BHC - DaVita: Continued Economic Hurdles Market Expectations May Be Correct

2023-10-04 21:46:29 ET

Summary

- DaVita Inc. stock has been heavily sold in '23, trading below its 50-day moving average for the past 8 weeks.

- The company lacks economic value, and its reinvestment runway looks limited, producing sub-standard returns on capital.

- The market expects modest earnings growth for DaVita, and it would appear that the stock is currently trading within its fair value range.

Investment briefing

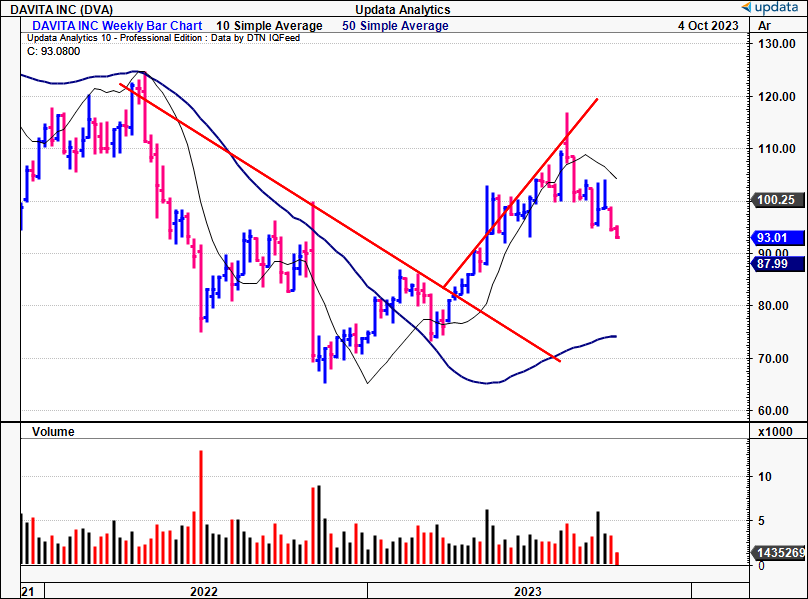

It turned out to be a prudent call to hold off investing in the equity stock of DaVita Inc. ( DVA ) in my last coverage . Since that publication in July, the firm hasn't unlocked additional risk capital for equity investors, as seen in Figure 1. The stock now sold below its 50DMA for the last 8 weeks, having rolled over after a climax top to end its rally from November '22 to August '23.

The last publication talked at length on a number of critical facts to the DVA investment debate. This report will unpack things further, with exquisite focus on the kind of value—or lack thereof—DVA is creating for its owners. The market has spoken on DVA's expectations, and it now trades back in line with its August/September '22 range, which looks to be a key level for the company in terms of price structure.

Critically, the firm lacks economic value in a world where money markets are paying 4–5% starting yields on short-dated Treasuries, not to mention with many high-grade corporates offering 9–10% yields as I write. Hence, the benchmark is high, DVA's reinvestment runway looks clamped and what capital is employed in the business is producing sub-standard returns based on this examination. Net-net, reiterate hold.

Figure 1. DVA topping and rolling over as we entered H2 FY'23. Classic climax top with selling volume with subsequent downside following. Now trades below 50DMA for the last 8 weeks.

{kind=link}

Critical facts pattern supporting reiterated hold thesis

1. Recent developments

- Dichotomy between sell-side and buy-side expectations

August saw the emergence of two differing views on DVA in the investment context. UBS analysts upgraded their stance on the company and upgraded the company a buy, acknowledging this is a contrarian view. UBS is looking to a price target of $142/share after the company's Q2 numbers, citing:

(i). " [B]etter pricing and a lower cost structure",

(ii). Tailwinds that support the upper end of Wall St's earnings estimates,

(iii). Growth in the number of DVA's dialysis treatments across the board,

(iv). It expects DVA to resume buybacks in Q4 this year.

The sentiment wasn't shared equally by the team at Glenview Capital Management, with the investment firm snipping 276,000 shares of its position in DVA. This is despite the firm adding to a number of positions within the healthcare spectrum, with sizeable positions in names like Bausch Health Companies ( BHC ) [1.77mm shares] and Cardinal Health ( CAH ) [257,000 shares].

The opposing views are interesting, to say the least. So far, UBS' thesis has yet to play out, with the stock pushing further to the downside, thus saving Glenview a few points of absolute losses.

- Latest numbers—revenue per treatment higher, flat elsewhere

DVA put up Q2 FY'23 revenues of $3Bn, ~250bps YoY growth, on operating income of $405mm, equating to a margin of 13.5%. Critically, regarding the unit economics:

- It performed 7.23mm total dialysis treatments, tallying 92,708 per day, up 30bps YoY.

