EQIX - Data Center REITs: Physical Epicenter Of AI

2023-06-08 10:00:00 ET

Summary

- Among the top-performing property sectors this year, the Data Center REIT rebound has been fueled by reports of "booming" demand for artificial intelligence ("AI") focused data center chips.

- Even before the Nvidia report, Data Center REITs were on the upswing in early 2023 after an impressive slate of earnings results showed improved pricing power and record-high occupancy rates.

- Ironically, this AI-wave comes just as Data Center REITs became a trendy “short” idea centered on a thesis of weak pricing power and competition from the "hyperscalers" - Amazon, Google, and Microsoft.

- A confluence of development bottlenecks - power shortages, higher cost of capital, supply chain constraints, ecopolitics, and NIMBYism - have created a more favorable dynamic and swung the pendulum of pricing power towards existing property owners.

- Barriers to supply growth combined with AI-accelerated demand should bring some sustained pricing power to a sector long-burdened by near-unlimited supply. With negotiating power tilting back towards landlords, there appears to be enough economic value to be shared.

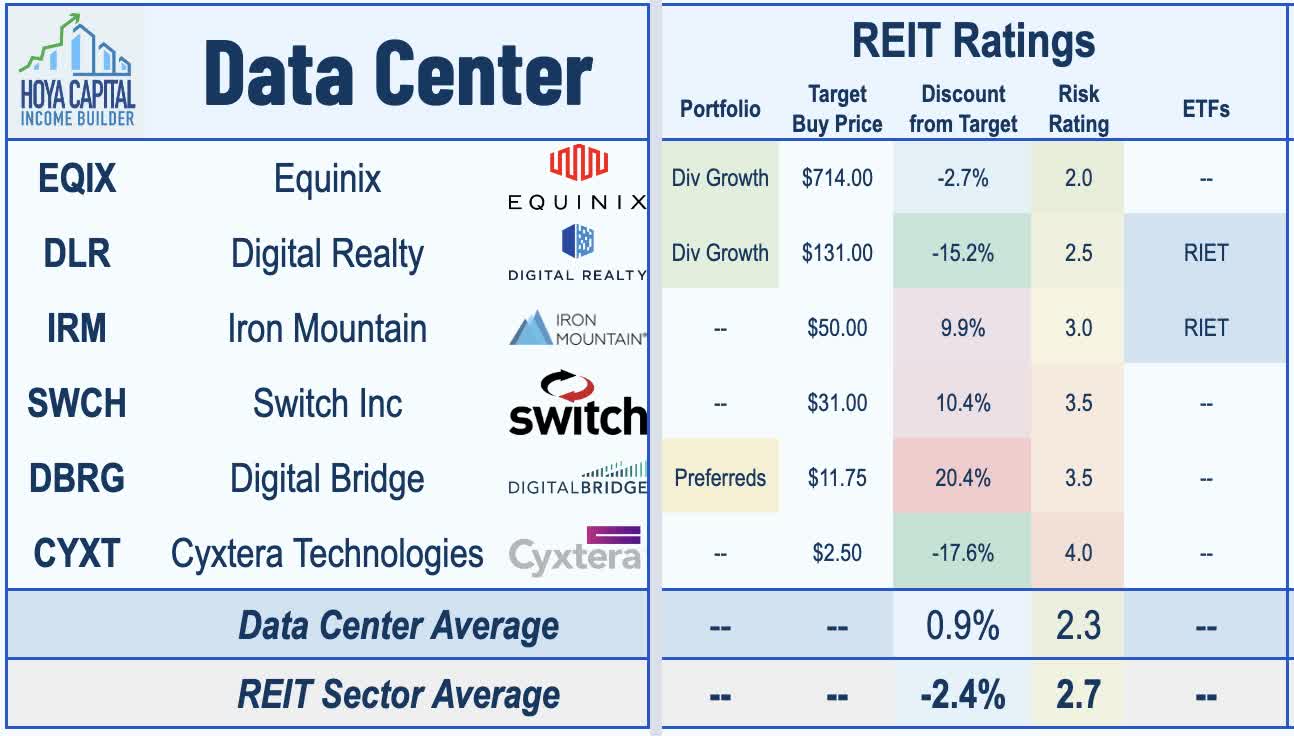

REIT Rankings: Data Centers

This is an abridged version of the full report and rankings published on Hoya Capital Income Builder Marketplace on June 6th.

