DASTY - Dassault Systèmes SE: Robust 3Q And Strategic Initiatives Signal Promising Future Growth

2023-10-28 03:31:11 ET

Summary

- DASTY exceeded revenue and profitability benchmarks in Q3 2023, with growth across all regions and product segments.

- The company's Industrial Innovation Software segment stood out, accounting for 54% of software revenue and showing double-digit growth.

- DASTY is undergoing a transformative shift to an experience-centric approach, emphasizing the Virtual Twin technology for industry innovation.

Overview

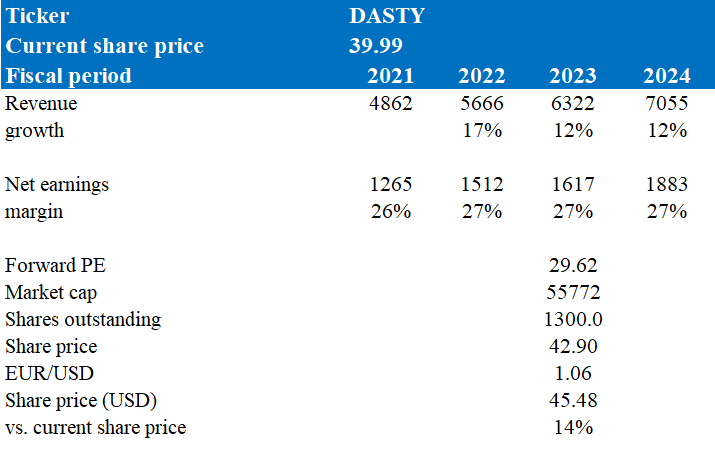

Note that I previously rated Dassault Systèmes SE (DASTY) with a hold rating due to the expectation that DASTY would revert to its historical growth trajectory and if it could meet its guidance for the third quarter of 2023. Impressively, for this quarter, DASTY outperformed, exceeding benchmarks in both revenue and profitability. Growth was evident across all geographical regions. On the product spectrum, every segment witnessed expansion, notably the Industrial Innovation Software segment, which registered a double-digit growth rate. In essence, DASTY's robust results surpassed both my expectations and their own internal guidance. My updated model now suggests a promising upside potential of 14%. Given these encouraging factors, I am revising my rating and now recommend a buy rating for DASTY, a change from my earlier hold rating.

Recent results & updates

In the third quarter of 2023 , DASTY showcased a commendable performance, exceeding expectations in both revenue and profitability metrics. Their software revenue witnessed a notable surge, increasing by 12%, which not only met but exceeded their set targets. This growth was further complemented by a robust 18% rise in subscription revenue. The company's financial health was further underscored by an operating margin that reached 31%. Additionally, the EPS, a key indicator of profitability, climbed by 20% when adjusted for constant currency fluctuations. These strong financial results have optimally positioned DASTY for the entirety of the fiscal year, reflecting the company's resilience and growth potential in the market.

During the third quarter, DASTY experienced varied growth across different geographical regions . In Europe, the company saw a significant uptick, with revenues growing by 21%. This growth was broad-based, indicating widespread acceptance and adoption of their offerings across the continent. Over in the Americas, the company registered strong performances across multiple sectors, further solidifying its presence in the region. Meanwhile, in Asia, the growth was more modest, at 5%. This was buoyed by a double-digit growth rate in India and a commendable performance in Japan. However, there were some soft spots, with Korea showing some sluggishness. Notably, despite challenging macroeconomic conditions in China, the company managed to demonstrate resilience, registering 6% growth in the country.

On the product front, the company's Industrial Innovation Software segment stood out, registering an impressive 18% growth and accounting for 54% of the total software revenue. This growth was driven by the company's flagship brands, with CATIA, SIMULIA, ENOVIA, DELMIA, and NETVIBES all showing double-digit growth during the period. In the Life Sciences domain, software revenue experienced a growth of 3%. MEDIDATA, a key player in this segment, achieved mid-single-digit growth in cloud subscription revenue. This growth, however, was set against the backdrop of a strong comparison base. Yet, there were bright spots, such as the significant growth in areas like decentralized clinical trials with MEDIDATA Patient Cloud, which is seen as a transformative approach shaping the future of clinical trials. Lastly, in the mainstream innovation segment, SOLIDWORKS recorded a growth of 7%. The transition of SOLIDWORKS to a subscription model was particularly noteworthy, accelerating at a high double-digit rate. This shift was primarily driven by the release of the 3DEXPERIENCE cloud-based solutions and options.

