DASTY - Dassault Systemes: To Evaluate Q3 2023 Performance Before Going Long

2023-07-28 11:11:29 ET

Summary

- I recommended a hold rating due to the heavily weighted end-of-year profile.

- DASTY's recent results showed slightly weaker recurring revenue growth, but operating profit was in line with projections.

- Meeting 3Q23 guidance is crucial for market expectations and could drive a valuation re-rating if achieved.

Overview

My recommendation for Dassault Systemes (DASTY) is a hold rating despite my expectation that DASTY will regain its historical growth rate as we move past FY23 and that its valuation will trade back to 36x, the same as where peers' are trading. The near-term concern is whether DASTY can meet 3Q23 guidance, as it has a huge impact on market expectations for 4Q23 and FY23. If DASTY can meet 3Q23 guidance, I would give the green light to buy the stock.

Business

DASTY provides software applications services designed to support client company's innovation processes. The company's line of business includes provision of 3D design software, 3D digital mock up and product lifecycle Management.

Recent results & updates

Overall sales for DASTY came in slightly below consensus expectations for the 2Q23 . This quarter's unexpectedly high license growth was propelled by both rapid Solidworks expansion and a rebound in China. However, recurring revenue growth was slightly weaker, driven by Medidata growth slowing to high single digit percent due to a decline in study starts across the industry compared to the extremely high levels seen immediately following Covid. Although revenue was lower than expected, operating profit was in line with projections.

To begin, this quarter's growth driver was Solidworks, which grew by double digits thanks to what I believe was primarily catch-up demand in North America and China over the prior two quarters. Demand was also high in Germany, likely due to early purchases by underlying customers who expect a price increase in July. In addition, despite facing very stiff competition in 2Q23, 3DEXPERIENCE managed to grow by 2% on a constant currency basis; this is particularly impressive considering that just a year ago, 3DEXPERIENCE was growth at a rate of 15% to 20%. This demonstrates DASTY's robust pipeline, which I expect to support its steady performance throughout 2H23. As things stand, I anticipate Solidworks' growth to remain in the high single digits, helped by 3DEXPERIENCE and the continuing recovery in China.

On the other hand, Medidata's growth slowed to the high single digits, influenced by a general slowdown in the number of clinical trials and the lingering effects of last year's COVID-19 megastudies. Although growth has slowed from 15-20% to the high single digits, I emphasize that the fundamental growth drivers of Medidata are still very much in place. Total bookings increased 17% year-over-year in 2Q23, and management highlighted win rates of >75% and multiple multi-year renewals with top50 pharma companies signed in the quarter. Finally, DASTY's value chain position in the market is unchanged, and I expect the company to reap benefits from industry consolidation.

For the coming 3Q23, management has set a target operating margin of 30.2 to 30.5%, and for the entire year of FY23, the goal is 32.3 to 32.6%. This means that a margin expansion of 190 bps is required for 4Q23. In my opinion, the current investment climate is not favorable for a profile like this one, which is heavily weighted toward the end of the year. Today's uncertain economic outlook has investors searching for safer investments. There's a chance of a hard landing one day, and no recession the next. If DASTY falls short of expectations in the 3Q23, it will need to accelerate its pace considerably in 4Q23, which means further risk of missing guidance. Management team feels optimistic because they anticipate a sustained rate of growth acceleration through the rest of the year. This will be propelled by an increase in large deal activity, which raises risk because of the degree of uncertainty surrounding the successful completion of such deals in the second half.

Overall, while I agree on the long-term growth potential of DASTY as the industry secular trend is positive, I would place my bet on the stock if DASTY meets 3Q23 guidance. This would signal to the market that management's outlook is "correct", instilling confidence in investors.

Valuation and risk

Author's valuation model

According to my model, DASTY is valued at EUR48 in FY24, representing a 25% increase. This target price is based on my growth forecast of 8% over the next two years, with FY23 meeting management guidance (giving management the benefit of the doubt). The rationale for 8% growth is that historically, pre-covid, DASTY has been growing in that range, so I do not see any structural reasons why it is not able to regain that growth pace.

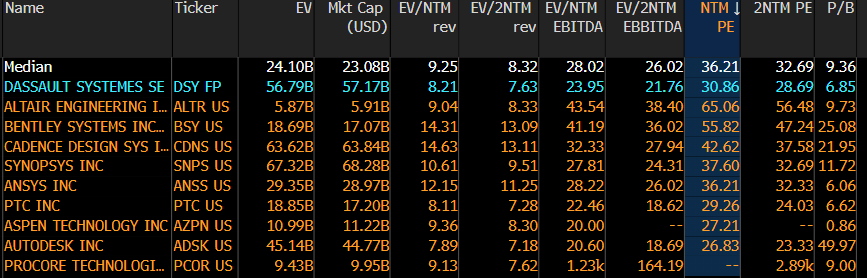

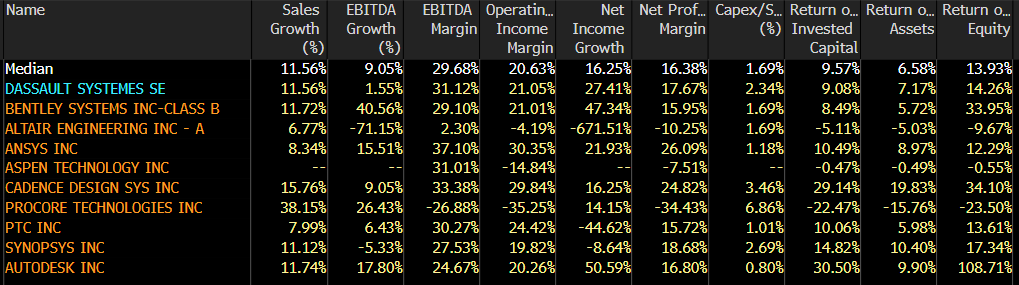

DASTY is now trading at 31x forward PE, which I believe will rise over the next two years as the market continues to close the gap it has vs. other application software peers. Historically, DASTY forward PE has traded at a 1x ratio vs. the group's median. In terms of top-line and net income growth, DASTY growth is in line with or slightly above the group. Importantly, DASTY is the largest player (by revenue) in the group. In FY24, I projected DASTY would trade at 36x forward PE.

{kind=link}

{kind=link}

Competitors in the architecture and construction industries (like Autodesk) could pose a threat to DASTY as it expands into these markets. DASTY will likely find a hard time winning market share as incumbents have established brand equity and distribution networks in place.

Summary

My recommendation for DASTY is a hold rating, as the current investment climate's uncertainty and the heavily weighted end-of-year profile raise some risks. Meeting 3Q23 guidance will be crucial for market expectations for 4Q23 and FY23. If DASTY meets 3Q23 guidance, it could instill confidence in investors, thereby driving the valuation re-rating that I am expecting.

For further details see:

Dassault Systemes: To Evaluate Q3 2023 Performance Before Going Long