{kind=link}

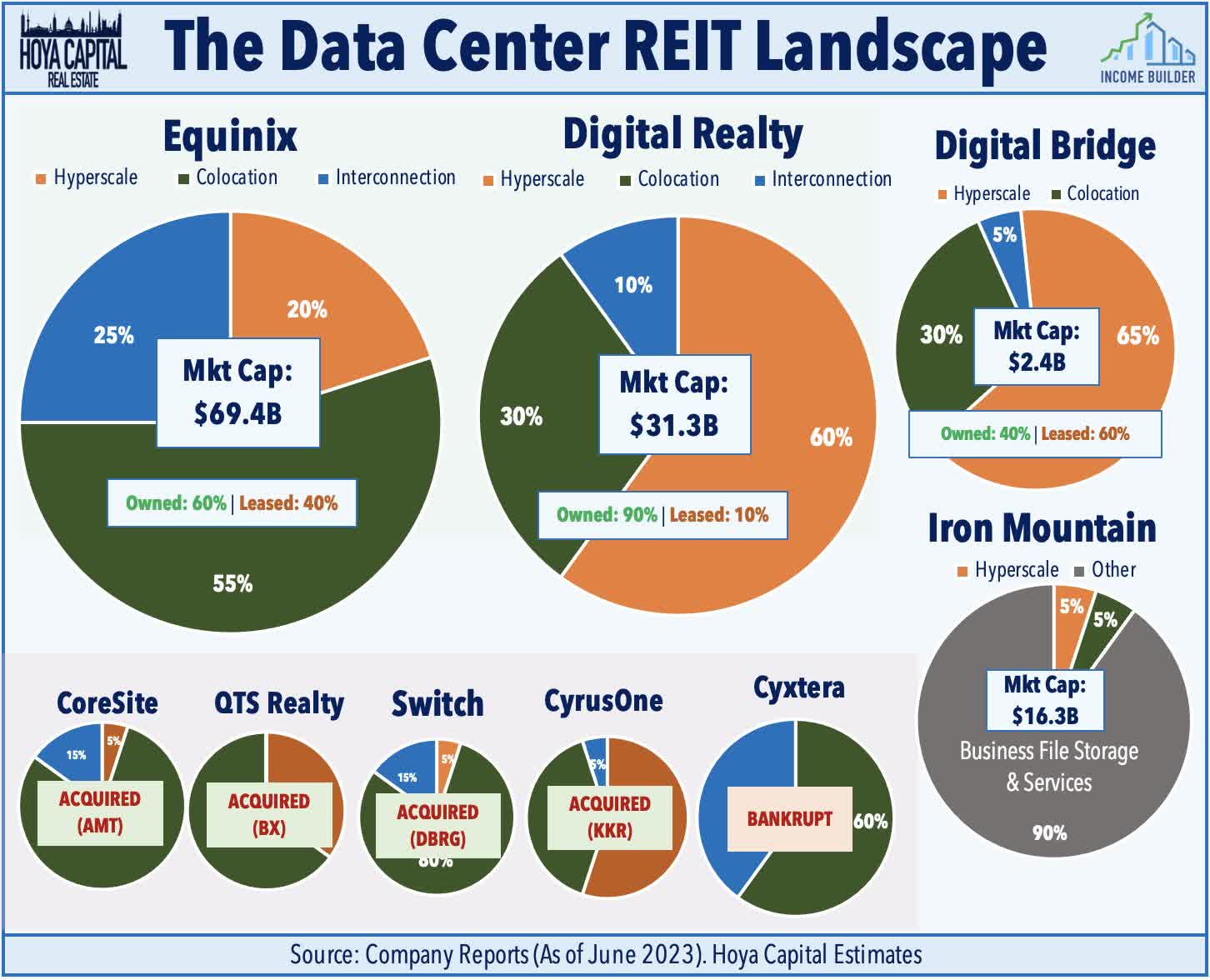

Among the top-performing property sectors this year, the Data Center REIT rebound has been augmented by reports of "booming" demand for artificial intelligence ("AI") focused data center chips. Even before the Nvidia report, Data Center REITs were on the upswing in early 2023 after an impressive slate of earnings results showed improved pricing power and record-high occupancy rates. Within the Hoya Capital Data Center Index , we track the two major data center REITs - Equinix (EQIX) and Digital Realty ( DLR ) - alongside DigitalBridge ( DBRG ) - a former REIT that now operates as a conventional c-corp, Iron Mountain ( IRM ) - a specialty REIT with a growing data center vertical alongside its document storage business, and Cyxtera ( CYXT ) - a former SPAC that had planned to convert to a REIT before hitting extreme turbulence this year under the weight of its significant load of variable rate debt.

{kind=link}

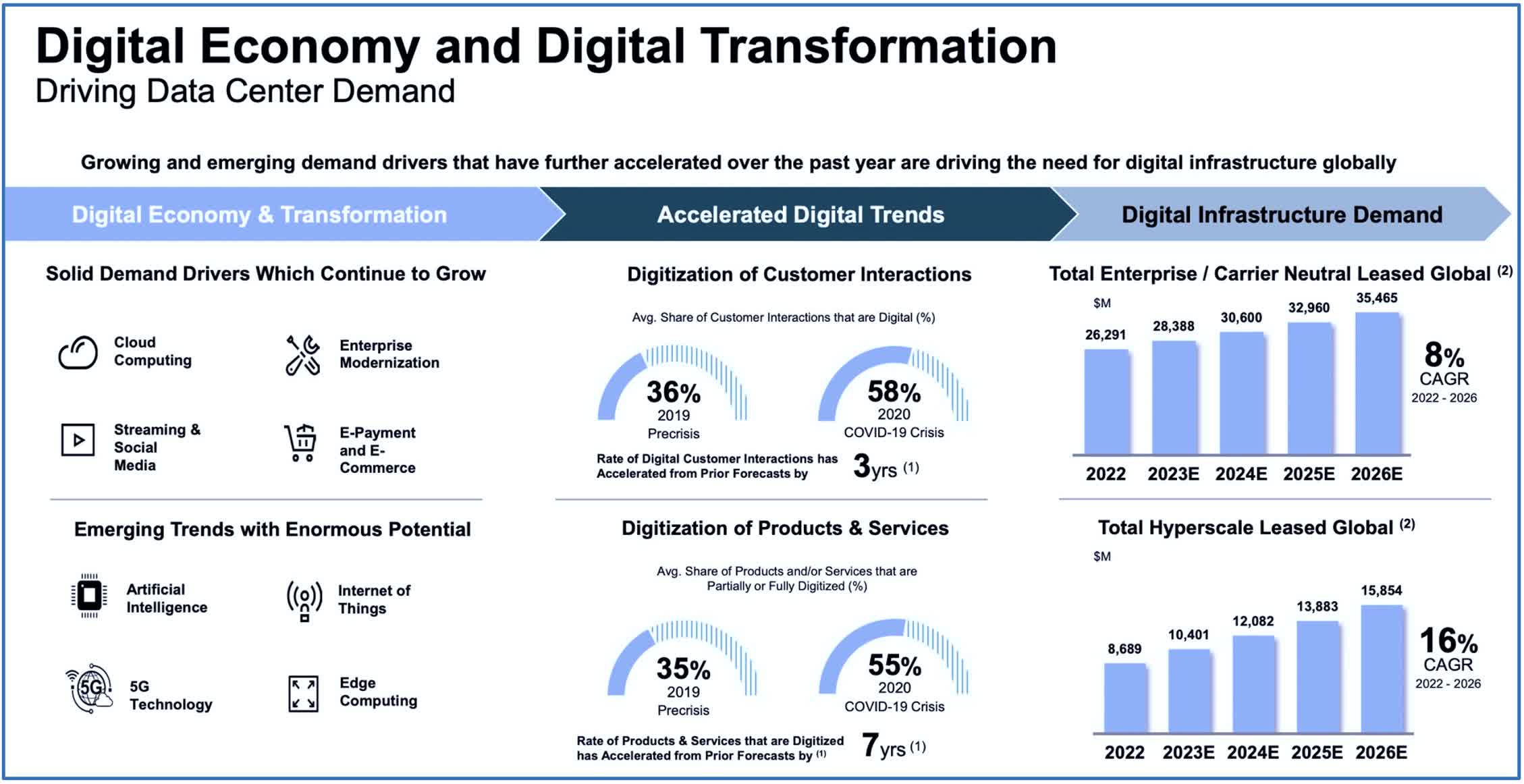

Data Center REITs have been thrust back into the spotlight in recent months - this time in a favorable light as the physical "epicenter" of the artificial intelligence ecosystem - after chip maker Nvidia ( NVDA ) reported blowout first-quarter results in late-May, driven by strength in its data center business. Nvidia said that it is "significantly increasing its supply of data center chips" to meet "surging" demand resulting from investments in artificial intelligence ("AI"), a technology that leverages the computing power of data centers to search massive datasets and to process intensive computing tasks to produce a seemingly "intelligent" output. In its earnings call, Nvidia commented that it believes that "a trillion dollars" of installed global data center infrastructure will transition from general-purpose computing to "accelerated" computing as companies "race to apply generative AI into every product and service."

