GPDNF - Danone: A Potential End To The Underperformance

2023-10-10 00:53:09 ET

Summary

- Danone's investment performance has been disappointing for the past few years, with lots of ups and downs due to material challenges in its business.

- While the company has not provided a positive experience for investors, I believe a turnaround may be in the future, and the upside is there.

- I view Danone as an attractive investment with an upside potential, even if the yield of below 4% might make it less than ideal for many investors given the rate environment.

Dear readers/followers,

Danone ( DANOY ) ( GPDNF ) has not been an overly pleasant experience to invest in thus far. The Russian invasion of Ukraine could certainly be partially blamed for this. While we at least have not seen declines since my last article back in January of 2023, the company is nonetheless not at a great overall ROR, not outperforming the current trends in the S&P 500 here.

However, I remain fully convinced in and invested in the attraction of dairy and consumer goods companies in Europe for the long term. And that includes Danone. The company also had a bit of a "peak" this year, but has since then declined back down, to give the RoR we're currently seeing of around 4.6% inclusive of the 2022 dividend.

Seeking Alpha Danone (Seeking Alpha)

The company's challenges are many - and I'm not even pointing to the fact that it still has operations in Russia which, other than its peers and most other Western businesses, are still active. I also of course mean things like inflation, SCM, and wage development which are putting pressure on the company's bottom-line development.

In this article, which is an update to this specific piece posted around 9 months back, we're going to take a look at what upside we can expect now that we've declined back down to almost the level I wrote at before.

We have 1H23 to look at - and that's the first thing we're going to do here.

Danone - Plenty to like about dairy products, even with the pressure we're seeing.

Danone is not a company anyone interested in consumer goods investing should be ignoring, or afford to ignore. That is because out of the world's consumption of dairy products, Danone has a 5% market share. This does not sound much, but consider for a moment the amount of dairy products being consumed, the company's brands therein (as well as in the Water sector)...

Danone IR (Danone IR)

...and then consider again what sort of appeal this company might have. The challenges to the businesses are several. Ownership, even if now sort of "solved", of Chinese Mengniu was one of the primary ones - but all of those risks always need to be put into context of the company's overall upside, which is being the sort of global dairy player with the sort of upside they are.

The simple fact is that there is not a single continent on earth where Danone's dairy products are not being sold.

The biggest geographical markets are by far the USA with 20% of sales - though this is not as significant exposure as it is for Nestlé. France is another 9%, and China is also 9%. Just as with Nestlé, emerging markets contribute to nearly 50% of the company's sales - so continents like South America, Africa, and other emerging markets are highly important to the business. (Source: 2Q23 Danone )

This is probably part of the reason why many view the company as somewhat risky - and indeed, this argument does hold some water.

