DAVE - Dave: Fintech Pioneer With Digital Banking Tailwinds

Summary

- Dave has developed a digital banking application that offers many unique features from zero overdraft "free cash" to side hustles.

- Its platform has 7.8 million members and the company increased its revenue by a rapid 48% year over year.

- Dave is poised to benefit from the growth in the digital banking industry and increased engagement in its ecosystem.

Dave ( DAVE ) is a fintech company that has developed a unique banking application. Founded in 2017, the company took the brave position to offer zero overdraft fees and "free credit" which helped to entice millions of users onto its platform. In the third quarter of 2022, the company continued to produce strong financial results, beating its revenue growth estimates and increasing monthly transacting members by 26% year over year. The fintech industry is forecast to grow at a 17.2% compounded annual growth rate [CAGR] and reach a value of $949 billion by 2030. Digital banking applications are expected to be a key part of this growth as they aim to disrupt the traditional banking industry. In this post I'm going to break down Dave's fintech business model, financials, and valuation, let's dive in.

Fintech Business Model

Dave's primary business involves its banking mobile application and associated debit cards. Its platform enables its customers to track expenses in an intuitive and easy-to-understand manner, in order to help users save, track and spend easily. Its brand philosophy is to focus on "caring" for its customers and has taken a different route from many traditional banks. A key selling proposition is Dave doesn't charge overdraft fees, as these reportedly cost Americans $12.4 billion in 2020. Dave has framed its value proposition with unique features such as "ExtraCash". This enables a user to borrow up to $500 until their next payday, and automatically deducts it from the account. The beauty of this system is the platform doesn't charge any interest rates or fees, or even do a credit check! I believe the only way the platform can maintain this business model is to keep the amount borrowed low ($500) and potentially track if a direct debit from a salaried job is still enabled. The "ExtraCash" is a key part of Dave's growth strategy to acquire new members it effectively offers "free credit", which has helped to accelerate a platform through viral word-of-mouth growth.