{kind=link}

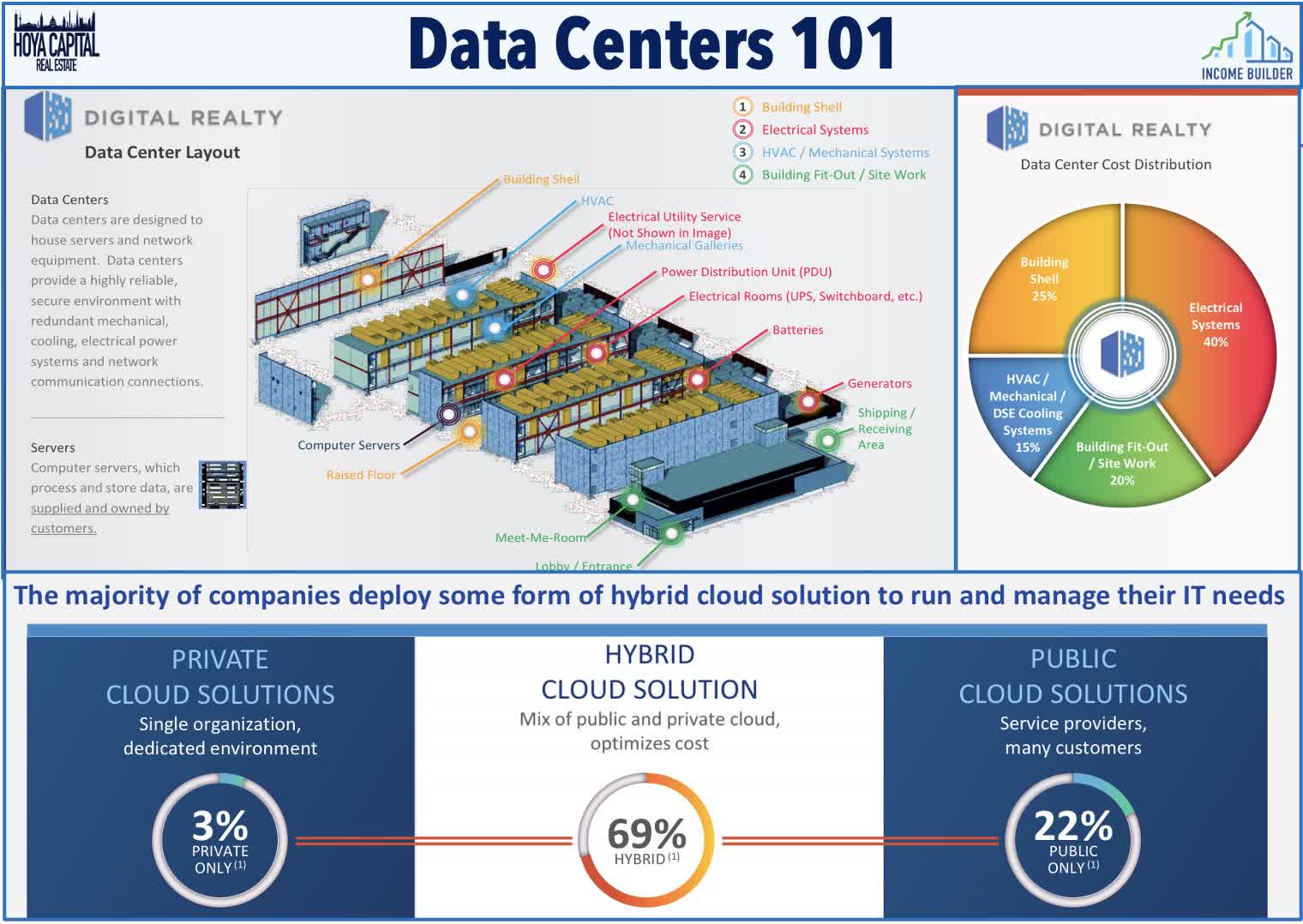

Housed in windowless buildings surrounded by massive generators and cooling equipment, data centers provide the critical infrastructure - power, cooling, and physical rack space - to a variety of enterprise customers with different networking and computing needs. Cloud computing is essentially the "outsourcing" of these computing tasks and data storage from the local device to a far-more-powerful and reliable off-site facility, which has been enabled by the ongoing deployment of high-speed and low-latency internet infrastructure. AI has long been viewed as the natural evolution - and next generation - of cloud computing, which further leverages the potentially "unlimited" computing power of the offsite facility by integrating specialized hardware such as Graphics Processing Units ("GPU") and Tensor Processing Units ("TPU") in addition to the conventional Central Processing Unit ("CPU") tasks.

{kind=link}

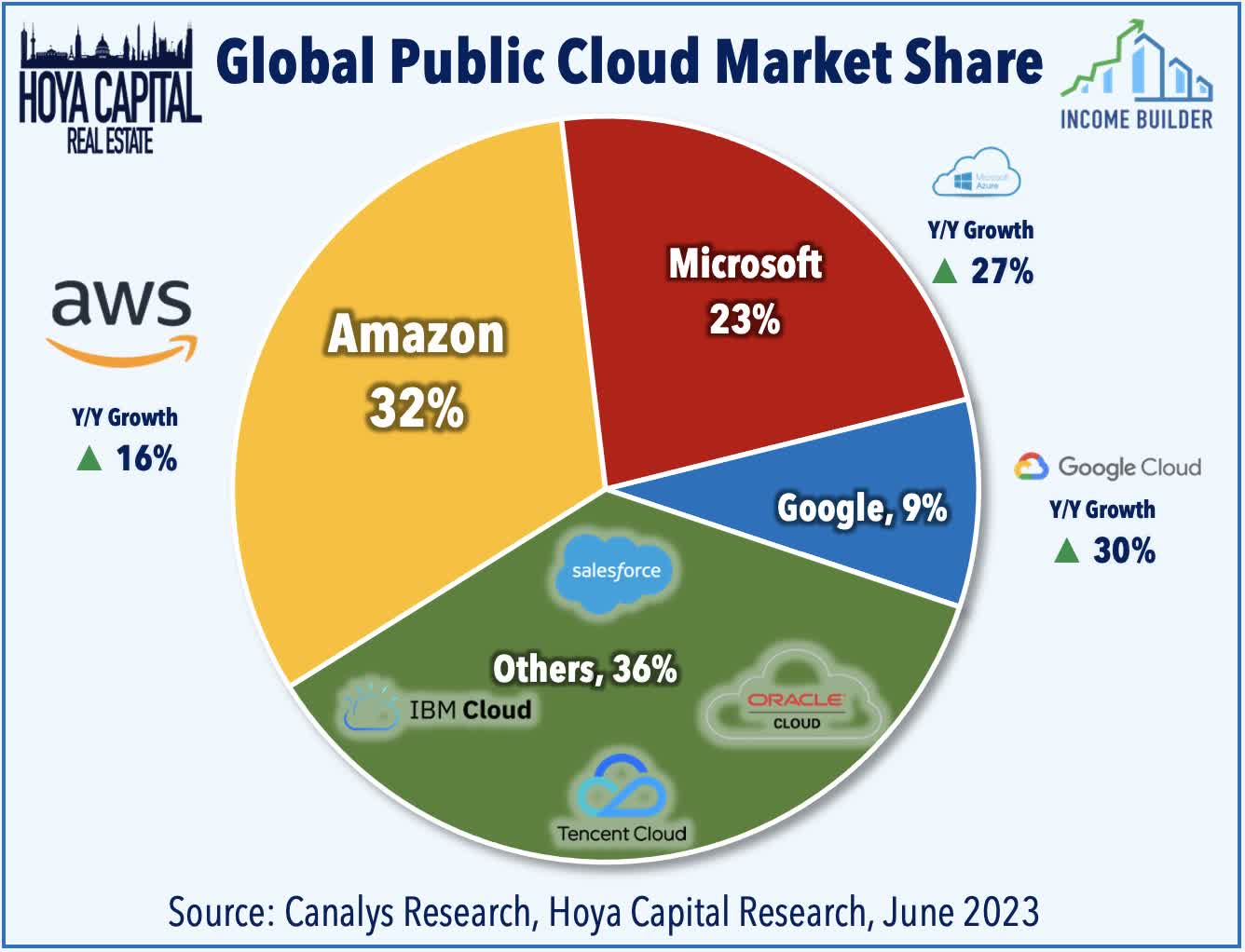

The companies that are synonymous with cloud computing - Amazon ( AMZN ), Microsoft ( MSFT ), Google ( GOOG ) ( GOOGL ), Alibaba ( BABA ), Oracle ( ORCL ), Salesforce ( CRM ), and Snowflake ( SNOW ) - are among the largest and most critical tenants of these data center operators, and have become even more critical tenants in recent years as a growing share of leasing activity has accrued to these "hyperscale" tenants which have increasingly dictated the terms of leasing agreements and pricing. While a larger share of leasing activity is indeed accruing to a smaller number of tenants, the overall pie continues to grow. The pendulum of pricing power swings between landlord and tenant over time based on market-level and national supply/demand dynamics, but ultimately we believe that there is enough sustainable economic value to be shared by tenants and property operators alike.

