SPLK - Datadog: 90% Of IT Spend Is Still On-Prem

2023-10-20 08:30:00 ET

Summary

- In 2020 and 2021, and even most of 2022, Datadog, Inc.'s valuation kept me away from the business.

- Today, with a chunk of its competition having been taken private or in the process of being taken private and its valuation more attractive, I like the business much more.

- Of course, it's a phenomenal company, and I likely do not need to tell you that, as a follower of the business.

- That said, I think a consideration of its valuation and its business in conjunction would be worth your while, and I will do just that for you today.

- In short, I like Datadog stock here, though I still don't love it, as incredible as that may be. The valuation excesses of 2020 and 2021 were so incredible that we may need another year or two for $90/share to become really compelling. In the mid-double digits, I like it a lot and have placed capital in accordance with this penchant.

My History With Datadog

In October 2020, I and my team at the time shared with my community and readers research on Datadog, Inc. (DDOG). At the time, I determined that Datadog was a high-quality business, but I could not make sense of the valuation.

That is, Datadog's valuation implicitly suggested that it would grow at something like 40-50% annualized for 10 years consecutively, which I felt was far too optimistic.

As such, our central takeaway was that either Datadog stock would decline precipitously or - and we thought this to be the more likely scenario - Datadog would simply stagnate for about five years before sales growth finally caught up with its valuation, pushing the stock higher in the process.

This essentially played out exactly as we expected: From 2020 to today, Datadog has more or less stagnated, with one precipitous collapse occurring in late 2022, during which time we began buying the business.

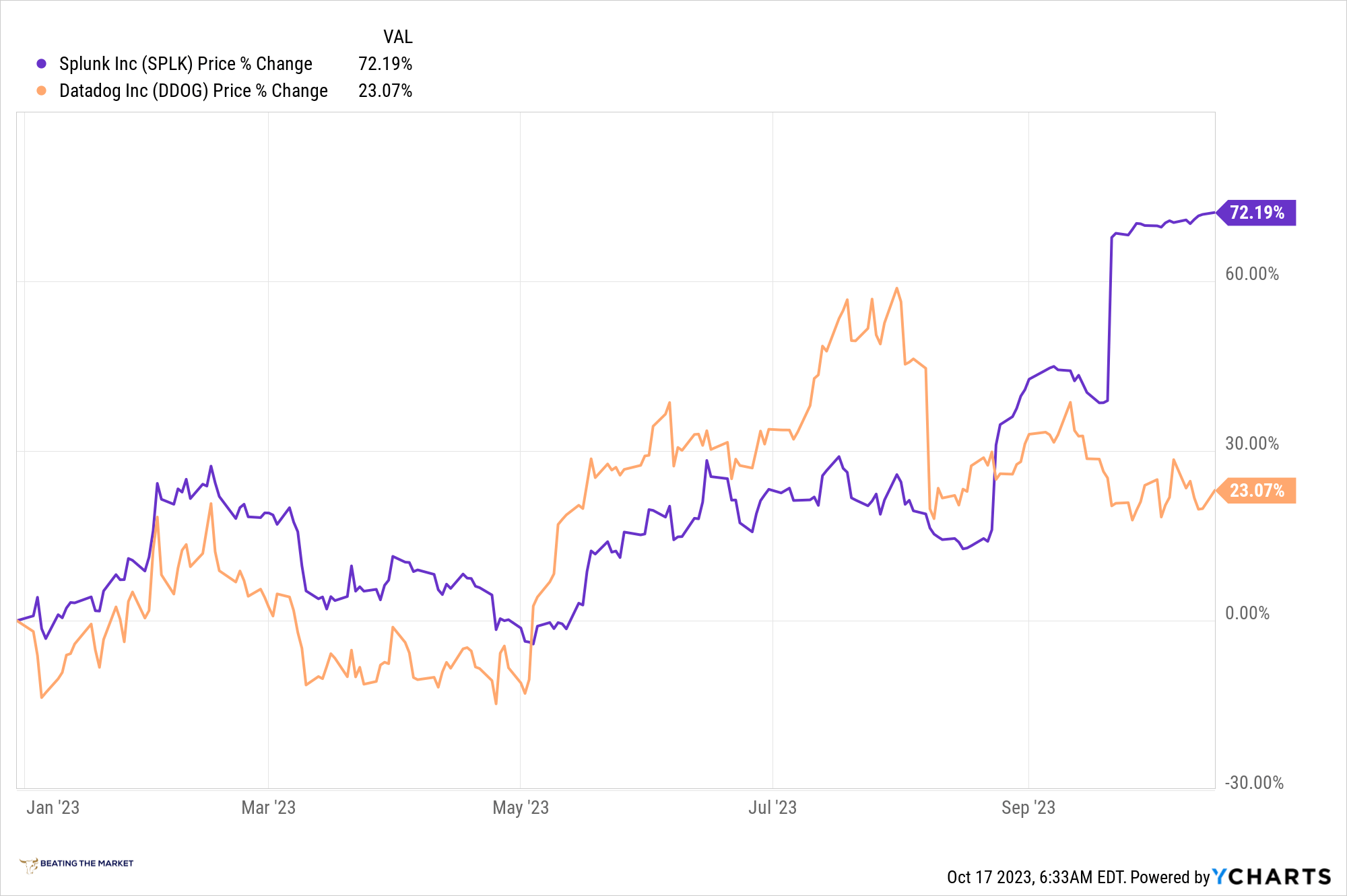

Additionally, over the last 6 months or so, I've been focused on Splunk's turnaround beginning to accelerate; as such, we've been buying Splunk routinely instead of Datadog, and this has played out well.

