DQ - Daqo New Energy: IRA Domestic Content Clarity Could Provide A Boost

2023-06-13 10:29:12 ET

Summary

- DQ offers an attractive risk-reward ratio here, since the stock remains well-supported at these levels since October 2020.

- The IRA domestic content tax credit clarity may also boost the polysilicon's lower ASPs while consuming the oversupply from China.

- Combined with the Mongolia plant potentially side-stepping the Xinjiang trade ban, we may see DQ's top and bottom lines improve from FQ2'23 onwards.

- Investors comfortable with moderate geopolitical risks may consider adding here for an upside potential of +46.6% to our price target of $59.70.

The DQ Investment Thesis Has Not Been Dismantled By Geopolitical Risk

We have previously covered Daqo New Energy (DQ) in April 2023, whose valuations continue to be compressed, attributed to the uncertain macroeconomic outlook, worsening geopolitical scene, and surplus in polysilicon supply. However, we believe the stock remains undervalued and has great tailwinds for recovery ahead.

DQ is easy to fall in love with, in our opinion, due to its depressed stock price, while also being well-balanced with its top and bottom line expansion thus far. Most importantly, the global cadence for decarbonization looks unstoppable through 2050, with renewables likely to comprise up to 44% of the US energy generation.

For example, DQ recorded revenue of $4.03B over the last twelve months (+49.8% sequentially), with expanding gross margins of 76.8% (+8.4 points sequentially). Their low-cost strategy is also reflected in the operating margins of 67.1% (+2.6 points sequentially), leading to stellar adj. EPS of $19.83 (+26.3% sequentially) at the same time.

These numbers also trump First Solar's (FSLR) gross margins of 8.1% (-13.9 points sequentially) and operating margins of -5.2% (-16.3 points sequentially) over the last twelve months, further highlighting DQ's labor cost advantage within China.

However, this is also the same reason why DQ faces geopolitical risks, given that the stock is a Chinese ADR, significantly worsened by its production location in Xinjiang, China, despite the ongoing diversification efforts to Mongolia. Its prospects are further impacted by the moderating Average Selling Prices of polysilicon to $12.62 per kg by June 7, 2023, compared to the $36.80 reported in December 2022.

This cadence is particularly attributed to the massive supply that flooded the market, impacting ASPs, a well-known risk for many other solar plays. DQ has guided a 205K MT production capacity by June 2023 ( +95.2% YoY ) and a total output of 195.5K MT by the end of 2023 (+46.1% YoY).

This is on top of the other five largest domestic players, including Tongwei and GCL Technologies, looking to further expand their total capacity to approximately 1.5M MT by 2024, nearly double China's production of 827K MT in 2022. As a result of the potential oversupply, the DQ stock has also lost -67.41% of its value at the time of writing, due to the bearish sentiments on its top and bottom line.

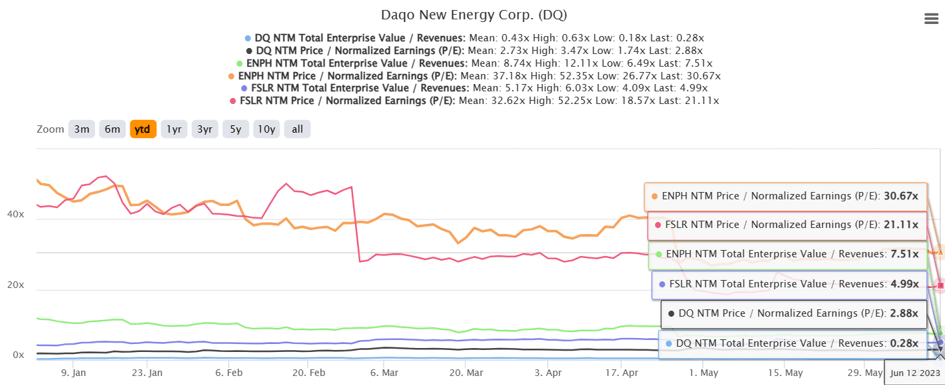

DQ YTD EV/Revenue and P/E Valuations

{kind=link}

Therefore, I believe it is unsurprising that DQ currently trades at an EV/NTM Revenue of 0.28x and NTM P/E of 2.88x, lower than its 5Y mean of 1.93x and 8.71x, respectively.

The same cadence has been observed with Enphase's (ENPH) valuations, though less severe, moderating to EV/NTM Revenue of 7.51x and NTM P/E of 30.67x, lower than its 5Y mean of 9.28x and 50.17x, respectively. The pessimism here is likely attributed to the sluggish transitionary period to NEM 3.0 in California , potentially impacting the demand in the US despite the potentially robust appetite from the EU.

On the other hand, FSLR valuations grew tremendously to EV/NTM Revenue of 4.99x and NTM P/E of 21.11x, way higher than its 5Y mean of 2.37x and 13.37x, respectively. The optimism embedded here is mostly attributed to its domestic production and its use of cadmium telluride technology, entirely bypassing polysilicon and any resulting geopolitical issues.

A highly strategic choice, in our opinion, already triggering the acceleration in the latter's ASPs, backlog, and footprint expansion in the US, especially aided by the Inflation Reduction Act [IRA].