{kind=link}

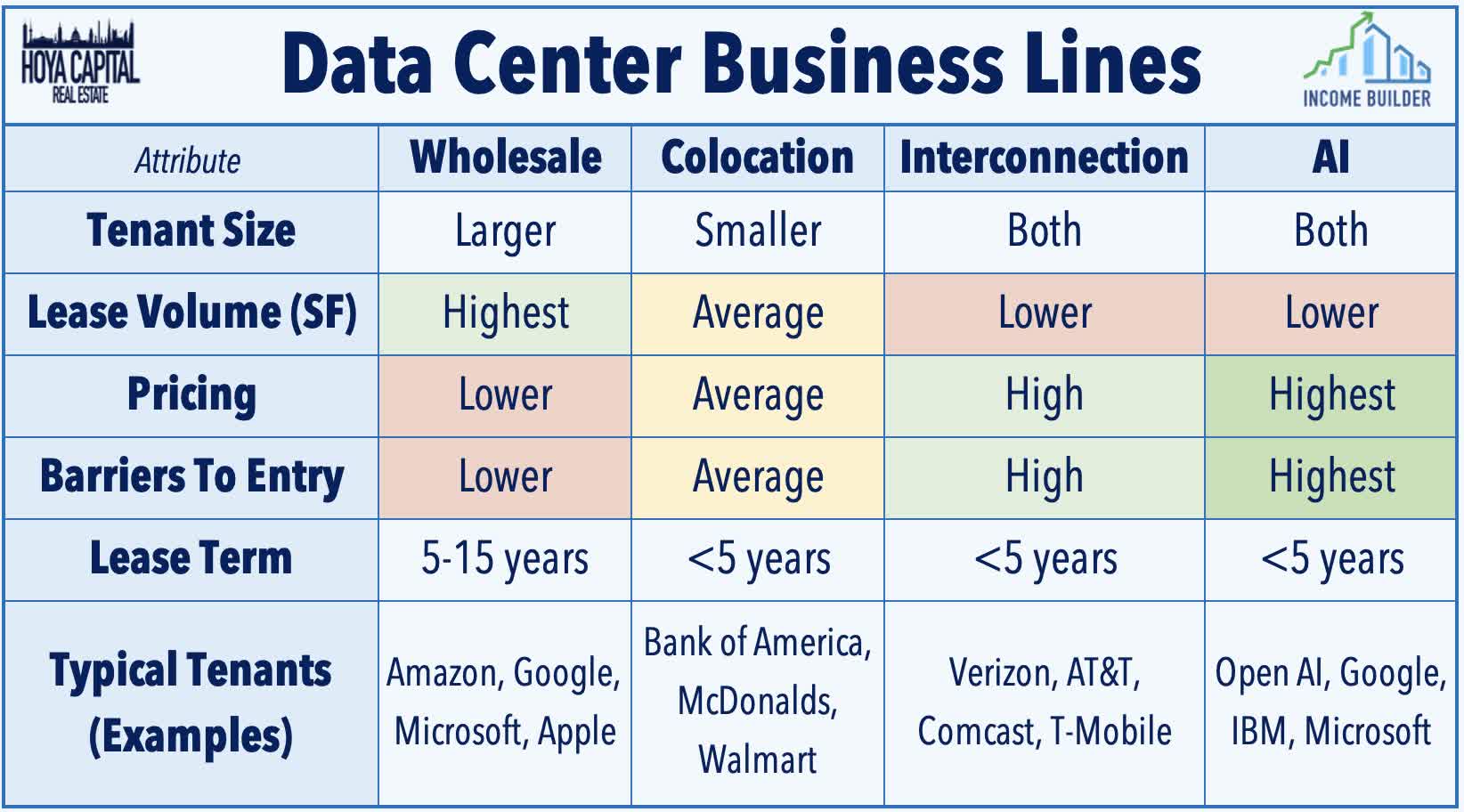

Data Center REITs own roughly 600 data centers - 30% of investment-grade data center facilities in the US - and command roughly a fifth of data center capacity globally. The value of each data center is largely a function of its position along the internet backbone, the physical fiber-optic network that links every connected device across the world. Properties within the backbone, or more precisely at the "intersection" of various networks, are able to provide higher-value and lower-latency network-based colocation and interconnection services, which command higher rent-per-MW and have higher barriers to entry due to the inherent "network effects." Low latency is especially critical for AI applications, which further intensifies the “data gravity” effects and need to be located in proximity to other networks. Properties on the periphery or those lacking a critical mass of interconnection tenants typically provide more ubiquitous enterprise-based wholesale services, including storage and cloud-based software applications.

{kind=link}

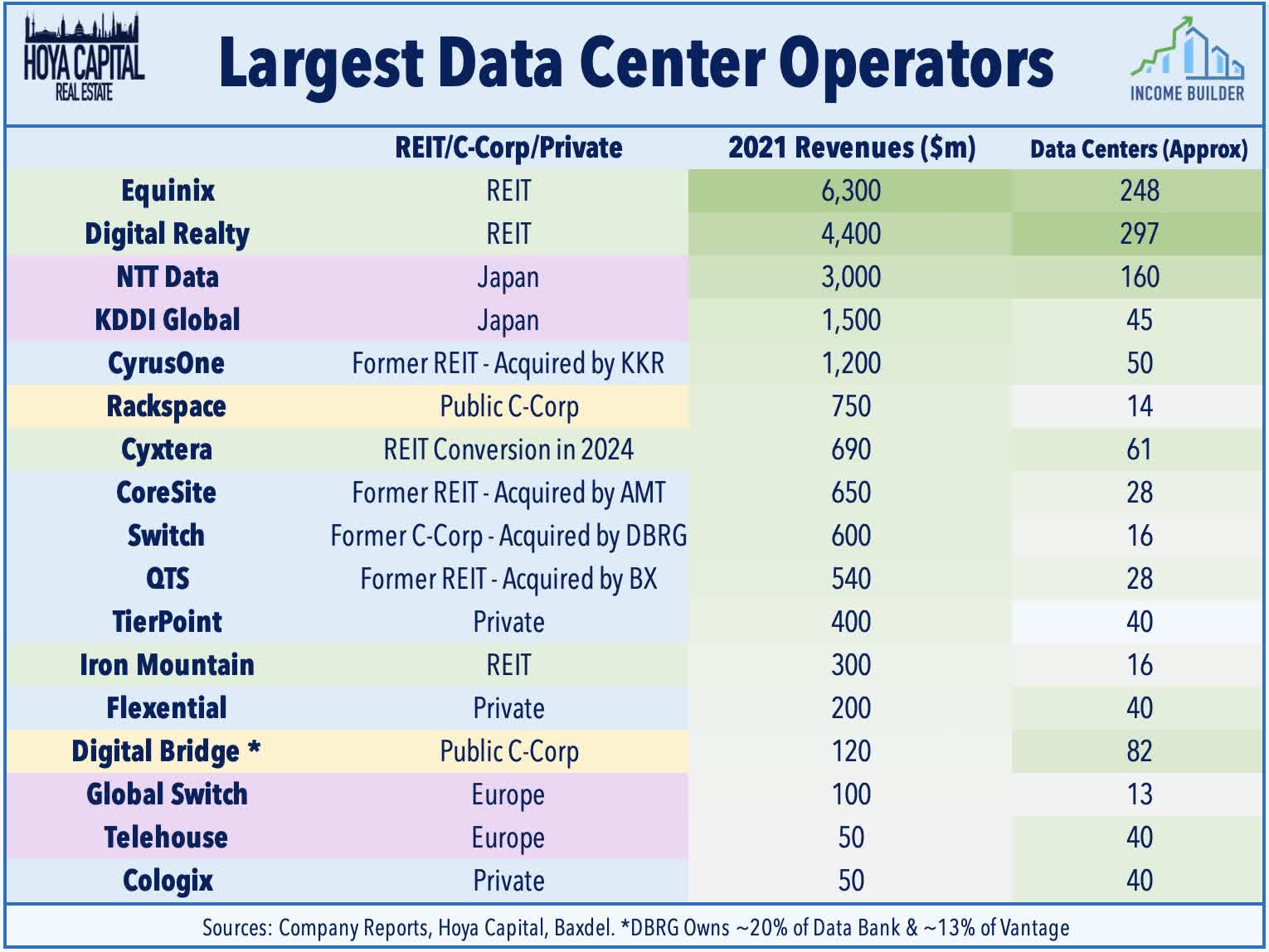

Interconnection, which relies on "network effects," can translate into a competitive advantage that new entrants have difficulty replicating. Equinix has the highest "quality" portfolio of network-dense assets followed by the smaller CoreSite - which is now owned by American Tower. Digital Realty significantly expanded its interconnection and colocation business through its Interxion acquisition and has staked-out favorable positioning in many of the most critical network-dense data center markets. CyrusOne , QTS , and the majority of non-REIT data center operators focus primarily on the more commoditized wholesale assets. Cyxtera - which filed for Chapter 11 this week - operates a relatively high-barrier portfolio of network-dense assets but only owns two of its facilities and leases its remaining 59 data centers, which was a major factor in its difficulty in refinancing its debt.