Splunk Vs Datadog YTD Returns

{kind=link}

With Splunk Inc. (SPLK) having entered into a definitive agreement with Cisco Systems (CSCO), in which both boards have agreed to the acquisition at $157/share, the competitive landscape of public competitors to Datadog is set to be pared down quite significantly.

NewRelic and Splunk will both have been removed from the public market competitive landscape, and I think there's some chance that Elastic N.V. ( ESTC ) will go the way of Splunk over time as well.

This will likely serve to reduce competitive pressures on Datadog, making it more attractive to me. As such, I will likely more routinely begin covering the business, starting with today's review.

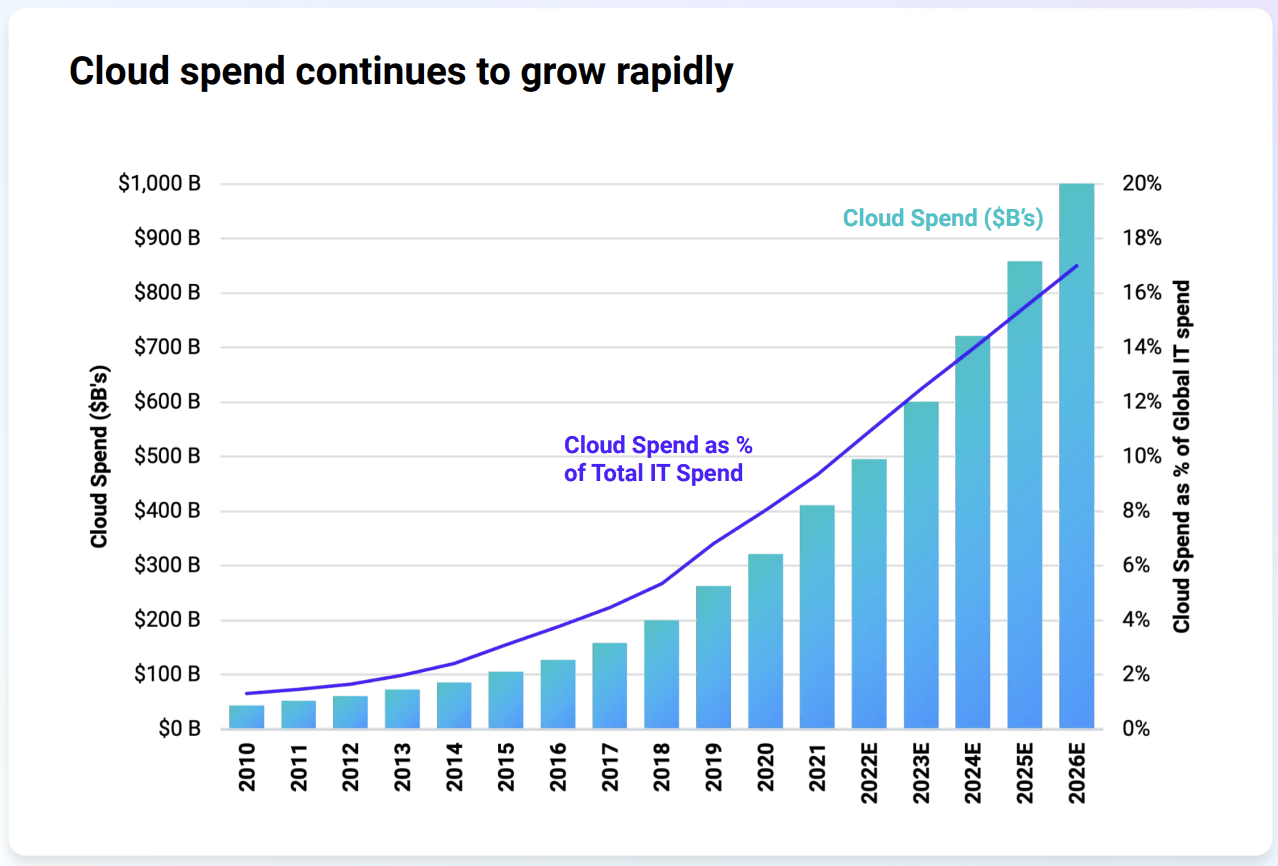

A Notable Chart: Datadog Has A Long Runway For Growth

In a recent review for subscribers of Amazon (AMZN), I shared an important quote from CEO Andy Jassy, in which he stated that cloud computing penetration of total IT spend remains at only 10%.

We've spent a fair bit of time analyzing what we're seeing, and I've spent a good chunk of time myself looking as well, and we like the fundamentals of what we're seeing in AWS. The new customer pipeline looks strong. The set of ongoing migrations of workloads to AWS is strong. The product innovation and delivery is rapid and compelling.

And people sometimes forget that 90-plus percent of global IT spend is still on-premises. If you believe that equation is going to flip, which we do, it's going to move to the cloud. And having the cloud infrastructure offering with the broadest functionality by a fair bit, the best securing operational performance and the largest partner ecosystem bodes well for us moving forward.

Andy Jassy, CEO, Amazon Q1 2023 Earnings Call (emphasis added).

