GPDNF - Danone: Quality Business With Market-Leading Brands

2023-05-26 15:02:49 ET

Summary

- Danone S.A. is a global food and beverage company operating in various regions around the world.

- Revenue has grown at a CAGR of 3%, as Danone has developed its product suite toward healthier options.

- Margins have dipped since the FY16-FY19 period, with no material evidence to suggest improvement.

- Danone looks fairly valued based on historical trading.

Investment thesis

Our current investment thesis is:

- Danone is a high-quality business, with several market-leading brands.

- The company generates its revenues globally, selling products that are highly valuable to consumers' lives.

- Revenue growth looks to be sustainable long term, although margins are disappointing.

- Danone is trading at its 10-year average multiple, which looks reasonable given its current position.

Company description

Danone S.A. ( GPDNF ) is a global food and beverage company operating in various regions around the world. The company is divided into three segments: Essential Dairy & Plant-Based, Specialized Nutrition, and Waters.

Share price

Danone's share price has trended sideways in the last decade, as slow growth and underwhelming profitability have deterred investor interest.

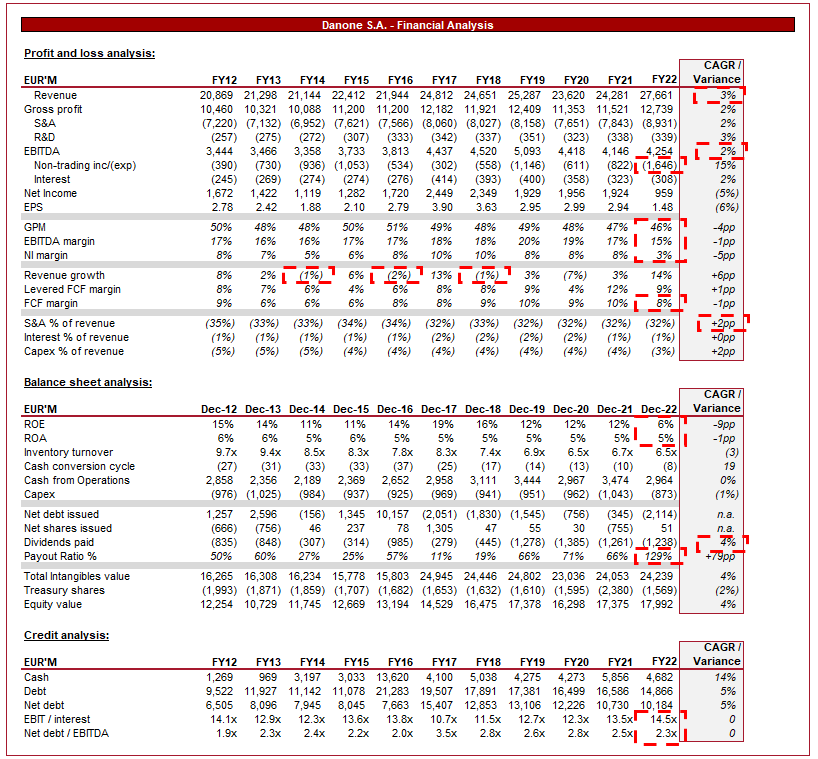

Financial analysis

Danone financials (Tikr Terminal)

{kind=link}

Presented above is Danone's financial performance for the last decade.

Revenue

Danone has grown revenue at a CAGR of 3%, reflecting what has been a mild decade for the business. During this time, the company experienced 4 periods of negative growth, reflecting what has been difficulties in achieving consistency. As a global business, the company is subject to FX movements, which somewhat muddy the results.

Europe remains Danone's largest market, with c.32% of revenue from this region. This diversification is highly valuable as it reduces the risk of market weakness in a particular region, as well as allowing the business to partake in growth markets. This flattens the revenue curve, creating greater certainty over cash flow generation.

Revenue split (Danone)

Danone is the premier provider globally due to its large range of market-leading brands. The company benefits from shared expertise and operational efficiencies across its division, generating accretive returns.

Market positoin (Danone)

Increasing consumer awareness and demand for healthier food and beverage options have been a significant trend in the industry, although reflect the characteristics of a fundamental market shift. Consumers are seeking products that align with their health and wellness goals, such as organic and low-sugar food and beverages. Danone has developed deep expertise in this area, largely committing to being a "health-conscious" provider. As the following illustrates, the majority of the company's sales are considered healthy.

Healthy goods (Danone)

The rise in popularity of plant-based diets has partially stemmed from the above. Stocks specializing in plant-based foods experienced large gains in recent years as the interest from consumers is strong. Danone has also expanded aggressively into this subsector, developing plant-based equivalents of its current products, as well as acquiring leading players in the market. Alpro is a leading milk-alternative brand that has been part of the Danone group for several years.

Environmental sustainability has gained prominence in recent years, with consumers increasingly conscious of the ecological impact of the products they consume. When McKinsey asked consumers if they care about buying environmentally and ethically sustainable products, the response was a clear yes. Danone has demonstrated a commitment to sustainability through initiatives like reducing packaging waste, improving water usage efficiency, and sourcing responsibly. Although anecdotal, Danone's whole annual report presentation felt underpinned by its ESG commitments, reflecting what is a priority for it.

This penetration into sustainability and healthy / plant-based foods will leave Danone on the right side of history in our view when considering where growth in food and beverages is. This exposure should allow Danone to maintain its current trajectory, with scope for medium-term outperformance as consumer uptake improves.

Economic considerations

Current economic conditions are dominated by inflationary pressures, with supply chain issues and other factors contributing to elevated levels for most of 2022 into 2023.

