DAVE - Dave: Losses May Extend And Remain Sticky

2023-06-22 13:22:53 ET

Summary

- I expect near-term losses to widen due to plans to increase marketing spend.

- I also feel that losses may not only extend but also stick, suggesting that the model entails expensive growth, until Dave can prove otherwise.

- My modeled target price of $4.92 for FY 2023 suggests that the stock is fully valued to slightly overvalued at present. I rate Dave neutral.

Dave ( DAVE ) is a digital banking app that aims to deliver various financial products and services, such as cash advances and budgeting tools. Dave is a relatively unique company in the digital banking space due to its business model, where it generates revenue primarily from the subscription of its budgeting tool and optional instant transfer fees and tips from using its cash advance offering, "ExtraCash".

Furthermore, unlike traditional banks with their own deposit products, Dave partners with Evolve (a Banking-as-a-Service provider) to provide a deposit product to its customers. As a result, despite being labeled as a digital bank, Dave does not generate revenue through the typical net interest spread. Instead, it earns deposit referral fees as part of its partnership with Evolve.

Currently trading between $5-$6 per share, the stock is now down ~39% from January this year, when it had a reverse stock split .

A potential near-term catalyst may enable Dave to deliver growth profitably. However, my view is that given the nature of the business, there remains a key risk that Dave may continue to see challenges in optimizing its cost structure as it accelerates growth in the near term. The management's expectation to increase marketing spend in Q2 and beyond may put further pressure on profitability. Meanwhile, Dave will also expect revenue growth to decelerate to 11%-23% in FY 2023.

At this time, I rate the stock neutral. My target price model suggests that at the current price, Dave remains fully valued to slightly overvalued.

Risk

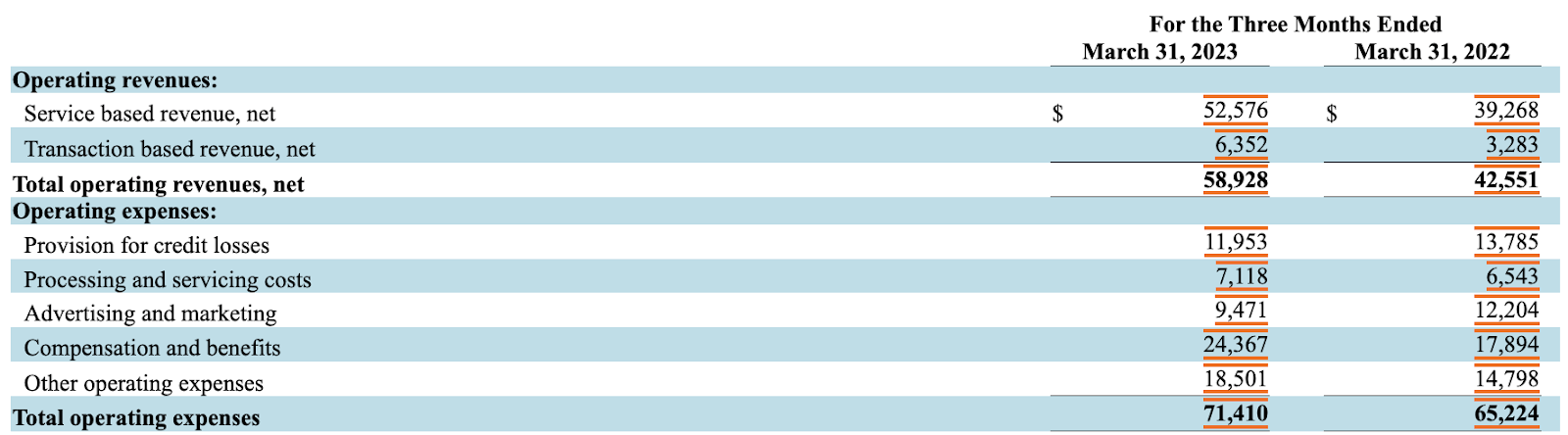

Despite the relatively steady revenue growth above 30% as of Q1, Dave has been unprofitable and generating negative operating and free cash flows/OCF and FCF. As Dave has been primarily relying on cash flow from financing as the main source of liquidity, widening losses may impact FCF and effectively the liquidity outlook, in spite of the relatively safe cash level today.

