DNMR - Danimer Scientific: Improving - But Could Still Go Either Way

2023-04-04 00:09:53 ET

Summary

- The company had another very unprofitable quarter and year, but may have positioned itself to gradually improve in the latter part of 2023.

- With the completion of its Kentucky facility, the company may have the tools at its disposal to meet growing demand, assuming it wins the business.

- Until the company proves it can generate revenue at a profit, I wouldn't consider it investable; it's good for trading but not for holding.

- Even with its Kentucky facility coming online, I think it's not going to perform in accordance with expectation in the near term because of macro-economic weaknesses.

Danimer Scientific ( DNMR ), which is a bioplastics company that produces sustainable and compostable materials to replace traditional plastics, continues to struggle on its top and bottom lines, even as it attempts to accelerate revenue growth and improve earnings with the completion of its Kentucky facility.

Concerns over its liquidity issues has been somewhat assuaged with the company announcing it has a new senior secured term loan in the amount of $130.00 million.

The company still guides for a weak first quarter of 2023 in regard to both product and service revenues, in part of the timing of shipments concerning a major customer.

Further out, DNMR expects its new commissioned facility in Kentucky to have a significant impact on its performance, with it starting to ramp up in the second half of 2023 and onward.

For no visible reason the share price of DNMR took off on March 24, 2023, jumping from approximately $2.00 per share to about $3.50 per share on March 31, 2023.

In this article we'll look at some of its numbers, the potential impact of its Kentucky facility, and what the surge in its share price suggests to investors.

{kind=link}

Some of the numbers

Revenue in the fourth quarter of 2022 was $15.3 million, compared to revenue of $17.7 million in the fourth quarter of 2021. Full revenue for 2022 was $53.22 million, compared to full year revenue for 2021 of $58.75 million, a decline of -$(5.50) million. Both product and service revenue were down in the fourth quarter and full year 2022.

The decline in product revenue was primarily attributable to a $9.9 million drop in PLA-based product sales associated with the conflict in Ukraine; that's not going to be mitigated anytime soon.

Lower service revenue was, for the most part, the consequence of a $2.6 million decline in research and development contracts as various projects moved forward to completion.

Adjusted EBITDA in the fourth quarter of 2022 was -$(8.6) million, compared to adjusted EBITDA of -$(10.2) million in the fourth quarter of 2021. Adjusted EBITDA for full year -$(45.00) million.

Net loss in the reporting period was -$(28.1) million, compared to a net loss of -$(12.4) million in the fourth quarter of 2021. Net loss for full year 2022 was -$(179.8) million, which included a goodwill impairment charge of -$(62.7) million in the third quarter of 2022.

The company had cash and cash equivalents of $62.8 million at the end of calendar 2022. It held $288.4 million in total debt at the end of 2022.

In order to bolster its liquidity issues, the company said it has a new senior secured term loan in the amount of $130.00 million.

As for guidance, management said with the visibility it has, the first quarter of 2023 will have further declines in product and services revenues in comparison to the first quarter of 2022. That was partially attributed to the timing of shipments to one of its customers in contrast to last year.

That points to a big risk the company has, which is heavy reliance on only two customers, which in 2021 accounted for 35 percent of total revenue, and in 2022 accounted for 40 percent of overall revenue. Any type of headwind from either of those companies would have a significant impact on the performance of DNMR. The company needs to develop a better customer mix over time, in order to mitigate that risk.

