ARCO - Dave & Buster's Entertainment: Navigating A Broken Balance Sheet

2023-04-17 07:28:58 ET

Summary

- PLAY has a unique business model combining food, drinks, and games under one roof, which has been successful in attracting a wide range of customers.

- PLAY has a mixed financial track record, with impressive revenue and free cash flow growth but a balance sheet that raises concerns.

- The company has potential to be a sound investment opportunity in today's market if it can fix its balance sheet.

Intro

Dave & Buster's Entertainment ( PLAY ) is a popular entertainment and dining destination that has been gaining traction among consumers in recent years. The company's unique business model, which combines food, drinks, and games under one roof, has proven to be successful in attracting a wide range of customers, including families, young adults, and sports fans. However, PLAY's financial track record has been mixed, with impressive revenue and free cash flow growth but a balance sheet that raises concerns.

In this article, we will provide an in-depth analysis of PLAY's business model and financial performance, as well as its prospects for future growth. We will examine the company's revenue and profitability trends, free cash flow generation, and balance sheet strength. Additionally, we will estimate PLAY's intrinsic value using various valuation techniques to provide investors with insights into whether the company is a sound investment opportunity in today's market.

Business Model

Dave & Buster's Entertainment is a leading American restaurant and entertainment chain with over 140 locations across the United States and Canada. The company's unique concept combines delicious food with interactive games and attractions, providing an unparalleled experience for customers of all ages.

Dave & Buster's offers a wide range of menu options, including burgers, wings, and desserts. The company prides itself on using high-quality ingredients to create delicious, satisfying meals that keep customers coming back for more. In addition to its food offerings, Dave & Buster's also features a full bar with a variety of cocktails, beers, and wines.

The entertainment side of Dave & Buster's is what truly sets it apart from other restaurants. The chain offers a variety of games and attractions, including arcade games, virtual reality experiences, bowling, billiards, and more. Customers can win tickets playing games, which they can then redeem for prizes at the company's Winner's Circle.

Dave & Buster's also host a variety of events, including birthday parties, corporate events, and team building exercises. The company's experienced event planners can help customers create a customized event that meets their specific needs and budget.

In 2022, Dave & Buster's made a total of $1.2 billion in sales. The company's primary market is North America, where it operates over 130 locations. Dave & Buster's is committed to providing a safe and clean environment for its customers and has implemented a variety of health and safety measures in response to the COVID-19 pandemic.

Track Record

Dave & Buster's Entertainment has had a mixed financial track record over the past decade. Despite growing revenue by an impressive 208% over the last 10 years, the company has struggled with its balance sheet. PLAY's current ratio is a cause for concern, with the company only having a current ratio of 0.67. Furthermore, PLAY's debt-to-equity ratio is extremely high at 6.82, indicating a significant amount of leverage.

Data by Stock Analysis

PLAY has seen impressive free cash flow growth over the past decade, but it should be noted that this growth may be skewed by an easy comparison point, as the company only had $4.2 million in free cash flow to start with. Nonetheless, the fact that PLAY has been able to increase its free cash flow by 4923% over the last 10 years is still an indication that the company has been able to generate strong cash flows from its operations. This is a positive development for investors, as free cash flow is an important metric to track as it can be used to fund future growth initiatives, pay dividends, and pay down debt.

Data by Stock Analysis

Another area where PLAY has performed well is in generating high returns on equity (ROE). Over the last 10 years, PLAY has averaged an impressive 25% ROE. However, it's worth noting that this figure does not include 2020, the year of the COVID-19 pandemic. The pandemic had a significant impact on PLAY's business, as many of its locations were closed for extended periods of time, resulting in a substantial decline in revenue.

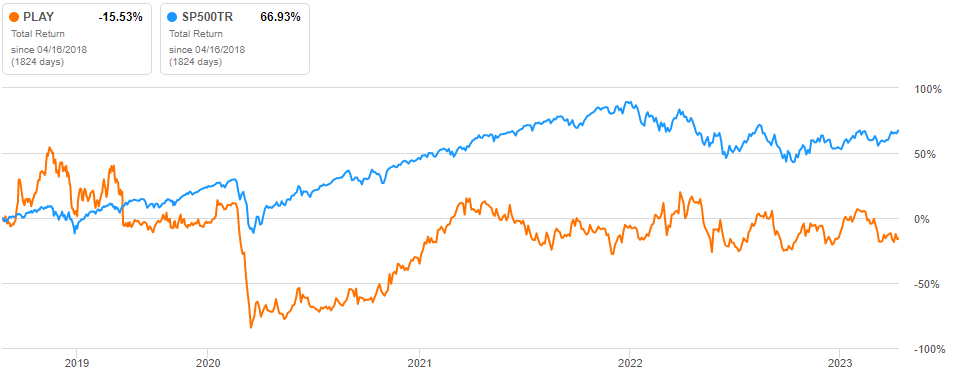

Despite these challenges, PLAY has remained committed to investing in its business and driving growth. Unfortunately, the company's total return has not kept pace with the broader market, with PLAY lagging the S&P 500 by a significant margin. Over the past five years, PLAY's total return has been -15.53%, compared to a total return of 66.93% for the S&P 500. This underperformance is a concern for investors, and it highlights the challenges that PLAY faces in driving long-term growth while also managing its balance sheet effectively.

{kind=link}

Outlook

When evaluating PLAY's future outlook, it is important to consider the company's strategy and its potential for growth. PLAY's strategy for growing the business is based on three key components which include driving growth of comparable stores sales, investing domestically in its brands, and investing internationally.