{kind=link}

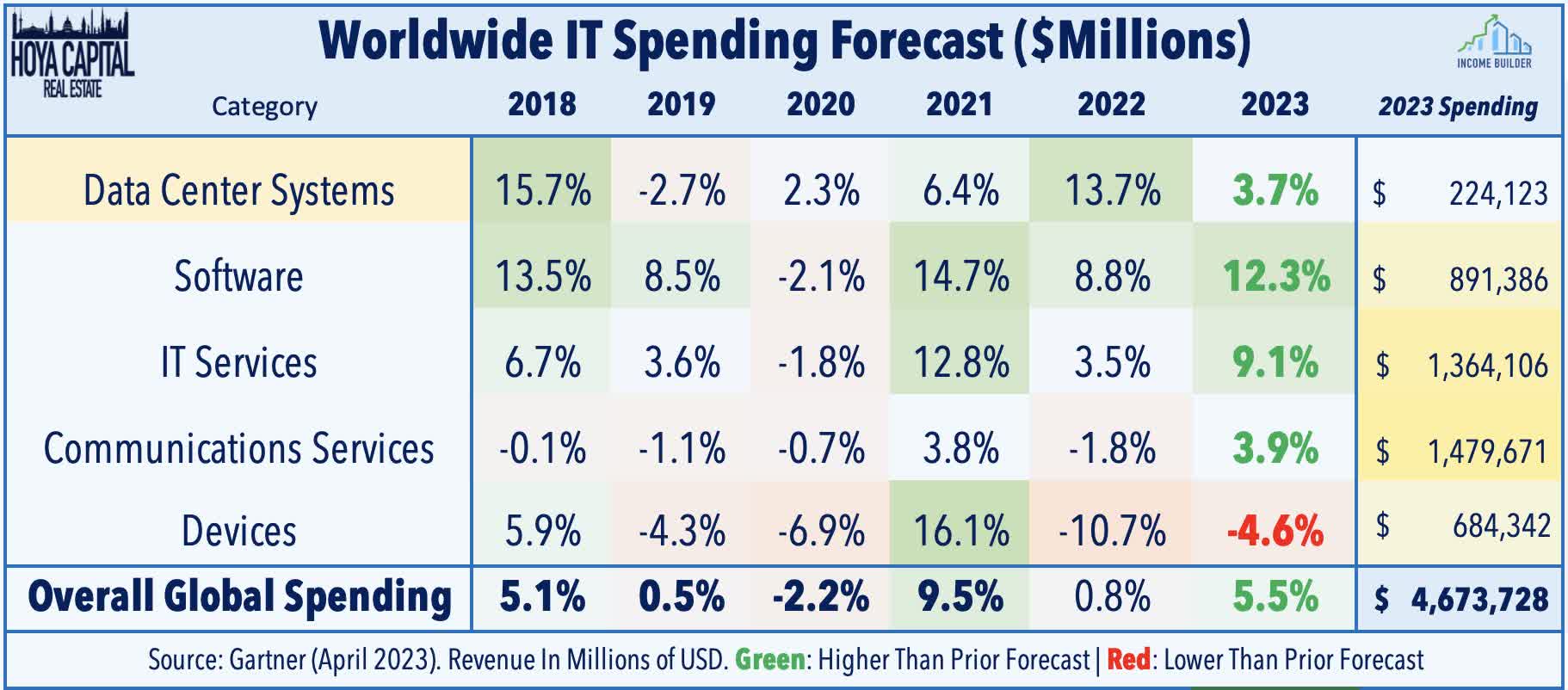

Major players on the hardware side include Intel ( INTC ), Advanced Micro Devices ( AMD ), Nvidia ( NVDA ), and IBM ( IBM ), which collectively provide the majority of networking equipment utilized by data center tenants. Spending on the "public cloud" by hyperscale providers remains at record-levels - rising nearly 22% year-over-year in the latest Canalys Research report . Spending on the physical hardware - servers and chips - has also seen a notable reacceleration in recent quarters after stalling in late 2021 and into early 2022 due, in part, to the effects of a global chip shortage during the pandemic. In their most recent forecast in April, Gartner upwardly revised its growth outlook for IT spending across the board with the exception of spending on end-user devices. Worldwide IT Spending is now expected to grow by 5.5% this year, led by a 12% jump in software spending and a 9% increase in IT services spending. Spending on data center systems - the strongest category in 2022 - is expected grow another 4% this year.