For FMCGs businesses, this generally allows them to outperform, as prices can be increased due to sticky demand. Danone benefits heavily from this inelasticity effect, as consumers are unlikely to cease drinking water, or feeding their children.

The difficulties come with the volume change, as consumers are encouraged to trade down for cheaper products. For this reason, long-term underperformance can develop if Brands are too aggressive with product pricing, as lost volume may never return.

For FY22, Danone experienced a 7.1% LFL increase in sales while experiencing a (0.6)% decline in volume. Considering the other FMCGs businesses we have covered, this suggests Danone is aggressive, given the decline in volume. Further, its volume decline increased more greatly QoQ, suggesting the pricing actions quickly deterred consumers. Many FMCGs have seen volume growth grind to a halt but remain positive.

Margin

Danone boasts underwhelming margins, with an EBITDA-M of 15% and a NIM of 3%.

Margins have slid in recent years, from a high of 20%/10%. Danone has faced rising costs, with disruptions in its supply chain, such as raw material availability and transportation logistics. In conjunction with this, the company has been unable to increase prices to the extent required to offset the elevated costs.

This is a disappointing result, and we are hesitant about whether the company can win back margins once supply chain issues subside.

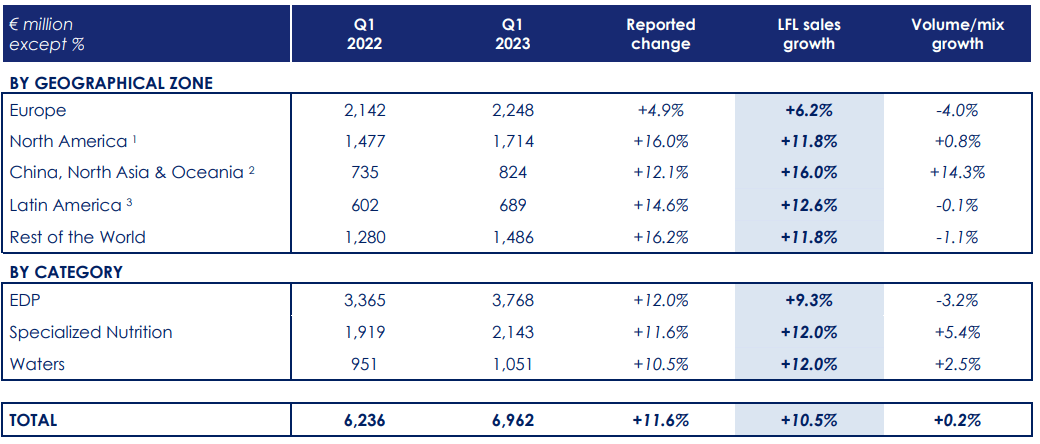

Q1 results

{kind=link}

Presented above is Danone's most recent quarterly results.

Danone has performed well in Q1, generating 10.5% LFL growth, with volume remaining positive. Further, growth has remained flat compared to Q4'22, suggesting no material slowdown QoQ.

Balance sheet

Danone's declining margins are reflected in its efficiency metrics, with ROE falling from a high of 19% to 6%.

Further, the company's inventory turnover has declined, as has its CCC. This is unlikely to cause a liquidity issue but represents a cash drag.

The company is conservatively financed, with a ND to EBITDA ratio of 2.3x. This affords Danone the flexibility to conduct further M&A should the opportunity arise.

Management's primary form of distribution is dividends, with payments growing at a rate of 4%. Danone's current payout ratio is 129% due to the poor net income in the current year.

The company currently generates c.€2bn FCF, which alongside its €4.6bn in cash should mean dividend growth is possible in the near term. This said, the fundamental sustainability is questionable until margins improve.

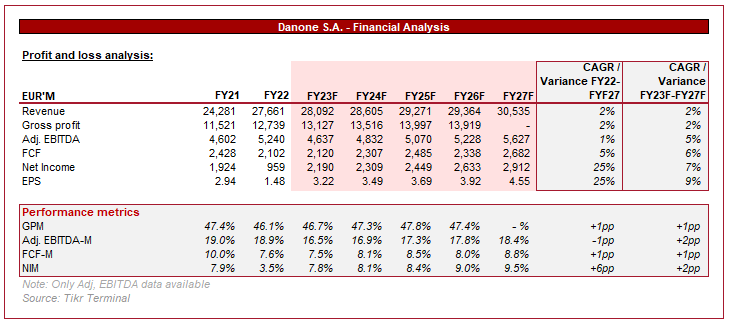

Outlook

{kind=link}

Presented above is Wall Street's consensus view on the coming 5 years.

Revenue is expected to grow at a CAGR of 2%, which is in line with what has been achieved historically. Our view is that the company has the scope to outperform this given the shift toward healthy consumption.

Further, margins are expected to remain flat, implying the business will be unable to recover what was lost in recent years.

Valuation

Danone valuation (Tikr Terminal)

Danone is currently trading at 11.2x LTM EBITDA and 10.3x NTM EBITDA.

This valuation is in line with its 10-year average, implying the company's fortunes have not materially changed.

The bull view would be that the transition toward healthier products should mean growth outperformance. Our view is that this is more than offset by the decline in margins. Danone's likely trading in the region of its fair value, if not slightly overvalued given the margin risk.

Final thoughts

Danone is a quality business with a fantastic range of brands. Given the products it sells, the company could feasibly grow at the long-term inflation rate forever. We like the company's product development and diversified revenue profile, but are concerned with its mediocre margins. With the company trading at its fair value, we rate it a hold.

For further details see:

Danone: Quality Business With Market-Leading Brands