DRI - Darden: Stable SSS Over The Next Few Quarters Should Drive Multiples Reversion To Mean

2023-10-03 06:31:57 ET

Summary

- I reiterate my buy rating, with the expectation that Darden's valuation will return to average as it outperforms peers.

- DRI's impressive performance in 1Q24, with substantial sales growth and outstanding SSS figures, suggests a return to stable seasonal trends, despite challenges in fine-dining.

- The return of the "Never Ending Pasta Bowl" promotion and pricing growth aligned with inflation contributes to near-term SSS stability.

Overview

My recommendation for Darden Restaurants ( DRI ) is a buy rating, as I expect valuation to revert back to average as the market recognizes that DRI is a much better business relative to peers when it continues to print stable SSS and growth in the next few quarters. Note that I previously gave a buy rating for DRI due to my belief that DRI will see a return to more typical growth in EPS going forward. Which, when combined with the dividend yield of 3%, could yield 16% IRR returns over the near term.

Recent results & updates

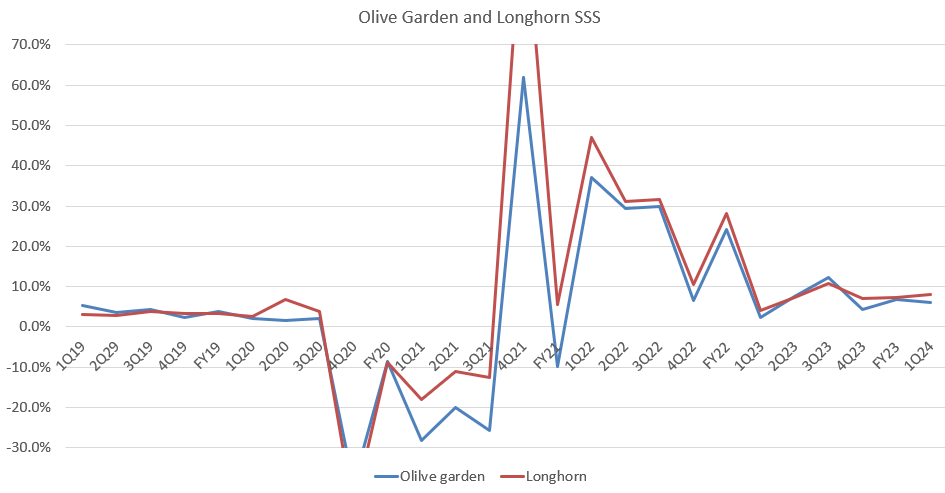

During 1Q24, DRI did exceptionally well, in my opinion. Compared to the 6.4% growth seen in 4Q23 and the 6.1% growth seen in 1Q23, quarterly sales grew by almost 12%. Olive Garden and Longhorn both played a significant role in driving sales. Overall same-store sales growth of 5% was also remarkable, as it implies that DRI gained 90 basis points of share during the quarter (the industry grew SSS by 410 basis points as per the 1Q24 earnings call). When comparing the industry growth to Olive Garden and Longhorn, the distinction deserves credit as well: Olive Garden SSS was 6.1% and Longhorn SSS was 8.1%, both outpacing the industry level by a huge margin. However, not everything was rosy; the fine-dining segment posted a 2.8% decline, which was largely attributable to a combination of factors including higher prices and weaker spending by consumers in the $125,000+ income bracket.

Nonetheless, DRI appears to be reverting back to seasonal trends. If we look at the historical SSS of the 2 key brands, Olive Garden and Longhorn, we can see that SSS has been gradually trending downwards back to the mid-single digit region. This clearly suggests that the post-COVID recovery dynamic is over and volatility from the inflationary environment is stabilizing.

{kind=link}

The management's positive remarks about the health of their customers at the flagship casual dining establishments (Olive Garden and Longhorn) were also supportive of my expectations that SSS should be stable. Importantly, in the call, management showcased their long-term thinking, in which they won't give discounts to meet short-term guidance or expectations. This is crucial because discounts are effective in the short term but can backfire if they become ingrained in customers' minds.