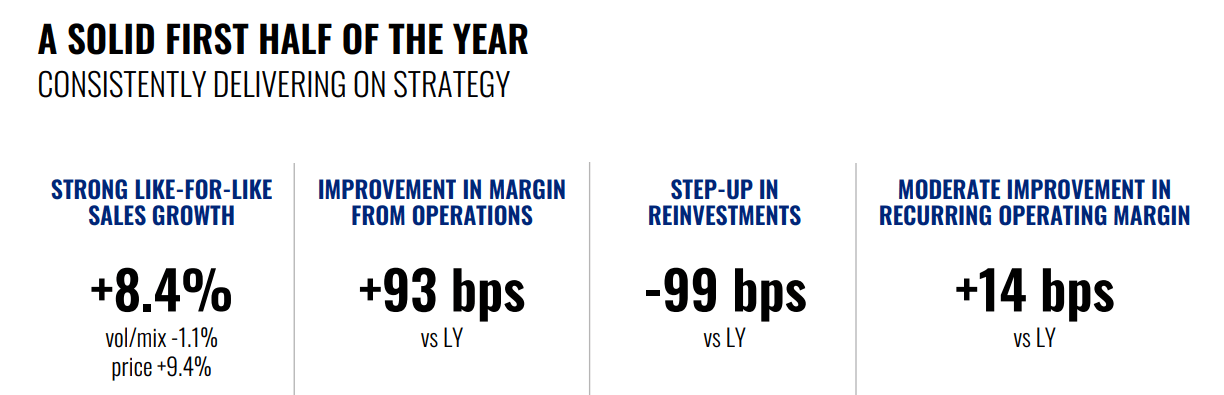

However, those risks need to be taken into consideration and compared to the actual upside we're seeing here. Because we have very strong LFL sales growth, good operating margin improvements, and slight margin improvements as well. (Source: 2Q23 Danone)

If you recall, part of the company's problems have been the sales development trends, and exactly what's being slowly improved here. Don't expect wonders though - because a turnaround like this obviously is going to take significant time.

{kind=link}

Progress on its fundamental categories in Europe is a set of good news though. The Danone brand remains the core brand, with Danonino for kids, while sweets and "indulgence" products are being marketed under brands like Danetter and Oikos, and with a solid healthy portfolio where Actimel and Activia are some of the most well-known brands out there. Both Everyday nutrition and VAP products are being ramped up and seeing growth.

{kind=link}

But the company has non-core winners like Evian, and YoPRO brands (albeit a very complex market on that one) as well as specialized nutrition - although the nutrition and supplement market is an absolute beast in terms of competition, flow, and volatility.

What's more interesting to me is how Danone chooses to handle its lackluster performers, of which there are quite a few. Like many companies in the situation, Danone is actively divesting and simplifying away from its portfolio and focusing on strong brands. (Source: 2Q23 Danone)

This led to 15.9% top-line LFL growth in 1H23, mostly volume-driven, which is of course a positive as opposed to that growth coming mostly from pricing. The company's market shares have been restored - albeit slowly, and it's introducing two new innovations, Zero and "Electrolytes", though this product reminds me quite a bit of the movie "Idiocracy"...

Danone Electrolytes (Danone)

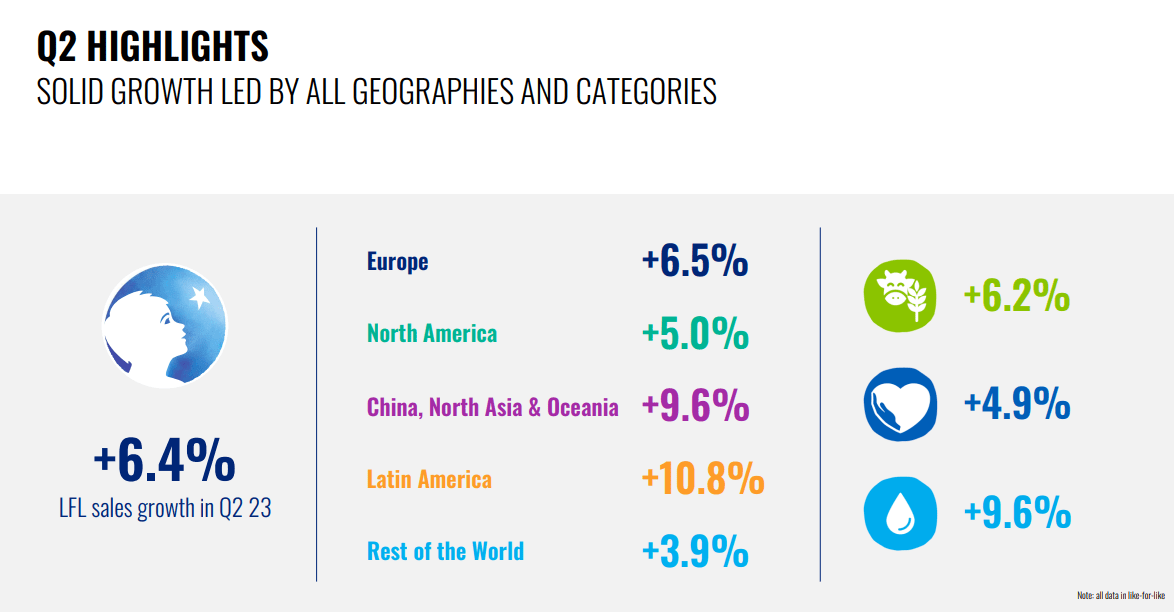

That aside, the company's performance in 1H23 was solid. By solid I mean that every single geographical segment grew, leading to 6.4% LFL growth in 2Q23 sales. Most of it came from LATAM, with almost 11% growth - but the growth was broad-based both geographically and in terms of products.