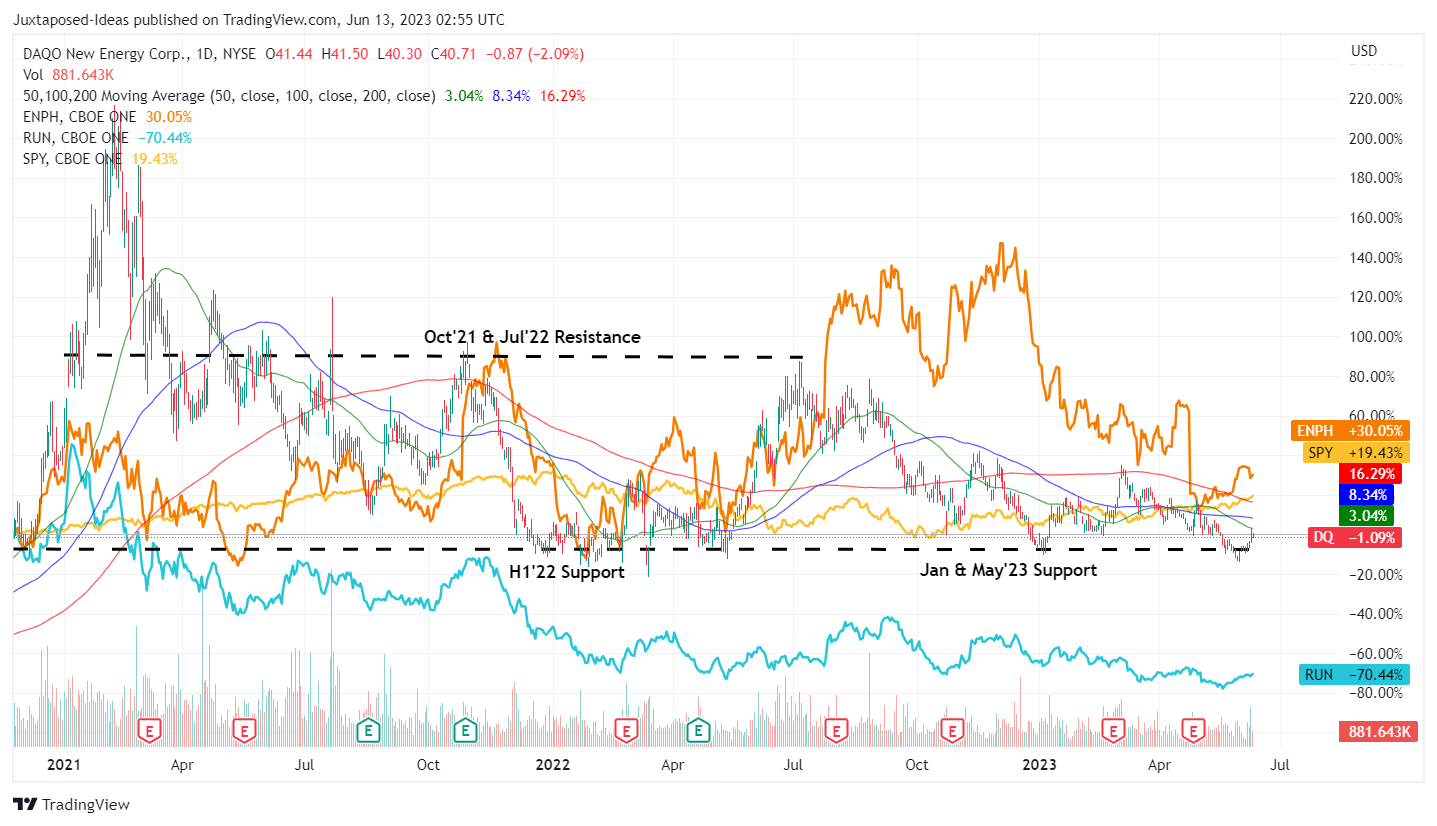

DQ 2Y Stock Price

{kind=link}

Pessimism has been observed in Daqo and Enphase's stock prices, with DQ and ENPH retesting their support levels as FSLR charts new heights. So, now that Daqo has been moderated to 3Y lows, is it a buy at these depressed levels? Our answer is yes, if the position is appropriately sized due to the geopolitical uncertainty.

DQ has already guided a diversification toward higher quality N-type polysilicon products, which commanded a premium spot pricing of approximately $12.84 per kg domestically, compared to the regular polysilicon spot prices of $10.62 per kg. For now, it is apparent that Chinese-made polysilicon continues to face a pricing headwind, compared to the overseas spot prices of $24.25 per kg.

Nonetheless, assuming that the made-in-Mongolia polysilicon is able to sidestep these headwinds, we may see the polysilicon maker's top and bottom line improve from here, on top of being exempt from the ongoing Xinjiang solar trade ban.

In addition, the US Treasury Department has released the confirmation that solar developers may claim up to 40% in tax credits through the IRA, allowing a maximum of 60% in solar components to be made outside the US.

This development may be a critical tailwind to DQ, since "the system's panels may contain cells made entirely with Chinese materials." This rule relaxation may then accelerate decarbonization at a time of polysilicon oversupply, negating the lower ASPs with higher volumes.

Therefore, with DQ's products likely to be cleared for export to the US, we may see demand improve from current levels, sustaining its top and bottom lines. Nonetheless, we must also warn investors that the pandemic-era levels of polysilicon spot prices are unlikely to return, due to the oversupply and economic downturn.

Market analysts already project an FY2025 EPS of $7.47, implying a drastic decline from FY2022 levels of $27.98. Then again, based on its normalized P/E of 8x, we still expect an upside potential of +46.6% to our price target of $59.70.

As a result of the attractive risk-reward ratio, we continue to rate DQ as a Buy here, especially since the stock remains well-supported technically at these levels since October 2020.

For further details see:

Daqo New Energy: IRA Domestic Content Clarity Could Provide A Boost