DRI - Darden Remains Solid But Isn't Immune To Industry Trends

2023-10-24 11:21:41 ET

Summary

- Darden Restaurants has recently acquired high-end steakhouse Ruth's Chris for $715 million in an all-cash deal.

- DRI's FQ1 results showed another solid performance, as the company remains an industry leader.

- However, DRI's stock is currently trading near the top of its pre-pandemic valuation range and there are risks that the consumer could pull back on eating out.

Back in February , I wrote that Darden Restaurants ( DRI ) had been doing a great job of navigating a difficult food inflation environment, but I thought the macro could impact the dining out as the year progressed. The stock has generated about a breakeven return versus a 6% gain in the S&P 500 since that write-up. Let’s take a closer look at the stock.

Company Profile

As a refresher, DRI owns and operates several full-service restaurant concepts. It breaks out its results in 4 segments: Olive Garden, LongHorn Steakhouse, Fine Dining, and Other Restaurants.

DRI's largest concept is Olive Garden, an Italian eatery with over 900 owned and operated locations that represents about 45% of its sales. LongHorn Steakhouse is its second largest concept, with just over 560 locations accounting for nearly 25% of its sales.

The Fine Dining segment consists of DRI's Capital Grille and Eddie V's concepts, as well the recently acquired Ruth’s Chris. The three brands carry much higher checks than DRI’s other brands.

DRI's Other segment includes several full-service restaurant chains, including Cheddar's Scratch Kitchen, Yard House, Seasons 52, Bahama Breeze, and The Capital Burger. Cheddar's is the largest concept in terms of number of locations with over 180 at the end of August.

Ruth's Chris Acquisition and FQ1 Results

The biggest news since I last looked at DRI was its acquisition of high-end steakhouse Ruth’s Chris for $715 million in an all-cash deal that closed in June. The deal was done at about a 9.4x 2022 adjusted EBITDA multiple, with the restaurant having about $500 million in sales and $76 million in adjusted EBITDA.

At the time of the deal, Ruth's Chris has 155 locations, including 81 company owned or operated and 74 franchises. With an average check just below $100, the restaurants have average unit volumes of $6.2 million with restaurant levels margins of about 19%.

DRI’s recent track record of solid performance continued with its FQ1 results, with revenue increasing 11.6% to $2.73 billion, topping analyst estimates calling for sales of $2.71 billion. EPS of $1.78 beat the consensus by 4 cents. Adjusted EBITDA rose to $388 million.

Olive Garden sales rose 8.6%, while its segment profit climbed 21.4% to $262.3 million. Same-store sales rose 6.1%.

At LongHorn Steakhouse, revenue jumped 10.8% on an 8.1% increase in comparable-store sales. Segment profit increased 27.6% to $117.4 million.

Fine Dining revenue soared 49.1%, helped by the addition of Ruth’s Chris. Comparable-restaurant sales, however, fell -2.8%, and don’t include Ruth's Chris. Segment profits rose 32.3% to $39.7 million. Other Business revenue, meanwhile, jumped 6.1% on a 1.7% increase in same-restaurant sales. Segment profit rose 16.6% to $84.3 million.

Looking ahead, the company guided for full-year adjusted EPS of between $8.55-8.85.

Asked about the current macro environment of its FQ1 earnings call , CEO Ricardo Cardenas said:

“Overall, we think the consumers continues to be resilient but there seems to be a little bit more selective. We are seeing a little softness versus last year with household incomes above $125,000 and that primarily affects our fine dining brands but it does affect all of our brands. Now this could be because the increase in luxury travel, particularly international travel, which you've heard a lot of people talk about. But as I've said before, many times, there is attention to really what people want to pay and what they can afford and they're going to continue to seek value, not always about low price. They're making trade-offs and food away from home is one of the most difficult things they can give up. So again, what does that mean for our brands? We believe that operators who deliver on their brand promise and value will continue to appeal to consumers. And so we're going to keep doing that. We're going to deliver our promise. We're going to execute our brands and we're going to keep doing that and deliver value to our guests. And I'm confident we're well positioned for whatever we have to deal with. Thanks to the breadth of our portfolio and the outstanding team members in our restaurants who are committed to exceptional guest experiences.”