Coincidentally, Datadog shared a chart that reflects this assertion from Mr. Jassy, which you may review below:

Cloud Spend As A % Of Total IT Spend Globally

Datadog Q2 2023 Earnings Presentation

{kind=link}

I believe this chart is important for our ownership of Datadog, as well as the ownership of many of our cloud computing businesses, e.g., monday.com Ltd. (MNDY), Snowflake (SNOW), SentinelOne (S), and CrowdStrike (CRWD), to name only a few.

It also largely illustrates why I like to invest in software: there's still a very long runway for quality cultures, with proven abilities to execute and capture market share, to grow their enterprises, and, by extension, share prices.

That said, while the long-term outlook remains quite attractive for software businesses, objectively, it has been quite a tough sledding in the sector for the last 20 or so months.

There was still a little bit of customers thinking about cost control, optimization and things like that, but we also see less. So when that kicks in [more aggressive spend by customers], in terms of the overall growth in aggregate, as David said, it's too early to tell, and we want to be careful there because we know sometimes our customers will not know everything themselves. They might face more difficulties as they go. But we're very optimistic about the mid, long term, obviously.

Olivier Pomel, DDOG CEO, Q2 2023 Earnings Call .

Mr. Pomel's optimism, of course, relates to the long-term opportunity associated with the growth of cloud computing depicted in the chart I shared with you just a moment ago.

I believe he felt compelled to note the long-term opportunity specifically because, as I mentioned, it's been tough sledding for about 20 months, and, based on Datadog's guidance, it's likely not going to get materially better anytime soon. Indeed, we are in something of a downcycle in software, as enterprises of all sizes around the world take note of the fastest interest rate hiking cycle in American history and the second and third order effects that may have (such as bank failures and an imminent recession).

And, of course, Datadog is not alone in the headwinds it has experienced: Other usage-based software businesses, such as Amazon Web Services, Twilio (TWLO), and Snowflake, have likewise experienced rather extreme collapses in their growth rates.

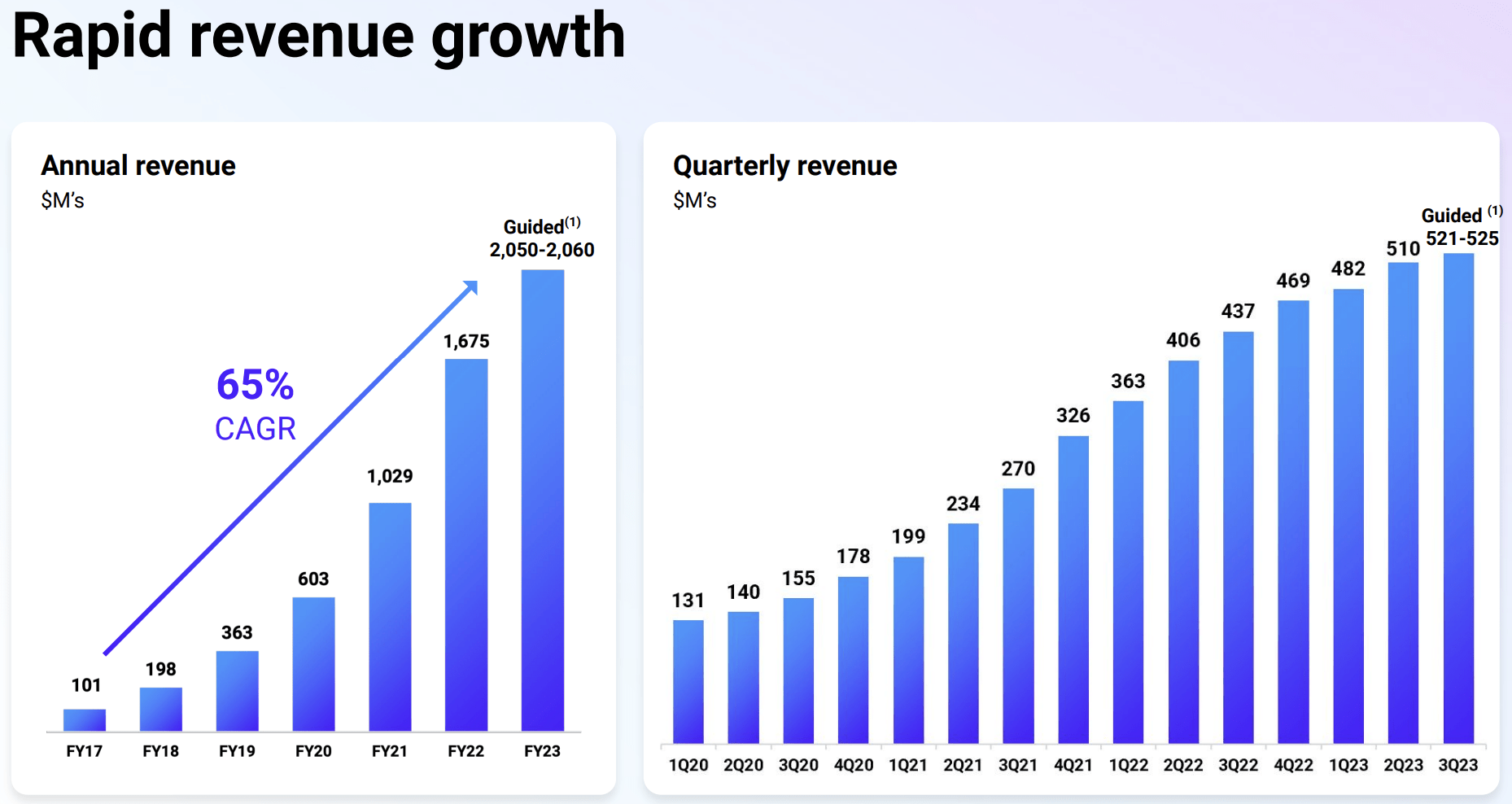

We can see Datadog's slowing growth rates in the flattening sequential growth depicted in the chart below:

Datadog's Flattening Revenue Growth

Datadog Q2 2023 Earnings Presentation

{kind=link}

Mark Murphy of J.P. Morgan noted Datadog's growth struggles by stating,

And then for all these reasons, should we be optimistic on growth picking up just relative to how it's going to exit in Q4 of this year, which I think is around -- which I think is around the mid-teens? And I know it's hard to answer because you haven't guided on that yet or would you be imagining, David, that we might kind of just drag across that 15% into 2024 as a starting point.

Datadog Q2 2023 Earnings Call (emphasis added).

I remember speaking with a Splunk employee about a year ago, and he raved to me about Datadog. I asked him why he didn't like Splunk more, especially in light of the valuation, and he stated that Datadog was just a superior platform. I share this to highlight that the business has been one of the darlings of the software community for the last half-decade or so.

It is, indeed, an exceptional, dynamic, highly durable business, growing within a very large addressable market.

To this end, it's fairly incredible to see the business guide for mid-teens growth at this stage in its lifecycle, but it's also very much par for the course following the fastest interest rate hiking cycle in American history.

Visual Capitalist

As we've discussed often recently, higher rates, all else being equal, serve to create a drag on economic growth, which, in turn, serves to slow the growth rates of businesses within an economic system experiencing higher rates.

That said, Monday, Axon (AXON), CrowdStrike, and others have demonstrated the ability to fend off the impacts of higher rates on their growth rates to some degree.

It's actually a bit surprising to me that Datadog would experience a deceleration, if only in the imagination of its guidance for now, into the mid-teens for its growth rate. In light of its likewise very high-quality peers' sustained, elevated growth through this software downcycle, this guidance has surprised me.

But, of course, this period of economic uncertainty and reduced usage of software will eventually abate, and I believe it's likely that Datadog will accelerate growth once again.

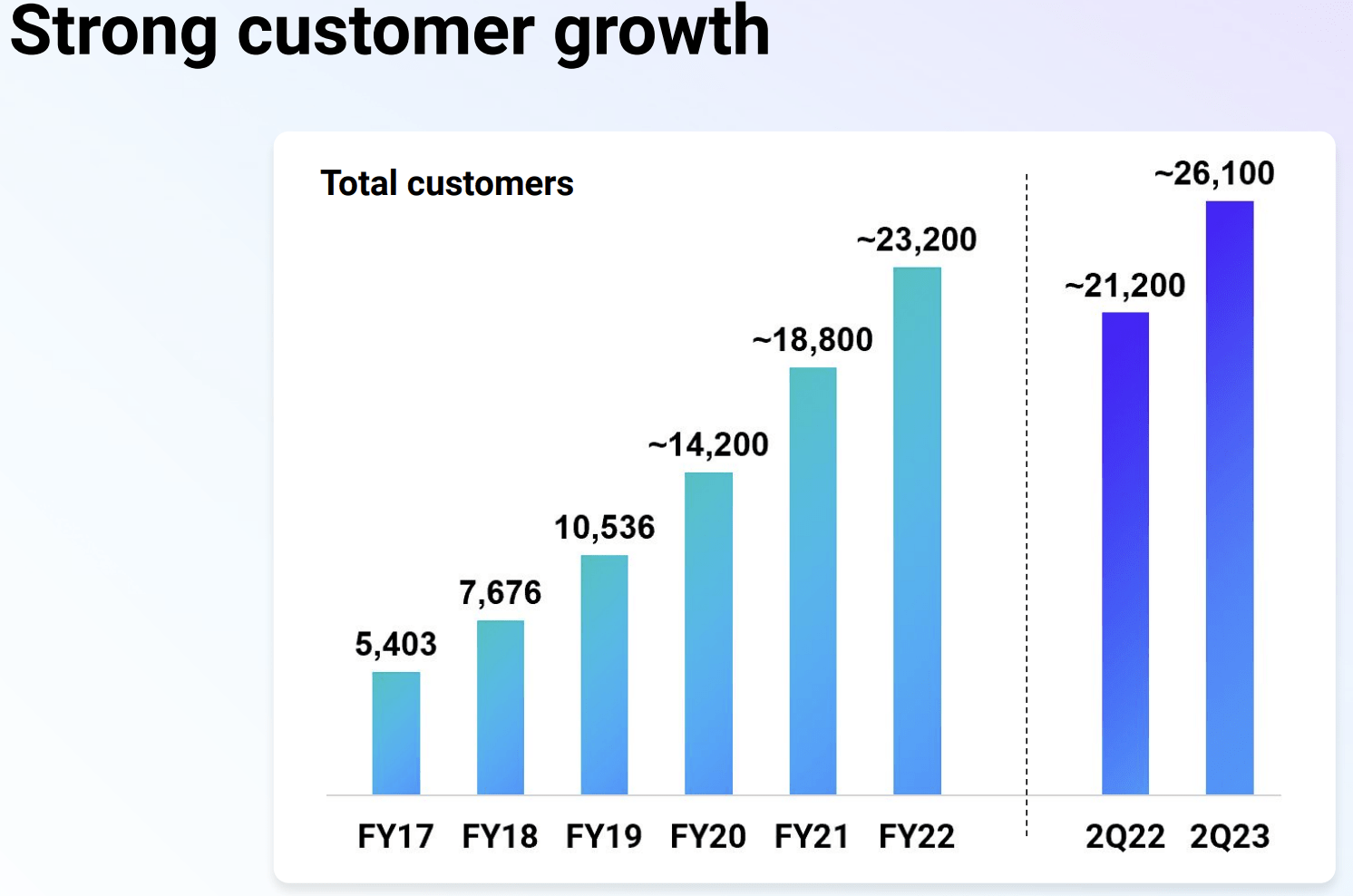

Sustained Customer Growth

Datadog continues to grow its customers at a very healthy rate, as you can see below.

