DASTY - Dassault Systemes: Decent Performance But Definitely More Of A 'Buy' In 2023

Summary

- I wrote about Dassault in late 2022, calling this one a decent "BUY" for the conservative investor despite a very low yield.

- I believe the prospects for the company are good enough to justify looking at the 3-5 year upside here.

- In my 2023 update for the company, I will show you why I believe the company is still an excellent "BUY", despite a decent 6.4% performance since December.

Dear Readers/Followers,

First off, this a reminder, because I did receive some inquiries after writing on Dassault last time. I'm not talking about the French Company Dassault Aviation Societe ( DUAVF ). This is another business - Dassault Systémes SE ( DASTY ), and they're very different. One is in aerospace and defense, the other is in 3D design.

I actually own both businesses at this particular juncture, and I think both are great businesses, but this particular article will be mostly focused on the IT/design part of things.

Updating on Dassault Systémes SE for 2023 - it's still a good "BUY here

When I first started researching Dassault Systemes back a few years ago, I was impressed by how the company managed to mostly fly under the radar for a long time - at least insofar as it went with me as an analyst and investor, and some of my closer colleagues here. The company was a non-trivial part of Dassault itself and was made its own company to fully focus on the 3d Surface design software - where it can be considered a market leader, with relative ease.

Why? What makes Dassault Systemes so good, in the past or currently?

Well, Dassault was clearly market-leading in the 1990s. The company's software was used to develop seven out of ten new airplanes, and almost 50% of all cars around the world at the time. Companies that used Dassault's software included Honda ( HMC ) Mercedes ( MBGAF ), BMW ( BMWYY ), and Boeing ( BA ). Examples of products that were designed this way are the Boeing 777, The Falcon 2000 Business yet, and the Rafale Jet Fighter - all of these were designed using CATIA.

At this point, they weren't a publicly traded business though - that didn't happen until the late 90s when the company IPO'ed and started M&A'ing heavily to ensure its competitiveness.