{kind=link}

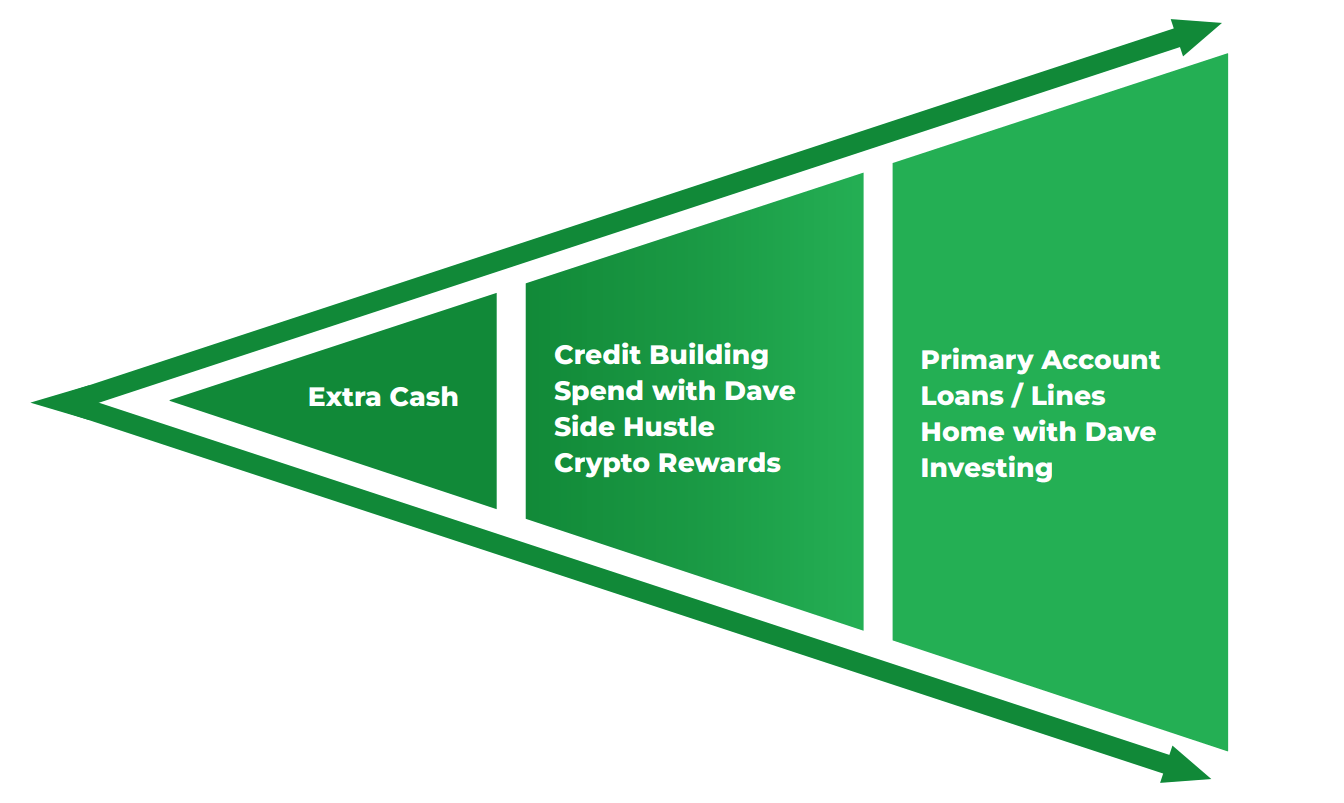

Another unique feature the Dave app offers is "Side Hustles", this enables a customer to look on the app for extra money-making tasks. These include, doing surveys and even dog walking. Financial apps are becoming more social and aim to not just help users save money, but also make money. I believe Dave is ahead of the curve in this regard as I've not seen other apps, such as Revolut with similar systems. Dave has also expanded into "Crypto rewards" and is building out its primary loans business.

Dave fintech (Investor Presentation )

{kind=link}

Dave is not technically a bank, but works with a partner bank in this case "Evolve Bank & Trust". This bank holds the deposits of Dave's app customers and issues the debit card product. Its management believes this is a great model until enough scale is reached to get its own banking license.