{kind=link}

Data Center REIT Fundamentals

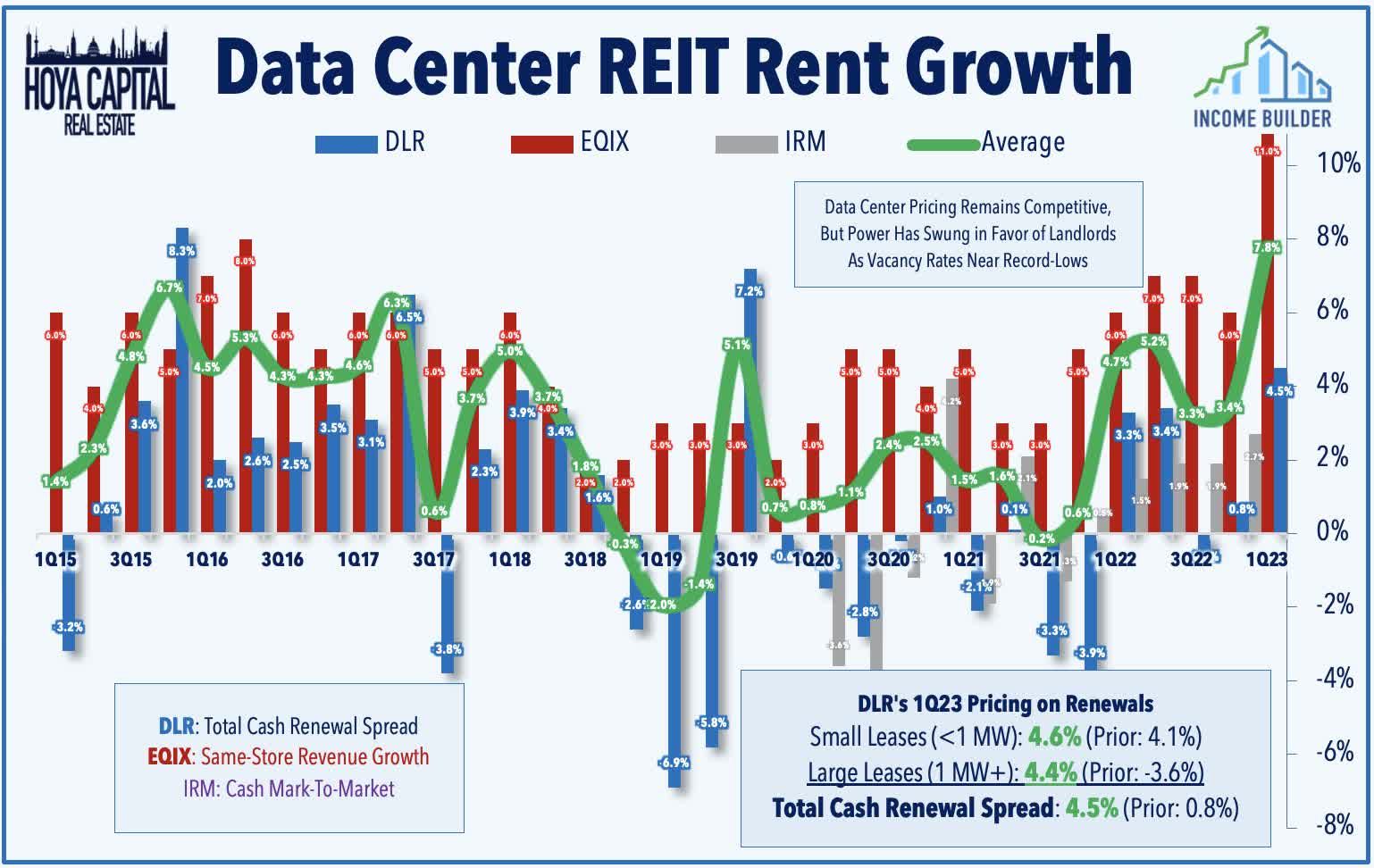

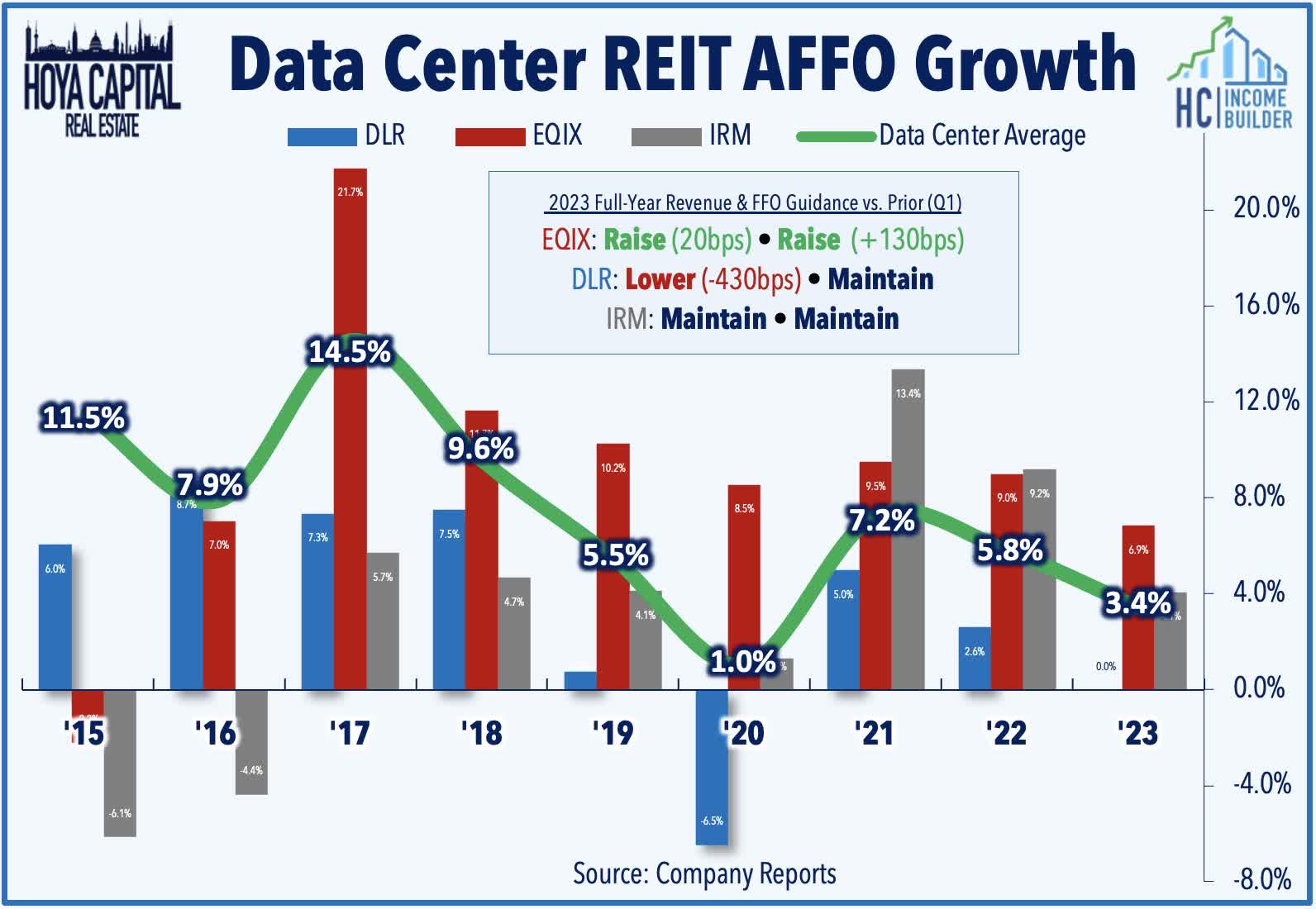

As discussed in our REIT Earnings Recap , impressive pricing power was the primary takeaway from a solid slate of first-quarter earnings results and subsequent REITweek commentary. Equinix recorded its strongest quarter of same-store revenue growth on record at 11% and while some of this revenue growth was attributed to power price increases ("PPI"), EQIX notes that even without these pass-through expenses, the increase was still impressive at 7%, commenting that "pricing is definitely firm...we've raised pricing both on the retail side, space, power and on the interconnection units." Digital Realty reported similarly strong pricing trends, with renewal rent spreads rising 4.5% - the strongest quarter since 2019 - to which DLR commented, "we feel confident that this positive pricing environment is sustainable and here to stay." Iron Mountain , meanwhile, reported cash renewal rent growth of 3.5%, its strongest quarter since late 2020.

{kind=link}

Diving deeper into earnings results, Equinix raised its full-year guidance across the board in Q1 and now projects full-year revenue growth of 13.2% - up 20 basis points from its prior outlook - and sees FFO growth at 6.9% - up 130 basis points. Digital Realty , meanwhile, affirmed its FFO and EBITDA guidance but lowered its expected revenue growth from roughly 23% to 18%, but the revision was due "purely" to lower expense pass-throughs from lower electricity rates. DLR also reiterated its guidance calling for "same-capital" NOI growth of 3.4% for full-year 2023, which would be the first year of positive organic growth since 2017. Iron Mountain maintained its full-year revenue and FFO outlook which calls for growth of roughly 9% and 4%, respectively, and for total data center leasing volume of 80MW.