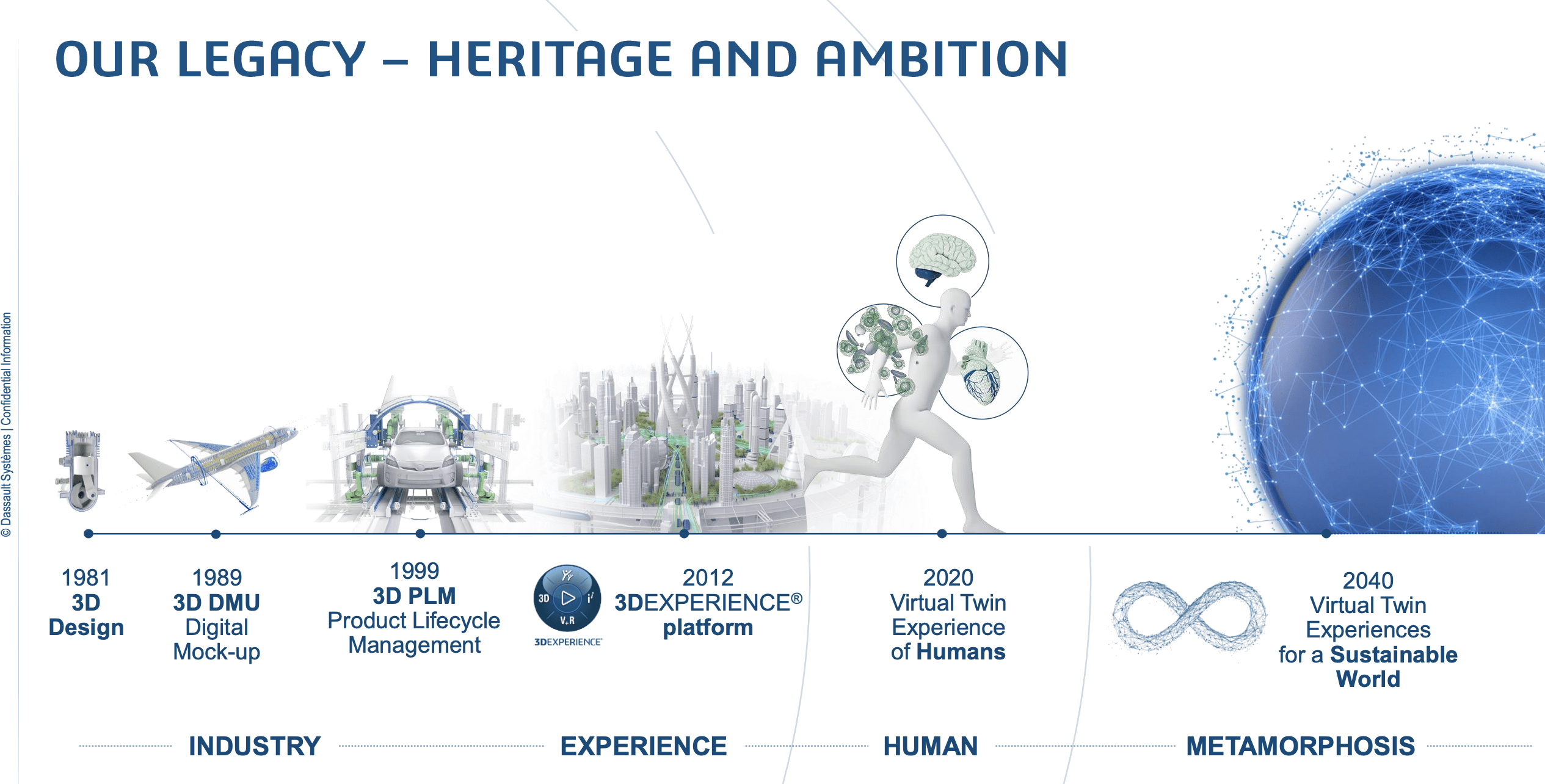

At the time, it still wasn't clear that this whole "digital tools" thing would win out over things like traditional design, but we know now that digital tools have become the gold standard in almost every industry, which is excellent because Dassault kept developing CATIA, eventually turning it into the 3DEXPERIENCE platform to connect its various software applications and enable global interoperability and cross-functional collaboration.

That's where we are today. Over 15 M&A's later which all improved the company's capacity and products, and even with the latest few years with things like ESG, that saw Dassault adding even more into its suite.

Many investors have a notion that European companies, especially French and PIGS investments are uninteresting and over-traditional monoliths that don't go anywhere. That's not the case with Dassault. The company has often been named one of the world's most innovative companies, the best employers, and the company with the most growth potential.

We have 4Q22 results. FY22 was an excellent year.

Why was 2022 an excellent year?

Because the company improved across the board.

Dassault Systemes IR (Dassault Systemes IR)