Growing Financials

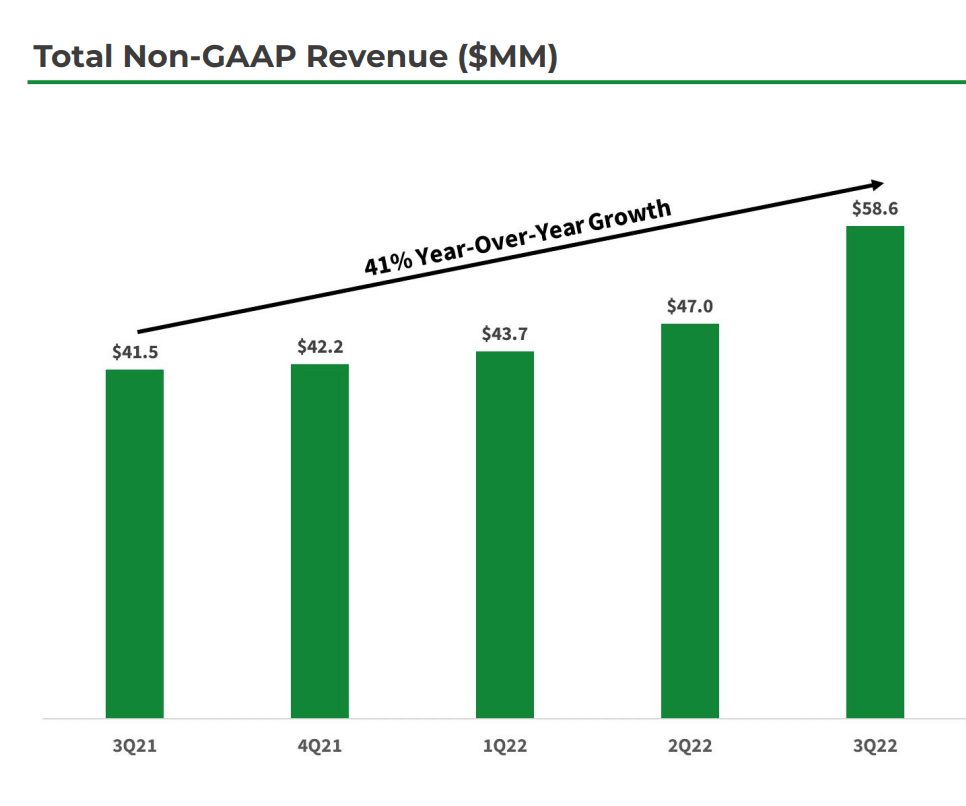

Dave reported strong financial results for the third quarter of 2022. Revenue was $58.6 million, which beat analyst estimates by $3.25 million and increased by over 41% year over year.

{kind=link}

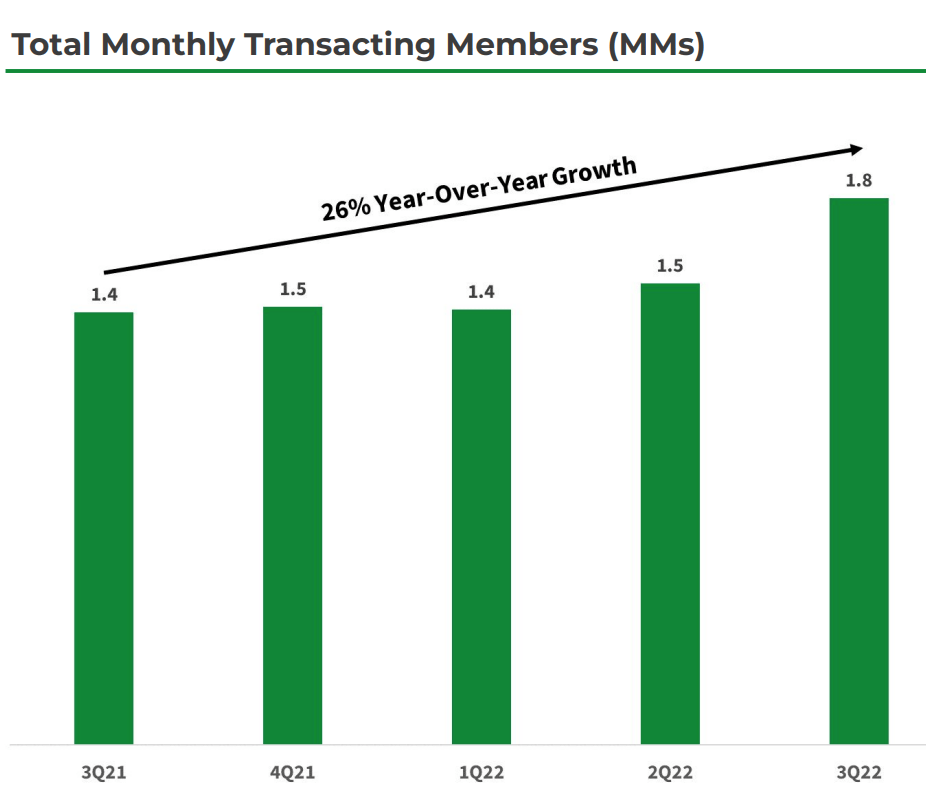

The top line was driven by strong customer acquisition, engagement, and retention. Dave's total members increased by a rapid 36% year over year to 7.8 million. Its total "multi-transacting" members, increased by 26% year over year to 1.8 million. This metric was also up a blistering 105% since 2020 which is a strong positive.

Monthly transacting members (Q3,22 report)

{kind=link}

The beautiful thing about Dave's "Free cash" value proposition is it has helped to drive member growth while driving down Customer Acquisition Cost [CAC] in the latter half of Q3,22. The business has expanded its marketing mix, which has resulted in new channels being discovered that have helped to drive more cost-effective growth. Its product also gains strong traction among the millennial cohort and younger, which is positive news for the potential lifetime value of each customer. Banking applications tend to be fairly "sticky" with users as once they change over their direct debits, most will stay for a considerable period.