One key component of PLAY's strategy to drive comparable store sales is its focus on offering novel food and drink and the latest entertainment to drive growth in comparable sales. This is a promising approach, as it indicates that the company is continuously innovating and staying up-to-date with consumer trends. If PLAY is successful in differentiating its brands and offering unique experiences to customers, this could drive increased foot traffic and revenue.

Another important aspect of PLAY's strategy is its focus on creating a fun experience for customers by aligning its team and improving service excellence. If PLAY can create a positive and engaging atmosphere for customers, this could lead to increased customer loyalty and repeat visits.

In addition, PLAY is planning to invest domestically in its brands through the opening of new stores. The company opened up eight new stores in 2022 and is planning to open many more in 2023 and beyond which is a sign of confidence in its ability to drive growth. However, it is important to note that this approach also carries risks, as the success of new stores is dependent on a number of factors, such as location, competition, and consumer demand.

Additionally, PLAY is investing in growth outside of the United States. In September 2022, the company finalized a franchise agreement to initiate the expansion of Dave & Buster's locations in the Kingdom of Saudi Arabia, with plans to expand to the United Arab Emirates and Egypt. In addition, its recent acquisition of Main Event gives PLAY another brand to develop globally. If done correctly, investors should feel positive about PLAY's international expansion since it provides opportunities to grow the company's top and bottom lines.

Valuation

To estimate PLAY's intrinsic value, we will perform a discounted cashflow analysis. We will start the DCF by using the average free cash flows of PLAY from the previous five years, which is $91 million. We will then use a growth rate of 5.88% per year for the next ten years, considering the average analyst growth estimates for the next few years.

We will assume a growth rate of 2.5% per year following the 10th year to find the company's terminal value. The discount rate used to discount the cash flows will be 10%, which is based on the long-term return of the S&P 500 when dividends are reinvested.

{kind=link}

Based on these inputs, the DCF analysis suggests an intrinsic value per share of $32.30 for PLAY. This reflects a possible loss of 8% for investors. However, it is essential to note that the DCF analysis relies heavily on the assumptions made, and it is not a guarantee of future performance. Therefore, it is crucial to use other valuation techniques to determine the intrinsic value of the business.

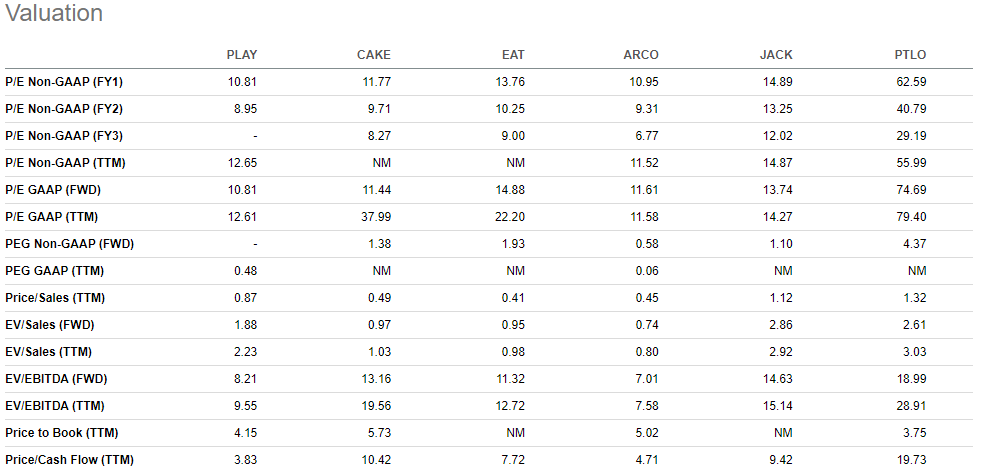

Seeking Alpha has a really nice "Peers" page which offers a comparison of PLAY against its industry rivals, using various popular valuation ratios. These ratios include the price-to-earnings ratio (P/E), price-to-sales ratio (P/S), price-to-book ratio (P/B), and many more. For each of these ratios, a lower number indicates better value for the company. By simply averaging these ratios together, we can identify the most undervalued company by seeing which company has the lowest score.

{kind=link}

Based on the given scores, it appears that PLAY has the second lowest valuation compared to its peers, with a score of 6.69. This suggests that PLAY may be undervalued compared to its industry rivals.

Arcos Dorados Holdings Inc. ( ARCO ), which is a McDonald's franchisee that operates and licenses McDonald's restaurants in 20 countries and territories across Latin America and the Caribbean, appears to have the best score of 5.91, indicating that it may also be undervalued.

On the other hand, Portillo's Inc. ( PTLO ), which is a popular fast casual restaurant chain based in Chicago, ended up with the highest score of 30.38, which means that it may be overvalued compared to its peers. Overall, these scores provide a helpful indication of how these companies' valuations compare to each other.

Takeaway

PLAY has a mixed financial track record, with impressive revenue and free cash flow growth but a balance sheet that raises concerns. The company has a unique business model combining food, drinks, and games under one roof, which has been successful in attracting a wide range of customers. However, the PLAY's valuation is unclear as it appears cheap when compared to industry rivals but a little expensive based on a discounted cash flow analysis.

PLAY has a good strategy for growing the business which is based on driving growth of comparable stores sales, investing domestically in new store growth, and investing in internationally expansion, and if successful, this could drive increased foot traffic and revenue. Overall, PLAY has potential to be a sound investment opportunity in today's market, but investors should hold until the balance sheet concerns are resolved.

For further details see:

Dave & Buster's Entertainment: Navigating A Broken Balance Sheet