DASTY is undergoing a transformative shift, transitioning from a product-centric approach to an experience-centric one. This strategic move is not just about offering products but about delivering holistic experiences to their clients. Central to this strategy is the company's unique positioning with the Virtual Twin. This technology is not just a tool but a significant driver for future growth, enabling clients to simulate, visualize, and optimize their operations in a virtual space before implementing them in the real world. The company emphasized the shift from tangible assets to software, highlighting the automotive industry's transition towards software-defined vehicles as a prime example of this trend. This shift underscores the increasing value of software in driving innovation and operational efficiency across industries.

Furthermore, the company highlighted the importance of the Virtual Twin in their strategic roadmap. These virtual replicas cover the entire product life cycle, from inception to disposal, providing unparalleled insights and optimization opportunities. The company believes that the Virtual Twin's capabilities will be pivotal in reshaping industries, driving innovation, and delivering enhanced value to their vast customer base. This strategic focus is not just about powering DASTY's growth but is aimed at delivering significant value to their clients, helping them navigate the complexities of their respective industries with greater precision and foresight.

Valuation and risk

According to my model, my target price for DASTY is $45.48 in FY24, representing a 14% increase. This target price is based on my growth forecast of the high teens over the next two years, with FY23 growth of 12% deriving from management's midpoint guidance provided during the earnings call. The rationale for my assumption is based on its commendable performance in the recent quarter, surpassing expectations in both revenue and profitability metrics. Their growth was evident across various regions, with Europe leading the charge, indicating widespread adoption of their offerings. The Americas and Asia also demonstrated resilience and adaptability, further solidifying the company's global market presence.

On the product front, DASTY's Industrial Innovation Software segment and flagship brands stood out, indicating their leadership in the market. The company's strategic shift from a product-centric to an experience-centric approach, emphasizing the Virtual Twin technology, positions them at the forefront of industry innovation. This focus on delivering holistic experiences and the transition from tangible assets to software underscores the company's commitment to driving innovation and delivering enhanced value to their vast customer base.

{kind=link}

Currently, DASTY's forward Price/Earnings ratio is 29.62x, aligning with the median Price/Earnings of its peers. This valuation seems reasonable, especially when considering that DASTY's EBITDA margin and net margin slightly surpass the median of its competitors. However, it's worth noting that DASTY's projected growth rate for the next twelve months in 2024/2023 is 9%, which is a tad behind the peers' median of 11%. Based on DASTY's current forward Price/Earnings, my target price for the stock is 14% higher than its present trading price. Given these factors and the tailwinds discussed above, I recommend a buy rating for DASTY at this juncture.

{kind=link}

One potential downside risk to my buy rating for DASTY is its projected growth rate for the next twelve months, spanning 2024/2023. At 9%, this rate is behind the median of its peers, which stands at 11%. Furthermore, while DASTY has provided guidance for FY23 with 12% growth using the midpoint of their guidance range, the management has also narrowed the range for total revenue. This adjustment in growth expectations could suggest potential hurdles in scaling or seizing market share in the forthcoming period. Such challenges could subsequently affect the company's future profitability and stock value. If rival firms persist in outpacing DASTY's growth, it may encounter heightened competition, which could jeopardize its market standing and revenue prospects.

Summary

DASTY's recent performance in the third quarter of 2023 has been exemplary, surpassing both revenue and profitability expectations. The company's software revenue and subscription growth have been impressive, underscoring its strong financial health. Geographically, DASTY has seen significant growth in Europe and maintained a robust presence in the Americas. Their product segments, especially the industrial innovation software, have shown remarkable growth, driven by flagship brands. Strategically, DASTY is transitioning to an experience-centric approach, emphasizing the transformative potential of the Virtual Twin technology. This technology promises to revolutionize industries by offering unparalleled insights throughout the product lifecycle. With a target price indicating double-digit upside potential, the compelling growth trajectory and strategic positioning make a compelling case for a buy rating for DASTY.

For further details see:

Dassault Systèmes SE: Robust 3Q And Strategic Initiatives Signal Promising Future Growth