{kind=link}

Take Europe for instance - all categories grew in terms of sales, even if that growth for Europe was more based on pricing than volume. Volume growth was impressive in China, North Asia, and Oceania, where price-driven revenue increases accounted for only 1.2%, but volume was up 11.2% for the Half-year. (Source: 2Q23 Danone)

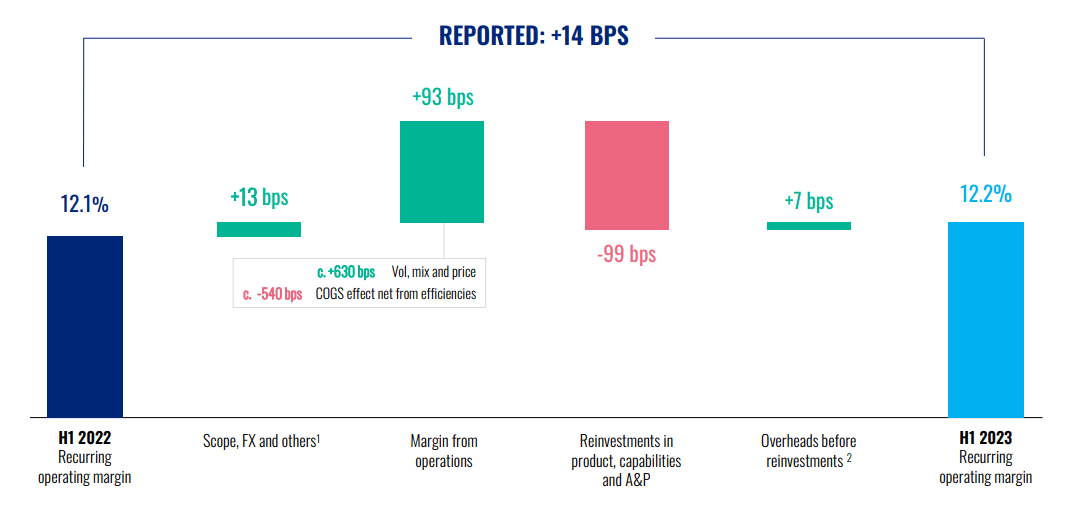

What about the company's struggling margins? Danone went into the half-year comparing to a 12.1% EBIT margin but saw almost a 100 bps improvement based on volume, price, and mix improvements. At the same time, reinvestments did this to that margin trend.

{kind=link}

So, slight improvement, even after that, but it is more or less flat. 10 bps is almost a rounding error here - the positive here is the clear operational improvement, which by the way is what many analysts have been specifically asking for.

We therefore finished the 1H23 with a 7.6% impressive EPS improvement, and Danone was able to generate €1.1B of free cash flow, based on operational improvements, FX with only small impacts from Tax and other effects. That comes to €1.7/share reported for the 6-month period compared to €1.14 reported last year. (Source: 2Q23 Danone)

Danone has also, far later than most companies, deconsolidated EDP Russia as of July in 2023. It's a complex situation because while the company no longer retains management control, the company is still the legal owner of EDP Danone Russia.

This is very different than other businesses I've been reviewing and how they've gone about treating Russia, and it's most certainly a risk as I see it here and how I would treat it as an investor.