Profitability

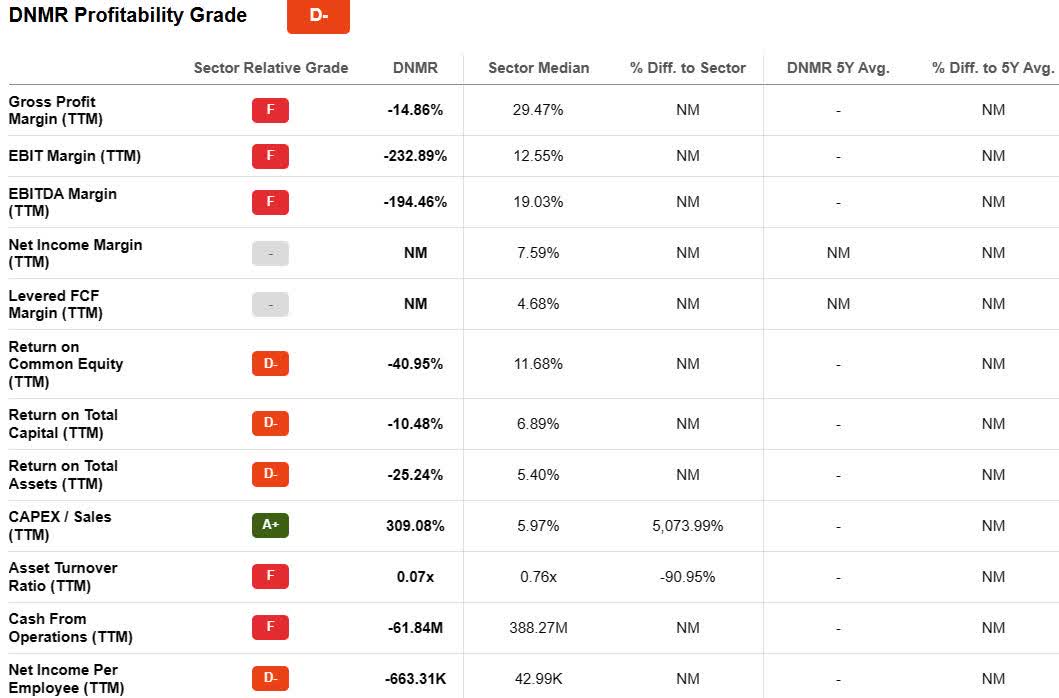

Almost all of DNMR's profitability metrics are dismal in comparison to the sector median.

EBIT margin [TTM] was -(232.89) percent, compared to the sector median of 12.55 percent. EBITDA margin was -(194.46) percent, compared to the sector median of 19.03 percent.

Return on equity [TTM] was -(40.95) percent, compared to the sector median of 11.68 percent, return on capital [TTM] was -(10.48) percent, compared to the sector median of 6.89 percent, and return on assets was -(25.24) percent, compared to the sector median of 5.40 percent.

Cash from operations was -$(61.84) million, compared to the sector median of $388.27 million.

{kind=link}

Concerning valuation metrics , EV/Sales [TTM] was 11.33, compared to the sector median of 1.48, up 664.67 percent. EV/Sales [FWD] was 6.54, compared to the sector median of 1.51, up 332.95 percent.

As for Price/Sales [TTM], that came in at 6.55, compared to the sector median of 1.14, up 476.85 percent. And Price/Sales [FWD] was 3.82, compared to the sector median of 1.14, up 233.95 percent.

Price/Book [TTM] was 0.93, compared to the sector median of 1.76, down -(47.08) percent.

In regard to revenue growth [TTM] the company was -(9.41) percent, compared to the sector median of 10.83 percent. Revenue growth [FWD] is 39.40, compared to the sector median of 4.79 percent, up 722.74 percent.

With no visible reason for the share price of DNMR to jump as it has recently, it appears the major reason is the high amount of short interest in the company, which stands at slightly under 19 percent at this time. In other words, it looks like it was a short squeeze, and with the metrics shown above, I don't see it being able to be sustainable.

Since there are no near-term catalysts, I see the value of DNMR at about the $2.000 level it was when the share price took off. And as management stated, it's likely to be a tough first quarter of 2023.

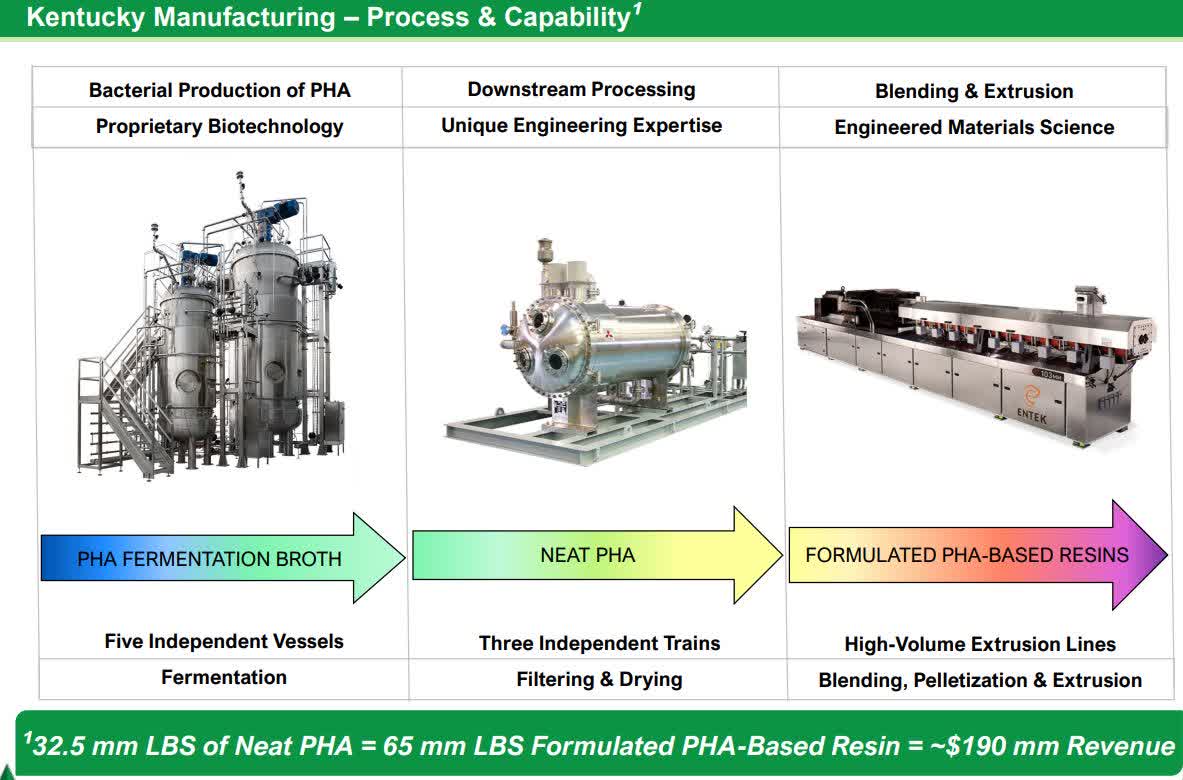

Potential from its Kentucky facility

Concerning the numbers associated with its Kentucky facility , management stated that it has PHA capacity of 32.5 million pounds, which would enable the facility to produce approximately 65 million pounds of formulated resin.

