DTEA - DAVIDsTEA In Trouble Again

Summary

- The company went through the Canadian Companies’ Creditors Arrangement Act at roughly the same time as Reitmans and pivoted to e-commerce.

- The strategy seemed to be working well at the beginning, but sales have been declining as tea customers return to physical locations following the end of COVID-19 lockdowns.

- In my view, DAVIDsTEA is likely to run out of cash in the near future and the most likely scenarios after that include significant stock dilution or another restructuring.

Introduction

On February 16, I wrote an article on SA about Canadian clothing retailer Reitmans ( RET.A.CA ) ( OTCPK:RTMAF ) ( RET.CA ) ( OTCPK:RTMNF ) in which I said that the company has successfully restructured its business and that the financials seem in excellent health. During the COVID-19 lockdowns, Reitmans went through the Canadian Companies’ Creditors Arrangement Act [CCAA], which is the Canadian equivalent of Chapter 11, and its share price has increased by over 60x from the 2020 lows thanks to the compelling improvement in the fundamentals of the business. The impressive returns sparked my curiosity in searching for other Canadian companies that had to go through the CCAA during the COVID-19 lockdowns and this led me to DAVIDsTEA ( DTEA ). There are many similarities between the restructuring of the businesses of the two companies, but I think that DAVIDsTEA has made a mistake by focusing on digital sales. It just doesn’t seem to be a good idea for the tea retail sector, and I think that the company is headed for significant stock dilution or will have to think about the CCAA again in the near future. Let's review.

Overview of the business and financials

DAVIDsTEA started operations in 2008 with a single store in Toronto with the idea of offering specialty branded tea products in friendly stores with great customer service. The company rapidly grew into the largest tea retail chain in North America with a total of 231 stores and over 2,500 employees at the start of 2020. However, revenue growth rates had stalled by then, similar to Reitmans. DAVIDsTEA generated sales of C$196.4 million ($148 million) for the fiscal year ended February 1, 2020, compared to C$212.8 million ($164 million) a year earlier. In addition, the net loss for FY20 came in at C$35.4 million ($26.7 million), compared with C$87.4 million ($65.9 million) for Reitmans for the same period as both companies were put under pressure by rising rent levels.

{kind=link}

With retail stores closing across Canada amid COVID-19 lockdowns, DAVIDsTEA experienced significant financial losses and liquidity issues and had to turn to the CCAA in the middle of 2020, just like Reitmans during the same time. Reitmans closed a quarter of its stores and is currently pivoting its business to e-commerce, with retail sales already surpassing 25% of its total sales. DAVIDsTEA had a similar idea but it decided to make the shift immediately, closing all but 18 stores which are concentrated in the Ontario and Quebec markets. The tea retailer adopted a digital first strategy and focused its efforts on online customer experience by bringing its tea guides online to provide human and personalized interaction. In addition, DAVIDsTEA upgraded the capabilities of its DAVI virtual assistant which helps clients shop as well as discover new collections.

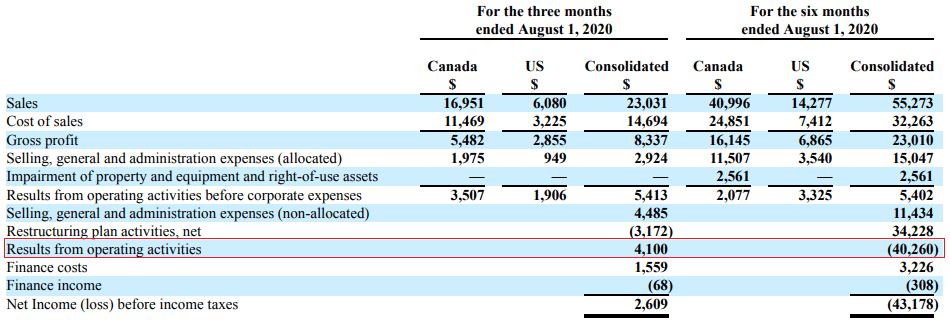

At first, the pivot to e-commerce seemed to be a success as e-commerce and wholesale sales soared by 189.9% year on year in Q2 FY21 and the company booked an income from operation of C$4.1 million ($3.1 million).

