DVDCF - Davide Campari: We Pass For Now

2023-06-23 07:20:42 ET

Summary

- Campari Group saw impressive organic revenue growth in Q1, with a strong performance in the US market.

- The company reiterates guidance for a flat organic EBIT margin in the current year, but there may be downside risks to consider.

- Campari's focus on M&A is expected to intensify; however, we should consider higher interest rates.

- Despite we increased the EPS target, Campari's valuation looks full compared to its closest peers.

Today, we decided to move on with Davide Campari-Milano N.V. analysis (DVDCF). The company is incorporated in the Netherlands and is active in the branded spirits industry. Campari owns a diversified product portfolio of over 50 brands and is in more than 190 countries thanks to 21 industrial facilities and a solid distribution network. Related to the company's growth strategy, Campari decided to focus on the APAC area by strengthening the distribution structure. Indeed, the group accelerated the acquisition of majority stakes in local commercial JV in Japan and New Zealand, exercising early call options and increasing its direct logistic network.

Japan and New Zealand latest acquisition (Campari Q1 Results Presentation)

{kind=link}

Q1 Results

Very briefly, the Italian beverage player closed the first quarter of 2023 with net sales of €667.9 million, up by +24.9% on a yearly basis (and beating consensus estimates of €618.6 million). The company delivered a gross margin of €389.7 million, up by +25.1%, and recorded a solid start to the year. Looking at the details, we see that top-line sales positively benefit from price increases which were carried out last year.

Downside Risks with Changes in Estimates

However, we'd like to report some downside risks and important notes to take into account in your Campari investments.

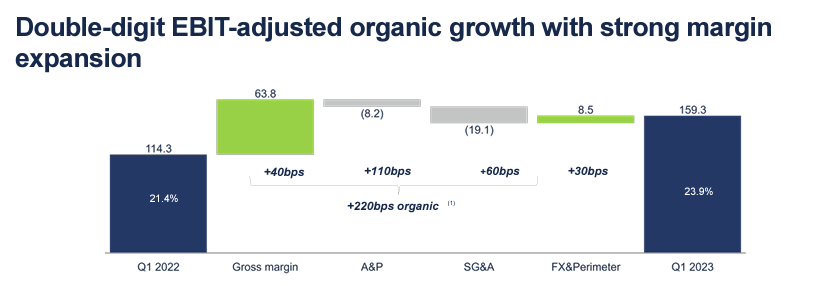

- Despite impressive sales momentum, the CEO is not too optimistic. He confirmed a stable adjusted EBIT margin as a percentage of Campari's turnover (Fig 1 and 3). If we look at the pre-COVID-19 level, in 2018 FY results, the company reported revenue of €1.7 billion with an operating profit margin of 22%, while in 2022, revenue reached almost €2.7 billion with an operating profit margin of 18.98%. Campari's operating leverage is not entirely working;

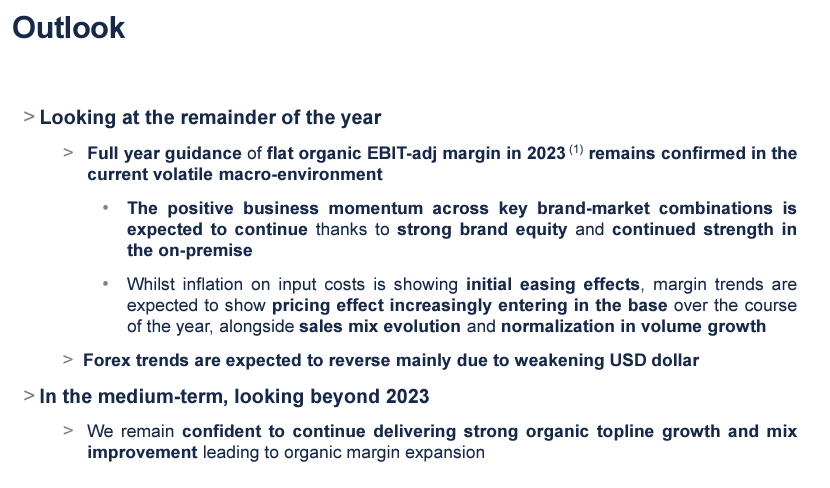

- We can say that guidance is also a bit misleading, in our opinion (Fig 2); indeed, the CEO also expects higher market share penetration in all Campari key markets while industry demand is normalizing;

