DVCMY - Davide Campari-Milano: The Americas Drive Q1 2023 Growth

2023-05-09 23:41:24 ET

Summary

- Grand Marnier disappoints but Aperol and Campari grow in double digits.

- Italy and the United States remain the two most important countries for this company.

- Inflation is not reducing margins; on the contrary.

Davide Campari-Milano ( DVDCF ) is an Italian company that markets and distributes alcoholic and non-alcoholic beverages worldwide. The most famous brands include Aperol, Campari, SKYY, Wild Turkey, Grand Marnier, Appleton Estate, and Wray & Nephew Overproof.

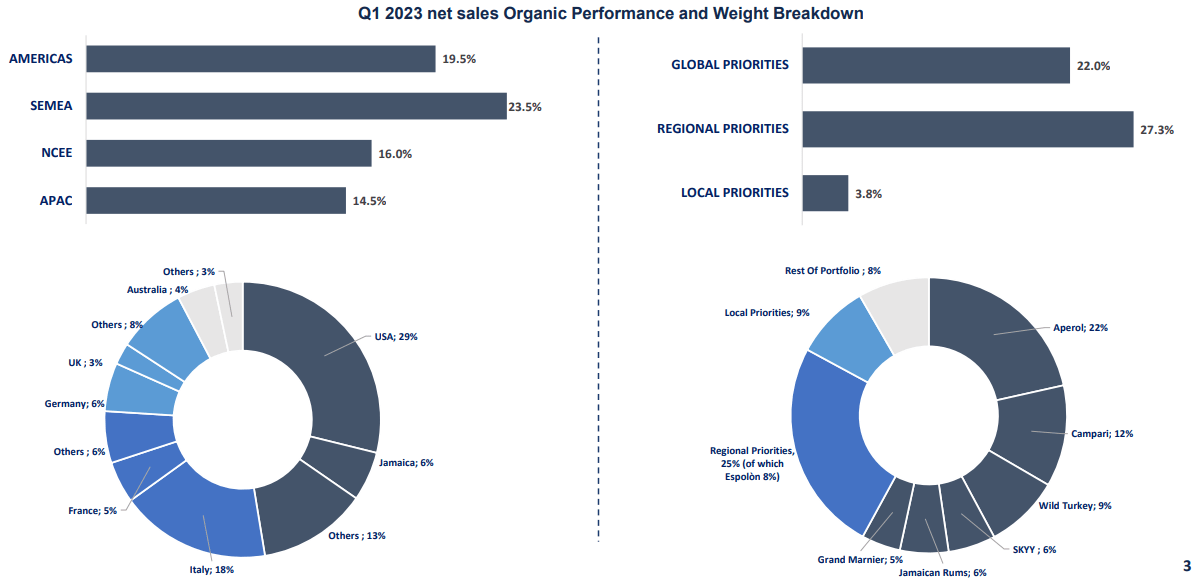

On May 2, the quarterly report for Q1 2023 was released, and the results were quite positive, as net sales showed an organic growth of 19.60% compared to the prior-year quarter. Driving this growth were mainly the main geographic business areas for Campari: Italy and the United States.

Disappointing was the Grand Marnier brand, which, as we shall see, saw an organic decrease of 30.70%.

Comment on Q1 2023

{kind=link}

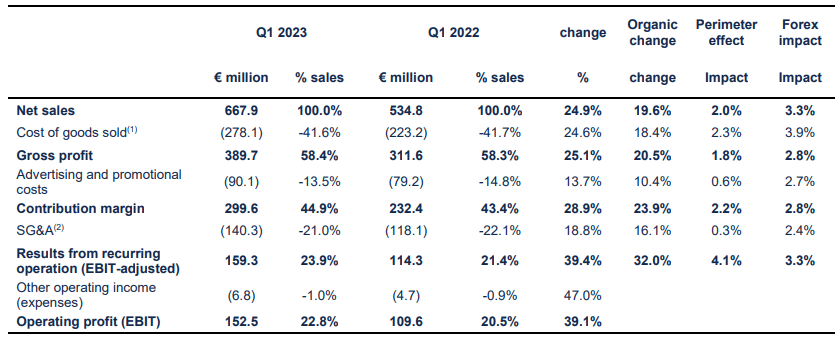

Net sales increased by 24.90% over Q1 2022. This result was achieved due to a triple positive impact:

- Organic growth +19.60%

- Perimeter effect +2%

- Forex Impact +3.30%

These three elements managed not to reduce margins despite input costs still being in the grip of inflation, especially for glass.