{kind=link}

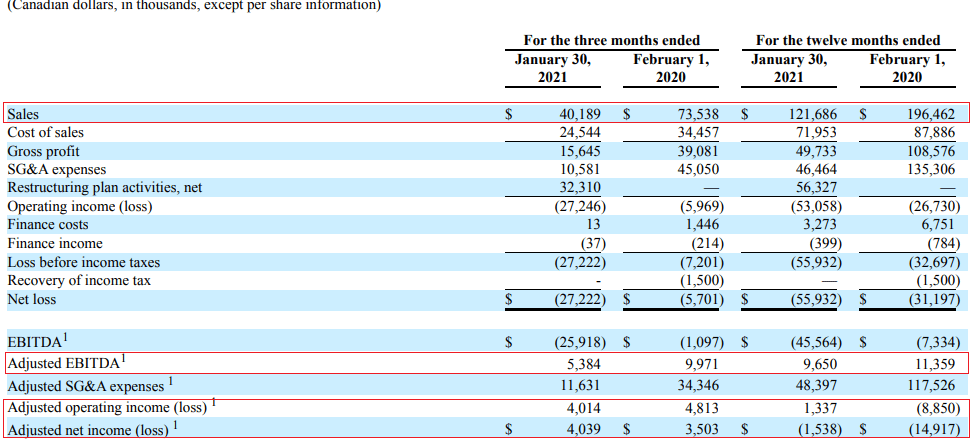

With the 18 physical stores reopening in late August 2020, Q4 FY21 sales reached C$40.2 million ($30 million). The e-commerce and wholesale segment accounted for C$35 million ($26.1 million) of that amount, up 96% year on year.

{kind=link}

Unfortunately, this was as good as it got as Canadian tea consumers have been returning to retail stores ever since COVID-19 lockdowns ended and this has led to a significant deterioration of the financial results of DAVIDsTEA. This is where the path of the company diverges from the one of Reitmans as the latter is still profitable and with growing sales. You see, buying premium tea can be viewed as a social thing as customers want to talk to the staff, smell the varieties, and learn new things about the leaves and their origins. In my view, DAVIDsTEA used to be the tea version of Starbucks (SBUX) and the business model just doesn’t work well when you move everything online. It’s a vastly different product compared to clothing, where several brands have found success after pivoting to e-commerce, e.g. Lands' End (LE) which I’ve covered here .