Datadog Q2 2023 Earnings Presentation

{kind=link}

From a new logo bookings perspective, we had our largest Q2 and second largest quarter ever , only behind the seasonally larger Q4 2022. We also closed a record number of new business deals larger than $100,000 in annual commitment.

And with our land and expand model, we expect new logos to turn into much larger customers over time as they lead into the cloud, and add more of our product.

So as a conclusion, while we do apply conservatism to our guidance, recent usage trends as well as strong new logo activity and customer ramp-ups are positive signs for our future growth.

Olivier Pomel, CEO, Q2 2023 Earnings Call (emphasis added).

It's heartening to me to see that Datadog continues to grow its new logos at such a high pace.

Specifically, it is heartening to me because I am aware of how valuable each of these customers could be over the next 5, 10 and 20 years. In this vein, I recently remarked, in a review of Splunk's Q1 2023,

A Fascinating Case Study

As mentioned above, Splunk has struggled to win new logos, and it makes sense when the leadership team was gutted for consecutive years.

That said, there is nothing stopping Splunk from continuing to evolve its holistic platform.

But, over the last few years, it has not had to because it has been able to upsell its current expansive roster of clients new products.

I found this dynamic particularly interesting: Splunk has more than doubled its total sales over the last few years, while not adding customers at the rate at which it should.

I believe this demonstrates the very attractive nature of the SaaS business model. I believe this demonstrates that, for instance, S1 or Snowflake could grow for the next few years by simply continuing to evolve their platforms and selling new products into their existing client base.

I believe this also illustrates that our companies have vastly longer runways than the market has been giving them credit for over the last six months.

Source (emphasis added).

Interestingly, Datadog actually provides tangible data with which we could create some estimation of future value for each of its customers.