Furthermore, my biggest concern today is that losses may not only continue but also remain sticky. I feel that Dave will struggle to bring down key operating expenses/opex items that have been driving its negative operating losses, primarily due to their structural importance to Dave's operational activities.

{kind=link}

These two items have been compensation and benefits/C&B and other opex. C&B includes third-party and in-house call center costs, as well as general salaries, while other opex includes technology and infrastructure costs, processor fees, losses from transactions, and bank card fees and fraud. Given what these activities entail, I expect that they may continue to rise alongside user growth and number of transactions.

Together, they represent the largest operating expenses, and it appears that Dave has not been able to achieve operating leverage here - they have consistently been steady as a % of revenue, instead of trending down. C&B has been the biggest expense item as % of revenue, representing ~40% of revenue on average. Meanwhile, other opex has generally been ~30% of revenue, but in Q1, it even increased to ~31% of revenue.

Given their sizes and necessities to Dave's operations, I believe that they will also continue to drive operating expenses and be relatively sticky. In Q1, for instance, Dave was able to deliver ~38% revenue growth despite bringing down marketing spend by ~22% YoY, but C&B and other opex increased by 36% and 25% consecutively and remain relatively flat YoY as % of revenue.

With Dave ramping up marketing spend in Q2 and beyond to grow its user base, I would then expect losses to widen, even if we assume that C&B and the other Opex items as % of revenue remain flat.