A key component of Dave's success has been the launch of its card product in 2020. This has helped to deepen engagement with the platform and I believe it adds a brand "realism" to a virtual application. For example, management reported in its earnings call that direct deposit members transact using the Dave Card around 40 times per month, which is substantial. Its ExtraCash portfolio also continued to perform strong and increased by a blistering 110% year over year.

Advance origination Volume (Dave)

{kind=link}

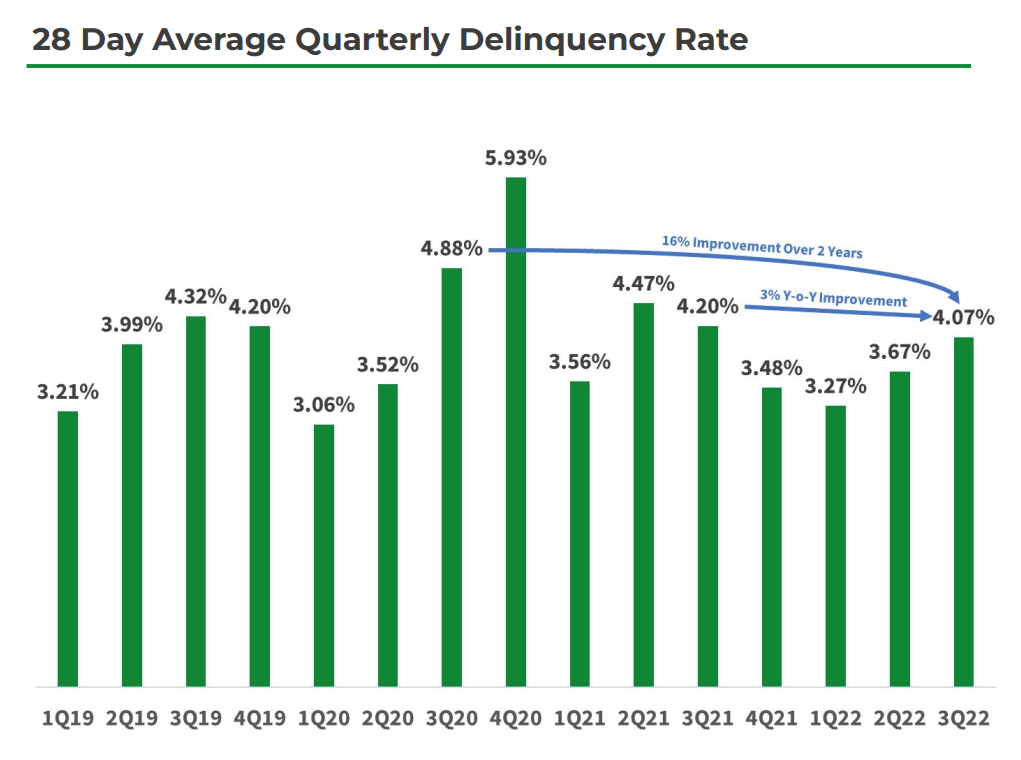

A key metric to watch for financial applications is the "delinquency rates" which is basically the percentage of loans overdue (lower is better). In this case, Dave's 28 day Delinquency rate has improved 3% year over year. This is a positive sign given the "recessionary" environment and the cost of living increases. However, I would note that its DQ rate has been fairly volatile and there is not a consistent downward trend yet.

Delinquency rates (Q3,22 report)