- Revenue per treatment was up to $376.73 from $366.14 last year, with patient care costs down $4.77 to $252.5 per treatment.

- For the YTD, it incurred dialysis centre closure costs of $43mm.

As to the H1 breakdown of dialysis revenues, 57% stemmed from Medicare and 32% from its commercial market, with the remainder made up through Medicaid and other government sources, as seen in Figure 2.

BIG Insights

2. Broader economic value

- Leverage and equity multiplier responsible for asset growth + ROE

Tallying all the debt on DVA's balance sheet, you'll be interested to note it has more in debt than it does in market capitalization ($11.48Bn total debt, $8.55Bn market value as I write). It left the quarter at a net leverage of 3.7x EBITDA, above its target range of 3–3.5x.

What's more is DVA's capital structure is heavily weighted to the liabilities side of the balance sheet. More than 86% of its gross asset value is financed through liabilities, around 50% considering long-term debt as a standalone item.

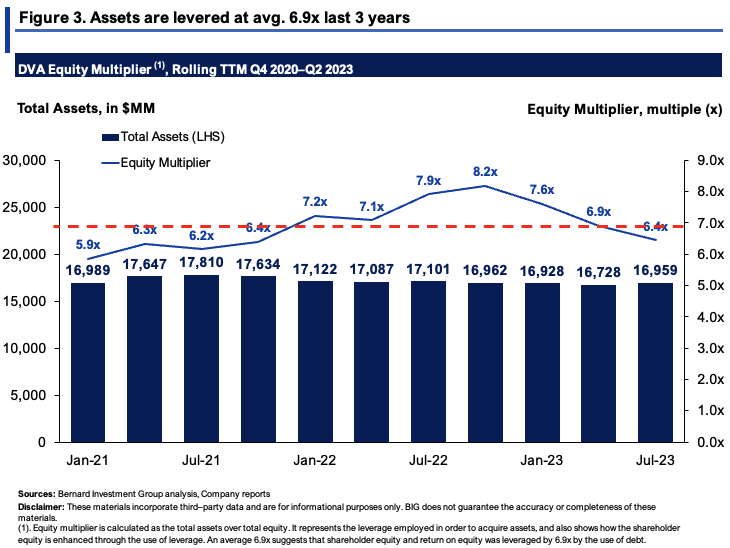

The firm's equity value is therefore highly leveraged. As seen in Figure 3, the multiplier on DVA's equity from the use of leverage has averaged 6.9x over the last 3 years. It was 6.4x in Q2, having reached as high as 8.2x earlier this year. Excluding all its minority interests, the equity multiplier is >16.6x as of Q2.

{kind=link}

This has a blurred impact on the company's profitability. Excluding all minority interests, the company's trailing ROE is 46.4% (467.7/1017.4 = 46.4%). Trailing net margin is 3.98% and asset turnover is 0.7x. As mentioned earlier, excluding all minority interests, the company's equity multiplier is 16.67x. Multiplying these 3 statistics is one way to arrive at a firm's ROE. But, as you can see, leverage has a huge impact on the outcome. For DVA, stripping all leverage out, its trailing ROE drops to just 2.8%.