Gross margin remained about the same, in fact gross profit grew at about the same rate as net sales, 25.10%. What is new is the operating margin, which rose from 20.50% to 22.80%, a result that does not go unnoticed in the current macroeconomic environment. What's more, this result was achieved in spite of advertising expenses that accounted for 13.50% of net revenues, a rather high figure but necessary to sustain the pricing effect.

{kind=link}

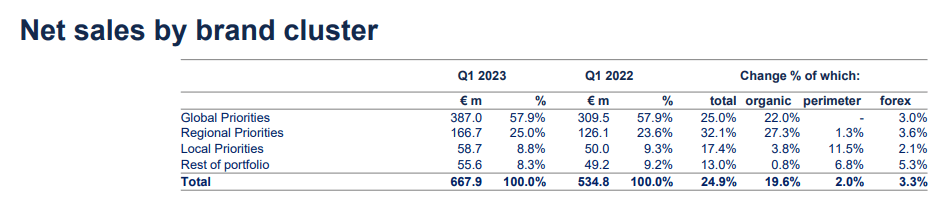

Going to break down Campari's portfolio, we can see that its composition has remained almost unchanged compared to Q1 2022, aided by the fact that Global Priorities (the largest segment) has kept its influence unchanged at 57.90% of total net sales. However, although its weight has remained unchanged, the main novelties belong to this segment.

{kind=link}

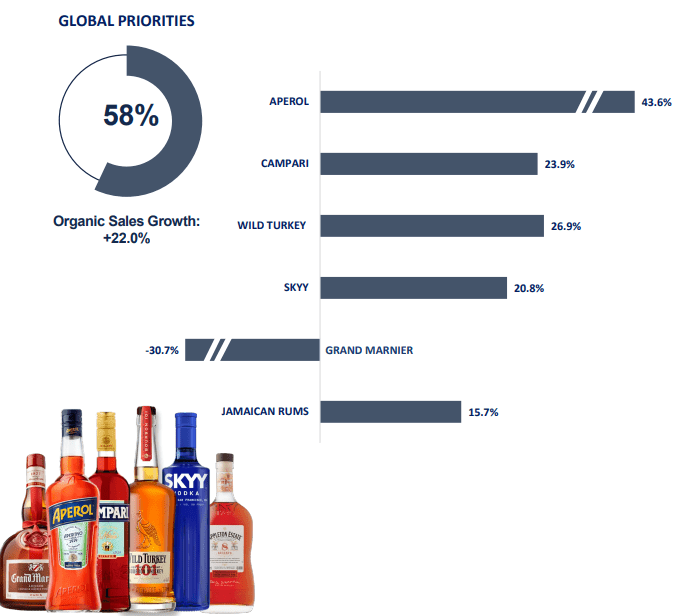

The Aperol and Campari brands are by far the most important, in fact together they generate 34% of total net sales. Their performance has been excellent, as the former has registered an organic growth of 43.60% while the latter 23.90%.

Behind the excellent performance of Campari and Aperol are a number of reasons, here are the main ones:

- Resilient consumer environment, particularly in the on-premise sector.

- Favorable shipment phasing.

- Easter calendar.

- Strong demand in the United States.

- Rising prices, especially in Europe.

Either way, this segment has not only had positive performance; in fact, Grand Marnier posted an organic decrease of 30.70%, by far the most disappointing result. According to the words of CEO Bob Kunze-Concewitz this is mainly a destocking problem.

With regard to inventory levels, I need to explain a little bit what happened to Grand Marnier. Grand Marnier is a large brand for us in the U.S. So the way it works is with direct shipments from our plants via container ships to our distributor partners. Last year, as the ports were being all backed up they were placing more and more orders where clearly, for us, as soon as something leaves the factory, it's a shipment credit, whereas they haven't received it in their warehouses, so they didn't have the inventory levels. So this year, we decided to rebalance all of that, and I think we'll be pretty much done at this stage and the brands will continue on a full year basis, hopefully reflect the depletion growth of mid-single digit.