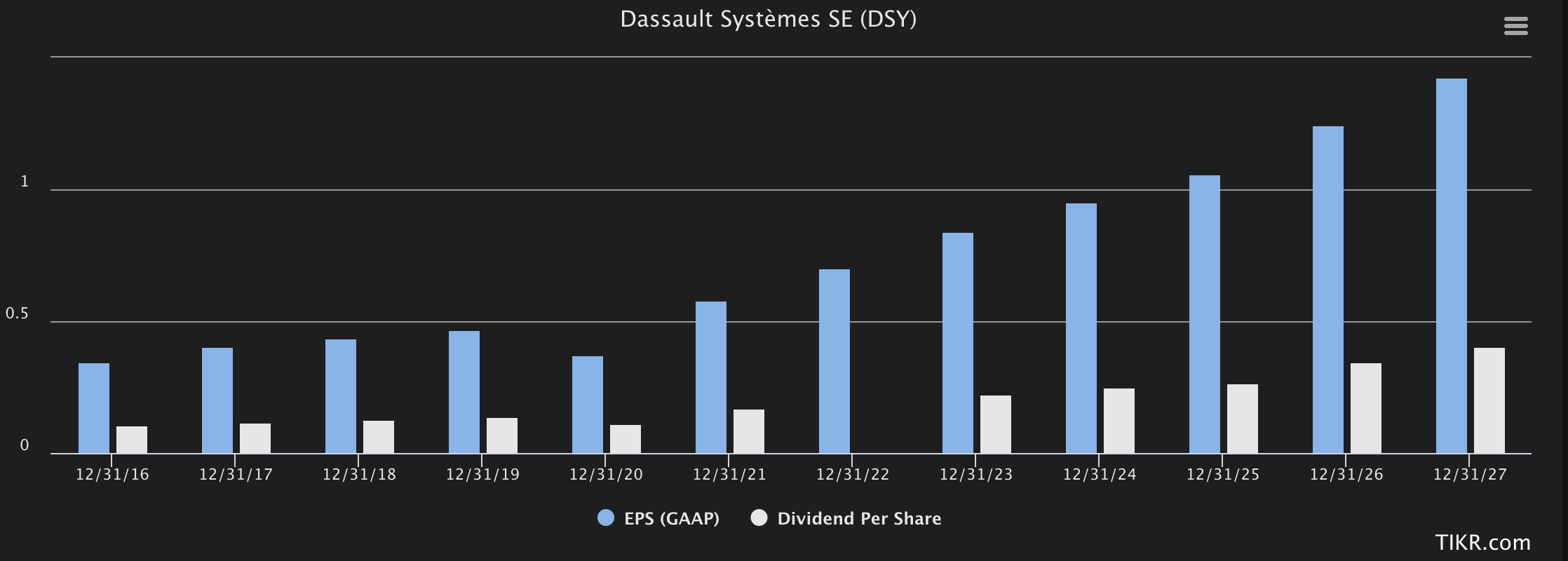

Across-the-board improvements are neither easy nor to be overlooked in today's competitive environment, and double-digit EPS in this environment is especially impressive, all things considered. Its 2023E targets include an EPS objective of upwards of €1.2. A quick history of its current platform, and where it is going, including things like VR.

{kind=link}

People often ask me what sort of IT and modern growth companies I would invest in. Where I would feel safe and conservative enough. My answer is easy - Dassault Systemes is a very good example of such a company. Not a high yield, and not high growth compared to some of the businesses in the sector, but it makes up for it with incredible know-how and tradition, and actual leadership in the business that has persisted for decades.

This is no spring chicken in terms of a company, and it continues to work with the leading companies in the world to deliver products and innovation.