Source: Company reports, BIG Insights

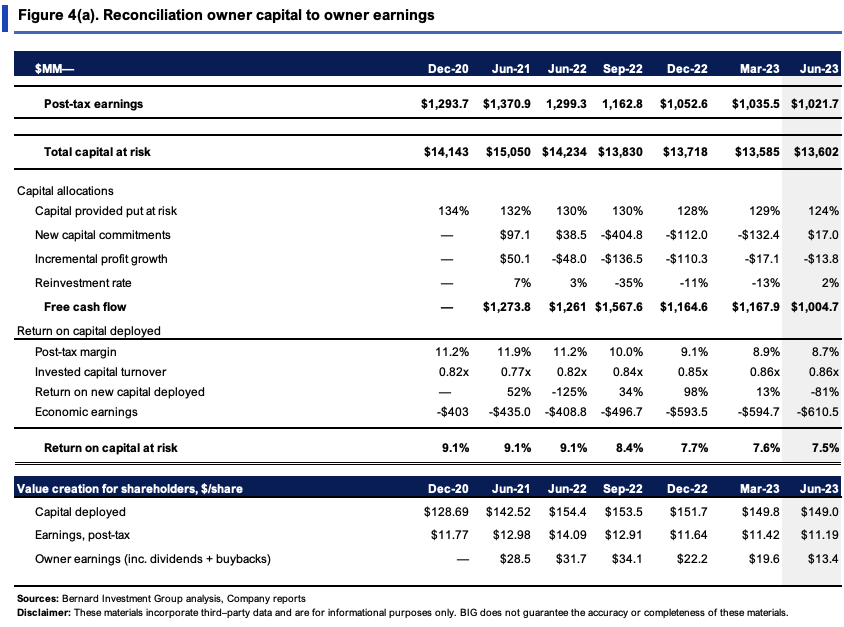

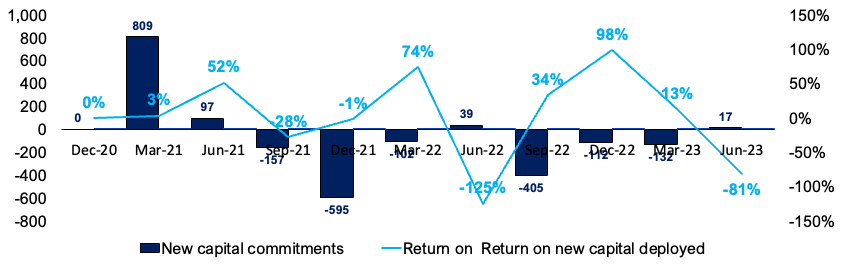

- Not investing for growth, minimal reinvestment runway

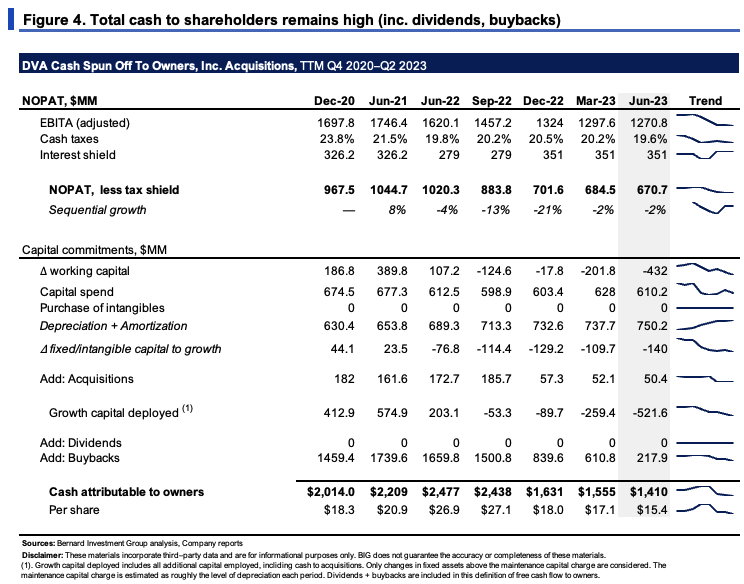

DVA is FCF positive, there's no doubt about this. Including buybacks, it routinely spins off $1–$1.5Bn in cash to its shareholders. However, a few notable trends are observed with the numbers shown in Figure 4. It shows the company's NOPAT, less the interest shield, and investments allocated to growth on a rolling TTM basis. Growth investment is calculated as all capital spending above the maintenance charge, which is approximated as the rate of depreciation. As you can see:

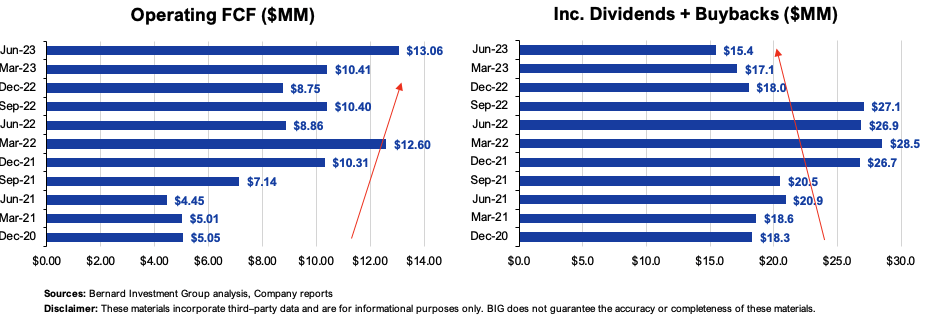

- FCF (inc. buybacks) are high but have been reducing on aggregate since Q1 FY'22, from $27/share to $15.40/share last period. Without the buybacks, it has actually increased from $8.86/share to $13 per share.