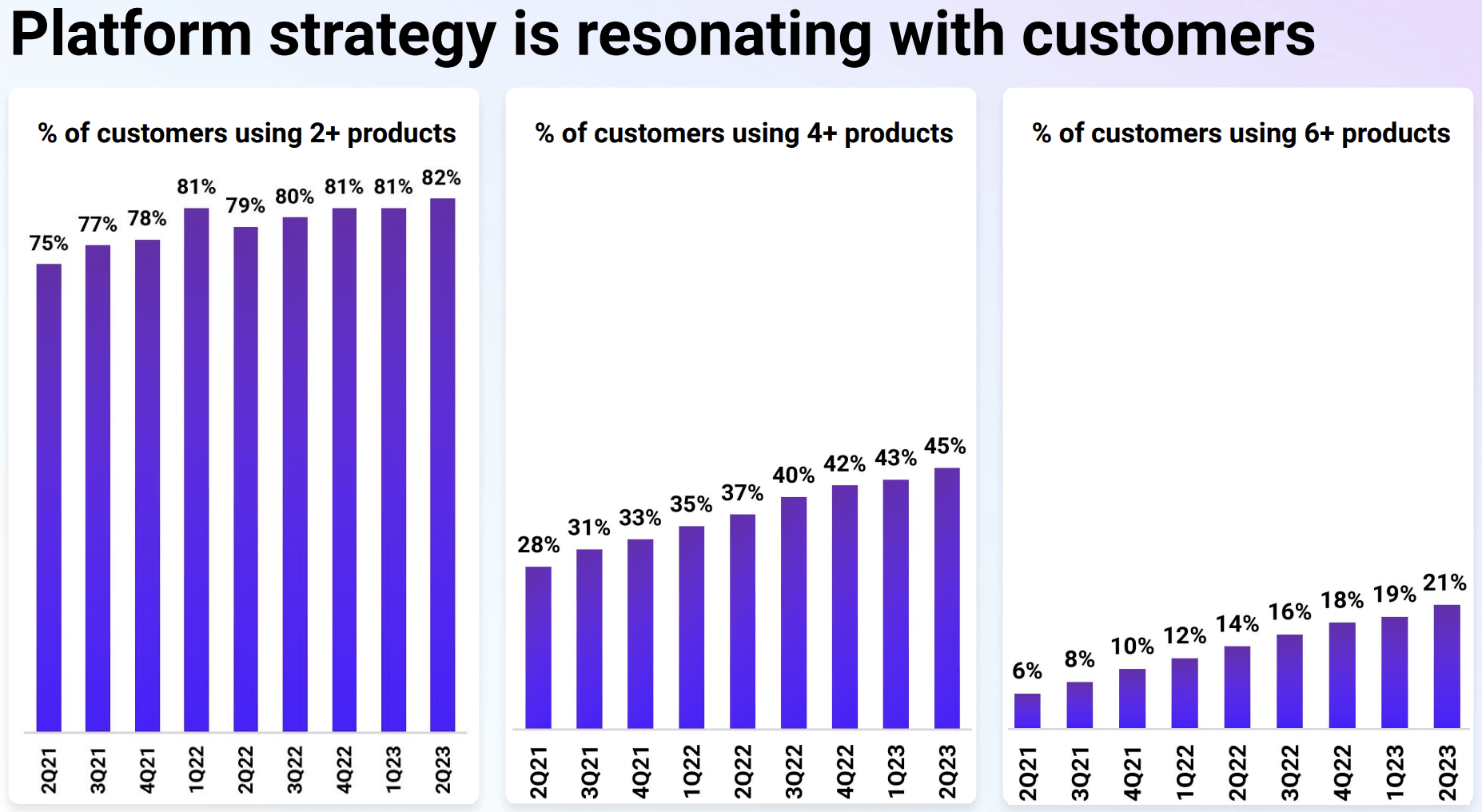

Below, we can see the % of customers using x number of products.

Datadog Q2 2023 Earnings Presentation

{kind=link}

The two columns on the righthand side illustrate that Datadog could arguably 2x to 3x its $2B run rate business via upsells of current customers alone.

It wouldn't need to add any new logos to achieve this.

That said, Datadog will continue to add new logos, and it will simultaneously continue to upsell its current customers, creating an outstanding engine of value creation in the decade ahead; near-term slowdown notwithstanding.

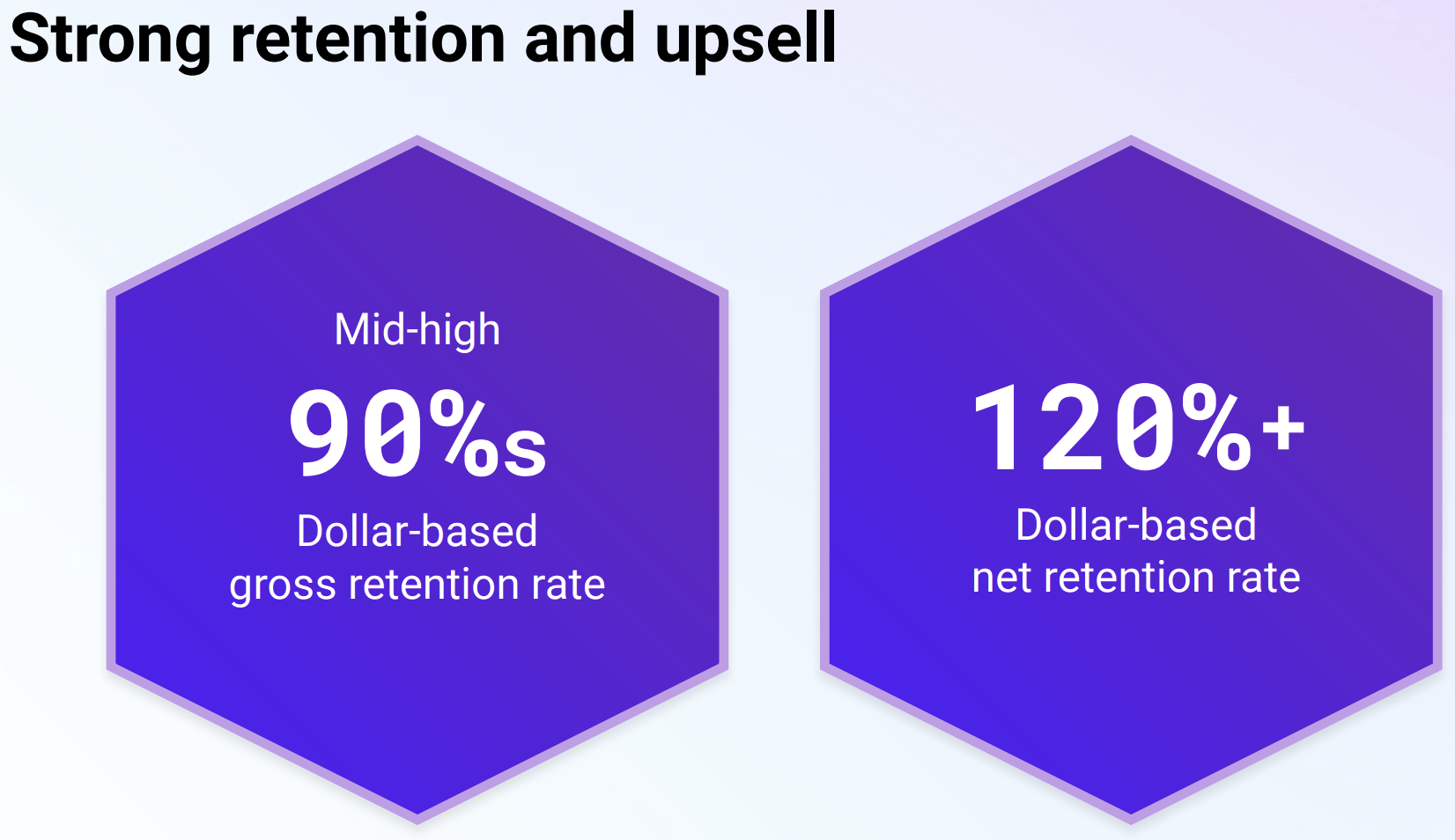

Now turning to platform adoption. Q2 metrics show that our platform strategy continues to resonate in the market. As of the end of Q2, 82% of customers were using two or more products, up from 79% a year ago. 45% of customers were using four or more products, up from 37% a year ago, and 21% of our customers were using six or more products, up from 14% a year ago.