Having analyzed the performance of key brands, let us now look at the geographical origin of net sales.

{kind=link}

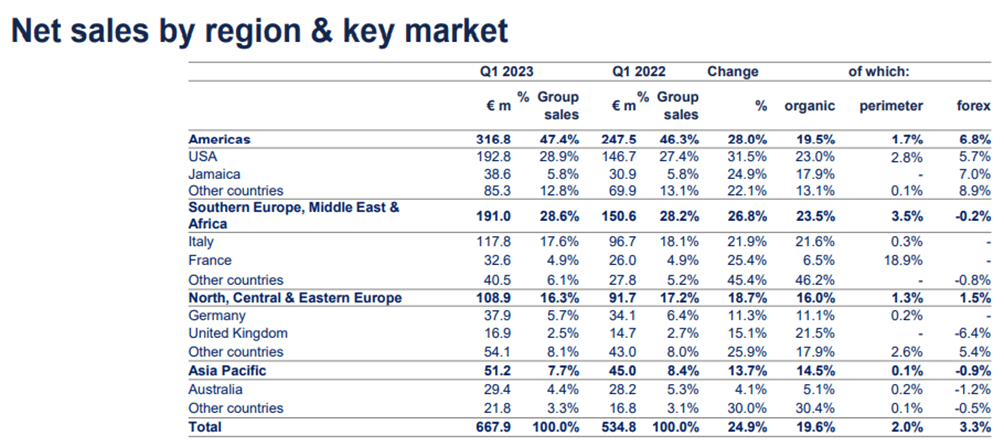

As anticipated, the Americas is the main market for this company as it has a weight of 47.40% of total net sales. The US segment is not only the most important of all, but it is also the one that grew the most, 28.90% over Q1 2022. Weighing heavily on this high growth rate was the Aperol brand, which experienced a surge in sales in Italy, Germany, France, Spain, and the UK. In the United States, growth was even in triple digits.

Europe also performed quite well, driven especially by net sales growth in Italy of 17.60%. Italy is the second largest segment behind the United States. The Americas + Italy generate 65% of the entire company's net sales.

{kind=link}

So, Campari's growth is due to increased demand in its key geographic segments. But how was triple-digit growth possible in such an already important market as the United States? Why did Campari achieve this performance while competitors did not? These questions were answered by the CEO during the conference call:

Compared to some of our peers, we're actually targeting more young urban professionals who aren't really being impacted currently by the economic situation and are maintaining a very active lifestyle. So that's a difference versus some of our peers, which, although they're selling more premium, let's say, aged spirit categories. They've been catering more to blue-collar consumers, which have been impacted by the return to normality and the challenges currently from a macro standpoint, and employment standpoint.

In short, the customer target is more focused toward people who are young, have an active life, and possibly have some financial stability. Indeed, Aperol's commercials often reflect this stereotype, and as we saw earlier a good portion of the revenue is aimed in advertising. For this target audience, it is hard to imagine that an economic slowdown would stop them from having a spritz at the bar with friends. What's more, the lower Covid-19 restrictions compared to last year have helped this growth.

Finally, I would like to talk about the composition of organic growth. We know that pricing has had a major effect on organic growth, but what can be said for sales volume?

On this the CEO was reticent and simply stated that volumes are up across the portfolio, with the exception of Grand Marnier of course. So, it would seem that the rising prices have not generated losses in sales volumes; on the contrary, they have increased.

Overall, I think this quarterly can be called positive, as both the main geographic segments and the main brands are growing in double digits compared to last year. Of course, there are still problems with inflation, but the company has managed to raise prices enough both not to reduce margins and not to reduce sales volumes. Moreover, in the medium term, management is confident of continuing to achieve strong organic topline improvement, which will lead to the expansion of organic margins. Thus, a positive FY23 is expected for Campari. Personally, I like this company, but not at the current price, which is why my rating can't be a buy.

For further details see:

Davide Campari-Milano: The Americas Drive Q1 2023 Growth