…Overall, we think the consumers continues to be resilient… Our marketing programs, we told you what we're going to do with marketing in the prepared remarks. It's going to -- whatever we do is going to elevate brand equity, it's not going to be deep discount and it's going to be simple to operate. And if it means that our traffic is at the lower end of our guide, then it's at the lower end of our guide. We're not going to do things that are going to impact us in the long term, just for short term. From: 1Q24 earnings call

As for the future, I do not anticipate a significant uptick in sales, but I do anticipate SSS to at least hold steady at the current level, as the "Never Ending Pasta Bowl" promotion will return in 2Q24 and is expected to be there for a total of 8 weeks, which is 1 week more than the 7 weeks seen in 2Q23. In addition, management also noted that pricing growth should mirror inflation. Given the current inflation rate, near-term SSS should be well supported by pricing (inflation-driven).

Valuation and risk

Author's valuation model

According to my model, DRI is valued at ~$163 in FY24, representing a 14% increase. This target price is based on my stable growth forecast of 10% over the next 2 years, as I expect DRI to grow at normalized SSS levels, supported by management's active focus on marketing. While some might argue that growth could accelerate (which I don't disagree with), I still think it is safer to be more conservative as the current macro environment is not out of the woods yet. I also expect the margin to stay at a similar level, as management has clearly communicated that they are not going to provide deep discounts to drive sales.

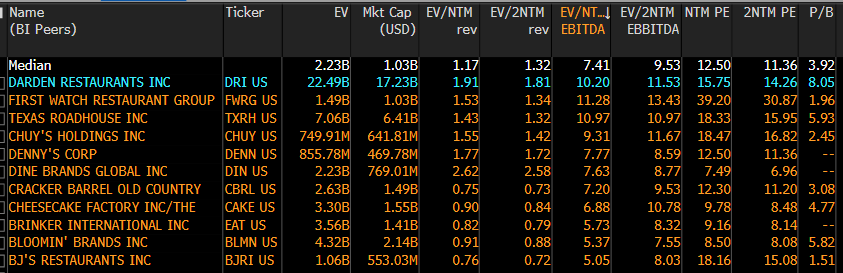

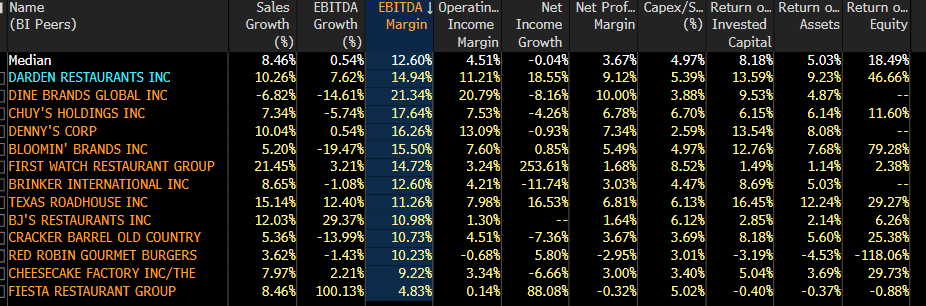

DRI is now trading at 10x forward EBITDA, which I believe will rise gradually as the market recognizes that DRI is a much better business than peers (similar growth profile but better margin metrics). DRI has had a tight trading range of 9.3x to 12x over the past few years and has recently dipped to 10.2x. I believe the negative reversion was due to the entire industry seeing a negative revision, which I don't think is fair as I expect DRI to recover over the next few quarters. Hence, I expect valuation to return to the historical average of 11x.

{kind=link}

{kind=link}

Even though DRI is a better business based on several metrics relative to peers, it is not spared from being disrupted by a weak macroeconomy. Suppose a major recession were to occur, I would not expect DRI to be able to sustain its SSS. In fact, SSS should turn negative due to lower traffic, as should its EBITDA margin, given the high fixed-cost nature of the business.

Summary

I maintain my buy rating for DRI based on the expectation that its valuation will revert to the mean. DRI's strong performance in 1Q24, particularly with impressive sales growth and remarkable same-store sales figures, is commendable. While challenges exist, such as the decline in the fine-dining segment, DRI appears to be returning to stable seasonal trends, indicating the stabilization of post-COVID recovery dynamics. Management's commitment to a long-term marketing strategy without deep discounts aligns with my expectations for stable same-store sales. Looking ahead, the return of the "Never Ending Pasta Bowl" promotion in 2Q24 and pricing growth in line with inflation should support SSS stability.

My valuation model suggests a target price of approximately $163 in FY24, reflecting a 14% increase. DRI's current trading multiple of 10x forward EBITDA is expected to rise as the market recognizes its strength relative to peers.

For further details see:

Darden: Stable SSS Over The Next Few Quarters Should Drive Multiples Reversion To Mean