{kind=link}

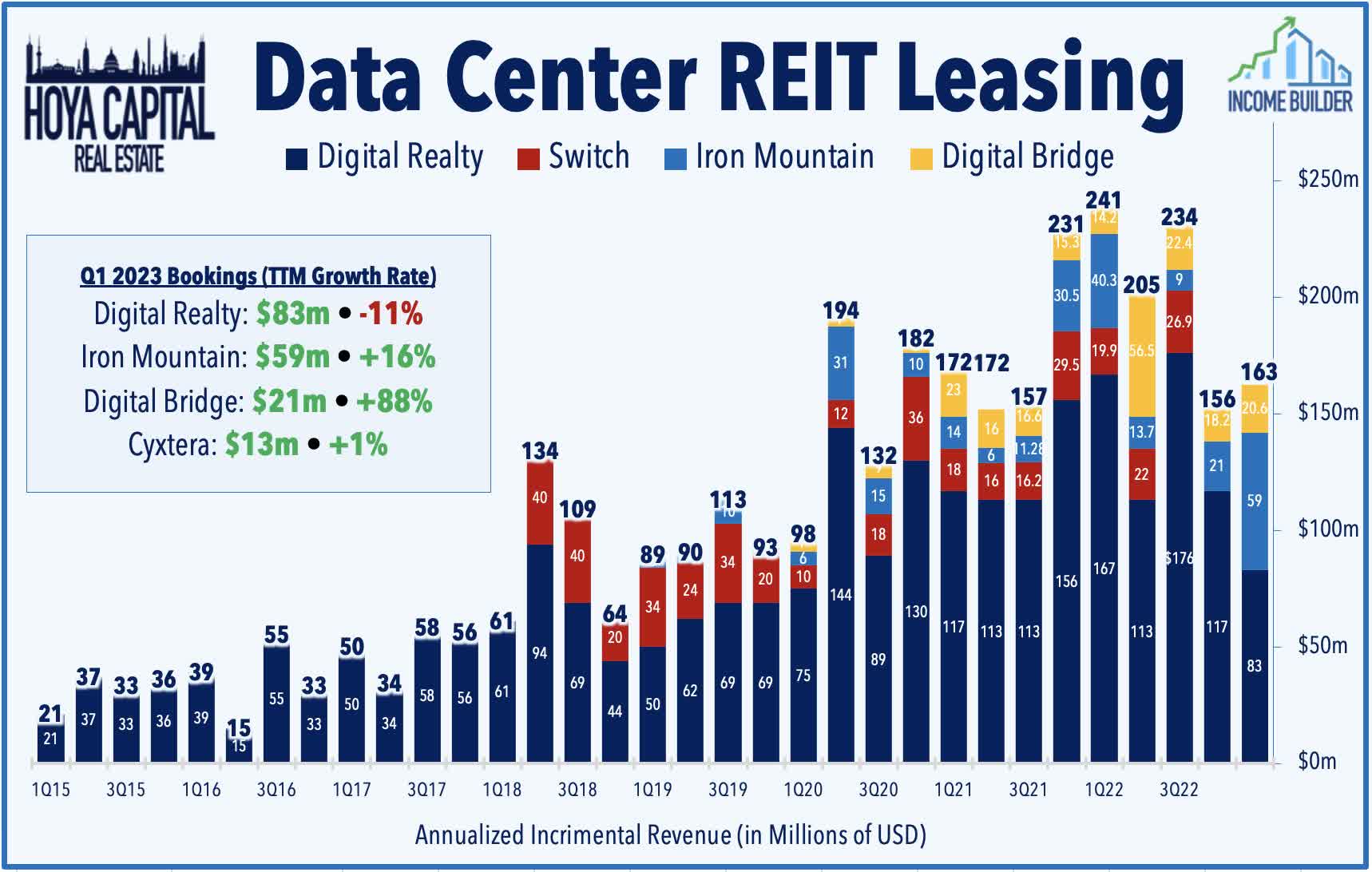

While pricing power has improved, total leasing volume has taken a step back in recent quarters from the record pace seen in 2021 and 2022 as hyperscalers have pumped the breaks a bit. Digital Realty reported $83M of incremental annualized GAAP rental revenues in Q1, which was the lowest since Q1 of 2020, but DLR did notch a record-high for interconnection leasing volume. Iron Mountain has picked up some of the slack, however, signing 52 megawatts of new and expansion leases - its strongest quarter on record for bookings - and well on its way to its 80MW full-year target. DigitalBridge reported $21M in bookings - nearly double its pace from Q1 of 2022 - while now-bankrupt Cyxtera reported bookings of $13M, which was about 1% above its pace last year.

{kind=link}

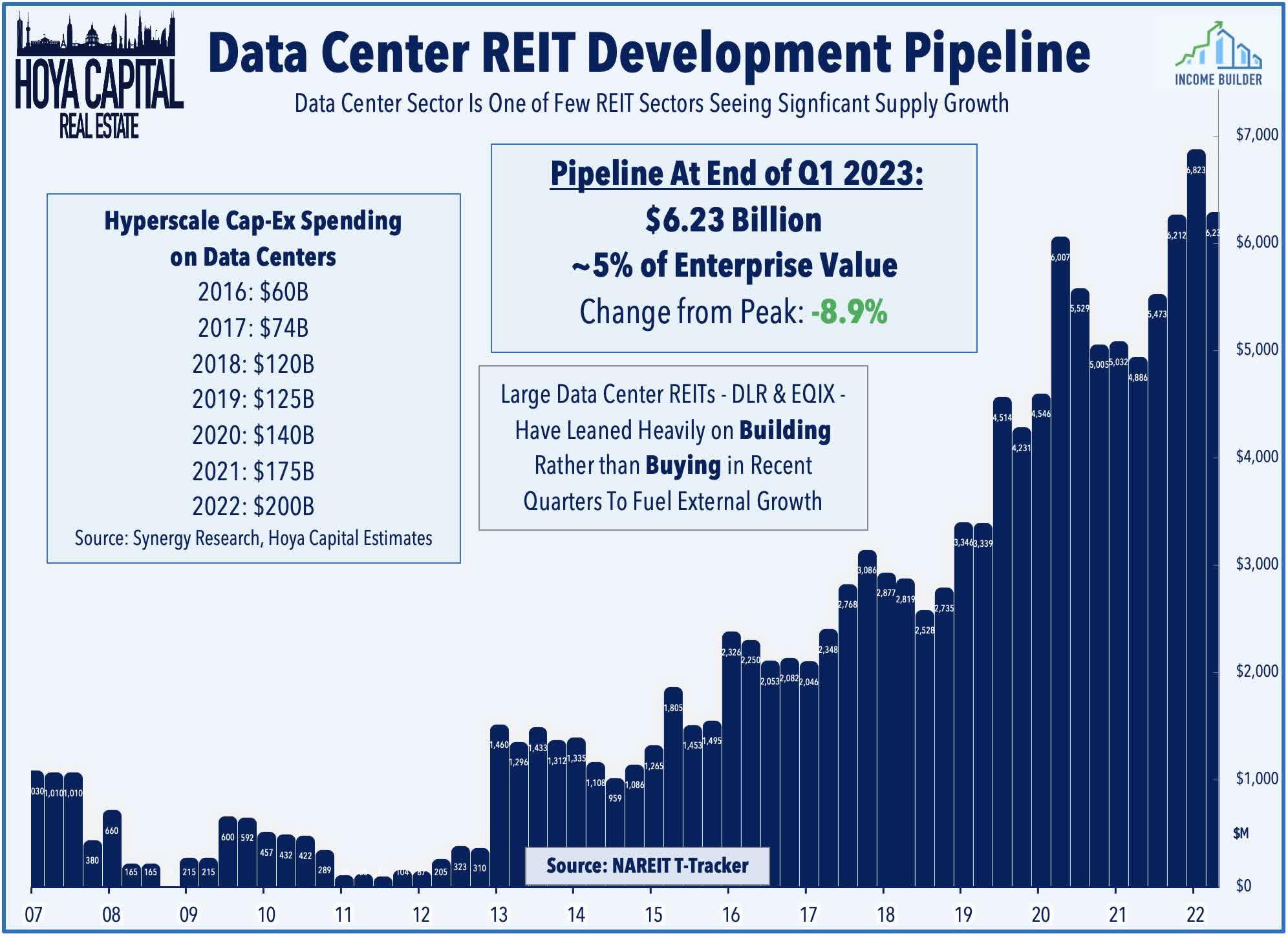

Citing a confluence of development bottlenecks - power shortages, a higher cost of capital, supply chain constraints, and politics/NIMBYism - supply has fallen behind demand in recent quarters, allowing these REITs to achieve record-high occupancy rates and to finally push rent growth. These development headwinds are having a particularly acute effect on Northern Virginia - the data center "capital" of North America - while European markets are also seeing resistance to new development at multiple levels. These REITs reported that the development pipeline stood at $6.2B in Q1, which was 9% below the peak levels from 2022 and commentary suggests that industry-wide development will continue to tail-off through the year given these bottlenecks.