{kind=link}

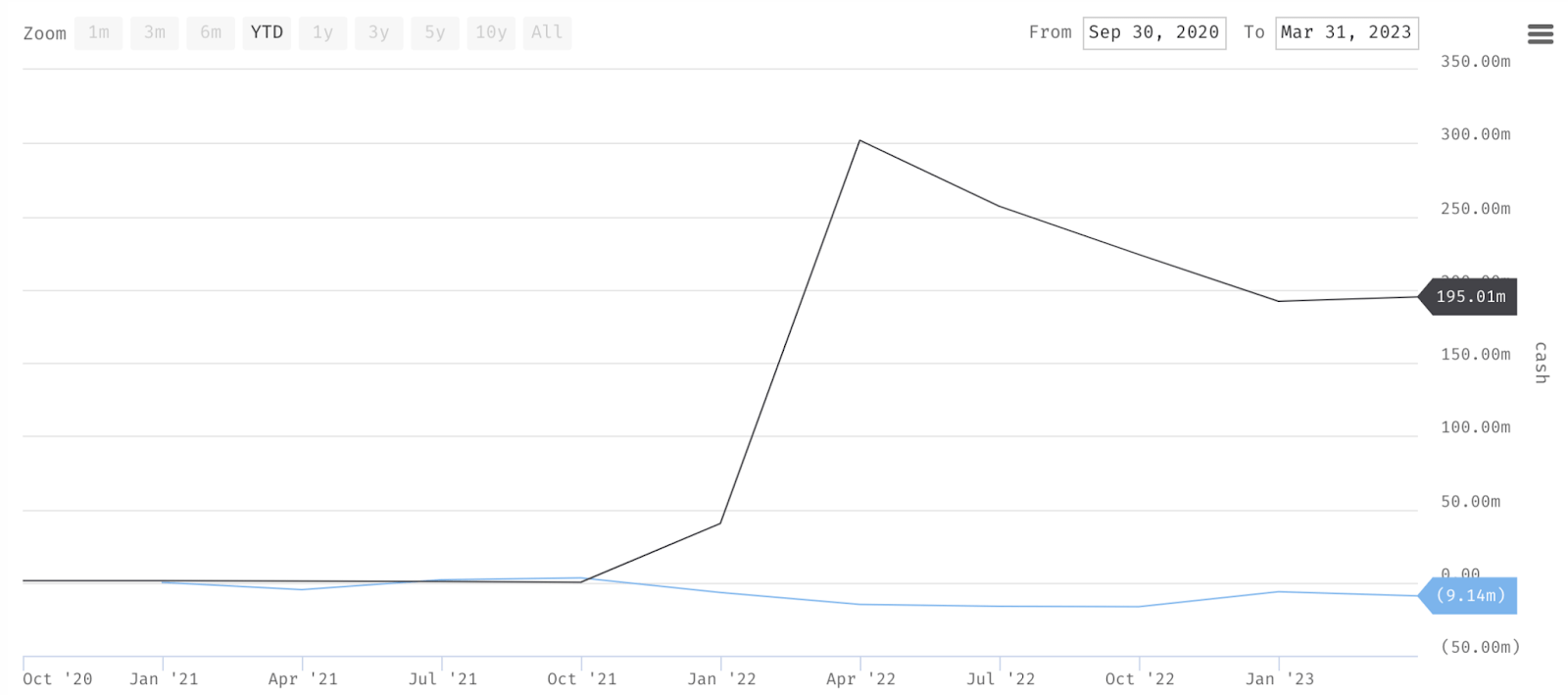

On the other hand, increased marketing spend may also threaten medium-term liquidity. Though Dave's cash and cash equivalent/CCE level is probably at a safe level for the next 12-18 months, growing FCF losses may potentially shorten that runway.

{kind=link}

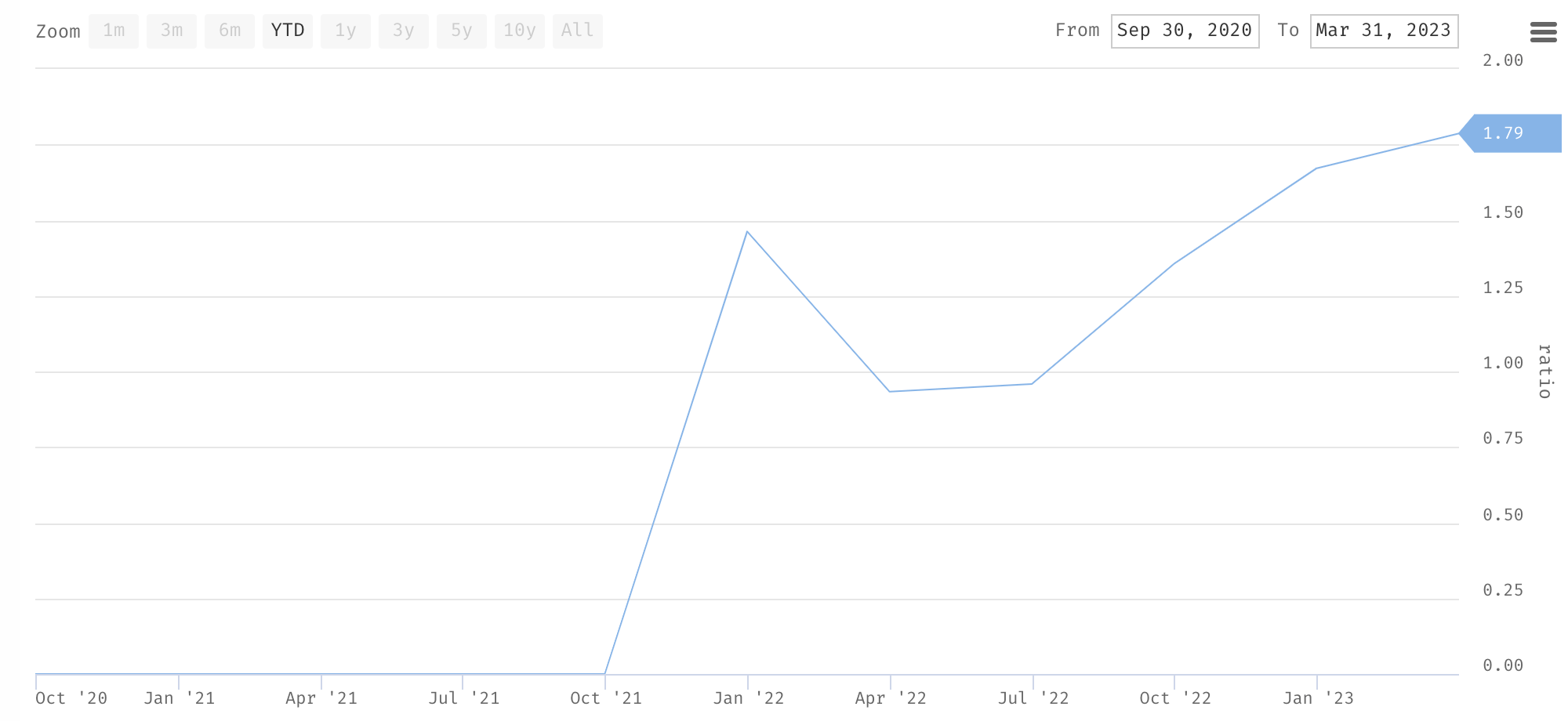

Furthermore, the elevated level of debt-to-equity (D/E) ratio since recent times will also increase Dave's exposure to macro risk, further creating potential pressure on the FCF outlook through increased risk of rising interest expenses.

