GLW - Daqo Vs. First Solar: Impacts Of A Potential Geopolitical Silicon War

2023-04-12 11:02:53 ET

Summary

- DQ's valuations continue to be compressed, attributed to the uncertain macroeconomic outlook, worsening geopolitical scene, and surplus in polysilicon supply.

- On the other hand, FSLR trades with a massive baked in premium, mostly attributed to its US based operations and zero reliance on polysilicon.

- FSLR's strategic decision is naturally prudent, entirely bypassing any potential geopolitically linked supply chain disruptions and human rights risks.

- However, while DQ may continue trading sideways in the intermediate term, we believe the stock remains undervalued and has great tailwinds for recovery ahead.

- Either way, the cadence of decarbonization remains unstoppable through 2050, with renewables likely to comprise up to 44% of the US energy generation then.

The Solar Investment Thesis

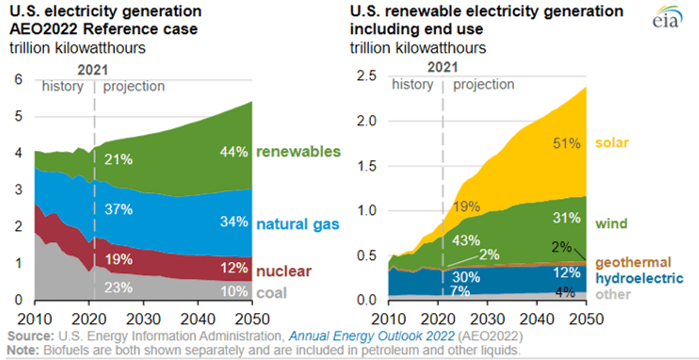

Solar Energy Share Of Energy Generation By 2050

{kind=link}

The US Energy Information Administration has projected a very bullish outlook for solar, expecting it may comprise up to 51% of renewable energies generated in 2050 and up to 22.44% of the total US generation by then.

It is apparent then that the availability of solar panel materials and technologies are key to achieving this decarbonization target, especially given the Biden administration's ambitious goal of net zero emissions in the electricity sector by 2035. For now, the US regulators are on track to approve up to 48 solar projects through 2025, with a total planned capacity of up to 29.59 GW then.

Due to this cadence, it is unsurprising that First Solar ( FSLR ) has reported a record high of 67.7GW in backlogs through 2029, with an improved Average Selling Prices [ASP] of $0.288 per watt.

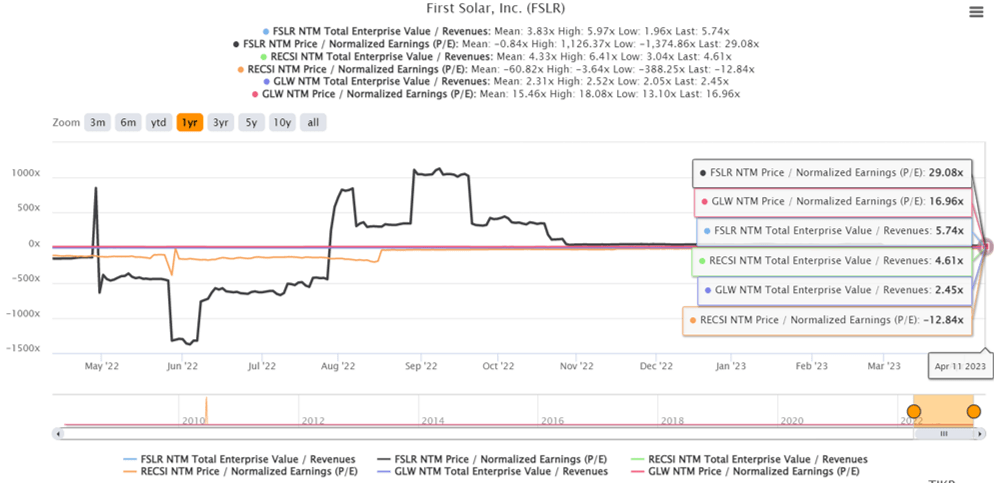

(US-Based Producers) FSLR, RNWEF, and GLW 1Y NTM EV/Revenue and NTM P/E Valuations

{kind=link}

This outperformance has naturally led to the massive premium baked in its stock prices, with FSLR recording NTM EV/Revenue of 5.74x, compared to its 3Y pre-pandemic mean of 1.22x and 1Y mean of 3.83x.