The strong multi-product adoption include expansion into our newest products. About 30% of our customers have already adopted at least one of our products launched since 2021, including CI visibility database monitoring, cloud security management, sensitive data scanner, cloud craft and others. We expect more opportunities to expand adoption of these products as we continue to broaden their capabilities over time.

Olivier Pomel, CEO, Q2 2023 Earnings Call.

Datadog's multi-product execution has been arguably the best in software over the last half-decade, the reality of which has caused its valuation to expand to the degree that we avoided it for years prior to making it a new Top Idea at $68/share recently.

This multi-product execution has produced a series of benefits for the business that you, as a reader of my work, likely know quite well by now, especially after the encyclopedic explorations of the value "going multi-product" that I've shared with you over the last 70 or so days.

Datadog Q2 2023 Earnings Presentation

{kind=link}

In the interest of brevity, I won't reproduce my explanations of the value of going multi-product with you today, but I will share an abridged, enumerated version.

A successful ability to "go multi-product" renders the following benefits to a company:

- Expanded avenues to "go to market" that help accelerate total sales growth

- Ecosystem "lock-in" that creates embedding/switching costs moat

- A more diversified, durable business with multiple streams of revenue.

If you'd like a more in-depth exploration, I'd invite you to read my most recent work on monday.com, which has been masterfully executing the strategy of "going multi-product":

Axon has also been doing a phenomenal job in this respect:

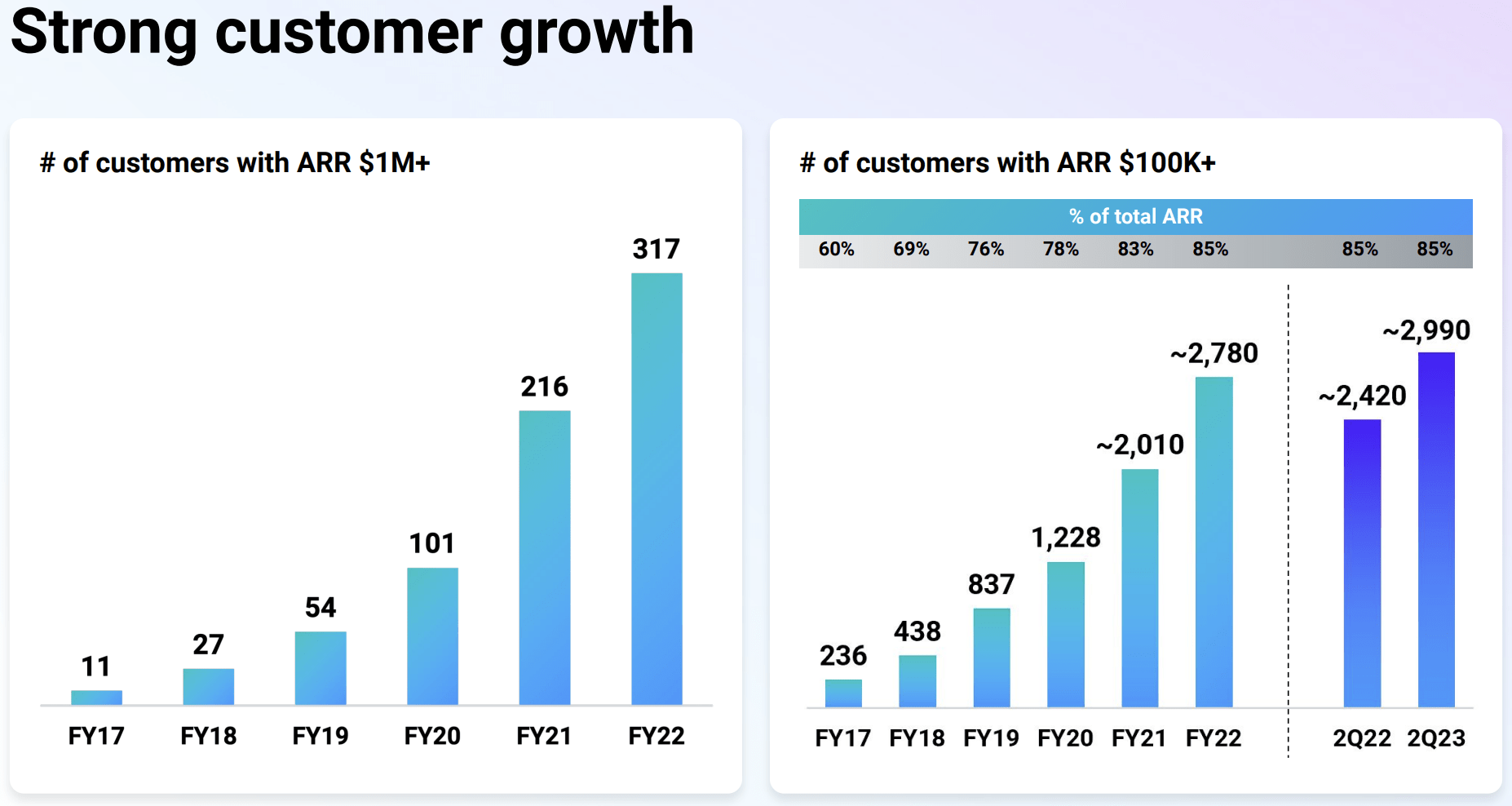

In accordance with point one, Datadog has many avenues to go to market, wedge itself into customers' wallets , and expand over time. We can see the fruits of this business model in the growth of large customers, which very likely started as smaller customers using fewer products, below:

Datadog Q2 2023 Earnings Presentation

{kind=link}

Concluding Thoughts: Incredibly, I Still Don't Absolutely Love Datadog, Though I Like It Much More Today

As I noted earlier, I've been a buyer of Splunk throughout 2023, as opposed to Datadog, with great success.

