DVA - DaVita: Assessing After The Rally

2023-12-29 16:15:21 ET

Summary

- DaVita's stock has rallied over 40% after concerns about the impact of GLP-1s on its business have quickly passed.

- Management ran through their scenarios regarding the potential limited impact of GLP-1s over the long run on the latest earnings call.

- DaVita has been successfully cutting costs and restarted its buyback program, this could be an inflection toward more consistent earnings growth.

- DaVita's FCF multiple has risen from 7x to 9.5x but is still much more attractive than the overall market.

DaVita ( DVA ) has rallied over 40% after cratering on Ozempic related fears . Additional commentary that GLP-1s could erode DaVita's business has been nonexistent since, proving once again Mr. Market can be quite an irrational fellow.

Nonetheless, the future is highly uncertain. Investors must be prepared for a wide variety of challenges and possible existential threats when investing for the long run. DaVita's management team gave the best answer possible on their November 7th earnings call. Any impact from GLP-1s would be well beyond a reasonable time horizon:

This thesis is built on many uncertainties within a progressive disease, but the one area where we can have clarity is in regards to timing. In this population, the progression to end stage renal disease is typically 15 to 20 years or longer. Suffice to say, this scenario is beyond the horizon of our strategic plan. - DaVita Q3 Earnings Call

DaVita's Chief Medical Officer ran through their findings and assumptions related to the impact of GLP-1s. First, GLP-1s have been available since 2005, and across the spectrum of studies on GLP-1s and kidney disease, 40% have shown no effect, 40% showed some improvement, and 20% have been mixed.

Currently, 5-8% of CKD patients are on GLP-1s, DaVita believes that rate could reach 30%, keeping in mind that the discontinuation rate of GLP-1s is around 65%. Right off the bat, 30% of CKD are not eligible for GLP-1s, from there DaVita assumes 40% of those eligible will end up on GLP-1s. They then estimate that disease progression will slow by 25%, based on the 40% of studies that showed efficacy in delaying kidney disease.

DaVita CEO Javier Rodriguez translated what these findings could look like in terms of affecting business results, and it's miniscule. DaVita believes about 700 commercial patients, those who would begin receiving dialysis between the ages of 62.5 to 65, would now delay the progression to dialysis to after they turn 65, when Medicare coverage kicks in. Medicare revenue is unprofitable for DaVita versus commercial insurance.

As anticipated, the market has very quickly reacted to the reality that dialysis is likely here to stay. For shareholders fortunate enough to ride the recent outperformance, it's important to take stock. While riding winners usually proves to be sage advice, it's good to view holdings with fresh eyes after swings in valuation.