- As a reminder, Campari increased its price twice last year, and for 2023, it has already accomplished a price increase in aperitifs. For this year, we are estimating no additional cost pass-through to Campari clientele;

- Q1 sales were favored by Easter timing in Italy, and this might provide a negative trend in Q2 results,

- We will monitor SG&A expenses; however, we are forecasting an easing in logistics costs starting from H2. This should positively impact the company margin. In detail, supply chain costs are coming down on transatlantic routes; however, we are still seeing a high-single-digit higher price than the pre-COVID-19 level;

- The top manager also underlined that " although inflation on production costs is going down, the trend in margins will progressively discount the effect of the price increases ." In addition, we believe that volume growth will stabilize. As suggested in our recent Heineken publication , in an inflation period, " consumers are looking for cheaper alternatives ." And we might forecast that clients might switch from spirits to beer/wine products;

- The company is forecasting a step up in CAPEX over the next three years. This needs to be better priced by Wall Street analysts. In our forecast, we are estimating CAPEX on sales at 10% per year. This will need to support Whisky brands, Tequila, and Aperitifs development;

- The currency development will be a negative headwind to the company's earnings, given the recent dollar weaknesses;

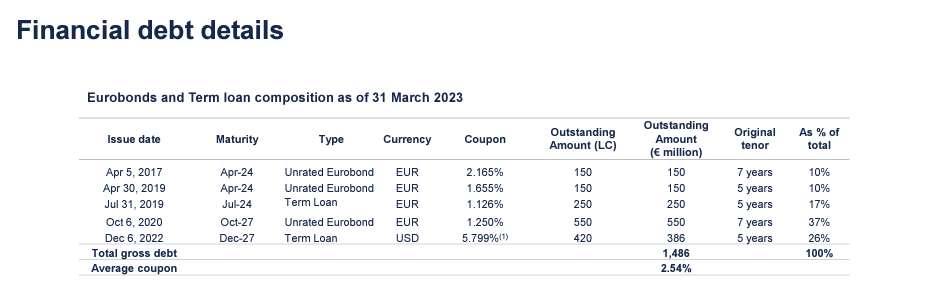

- Also, Campari has an extremely low cost of debt, with an average interest of 2.54% (Fig 3). Recently, the company announced a €300 million bond with a coupon of 4.71%. Therefore, we expect a slight increase in finance costs. Looking at the detail, the interest expenses already increased on a yearly comparison by €7.9 million. This was due to higher debt (Q1 2023 €1.58 billion vs. Q1 2022 at €832.7 million);

- The company has made no secret that it is looking for external acquisitions, including transformational deals. However, the company's net debt to EBITDA is at 2.3x, and interest rates are not particularly favorable at the moment (Fig 4). Despite a positive M&A track record, and an ability to pay lower multiples, we believe this time is over. Spirits valuations are pricey, and the latest deals demonstrate these latest deals. In addition, we should say that size matters in M&A; Diageo and Pernod Ricard have a market cap of €88 and €50 billion, respectively, while Campari is at €13.8 billion. Again, this cannot go unnoticed.