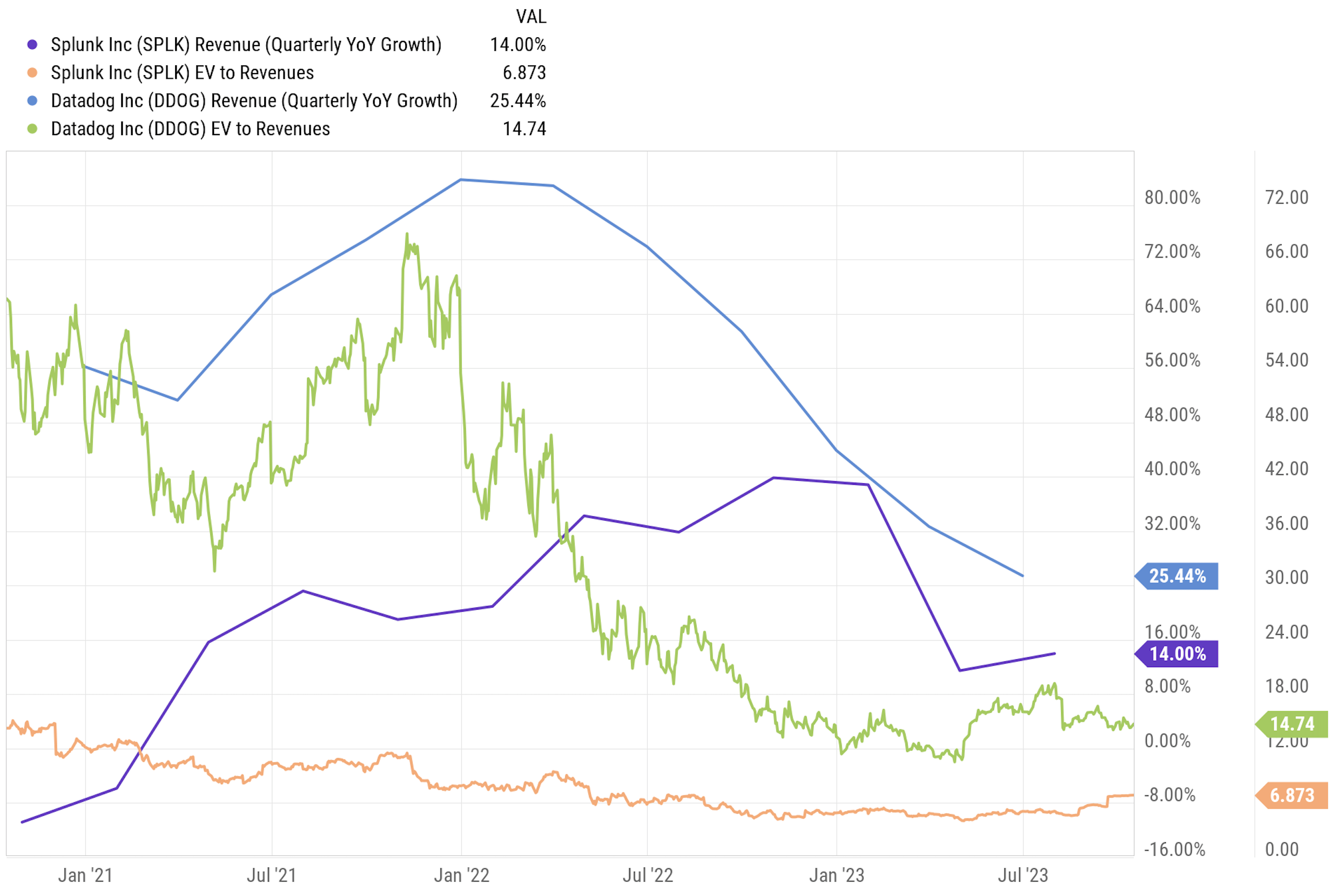

Interestingly, as of today, Splunk and Datadog are growing at approximately the same rate; yet, one trades for ~14x EV/sales and the other trades at about 7x EV/sales.

Based On Guidance, Splunk Will Likely Grow At 15% Q4 2023 And Datadog At Roughly 18-20% Q4 2023

{kind=link}

Both have approximately the same free cash flow margins, at roughly 25%.

To some degree, I have been disappointed with Splunk's buyout price, as this math indicates that Splunk could fetch as much as $200/share, and, over the last 6 months, I did note that, from $100/share, Splunk could have 100% upside.

This rough math substantiates as much.

That said, we've done well with Splunk and Datadog over the last 12 months or so, leveraging a focus on valuation to make wise purchases with both, and I believe we'll get a couple more big swings at Datadog, Inc., akin to our late 2022 purchase.

Over time, as Datadog becomes more quantitatively attractive, I will share this thinking with you and highlight the opportunity it may come to present.

Thank you for reading, and have a great day.

For further details see:

Datadog: 90% Of IT Spend Is Still On-Prem