D/E ratio was 0.93x the same time last year, but it increased by over 92% to 1.79x in Q1, as Dave needed to raise more capital from debt issuance due to its negative operating cash flow last year. Over the same period, interest expense almost doubled on a YoY basis to ~$2.9 million in Q1 from ~$1.5 million. At that level, it made up a considerable 30% share of the FCF loss in Q1.

Since we are still in the high-interest rate environment today, the chance of interest expense increasing further remains high. As per its 10-Q, Dave is exposed to floating interest rates from its debt issuance . Despite the rate-hike pause in recent times , the market continues to expect future rate hikes.

Catalyst

Given the suggestion of increased marketing activities to drive user growth, I would probably be most interested in monitoring how they unfold in Q2 and beyond:

As Jason touched on, we anticipate ramping marketing spend back up in the coming quarters to capitalize on demand for ExtraCash and the higher returns on investment we can achieve at greater scale in those periods. We expect that these investments, along with the demand for ExtraCash rebounding after tax season should accelerate originations of ExtraCash-related revenue throughout the rest of the year.

Source: Q1 2023 earnings call

Having cut marketing spending quite significantly and still seeing 27% growth in new members in Q1 , I may anticipate a best-case scenario where Dave could continue driving revenue growth while maintaining good unit economics/UE.

I think that there are three key factors that differentiate the upcoming marketing initiative from the past ones - first, Dave will start from a lower expense base. Second, it will also start with a higher level of existing engagement and transactions and the lowest delinquency rate in the last four years, and third, Dave will also expectedly have had a better grasp on the most effective marketing channels and tactics to optimize given the learnings from the past recent quarters.