Using a baseline price of a little under $3.00 per pound, the Kentucky plan could deliver close to $190.00 million in revenue per year. At this time, it isn't known how much margin it'll produce until the facility is being fully utilized. As a rough guess, management sees it being above 30 percent.

Assuming the accuracy of the numbers, that would generate about $60.00 million in cash flow at the plant, which should produce positive EBITDA for DNMR.

The key for the company in the near and long term will be how much demand for its PHA-based resins grow and how it executes on boosting production capacity at its Kentucky facility. One thing not being discussed much is, the potential impact of a declining global economy in 2023, and possibly in early 2024. I think it's going to get worse during that period of time, and that is very likely to limit, or even result in a decline in demand over the next year or so.

{kind=link}

To me, that suggests that even with the launch of the Kentucky facility, it is unlikely to tap into the benefit of that in the first half of 2023 for sure, and with the increasing probability of a recession, in the latter half as well. The issue at this time with the Kentucky plant isn't its potential, but rather, whether or not demand for PHA will be enough to tap into the full benefit of the plant. I don't think demand will rise to levels where it will over the next year or so, which is another reason why I see it falling back to the low $2.00s, and possibly lower.

Demand outlook

The company sees demand for the materials it produces as having long-term growth potential, particularly from young adults that have an increasing amount of buying power, which will grow over time.

Citing the passion that the demographic has for issues of which PHA can be part of the solution, and how they're educating themselves in regard to products companies offer, management sees this as a long-term growth runway for the company.

DNMR sees younger consumers basing buying decisions based upon the materials products are made of. It also believes that companies will lose market share to younger consumers if they don't adapt and embrace products like it can offer. Assuming that's how it plays out, DNMR is positioned for a long-term growth cycle if it's able to win market share and grow revenue at a profit. It isn't close to being able to at this time, and it appears it's going to take quite a while before we know if it's able to do so.

Management cited an example in Europe concerning the potential of the sector. It pointed to proposed legislation in Europe that if approved, would by the end of 2023 trigger a 24-month window where petroleum plastics would be banned from use in manufacturing single-use coffee pods, and other products as well.

Based upon anticipation of the legislation being enacted, DNMR is currently working with three large producers in Europe to launch test market launches in the latter half of 2023.

According to management, if the company grabbed 10 percent share of the coffee pod market in Europe, it would require all of the nameplate capacity at its Kentucky plant to meet that demand.

Conclusion

As many readers know, we've all heard this type of narrative before in regard to 'green' markets. The potential is always defined as extraordinary, and as being inevitable concerning its success.

While that may be true generally, there's no way of knowing at this time whether or not DNMR can execute on it vision and strategy, and if it can boost revenue at a profit. Based upon the numbers, it's a long way from being profitable, and even though it secured a loan, that only solves short-term liquidity.

It's readily apparent that how its Kentucky facility goes, so will go the company. While I think it can ramp up production, the key question that must be answered is if the demand will be there to justify it, especially in an economy that I believe is going to get worse going forward.

The company has enjoyed a recent boost in its share price, but I think that's related to investors pushing up the price in anticipation of its earnings report. Nothing in the report warrants the share price to remain elevated, so I'm looking for a big drop in the price in the near term as investors quickly start to take profits.

That said, the share price has broken well above $3.00 per share, and if it retains momentum, it could move up even more before it corrects. Nonetheless, with no immediate, positive catalysts with the company, there's nothing to justify the price remaining at these levels, even if it temporarily moves higher.

As for the long-term, 2023 is going to be an important year for DMNR because of the launch of its plant in Kentucky. Now we'll be able to get feedback from the results associated with the plant and have more clarity and visibility concerning the prospective performance of the company on the top and bottom lines.

To me, the time to buy DNMR was when it was trading under $2.00 per share. Now that it's trading near $3.50 per share, it's far too high for it to be an attractive risk/reward scenario. If the economy continues to go south as 2023 unfolds, the share price of DNMR is going to take another big hit and could test its 52-week low of $1.57 per share. If it falls below that, it could the time to consider taking a position, with the idea of it being considered a highly speculative buy, and one that could take time to be profitable for traders.

As the company stands today, I don't consider it one that should be invested in with a buy-and-hold mentality, but one that has the potential be a trading vehicle because of its volatility.

For further details see:

Danimer Scientific: Improving - But Could Still Go Either Way