Q3 Earnings

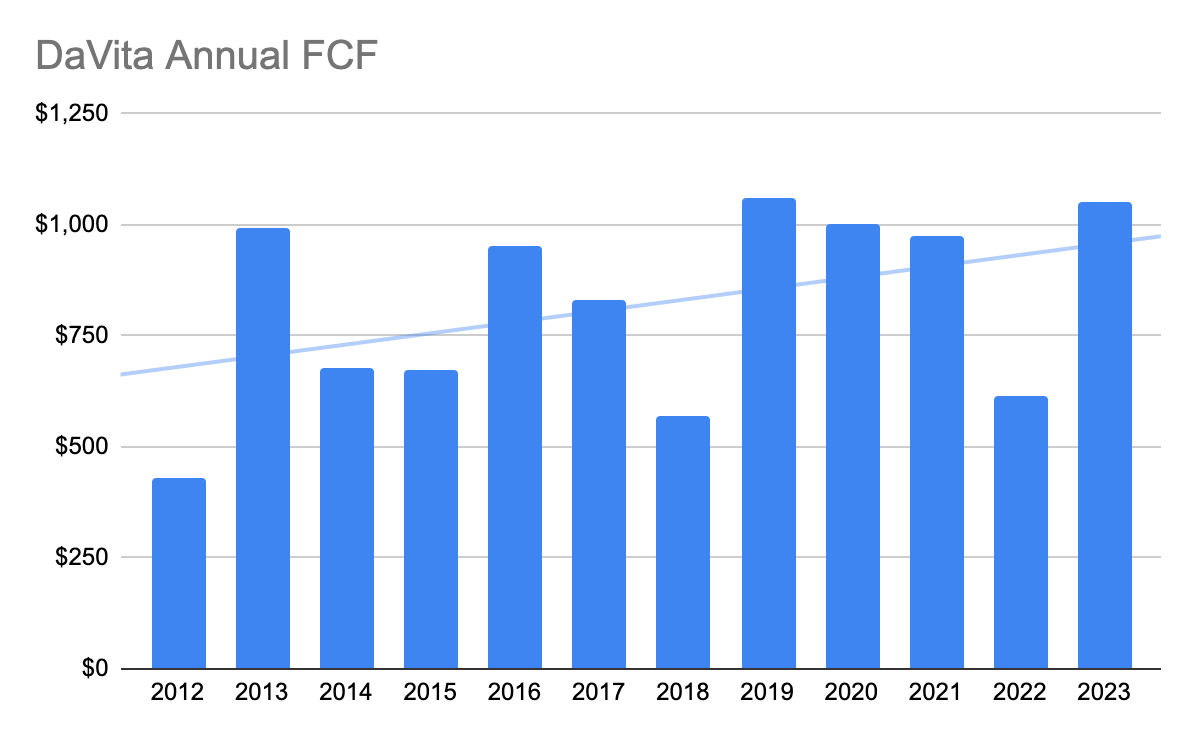

Once again, DaVita is a very simple business that has substantial market share providing a life-sustaining service. DaVita posted strong results in Q3, guiding to full-year FCF of over $1B, following a period of cost pressure.

DaVita's FCF has historically been volatile. With a $10B cost basis, a few points of margin in one direction make a meaningful difference to profitability. While capital intensive, DaVita's revenue is not cyclical, but profitability has been:

{kind=link}

DaVita may be reaching an inflection toward a smoother FCF curve going forward, with cost inflation largely in the rearview. Management has reduced costs by increasing the usage of contract labor, switching to Mircera for anemia management, and consolidating its footprint.

It appears DaVita is on a better path to more sustained earnings growth through cost reduction. Beyond the obvious that higher earnings improve shareholder value, more consistent cash flow should inspire more confidence in investors who have witnessed a choppy share price for the past decade. It is a risk, however, given DaVita's history, choppy FCF can cause optically cheap multiples to look more expensive very quickly.

In addition, management noted it indeed would begin repurchasing shares after reducing the leverage ratio and capturing the opportunity Mr. Market presented during the Ozempic sell-off:

As a result, and after considering our typical set of capital allocation principles, including our view of intrinsic value relative to current market price of our stock, we intend to resume purchasing shares this quarter.

Great management teams know that buybacks are most accretive when performed at prices below intrinsic value. The window of time that DaVita traded down significantly closed quickly, but hopefully management was able to make a dent in the share count while the sun was shining.

Valuation

The rally has increased DaVita's FCF multiple from 7x to 9.5x, while the S&P 500 trades closer to 25x. DaVita increased the midpoint of guidance by $75M. DaVita's only true peer is Fresenius Medical Care ( FSNUY ), which commands a similar market share in dialysis. Fresenius trades at a similar multiple but is much less compelling for two primary reasons: DaVita is listed in the United States, thus domestic investors are not subject to fluctuations in foreign exchange, and Fresenius has not been a large repurchaser of shares.

The primary fear created by GLP-1s was reducing the time that dialysis would remain a relevant treatment for chronic kidney disease. With management's analysis assessing the impact of GLP-1s, it feels even more likely that dialysis will be the primary treatment option for years, if not decades to come.

When a stock is very cheap, and the underlying earnings are consistent and durable, all investors must do is own and wait. Hopefully, DaVita will continue to sensibly deploy buybacks while reducing its cost structure. The reason multiple expansion has meaningfully reduced the FCF yield from about 14% to 10.5%. But, this is still attractive relative to the rest of the market.

For further details see:

DaVita: Assessing After The Rally