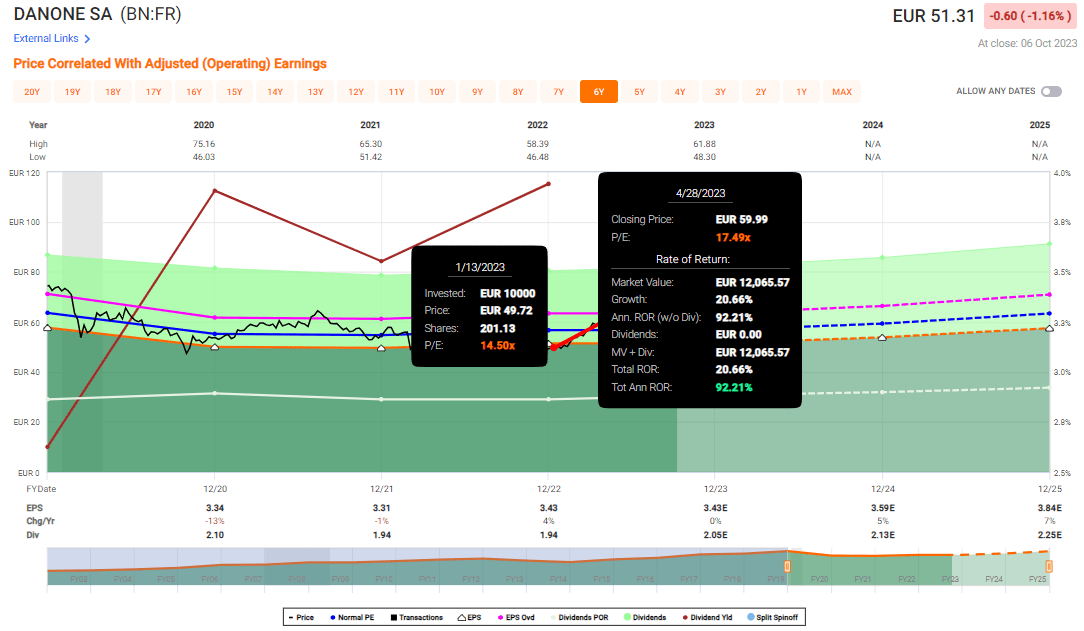

Danone has been troughing in terms of valuation for about 3-4 years at this point. It used to be a company trading in accordance with its incredible dairy market share, commanding a P/E of at least 18-20x.

That is no longer the case. The last few years have seen Danone staggering between a 15x-17x P/E, while drops down to 15x P/E have been almost common, happening at least 2-3 times in the last 4 years.

This makes the valuation treatment of this company as an investment fairly easy as I see it.

Danone - The valuation is getting more compelling here.

Danone has been hammered not only by the market but by analysts. Yet if you look at the trends since I went bullish in January of 2023, there was a very "easy" time when you could have made over 20%, or 90+% annualized by simply sticking to fairly simple valuation theses of selling at or close to 15x, and watching the company at 17.5x.

