DVCMY - Davide Campari: Q2 Results In Line Again A Pass

2023-08-03 12:31:54 ET

Summary

- Campari's net sales increased by 16% to €1.457bn in H1 2023, with organic growth of 14.2%, but the company's stock price fell, having left unchanged its 2023 guidance.

- The company's net profit increased, but also the financial debt and the interest payment.

- Campari's valuation is still pricey versus competitors, and the company might suffer from a negative FX evolution. Our neutral rating is confirmed.

Here at the Lab, we recently deep-dive into the branded spirits industry with an analysis of Campari called We Pass For Now , and a supportive buy rating on Diageo titled Promising Scotch Development, with Near-Term Challenges . So far, so good. Indeed, Campari ( OTCPK: DVDCF ) is broadly flat at the stock price level, while Diageo is up by 3.4%. We reported ten downside risks mainly related to interest rate evolution, lower guidance due to FX negative drag, slower consumer demand, and a pricey valuation vs Diageo and Pernod Ricard.

DC: Mare Past Analysis Diageo: Mare Past Analysis

{kind=link}

{kind=link}

Q2 results

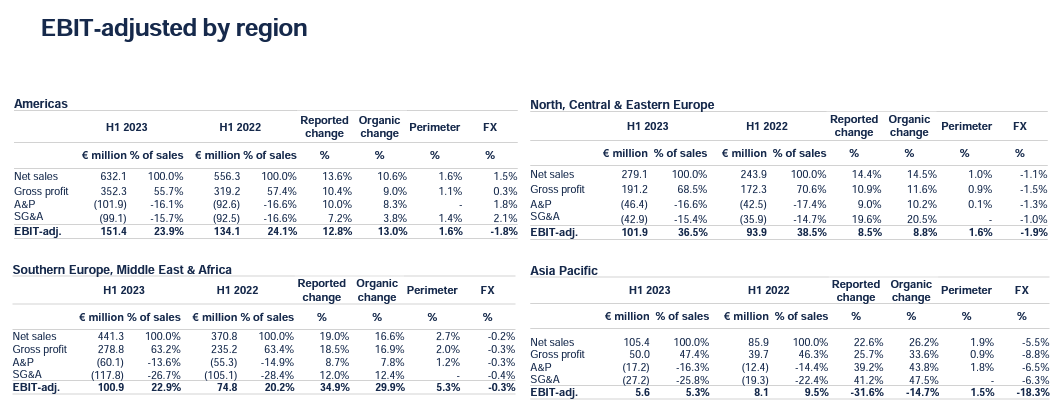

Checking the company's H1 financial figures, Campari delivered sales up 16% to €1.45 billion, while Wall Street analysts forecasted a turnover of €1.47 billion. The company's leading brands recorded a positive performance in Q2 with a plus 10.1% growth with a particular emphasis on tequila, aperitifs, and premium bourbon. Higher prices also supported this. It is essential to report the CEO's words. He explained that Q2 results " reflected the expected reversal of the temporary phasing effects from the first quarter, as well as very poor weather across core Southern & Central Europe and temporary delistings from selected European retailers due to commercial negotiations in connection with price increases." Geographically speaking, sales in the Americas, representing 43% of the total company's turnover, grew by 10.6%, with a US positive trajectory of 11.7%. In Southern Europe, the growth was 16.6%, while Italy reached a plus +13.4%, with a supportive Q2 at 8.1%. According to the P&L analysis, Campari's adjusted net profit reached €233.9 million and was up by +6.2% versus last year.

Downside Risks still in place

Cross-checking Wall Street analyst expectations, the company missed EPS estimates by 6%. Therefore, we might expect a few price re-ratings on the downside. We should also report a slight miss on the company's adj. EBIT margin.

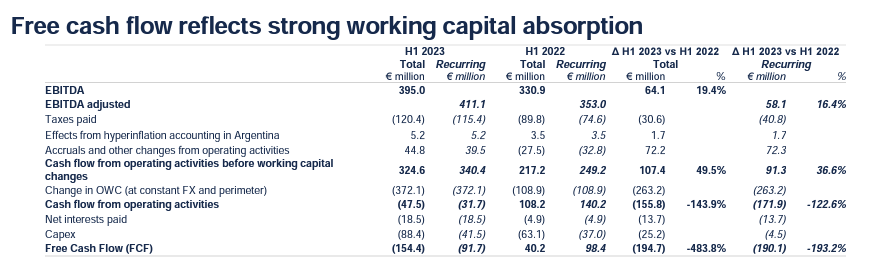

Looking at our negative downside: we report that Campari's net interest amounted to €18.5 million vs. payment of €13.7 million in H1 2022. For 2023, we are now guiding a net finance cost of €55 million versus our previous estimate of €45 million.

Campari higher interest payment

{kind=link}

Lastly, net financial debt worsened to €1.82 billion, with €268 million more in December. This was due to working capital requirements on investment in inventories. In numbers, the company's net financial debt/adjusted EBITDA multiple reached 2.5x vs 2.4x

{kind=link}

As expected, the adjusted EBIT reached double-digit growth of +15.7%, equal to €359.7 million. However, the gross margin was diluted by -50 basis points due to continued inflation on production costs, advertising, and promotion expenses. In addition, the company postponed a few launches in Q3 (summer season) due to adverse weather conditions. In Q2, it is essential to report glass cost and an unfavorable exchange rate effect evolution of -1.9%, equal to 6 million. This was due to dollar depreciation.

Still related to EBIT margin, H1 increased by 20 basis points, and the flat guidance for 2023 implies a minus 30 basis point in H2. In addition, there were no financial targets for Fiscal Year 2024 margin expansion. Despite being neutral on Campari, we model an EBIT margin of 22.7% in 2023 vs. a core operating profit of 22.1% recorded in 2019. We believe that the benefit from slowing COGS inflation is limited in 2023, but we might see a positive trajectory for next year. These are mainly related to lower supply chain and glass costs.

{kind=link}

Conclusion and Valuation

Here at the Lab, we were broadly in line with the company's internal estimates for sales and EBIT. However, net income is approximately 3% lower due to higher finance costs. Campari's management reaffirmed the Fiscal Year 2023 guidance with flat margins. Although we are not surprised by these results, the expectations of those with a supportive buy rating envisaged a possible guidance upward revision. While Campari's track record of bolt-on acquisitions should give some comfort that any transaction would be well thought out, a large-scale acquisition/merger could pose execution/integration risks in the near term.

In our model, we estimate 2023 organic sales to be up by 12.5%, with an increase in the EBIT by 15.6% (a margin expansion of 50 basis points). After analyzing the H1 results, we are still optimistic about the company's future performance, and Campari continues offering a double-digit EBIT and EPS growth CAGR. However, the valuation is increasingly looking full.

Aside from multiple valuations, in our DCF model, with a WACC of 8.5% and a long-term growth rate of 3%, we derive a target price of €12.5 per share. For this reason, we maintain a neutral rating and our short-term preference for the rival Diageo in the spirits industry and Heineken in the beer sector. In addition, after a solid yearly performance of +30% year to date, the stock trades at 30x 12-month earnings P/E. This represents a 60% premium compared to the Stoxx F&B (index of European companies in the food and beverage sector) to a historical 5-year average of 57% and 45% compared to the pre-pandemic level. We believe this premium is not justified. Upside risks on our equal weight valuation are 1) better-than-expected price development, 2) Chinese growth rate, 3) supportive demand for the Campari product portfolio, and 4) input cost pressures easing.

For further details see:

Davide Campari: Q2 Results In Line, Again A Pass