{kind=link}

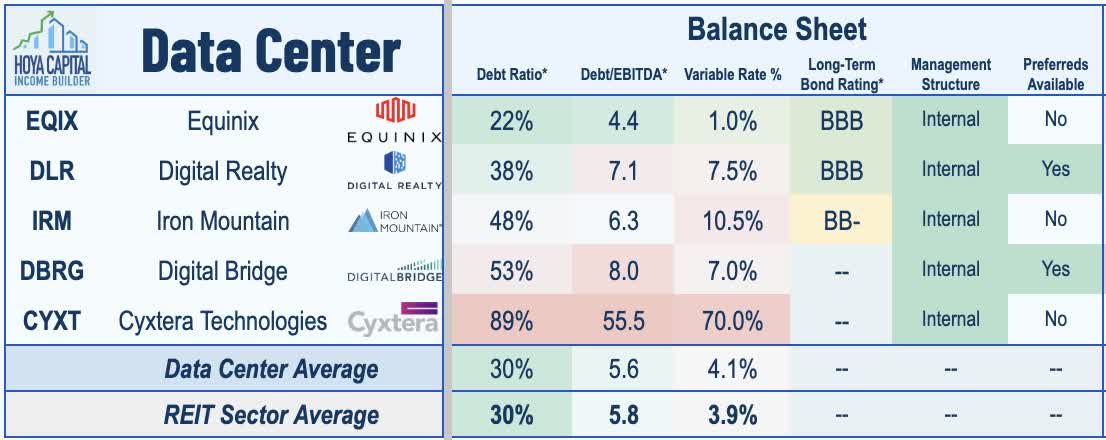

Equinix and Digital Realty were notably quiet on the acquisition front amid the frenzy of M&A activity during the pandemic. Their patience appears to be quite prudent in hindsight, allowing these REITs to de-lever their balance sheets and avoid a more pronounced drag from higher rates, while also positioning them to be aggressors as other more-highly-levered private players seek an exit. High debt loads - and specifically high variable rate debt exposure - appear likely to take down a fourth former competitor in the space - Cyxtera – which had planned to convert to a REIT this year following its SPAC listing in 2021. After failing to attract M&A interest from its larger peers and failing to refinance its variable rate debt, Cyxtera announced this week that it filed for Chapter 11 and plans to restructure through a pre-packaged bankruptcy as part of an arrangement with its lenders.

{kind=link}

Three data center REITs were acquired last year, including Blackstone's ( BX ) acquisition of QTS Realty , KKR's ( KKR ) acquisition of CyrusOne , and cell tower REIT American Tower's ( AMT ) acquisition of CoreSite. We're now down to two major REITs after DigitalBridge announced its transition to a conventional C-Corp as it focuses its strategy on its fee-based investment management business. DBRG also reached a deal last May to acquire Switch ( SWCH ) - an operator that had planned to convert to a REIT by 2023. Other companies operating space include a mix of international, private, and "c-corp" entities, including Rackspace ( RXT ), TierPoint , Flexential , Cologix, Lumen (formerly CenturyLink), and Global Switch .

{kind=link}

Data Center REITs Performance

As noted above, Data Center REITs are among the top-performing property sectors this year, a rebound that has been augmented by reports of "booming" demand for artificial intelligence ("AI") focused data center chips and by strong earnings results from these REITs showing impressive pricing power. So far in 2023, the Hoya Capital Data Center Index is higher by 8.1% - trailing only the Single Family Rental and Industrial REIT sectors - while outpacing the 1.0% gain from the Vanguard Real Estate ETF ( VNQ ). Data center REITs are still among the better-performing REIT sectors over most longer-term measurement periods, with 5-year total returns of roughly 9.7% - roughly six percentage points above the broader REIT average during that period.

{kind=link}

Data Center REIT Dividend Yields

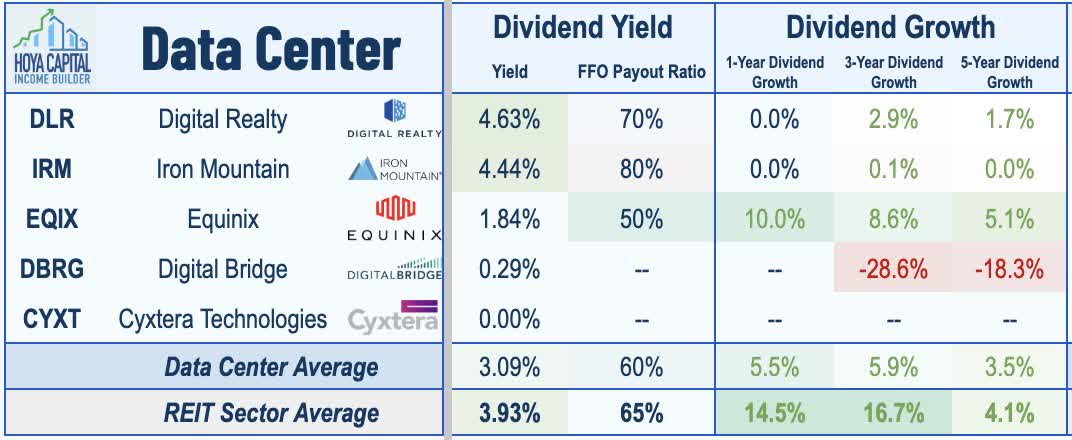

Few property sectors have delivered more consistent dividend growth than data center REITs, as Equinix and Digital Realty are among a small handful of REITs that raised their dividends every year through the pandemic. Still very much a "growth-oriented" property sector, data center REITs pay an average dividend yield of 3.1%. DLR commented at REITweek that it "does not see the risk to the dividend," pushing back on recent speculation from a contingent of short sellers that have had data center REITs in their cross-hairs since mid-2022. Specialty REIT Iron Mountain pays a dividend yield of 4.44% while paying out 80% of its FFO. Equinix pays a yield of 1.84% while paying out just 50% of its FFO. DigitalBridge , meanwhile, reinstated its cash dividend at $0.01 in the third quarter last year, fulfilling a pledge made to reinstate the dividend that the firm made before its decision de-REIT.

{kind=link}

Takeaways: Positive Inflection in Fundamentals

Even before the AI-driven rally, Data Center REITs were on the upswing in early 2023 after an impressive slate of earnings results showed improved pricing power and record-high occupancy rates. Ironically, this AI-wave and improving fundamentals comes just as Data Center REITs became a trendy “short” idea centered on a thesis of weak pricing power and competition from the "hyperscalers." Instead, a confluence of development bottlenecks - power shortages, higher cost of capital, supply chain constraints, ecopolitics, and NIMBYism - have created a more favorable dynamic and swung the pendulum of pricing power towards existing property owners. Barriers to supply growth combined with AI-accelerated demand should bring some sustained pricing power to a sector long-burdened by near-unlimited supply. The market concentration of data center REITs shouldn’t be discounted either as these REITs have built relatively dominant platforms through M&A and new development, and market share gains are more likely to increase rather than decrease in an environment of constrained capital availability.

{kind=link}

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Data Center REITs: Physical Epicenter Of AI