{kind=link}

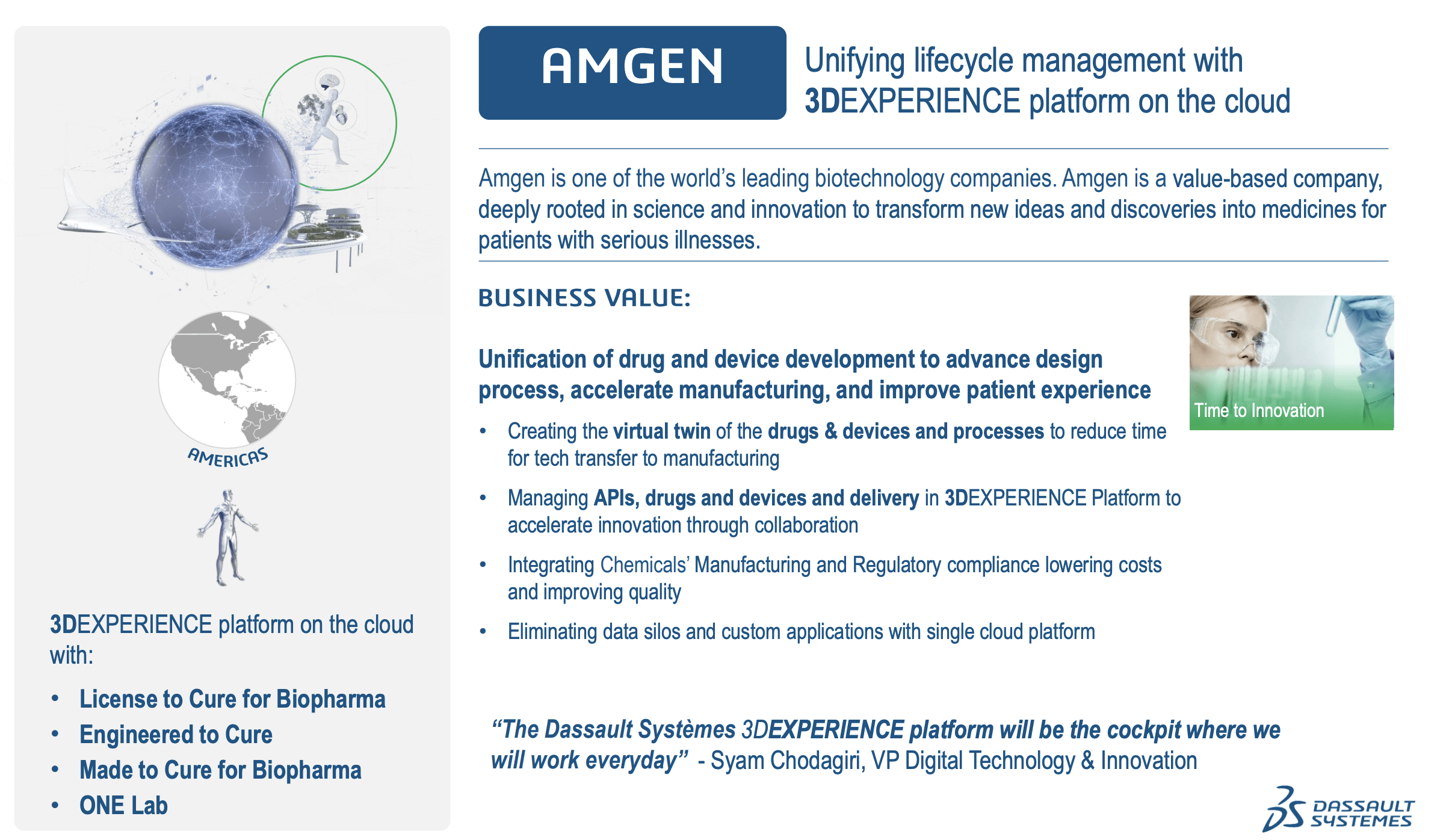

The company's operations are found not only in Manufacturing, which was the main area a few decades ago, but are now also found in Life Sciences, as well as infrastructure and other areas. There are a couple of interesting case studies showcasing what the company is doing- Amgen is certainly one here, and through the company's platform, Dassault does the following.

{kind=link}

The company's customers number in the hundreds and every single region grew as a contributor of revenues, with the Americas up 13% YoY, at a 40% market share. Dassault is relatively unique in that it is a French business, but with a business mix that is predominantly non-EU. EU is a 36% share of the company's revenues, and Asia is growing as well with a 24% share of the company's revenues.

The largest segments in terms of end-user segments are Industrial innovation, life science, and Mainstream software. Dassault manages an operating margin close to 35%, with a revenue of over €1.5B per quarter. It also maintains extremely conservative leverage, with an adjusted net debt/EBITDAO of less than 0.5x, which is down 0.4x from FY22. Dassault Systemes has been assigned an A-, and this remains the rating the company is currently operating at.

That makes the company one of the most conservatively-rated software companies on earth. The dividend is so-so. Part of the issue with Dassault has been the incredible premium the company commanded through most of the pandemic, which saw it rising above levels I would consider sustainable. Here are the current forecasts for the company, which are not outside the realm of possibility, as I see it.

{kind=link}

Dassault is set to grow - and fast. The dividend is set to expand as well, and the 2022 results mostly confirm this forecast estimate that we're looking at here. The relevant ADR from Dassault remains DASTY, a 1:1 ADR and this is calling for similar levels of growth at around double digits for the company.

The dividend yield is terrible. At a current price of just below €37, you're looking at a yield no higher than 0.46%, which is significantly less than overall inflation and where most of the risk-free rate is currently found.