It is also important to highlight that the stock has always enjoyed elevated P/E valuations, at a 3Y pre-pandemic mean of 45.45x. While its NTM P/E has been moderated to 29.08x at the time of writing, the differential factor is naturally attributed to the massive upgrade in its profitability, from $1.48 in FY2019, -$2.79 in FY2022, to the projected $20.54 in FY2025.

Based on that figure and normalized 3Y P/E mean of 10.46x, we are looking at a moderate price target of $214.84, suggesting a minimal upside potential from current levels. Otherwise, based on its NTM P/E, it seems that FSLR has a tremendous potential for doubling to $597, though somewhat ambitious attributed to the uncertain macroeconomic outlook.

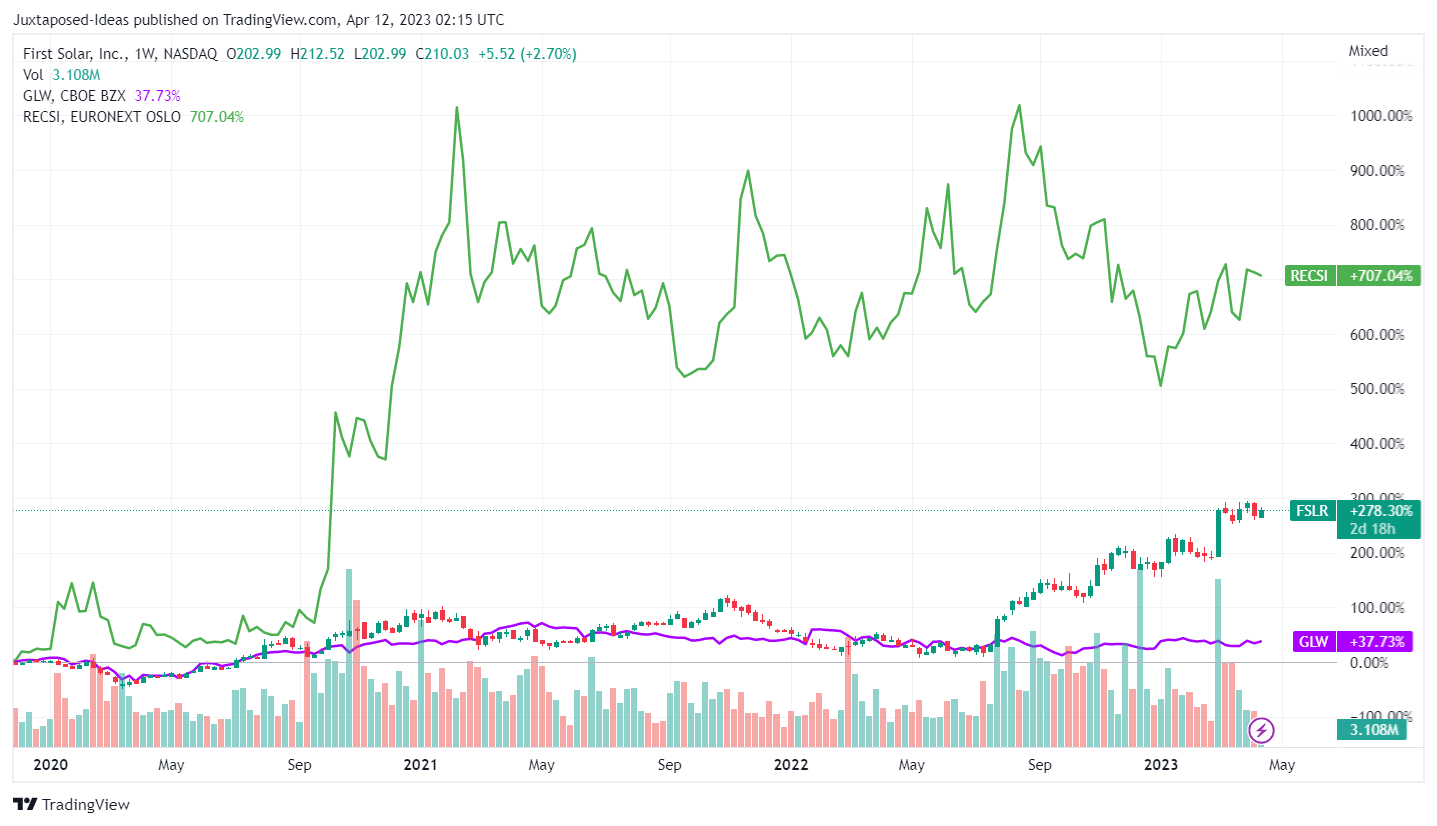

FSLR, RECSI, & GLW 3Y Stock Price

{kind=link}

Meanwhile, FSLR utilizes cadmium telluride technology, entirely bypassing polysilicon , allowing the company to reduce any potential impact from geopolitically linked supply chain disruptions and human rights risks from Xin Jiang, China. The firm utilizes the mineral as the absorption layer for its modular semiconductor film, which reportedly also offers improved system performance.

Combined with the fact that FSLR plans an aggressive expansion in its manufacturing capacity in the US (thanks to the Inflation Reduction Act), it is unsurprising to see its impressive +173.6% rally since July 2022.