{kind=link}

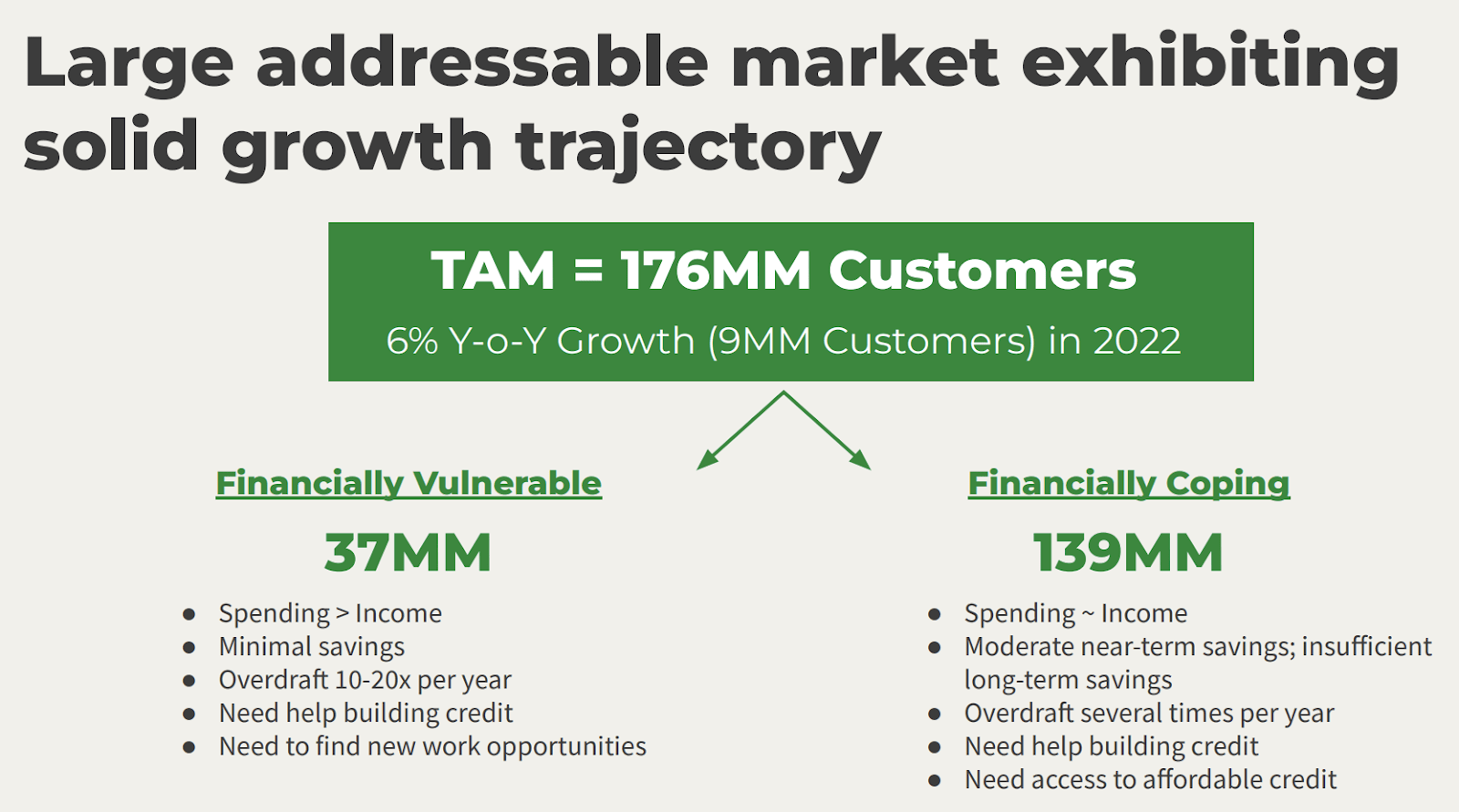

In addition, I continue to believe that there is indeed a large TAM associated with the financially underserved population. Outside the US, I would also expect the TAM to be a lot bigger, and if Dave can successfully scale this model profitably in the US and have a good handle on the key drivers for unit economics, the model may be replicable to other large growing markets like LATAM or India, presenting an attractive cross-border expansion opportunity.

Valuation/Pricing

My target price for Dave is driven by the following assumptions for the bull vs bear scenarios of the FY 2024 target price model:

-

Bull scenario (50% probability) assumptions - Dave to finish FY 2023 with a revenue of $240 million, a ~17% projected YoY growth around the midpoint of its guidance . Considering the current macro weakness, market sentiment around the financial services stocks, as well as the unprofitable outlook, I expect Dave to maintain its rather currently depressed P/S of ~0.3x at the end of FY 2024.

-

Bear scenario (50% probability) assumptions - Dave to miss its FY 2023 estimate with a revenue of $220 million, a 7.4% projected YoY growth, as opposed to the ~11% growth at the lowest end of the guidance. In this particular situation, I expect Dave's P/S to contract to 0.2x, lower than that of today.

Author's own analysis

Consolidating all the information above into my model, I arrived at an FY 2023 weighted target price of $4.92 per share. With Dave trading around $5.4-$6 per share recently, I conclude that the stock remains fully valued to slightly overvalued.

My target price also seems to be quite sensitive to the expected revenue growth for FY 2023. I think that given Dave's unprofitable outlook, investors would require at least a moderate double-digit return to justify making a buy.

My findings suggest that Dave needs to meet its midpoint revenue estimate to at least provide a ~7% upside. However, this would probably be an unattractive return for many growth investors. The biggest issue here seems to be the relatively depressed P/S level. But with growth expected to decelerate from +30% in FY 2022 to ~17% under my best-case scenario in FY 2023, as well as negative profitability and cash flows, P/S expansion will probably be a bit challenging.

Conclusion

I expect Dave to continue seeing near-term losses, primarily due to management's plans to increase marketing spend. The company also expects a deceleration in revenue growth for FY 2023.

I assign a neutral rating for the stock with a weighted target price of $4.92 per share, suggesting that Dave is fully valued to slightly overvalued at its current price of $5.4-$6.

Meeting the midpoint revenue estimate would provide approximately a 7% return for the stock, but it seems that the risk/return profile may still not be too attractive at present, especially with the unprofitable outlook. I give the stock a neutral rating.

For further details see:

Dave: Losses May Extend And Remain Sticky