However, much of this company's appeal lies in its growth potential, not in its meager dividend - though I expect investors today will be able to count on a 1-2% YoC in a few years' time.

Let's look at the valuation of the business.

Dassault Systemes - The valuation is decent, but long-term expectations are key here

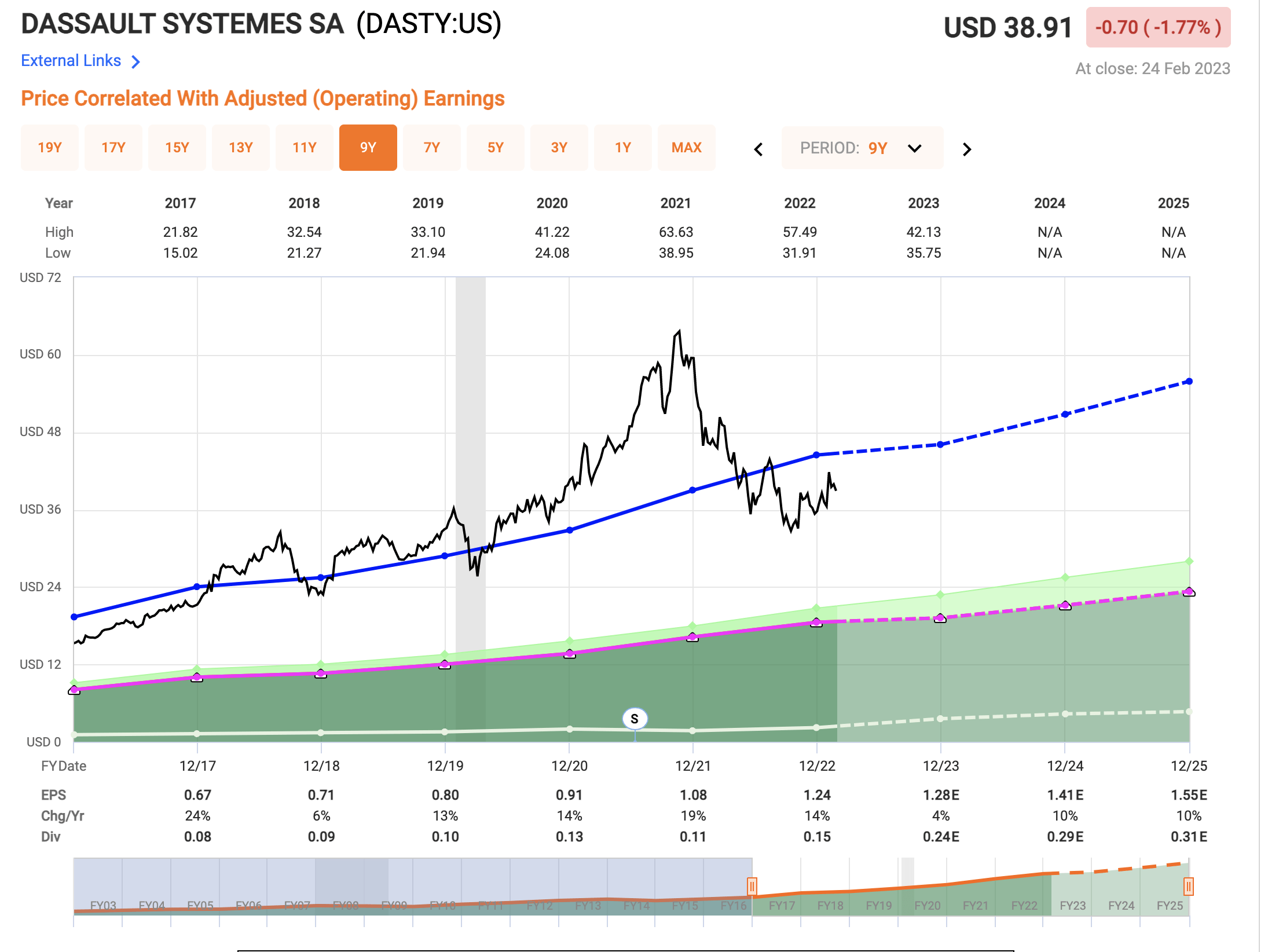

So, Dassault is a tricky business because it's not often a "BUY". This is especially true for the latest couple of years, where it has seen more over- than undervaluation. Take a look at the latest few years for the business, and specifically the ADR.