The same optimism has also been observed in its other polysilicon peers with US-based production capacities, such REC Silicon ( OTCPK:RNWEF ) and Corning (NYSE: GLW ). RNWEF's NTM EV/Revenue has been visibly upgraded to 4.61x as well, compared to its 3Y pre-pandemic mean of 1.47x and 1Y mean of 4.33x, with GLW's valuations remaining consistent at 2.45x thus far.

Market analysts are already expecting both companies to record improved top and bottom line growth at 63%/73.5% and 2.9%/22.3% through FY2024, respectively, attributed to the robust demand ahead.

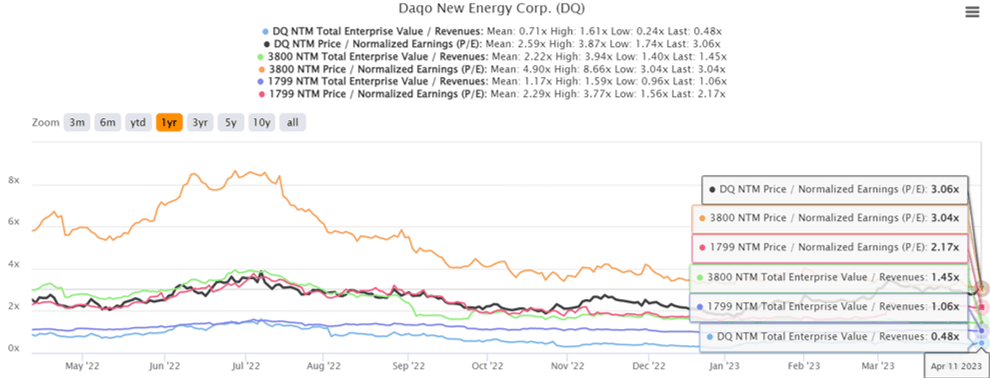

(China-Based Producers) DQ, GCL, and Xinte 1Y NTM EV/Revenue and NTM P/E Valuations

{kind=link}

The same unfortunately cannot be said about Daqo New Energy Corp. ( DQ ), since it produces 132K MT of polysilicon in Xin Jiang, China as of 2022. This led to the compression in its NTM EV/Revenue of 0.42x and NTM P/E of 2.81x, compared to its 3Y pre-pandemic mean of 1.69x and 9.01x, respectively.

The pessimism in DQ's stock valuations is not surprising, given that China commands the majority of solar-grade polysilicon supply at 88% (+6 points YoY) in 2022, with Xin Jiang comprising more than half of the global capacity.

Due to the ongoing ban of solar exports from Xin Jiang attributed to " human right issues ," the prospects for producers who relies on polysilicon are mixed ahead, as similarly seen in the moderated valuations of GCL Technology Holdings Limited (3800) and Xinte Energy Co (1799).