{kind=link}

Fig 1

{kind=link}

Fig 2

Campari's current int. rate (Campari Q1 Results Presentation)

{kind=link}

Fig 3

{kind=link}

Fig 4

Valuation and Risks

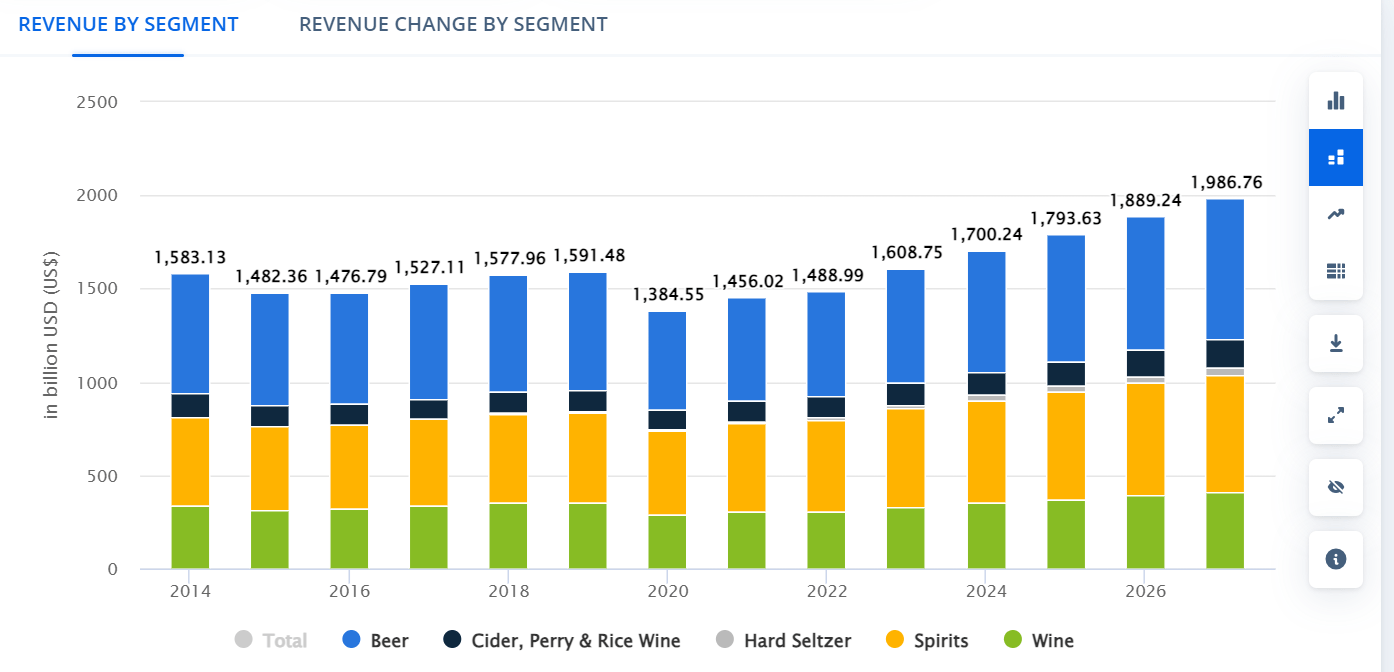

Here at the Lab, much growth is priced in Campari valuation. However, as already mentioned in point 7, the beer segment will be back to growth over the next visible period, outpacing spirits development. This is evident by Statista Alcoholic Drinks - Worldwide's latest projection (Fig below). Compared to its peers, such as Diageo , Campari has no beer brands in its current portfolio. Despite that, given the solid Q1 and the spirits projection growth trend, we decided to raise our 2023 top-line sales and EBIT by 11% and 13%, respectively. Our EPS is up by 5% at €0.41 per share, including the higher cost of interest expenses and a decremental FX development. So, we decided to initiate coverage of Campari with a target price of €12.50 based on a 30x 2024 EPS estimate. The company is currently trading at a 45% premium compared to large-cap spirit companies such as Diageo and Pernod. For this reason, we remain neutral due to a limited upside to our target price (the company is trading at €12.28 per share). Aside from the above risks, additional downsides are a weaker spirit demand (especially in the EU) and a further escalation in raw material input costs.

{kind=link}

For further details see:

Davide Campari: We Pass For Now