{kind=link}

And I would consider that average P/E a bit on the high side, despite excellent and proven growth rate capabilities. If we forecast this company based on current trends and apply the expected annualized GR of around 8%, we find ourselves at a 16% annualized growth rate at 37x, and around double digits at 34-35x. This is "good enough", and there's potential for outperformance here, but there is also the potential for somewhat lower growth, at least. Over the past 10 years, these analysts haven't been off often by more than 5-6%, which gives me a high degree of conviction with regard to these targets.

However, there's been a decent amount of premium decline, that's still considered part of the company here. In a short time, we've gone from 50x to less than 40x. From a nearly 40x EBIT and 33x EBITDA multiple, as well as an almost 50x P/E, which I wouldn't pay for any business, we're now down to below 30x in all of those NTM multiples, with EBIT down below 23x.

Analysts have had a hard time catching up, especially being somewhat more event-driven as opposed to fundamentals-driven, as I am. When I last wrote on Dassault, analysts were at around €40/share, from over €70/share a few years back. That's down even further to around €39.5 at this point, with only 9 analysts out of 22 at a "BUY" or equivalent rating for the business.

When to buy an investment like this is always the big question. That the company is attractive, there is no question to me. The company's DASTY ADR trades at a normalized P/E of 30.5x, and we're not there just yet. We were there a few months back - and that's when I loaded up on a few shares of the company when the native share price briefly broke below €33/share. We're back up a bit again, and we're up even more compared to when I last wrote about the business.

Looking at comps does work, but the company is heavily premiumized to most of the comps, except businesses like Autodesk ( ADSK ). I also argue that most of these comps aren't really comparable. While they're in similar businesses, there is enough difference to make up for the respective difference we see in valuation here.

DSY, the native ticker, currently is about 8x revenues, 30x P/E with a market cap of just south of €50B. There aren't many companies that compare to this. SAP (SAP) exists, but again - slightly different sector.

I expect Dassault to be able to grow at least at 6-8% going forward - potentially more. I believe the market may be underestimating the company growth potential here.

At the same time, Dassault isn't cheap here. It's rarely ever "cheap". In fact, the last time the company was "cheap" was during the financial crisis. Even then, it barely broke the 15x P/E ratio limit, and only for a short time. Its history is a tradition of trading above 28x, but below 30x.

I still believe that the future growth for the company will be able to deliver outperformance, and will be able to match the closer average P/E-valuation, namely around 30-35x. This isn't necessarily an "easy" investment, because much of this growth will come with time. That's why my exposure to the company is still relatively limited at this point - there are higher-yielding alternatives out there.

But to those that invest in tech growth and similar businesses, I would argue that you should take a closer look at Dassault - because it might have what you're looking for in an investment. Good growth of upwards of 8%, but also the safety that comes with an A-rating.

But yeah, the dividend isn't great.

However, this is my thesis for 2023 for Dassault Systemes.

Thesis

- Dassault is a class-leading superb company in the realm of product modeling, life/health, and infrastructure technologies, or if we want to cover it all, "Application software". It has superb management, and a solid, market-beating history. I want to own the company at a good price.

- I would argue that you should not pay above 30x normalized native P/E for the company. Given the company's current price, this is actually possible here.

- I give Dassault Systémes a "BUY" with a PT of €37 here - a low target compared to analysts, but a conservative one, even though I increased it by over €1 on the back of excellent results. This leaves us with a small upside at this time.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

It would still be a massive stretch to call Dassault "cheap" here, but it does have a realistic upside, therefore fulfilling 4 of my 5 investment criteria.

Because of that, I still say "BUY", though that buy rating is weak.

For further details see:

Dassault Systemes: Decent Performance, But Definitely More Of A 'Buy' In 2023