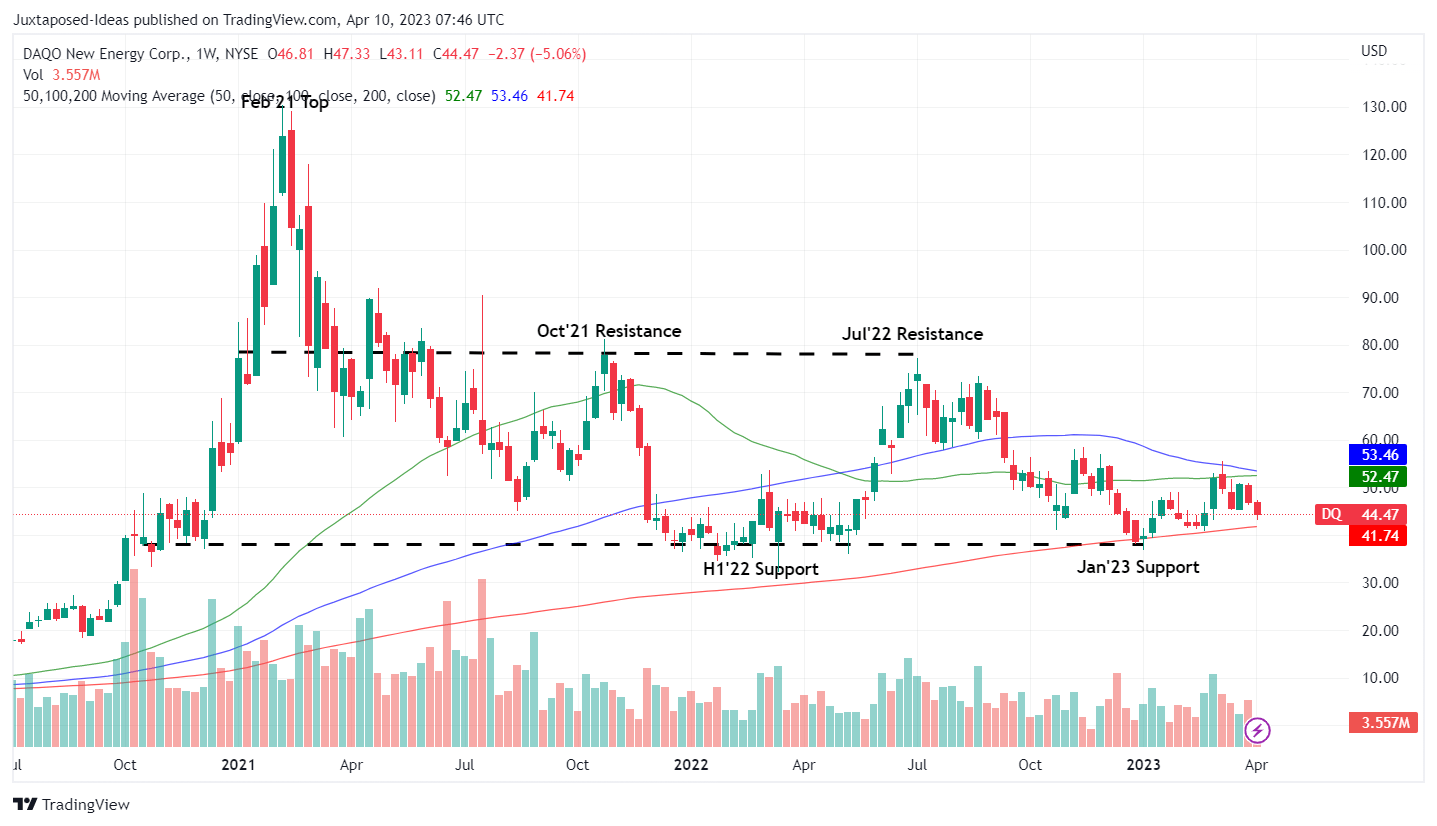

DQ 3Y Stock Price

{kind=link}

For now, DQ has been trading sideways over the past few months, retesting its previous H1'22 support and successfully rebounding in January 2023. Naturally, the geopolitical risks have caused the stock to trade below its book value of $310.53 and our projected price target of $57.60, based on its 3Y normalized P/E mean of 7.59x and its projected FY2025 EPS of $7.59.