The company noted that about 22% of its commodity costs come from beef, which it said remains elevated with supplies down. It said some additional imports could lower costs, but it was too early at this point to tell if it would help lower prices.

DRI has continued to perform well despite some macro softness, although recent data does show that restaurant growth and traffic began to slow starting in August. DRI’s Olive Garden and LongHorn concept generally outperform, but they are not totally immune to industry trends.

The Ruth’s Chris acquisition looks like a nice fit into its fine dining segment at a decent price. Fine Dining has a bit different drivers than more casual restaurants, often following corporate spending trends, so we'll see how the near term timing with the acquisition plays out, as many corporations have begun tightening their budgets.

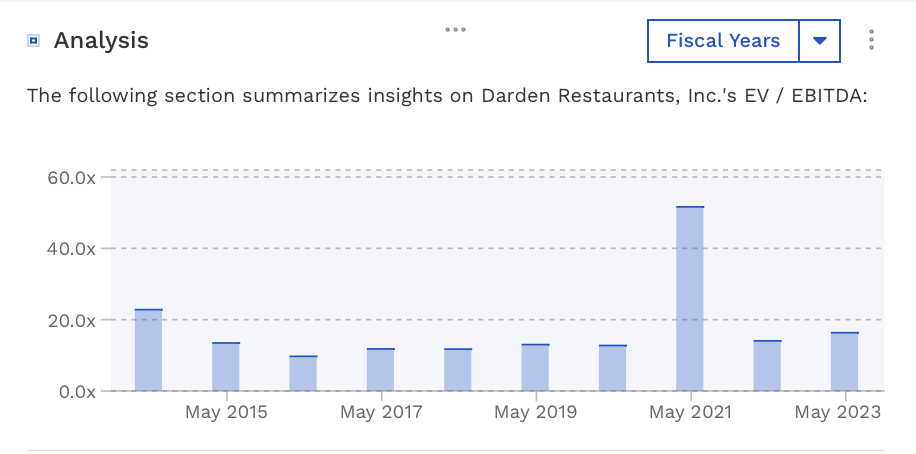

Valuation

DRI currently trades around 13.4x the FY 2024 (ending May) consensus EBITDA of $1.78 billion and 12.5x the FY25 consensus of $1.90 billion.

From an EBITDAR perspective, its trades at an 11x FY2024 multiple and 10.4x FY 2025.

It trades at a forward PE of 16.1x the FY24 consensus of $8.79 and 14.7x the FY25 consensus of $9.62.

The company is projected to grow revenue 10.3% in FY24 to $11.6 billion and 5.5% in FY25.

Its valuation is considerably higher compared to rivals like Bloomin' Brands ( BLMN ), which trades at an EV/EBITDA multiple of 7.3x 2024 EBITDA, and Dine Brands ( DIN ), which trades a 9.0x. Texas Roadhouse ( TXRH ), meanwhile, trades at around 12.0x 2024 EBITDA.

The stock historically often traded between 10-13x trailing EBITDA before the pandemic. As such, I think the stock looks fairly valued to slightly overvalued based on historical valuations and its premium to peers.

{kind=link}

Conclusion

DRI continues to be a solid performer, however, with the stock still trading near the top of its pre-pandemic valuation range, I continue to think the stock is close to fairly valued at the very least. There also remains the possibility that the industry slumps if the macro worsens. Right now, consumers have remained pretty resilient, but the Fed continues to seemingly want to raise rates to push inflation down and cool the economy.

Overall, the biggest risk to DRI at the moment appears to be a shift in the consumer and dining out trends. If this happens in a significant manner, I’d expect to see multiple compression towards the lower end of its pre-pandemic range, as well as estimates to come down, which could put the stock under $100. My base case, though, is a more moderate change in consumer trends at the moment. As such, I remain “neutral” on the stock.

For further details see:

Darden Remains Solid, But Isn't Immune To Industry Trends