- Investments towards growth have been negligible. The firm has been paring back its capital investments and earnings reinvestment for the last 2 years. Whilst sales growth has languished since 2020, it has:

- Invested $0.99 towards M&A for every new $1 in new revenues,

- Reduced NWC by $0.39 on the dollar, adding to FCF by that much,

- Reduced fixed asset intensity by ~$3.60 for every $1 growth in sales. So in my opinion, a whack of the FCF it has thrown off each period has been related to changes in capital intensity, versus outright earnings power.

{kind=link}

{kind=link}

Adding to the economic hurdles, what investments the firm has made in the last 3 years haven't added shareholder value. Consider that:

- DVA had invested $149/share at risk into the business by Q2 FY'23, up from ~$129/share in 2020. Conversely, the firm's post-tax earnings have decreased from $11.77/share in 2020.

- The $149/share produced $11.20/share in tailing NOPAT last period, equating to 7.5% return on investment, in line with its historical range.

- More critically, the firm's post-tax margins and capital turnover are low on inspection, at 8.7% and 0.8x last period. This suggests it enjoys neither cost differentiation nor cost leadership benefits, nor does it enjoy consumer of production advantages. The capital employed to run the business is not highly profitable, simple as that.

Furthermore, the reinvestment runway looks to be short, as mentioned earlier. DVA has made minimal new investments from its earnings these past 3 years, M&A included. This would be great if only the earnings and FCF it was producing were substantially high and/or growing. But they aren't, as the return on incremental investment has been lumpy, and the returns on existing capital are low.

{kind=link}

{kind=link}

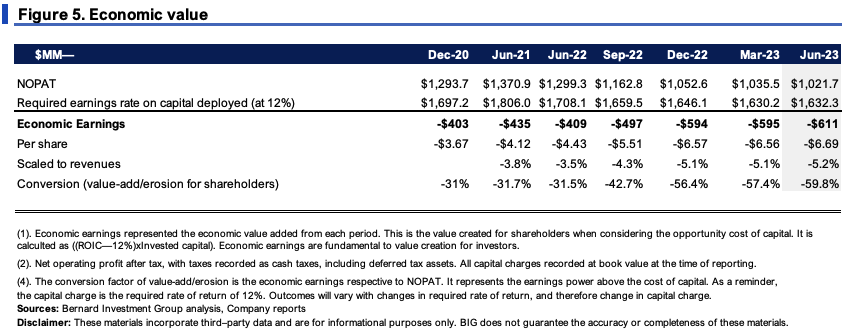

As a result, I'm not eyeing that DVA is creating economic value for its shareholders. I would go as far as to say there's a lack of economic value on offer. I say this because we employ a 12% required rate on capital for all current and potential equity holdings, in line with long-term market averages. Figure 5 outlines what DVA needed to have produced in NOPAT to hit this threshold rate, compared to what it did produce. Anything above the threshold rate is economically valuable and vice versa. As seen, there have been economic losses since 2020, at $6.70/share last period.

{kind=link}

3. Price implied expectations and valuation

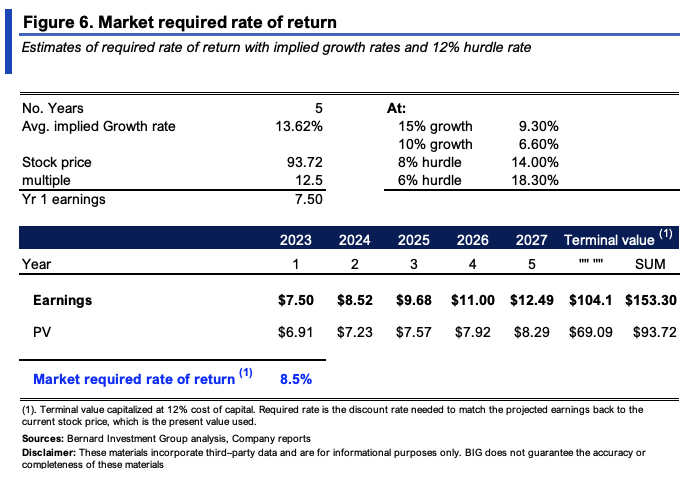

It's a useful exercise to see what needs to occur in order for DVA's current market values to make sense. You can buy DVA for a market value of $8.55Bn and an EV of $21.3Bn as I write. It sells at 12.5x forward earnings and 13.33x forward EBIT. This implies the market expects ~$7.50/share in FY'23 earnings (93.72/12.5 = 7.49) and $1.59Bn in pre-tax income (21,300/13.33 = 1,597). Both imply a YoY growth of 14–21% across the figures.