{kind=link}

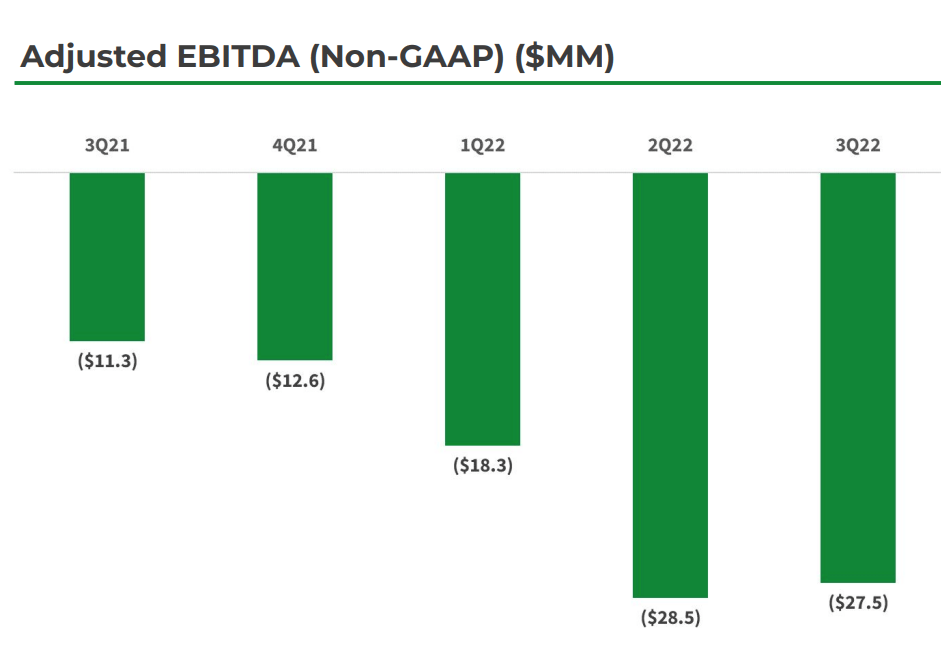

In Q3,22 Dave reported a non-GAAP variable profit of $24.7 million, at a 42% margin, which increased by 280 basis points quarter over quarter. However, operating income was negative $37.9 million, which was substantially worse than the negative $15.7 million reported in the prior year. Adjusted EBITDA also showed a similar trend with negative $27.5 million reported, which was worse than negative $11.3 million in the prior year. This increase looks to have been by a 70% increase in "unrecoverable advances" to $18.4 million. This was partially driven by a general increase in ExtraCash originations (which was positive). However, the company also had a sizeable but "one off" fraud event.

Adjusted EBITDA (Q3,22 report)

{kind=link}

Dave has a solid balance sheet with $223.9 million in cash and short term investments. In addition, the company has total debt of $167.4 million of which the majority, $146.6 million is long-term debt and thus manageable.

Moving forward management has guided for operating revenue of between $200 million and $215 million, for the full year of 2022. In addition, the company is expecting margin improvements with EBITDA profitability forecast by 2024. This EBITDA profitability forecast may seem like a long way of, given the current declining trend. However, assuming its "one off" fraud event contributed substantially to losses in this quarter, it is achievable but still challenging.