{kind=link}

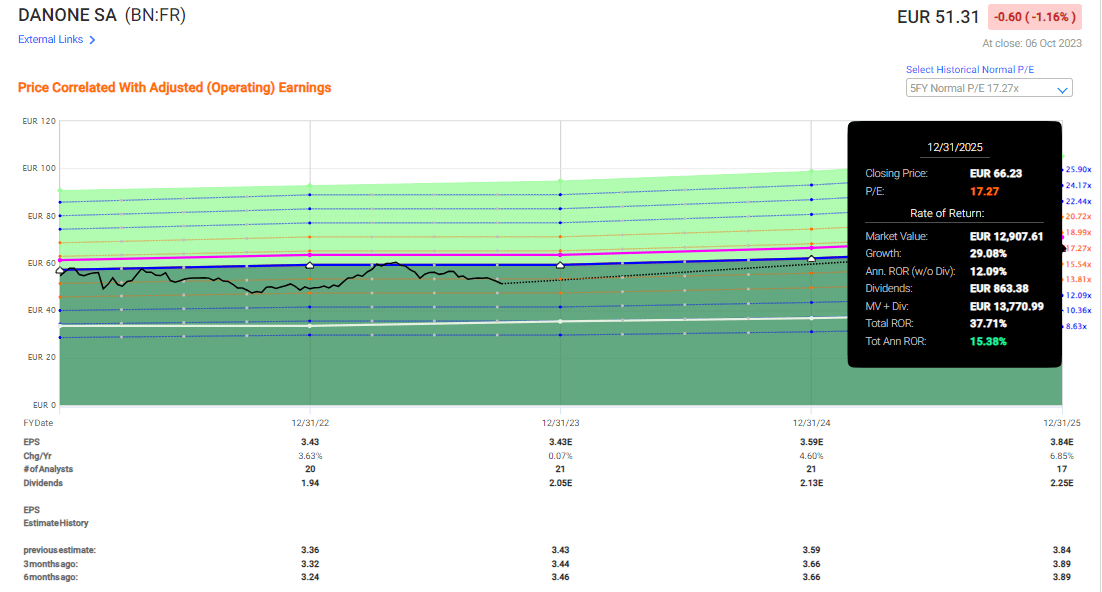

I furthermore remain convinced that the company won't for long drop far below 15x P/E without some sort of very serious long-term impact, and a 17-18x P/E valuation is a good target for Danone - that's where I target the company. I do not expect a lot of growth this year, maybe 3-5% for 2024 and 2025E.

The main appeal of Danone at this time is the above-average yield for the consumer goods sector - almost 4% here - coupled with a reversal and growth upside.

If you forecast at 17.2x, the lower mid-end of that spectrum, then that RoR is over 15% per year here and is good enough to where I consider the company a worthy "BUY".

{kind=link}

Remember, my last PT for Danone was a conservative €58/share. I'm sticking to this PT as of this article, and my sticking to my PT shouldn't surprise any of you who follow my articles - because I very rarely actually shift my targets. A 17.27x P/E for Danone on a basis of 2025E implies a share price of €66/share, which shows you just how conservative my targeting for this company is.

I also, in my last article, went through a few possible options plays. Despite the increased volatility here, I was unable to find attractive options plays for Danone on the basis of CSP here.

I continue to believe that common share investments mark the best option for those interested in Danone. While the increased risk-free rates might have made this investment less interesting than before - a simple savings account gives you more interest than a 3.9% yield - the capital appreciation upside to this company here makes it interesting to me, and that is why I might buy more of the company here.

I continue to value and model for growth in this company, albeit a low one, and the DCF valuation models still show a significant potential upside to at least the mid-€50's to low €60's here , even accounting only for slight growth.

The current overall valuation targets looking at other analysts come to a range of €41 to €70, with an average of €58.5, implying an undervaluation of 14.3% at this time. 9 out of 22 analysts are at a "BUY" or equivalent here, which actually means that analysts are more negative on the stock than the last time I wrote about it.

I personally am more positive about the upside after 1H23 - and I expect continued stability and margin improvement going into the second part of 2023, as well as going into 2024. I expect that the company's pricing power due to its sheer size and scope will overcome the current macro challenges presented, and this is why I focus on companies such as this one for most of my investing - stable, reliable, dividend-paying core companies that based on their operations represent crucial goods and services that are non-optional to most individuals.

Here is my updated thesis for Danone at this time.

Thesis

- Danone is one of the largest food companies on earth. It is less qualitative and less safe than Nestle, which is also why my position in Danone is far smaller than in Nestle, but it's the world's biggest Dairy company, with a #1 market share in Yogurts.

- While the company is facing pressures on the margin side, and with sales as well as leaving behind Russia, the fundamentals of the company remain sound and attractive. I consider this business to be appealing here, even if the company is no longer as dirt-cheap as we've seen it being.

- I give Danone a 2023 October PT of €58, and I consider it a "BUY" here. My PT remains unchanged from my last article.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

I can't fault anything with the company here - at the double-digit upside. I just won't call it "cheap" here - cheap would really be below €50/share, but that is not where we currently are.

For further details see:

Danone: A Potential End To The Underperformance