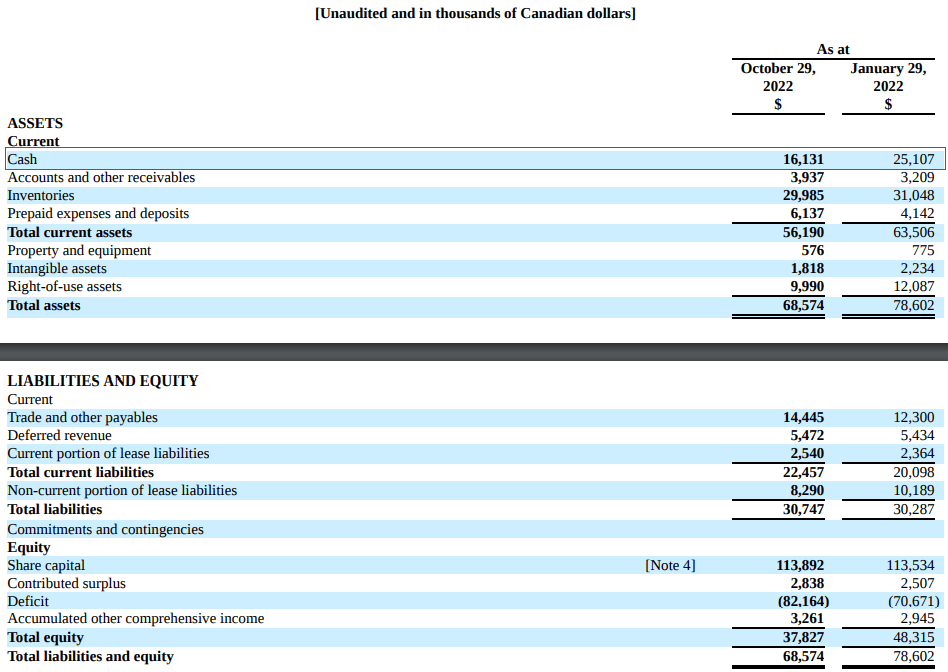

On February 2, DAVIDsTEA announced that sales for Q4 FY23 are estimated between C$29 million ($21.5 million) and C$31 million ($23 million), and the midpoint of the range represents a year-over-year decline of 25%. The company added it will implement cost-cutting measures which include the temporary layoff of 15% of its head office staff as well as the elimination of IT transformation investments of C$4 million ($3 million) undertaken in FY22. With this, SG&A costs on a pro-forma basis are forecast to decrease by between C$8 million ($5.9 million) and C$10 million ($7.4 million) in FY23 but I expect the lack of investment to lead to a further decrease in sales which will pretty much wipe out the effect of the cost-cutting measures. In my view, DAVIDsTEA is in survival mode once again and its future is grim. Looking at the balance sheet, the situation looks bad as cash was down to C$16.1 million ($12 million) as of October 29, 2022. Unlike Reitmans, DAVIDsTEA does not have significant real estate properties that it can sell to strengthen its balance sheet and cash flows used in operating activities stood at C$6.6 million ($4.9 million) for the first nine months of FY23. Unless the fundamentals of the business somehow improve significantly soon, the DAVIDsTEA is likely to run out of cash in the near future and the most likely scenarios after that include significant stock dilution or another restructuring of the business through CCAA. Both of these scenarios would be unpleasant for investors.

{kind=link}

So, how do you play this? Well, short selling seems like a viable idea as data from Fintel shows the short borrow fee rate is 2.95% as of the time of writing. The short interest is just 0.14% of the float and it takes less than a day to cover. However, hedging would be challenging as the only available call options have a strike price of $2.50.

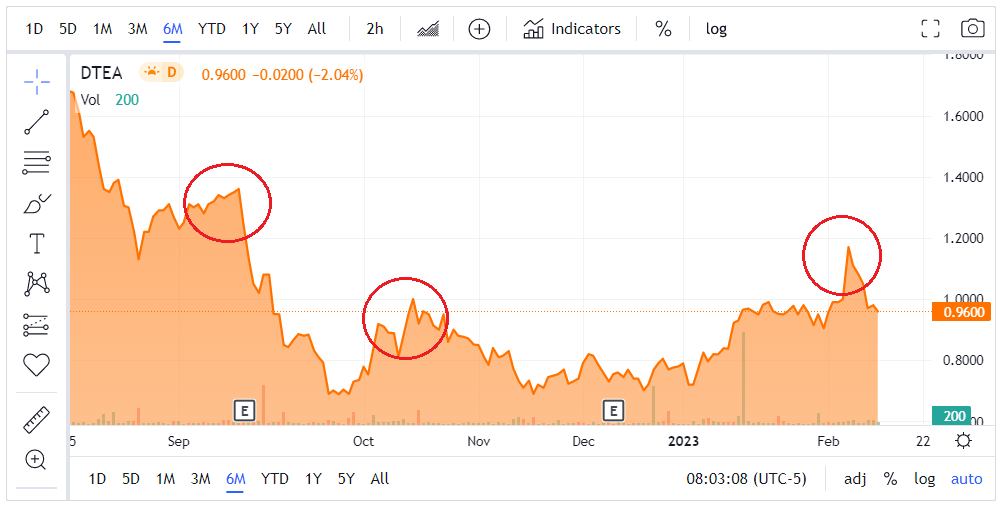

In addition, short selling could be dangerous as the share prices of microcap companies can sometimes increase for spurious and unknown reasons. This has already happened here in the past on a few occasions over the past six months alone.

{kind=link}

Investor takeaway

In my view, DAVIDsTEA’s pivot to e-commerce was just not a good idea and the company is now in trouble again from a financial standpoint. Sales are declining as tea customers return to physical locations and cash is running out fast.

The short borrow fee rate seems low enough to make opening a small short position viable. However, the lowest available strike price for call options is $2.50 and the share price has been volatile over the past few months. In my view, it could be best for risk-averse investors to avoid this stock.

For further details see:

DAVIDsTEA In Trouble Again