Advanced Valuation

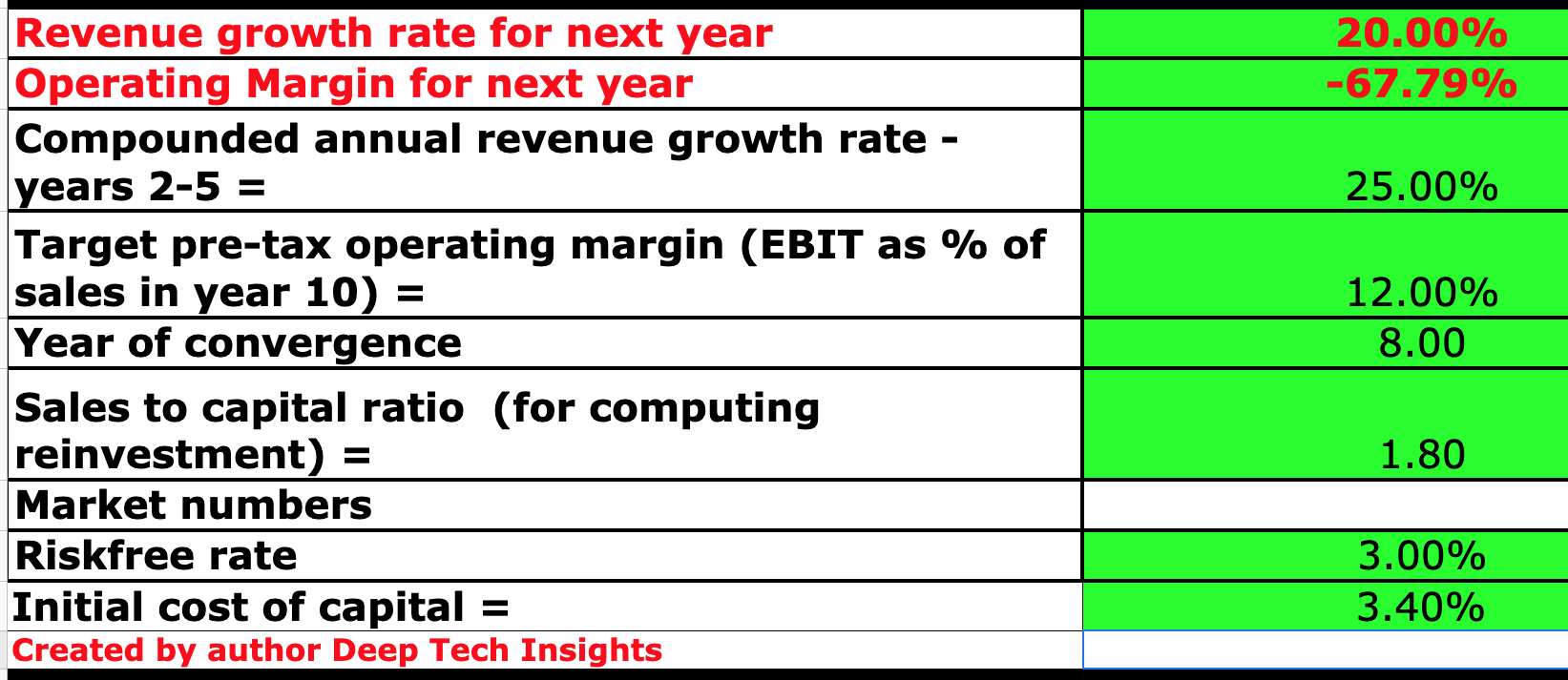

To value Dave I have plugged its latest financials into my discounted cash flow model. I have forecast 20% revenue growth for next year, which is lower than the 30% growth forecast for the entire year of 2022. I have forecast slowing growth to the macroeconomic environment and expected recession (more details in the Risks section). However, in years 2 to 5 I have forecast 25% growth per year, as I believe economic conditions will improve.

Dave stock valuation 1 (created by author Deep Tech Insights)

{kind=link}

I forecast Dave to increase its operating margin to 12% within the next 8 years, which is the average for the financial services (nonbank) industry. I forecast this to be driven by increased member growth, and engagement inside its entire ecosystem. This should then boost further transactions, loans etc. In addition, I am expecting further declines in the cost of customer acquisition [CAC], as per the current trend. Management has reported approximately 50% of its customers come from organic channels, which is a strong positive for the scalability of its profitability.

Dave stock valuation 2 (Created by author Deep Tech Insights)