Consensus expects an average 13.6% earnings growth rate from '23–'25. I assume this will continue until FY'27, and then I've capitalized the terminal value at our 12% threshold rate. In the model shown in Figure 6, the market's required rate of return on DVA is the discount rate needed to discount these future values to the current stock price of $93.72 as I write. You can see, under this convention, the market has an 8.5% required rate of return on DVA, ranging from 6.6% to 18.3%, depending on various stipulations (Figure 6).

Do I believe the company will achieve this? For one, this is above what DVA has been producing on its capital investments, as outlined earlier. Secondly, this doesn't capture the additional investment activity it would need to deploy in order to achieve these rates. I'm not confident, therefore.

{kind=link}

Relating to the points on leverage before—how this links to the firm's ROE and valuation is telling:

- As mentioned, the company produced a trailing ROE of 46.4%, helped by its use of leverage.

- Still, this may be considered high—and it is, especially compared to the sector median of negative 42.5%.

- But investors are asking to pay 8.4x book value, implying its net asset value is worth that much—8.4 times $1.02Bn ($2.7Bn inc. all minority interest). So you're being asked to pay $8.5Bn ($22.7Bn) for a book value of equity recorded at $1.02Bn.

- For the investor, things are now entirely different. The ROE of (467.7/1017.4 = 46.4%) is now priced at just 5.4% for the investor if paying that multiple (467.6/8,550 = 5.4%). This is below the required rate of return outlined earlier as well.

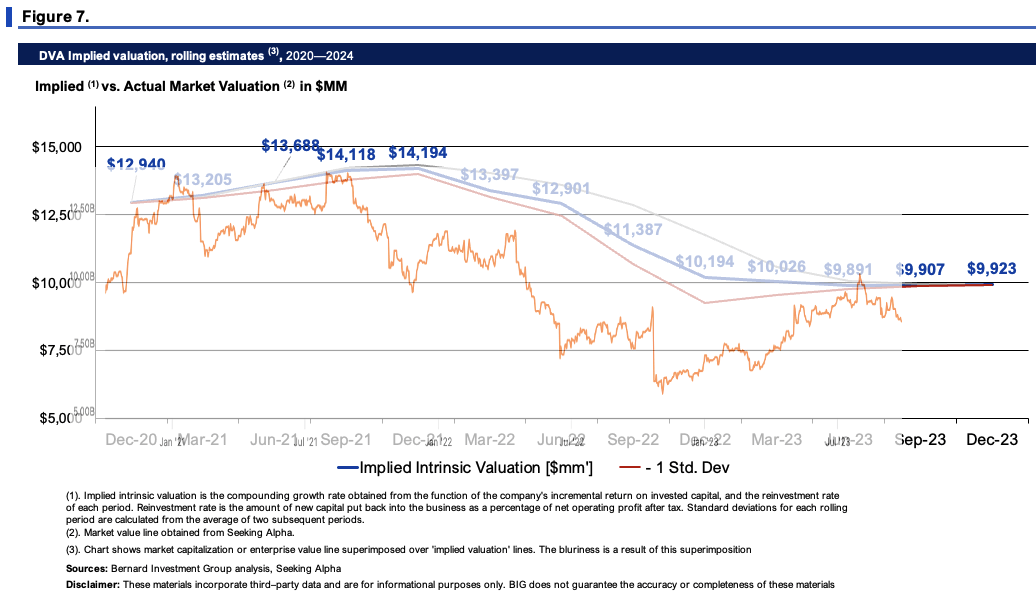

Finally, investors have priced the company at 1.57x EV/invested capital, a small premium that indicates its flat expectations going forward. The market looks to have been a good judge of fair value these past 3 years as well. Compounding DVA's intrinsic value at the function of its ROIC and reinvestment rates, including FY'23 forecasts, implies the company is fairly valued at its current marks (Figure 7). Hence, I estimate the company is trading within its fair value range.

{kind=link}

Discussion summary

Based on the myriad of factors raised here today, a hold rating is well-supported for DVA at this point in time. The question of opportunity cost immediately arises. The firm is producing a sub-par rate of earnings on its investments, both new and existing. It has not been investing towards growth either. Whilst its financials have shown promise via healthy unit economics, how this translates to shareholder value is yet to be identified in this examination. Instead, the market's expectations indicate a rather flat outlook for the company's stock price moving forward. Based on my assumptions, there is no reason to deviate from this view. It would appear that DVA is valued fairly at its current marks. Based on the factors raised here today, reiterate hold.

For further details see:

DaVita: Continued Economic Hurdles, Market Expectations May Be Correct