On the other hand, China has recently banned the export of their large silicon, black silicon, and cast-mono silicon technologies often used in the manufacturing of low cost polysilicon used in solar power generation.

With 305K MT (+131% YoY) of total polysilicon capacity by the end of 2023, we reckon DQ's top and bottom line prospects remain excellent. Lan Tianshi, the CEO of GCL Technology (as the world's second-largest polysilicon manufacturer) has optimistically projected the recovery in polysilicon prices to between $17 and $20 in 2023. This is compared to H2'22 average of $11.50 and 2022's peak of $39:

Polysilicon makers will return to a relatively normal profit margin this year as the unbalance between supply and demand begins to ease. ( Bloomberg )

Even if geopolitical relations worsen between the US and China, we reckon DQ's prospects remain excellent in serving the world's massive polysilicon appetite, which is expected to reach 315 GW (+17.5% YoY) in 2023.

We reckon the robust demand may be further boosted by the recent OPEC+ cut , which has triggered the sharp rise in Brent oil prices to $84.75 at the time of writing, compared to the March 2023 bottom of $72 and the pre-pandemic average of $65. Furthermore, the Bloomberg Consensus already projects normalized Brent prices of up to $96 in 2023, while averaging at $85s through 2026, potentially incentivizing further investments in renewables ahead.

China's Key Role In The Global Electrification Movement

Bruegel

Furthermore, the global electrification supply chain remains highly dominated by China, commanding the majority of material processing/ refining, intermediate manufacturing, and final assembly in 2021, based on the Bruegel market report released in April 05, 2023.

While FSLR may not have any operations in the country, its supply chain may be similarly impacted by future trade restrictions on materials/ equipment/ technology transfer imposed by either China or the US, impacting its forward execution.

For example, China is now deliberating a ban of rare earth export , potentially impacting the global solar panel market ahead, since the country produced 70% of the world's rare earths. While other countries have been trying to shore up their supply chain and reduce their reliance on Chinese exports, it remains to be seen how the US plans to proceed with its electrification plan, due to the critical importance of rare earth to the global decarbonization cadence.

Therefore, we reckon that geopolitical risks remain an inherent concern for both stocks, though rather heavily weighted on DQ compared to FSLR. This explains DQ's headwinds in its intermediate term prospects, depending on how things develop ahead.

However, here is where opportunistic investors may try to take advantage of DQ's compressed valuations, by adding a small/ speculative position in their portfolios, due to the importance of polysilicon in the 2050 decarbonization cadence.

Furthermore, assuming a rerating in its P/E valuations to 15x (nearer to its pre-pandemic highs and halfway to FSLR's), we may see the former's price target further upgraded to $110, suggesting an excellent upside potential of +147.3% from current levels.

This is not overly bullish in our opinion, since DQ has expanded its footprint to Inner Mongolia, potentially bypassing any human right risks specifically from Xin Jiang. Since the regulations for exports of polysilicon remain unchanged at the time of writing, we may see further tailwinds for the polysilicon manufacturer since it expects to produce up to 173K MT in the neutral region by 2023, likely exempted from the US solar tariffs.

Given China's plan of achieving net zero by 2060 through 5.8 TW of renewables, the country has also been aggressively expanding its investments in solar and wind energies, potentially achieving 1.5 TW of renewables by 2025, accelerated compared to its original plan by 2030. Therefore, even if DQ only serves the Chinese market, the solar company may still thrive moving forward.

The same may be observed with FSLR, attributed to the US's target of achieving 80% of renewable energy generation by 2030 at approximately 4.1 TW, based on 2022's consumption of 3.9 TW and a sustained CAGR of 3.5%. Naturally, the country still has a long way to go, since the current renewables capacity (solar and wind) only delivers approximately 212 GW in 2022 .

Nonetheless, since FSLR is trading at fair value, we reckon investors that add here may have a reduced margin of safety for long-term portfolio growth. Therefore, we recommend interested investors to exercise some prudence and wait for this optimism to be slightly moderated ahead.

For further details see:

Daqo Vs. First Solar: Impacts Of A Potential Geopolitical Silicon War