{kind=link}

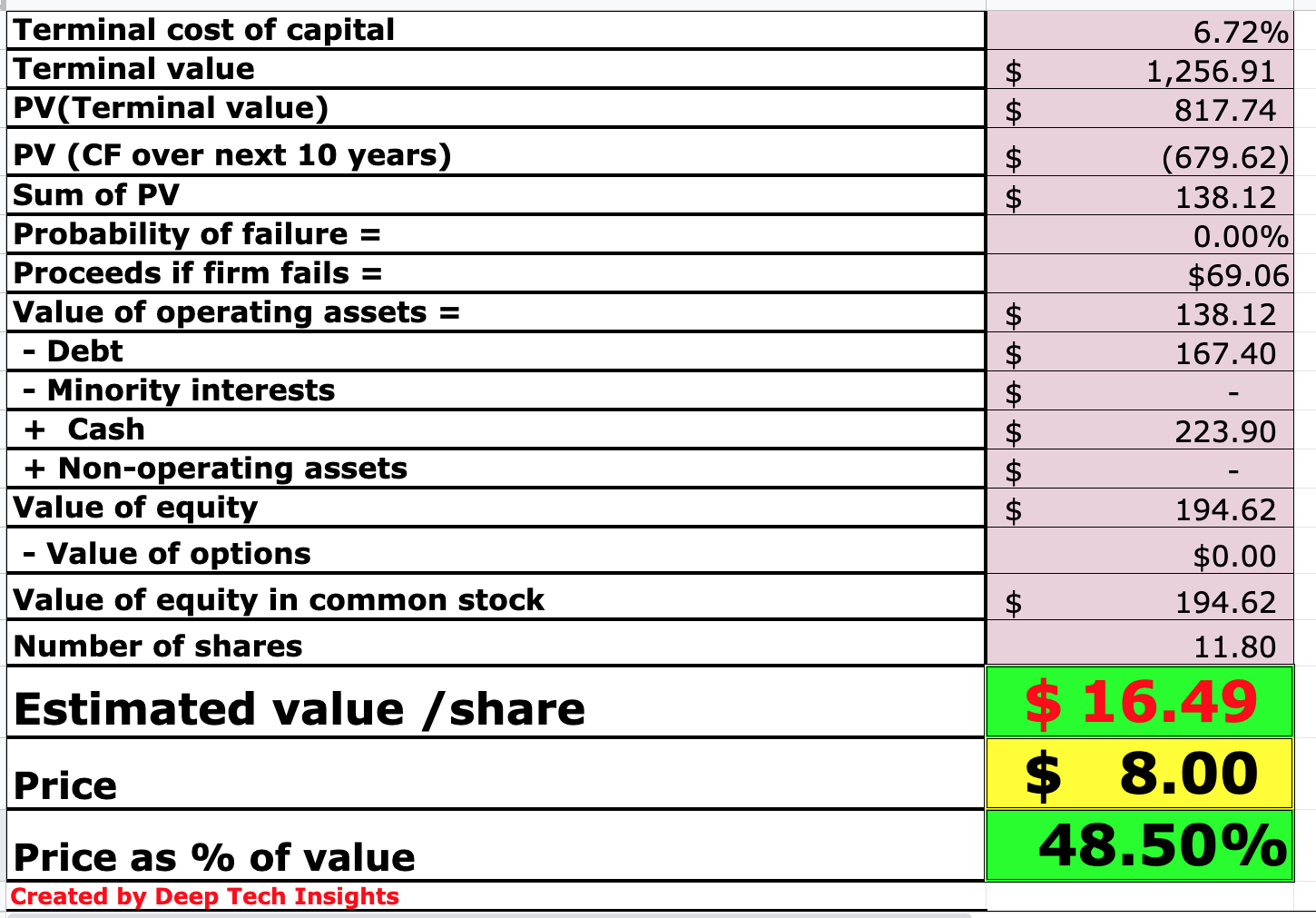

Given these factors I get a fair value of $16.49 per share, the stock is trading at ~$8 per share at the time of writing and thus is over 50% undervalued.

As an extra datapoint, Dave trades at a price-to-sales ratio = 0.43, which is cheaper than industry peers such Block ( SQ ) and SoFi ( SOFI ).

Risks

Recession/Loan Defaults

Many analysts have forecast a recession which is bad news for the financial industry as it generally results in lower payment volume, engagement and higher defaults on loans. This could be a particular risk for Dave, as even though its free cash proposition only offers up to $500, if a consumer loses their job in between the borrowing then that could result in the company losing out.

Growing Losses/Capital Raise/Bankruptcy

Dave reported a "cash burn" of ~$38 million in the last quarter. Therefore if the business produces the same result is as ~5.8 quarters' worth of cash left. This would mean the company would likely have to raise capital again in the future which would dilute shareholders. A positive is this seems unlikely given the company's strong top-line growth and focuses on driving down its customer acquisition cost. However, I believe it will be best to watch for operating loss improvement in the next quarter and see if the "one-off" fraud event in the prior quarter was the only major impact. If losses continue to increase and the company doesn't seem on track for its EBITDA profitability by 2024, then that could be a great time to abandon the bullish thesis.

Final Thoughts

Dave is a popular fintech company that is loved by millions of members and offers a series of unique features. The company has continued to grow its customers at a rapid rate, while also driving down its acquisition costs. The business still has a long way to go to improve its overall margins, but given the stock is over 50% undervalued this looks to be a great long term investment.

For further details see:

Dave: Fintech Pioneer With Digital Banking Tailwinds