DRKTY - Darktrace: Substantially Cheaper Than Peers

2023-12-20 02:19:17 ET

Summary

- Darktrace came to market cheaper than its peers and remains so.

- However, its performance, although good in an absolute sense, lags some cybersec peers.

- The peculiarity here is the short thesis out on the company, which may affect trading dynamics, and limit institutional take-up for the time being.

- It could also partially explain the extent of the current differences in multiples.

- However, we see that Darktrace is performing in line with the ordinary, and think that the short thesis isn't even the primary reason to eschew the stock if being conservative.

Darktrace ( DRKTF ) is an interesting company and story. It trades much more cheaply than other cybersecurity players like SentinelOne ( S ) and Palo Alto Networks ( PANW ), but it also has a short thesis out on it that might be the reason for the stock to still be weighed down. While we pay attention to the short thesis, we note that the current performance trends are very much in line with a company line SentinelOne and the industry as a whole is growing. However, if this company underperforms it would be difficult to explain to fiduciaries, which could be an issue for institutional support.

Earnings

Let's have a look at the IS snapshot.

{kind=link}

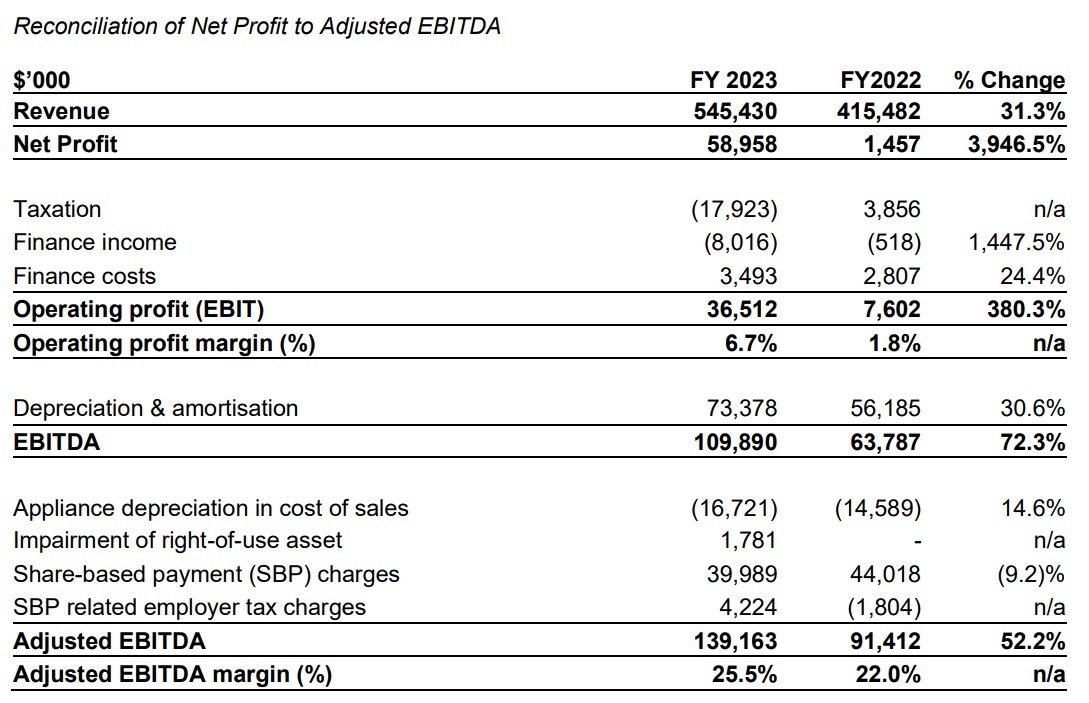

Revenue growth is pretty solid at over 31%, which is around the mid-double-digit growth seen by peers like SentinelOne which we also covered recently . ARR growth is a little shorter than sales, and a little shorter than at S1, which means there is less momentum to Darktrace's sales growth compared to S1.

The sales growth is contributing to higher margins, with good EBIT evolutions and a very solid ongoing gross margin. FCF is also strong, with the only major cash outflow coming from pretty major share buybacks that were done in response to the QCB short attack. EBIT levels are much higher than peers, although that's because of a somewhat worryingly low R&D expense line relative to revenues compared to peers, of around 10% compared to more than 30% at peers.

ARR per customer growth was a little weaker than at S1 compared to headline figures, and S1 was already understating their figures a lot due to growth in MSSP channels and their large relevance to begin with.

In general, Darktrace isn't quite as premier in terms of performance as S1.

Short Thesis

The valuation for Darktrace is much lower than competitors, more than 4x EV/Sales compared to around 10x for US peers. The YTD performance in price was also quite a bit worse than S1, and in general, this might be due to the short thesis, although we should mention that Darktrace came to the market quite a bit cheaper in 2021 than the other companies as well, before the short thesis was published.

The short thesis reads a little like this:

- Accusations of channel stuffing and other irregularities around booking sales. Something we can't do anything to verify.

- Concerns around connections of Darktrace management and original funding to fraudsters, both alleged and convicted, in the Autonomy sales to Hewlett-Packard 9HPE0.

- They also complain about falling deferred revenue compared to overall sales despite the fact that these are subscriptions that they are selling.

Honestly, we aren't that worried about the short thesis. Irregularities were concentrated in the period prior to IPO. The stuff about using marketing events to compensate customers for subscriptions that they were forced to offtake is something we cannot confirm, so it's a concern. The connections to convicted criminals around the Autonomy financial fraud are worrying mainly for the current trading dynamics and headline risks, where a pending extradition Mr. Lynch of Autonomy provided some of the initial funding for Darktrace, and top executives at Darktrace were also at Autonomy in the past. Apparently, the deferred revenue matter, also defended by sell-side analysts, squares with evolving industry practices of selling shorter subscriptions.

Bottom Line

Ultimately, the short thesis is a concern as it affects the trading dynamics and may limit institutional support, particularly this taint from Autonomy where distance really needs to be created. However, Darktrace's current performance isn't out of the ordinary, including its stock price performance, despite having this idiosyncratic overhang. There may be more concerns around persistently low R&D. That is something we'd focus on. And the valuation isn't tiny either, even if there are at least profits to show, with the valuation above 20x EV/EBITDA. It's a competitive industry, and everyone wants to provide the most comprehensive solution possible and cross-sell products. We'd pass on Darktrace, we don't see a great angle here. The outstanding short thesis doesn't help but we still wouldn't love it.

For further details see:

Darktrace: Substantially Cheaper Than Peers