:

Dana Incorporated: Recent Share Weakness Unjustly Overshadows Value