DVA - DaVita: Simple And Compelling After Sell-Off

2023-10-26 09:46:18 ET

Summary

- Concern over weight loss drug Semaglutide has caused an unjustified sell-off in DaVita shares.

- Dialysis is essential to life for people with late-stage chronic kidney disease, making DaVita non-cyclical and resilient in any macro.

- DaVita has a significant market share, competitive advantage, and has historically been an aggressive share repurchaser.

- At 7x FCF, DaVita is a compelling investment opportunity, even after factoring in risks created by leverage and the potential for obsolescence.

Even Ben Graham would be stunned at the character arc of Mr. Market, the emotional character featured in The Intelligent Investor . The added complexity of flows, sentiment, and speculation have exacerbated his mood swings.

The ripples across the market created by weight-loss drug Semaglutide reflects this strangeness. Consumer staples, ranging from Coca-Cola ( KO ) to McCormick ( MKC ) kickstarted a sell-off on fears that GLP-1s might meaningfully impact consumer spending. This spread to dialysis giant DaVita ( DVA ), following a positive Ozempic trial for kidney disease .

The collision between a perceived negative catalyst for DaVita and strange market dynamics have created one of the most compelling risk to reward opportunities in recent memory. For value investors capable of removing themselves from the information flow matrix, they will find a clear opportunity in my view.

Fundamentals:

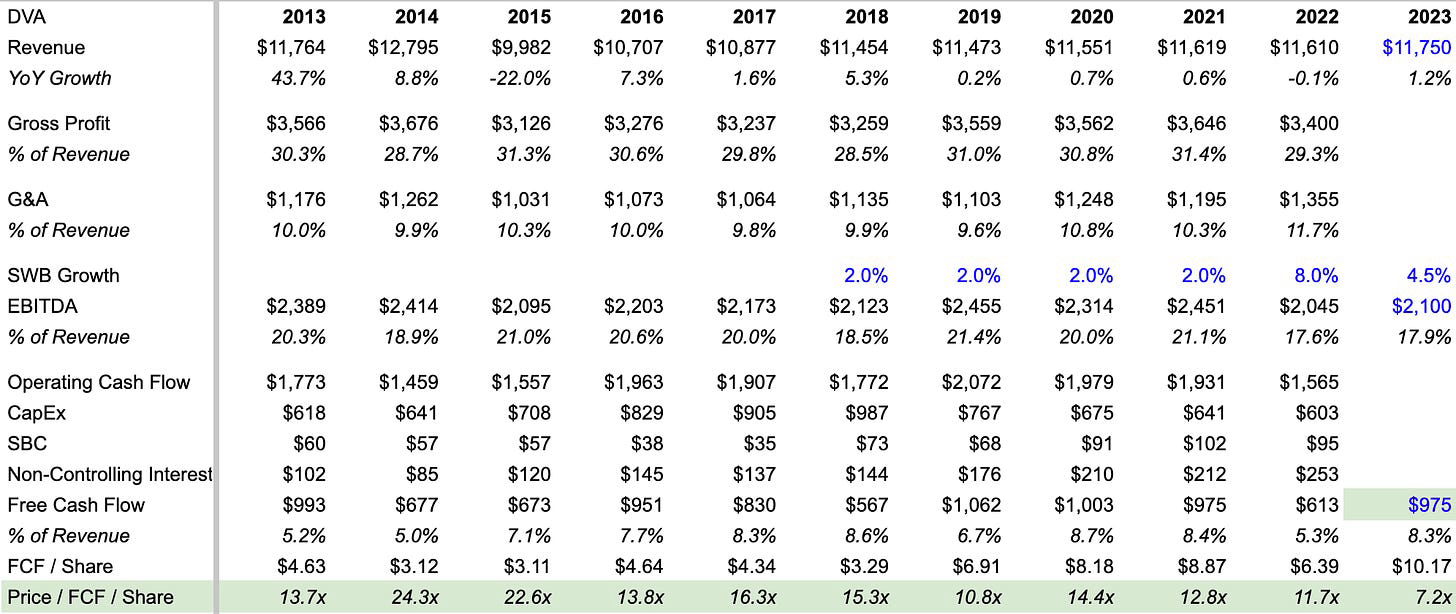

The DaVita thesis is simple for one reason: dialysis is essential to life for people with late-stage chronic kidney disease. This means DaVita is non-cyclical and thus insulated from macroeconomics, so forecasting future earnings is quite easy. Typically stocks that trade at cheap multiples have fundamentals heavily influenced by extraneous factors and market conditions.

DaVita has a 36% market share in US dialysis according to its 10-K. DaVita’s market share is solidified by its size advantage and relationships with kidney doctors who recommend their patients to dialysis centers. Industry growth is flattish, a few percentage points in either direction doesn’t affect the intrinsic value calculation much.

DaVita employs 70,000 people and has spent $7.3B in CapEx over the past decade. The business is labor and capital intensive, and may be replaced by better treatments options somewhere down the line. This makes it extremely unattractive for new entrants to try grabbing existing market share.

DaVita's payers are stable entities. Less than 1% of revenue is paid by patients. 2/3s of revenue is treatments covered by government programs such as Medicare and Medicaid. The other 1/3 of revenue, and 100% of profits is from commercial insurers. Insurers are required to pay the first 33 months of a patient’s treatment costs.

Valuation:

When the math is very simple, investors must take a stand against Mr. Market.

DaVita is ultimately a bet that the business will not be meaningfully disrupted over the next decade. DaVita trades at 7x FCF or a 14% FCF yield with the US 10 year yield at 5%. If FCF stays flat (base case), and DaVita resumes aggressive share repurchases, DaVita will trade at 5x or a 20% FCF yield in just 2 years. Other stocks victimized by Semaglutide aren’t as big a bargain.

DaVita’s hasn't traded at this cheap of a multiple in the past decade:

{kind=link}

DaVita has repurchased 120M shares since 2015, leaving just 93M shares outstanding. 36M or about 40% of those are owned by Berkshire Hathaway (BRK.B) (BRK.B). At today’s share price, DaVita could theoretically repurchase all shares not owned by Berkshire in the next 4.5 years. Ted Weschler laid out an equally simple thesis for DaVita back in 2011, and even though the stock price has underperformed, DaVita has significantly increased intrinsic value:

“When we explained buyouts to prospective management teams (in private equity), we told them there were 3 ways to increase the value of their equity stakes: (1) increase EBITDA, (2) pay down debt, and (3) get the market to apply a higher multiple than paid initially in the transactions. With public companies, the above 3 value-creating methodologies still apply, with the addition of an important fourth: Through active capital management, repurchase shares at less than their intrinsic value. I expect all four of these methodologies to be working in our favor at DaVita over the foreseeable future.” - Ted Weschler, 2011

DaVita paused buybacks this year to focus on reducing debt to the standard level of 3-3.5x EBITDA, down from 4.1x in Q2. DaVita is highly levered, but is paying an interest rate of 4.3% across fixed and hedged debt which makes up over 90% of total debt. This means DaVita is paying a lower rate than the US government can borrow for today. About 30% of its debt matures in 2026, 15% matures in 2028, the bulk of the rest doesn't mature until 2030 or later. Should higher interest rates persist, that could introduce a modest headwind several years down the line.

Risks

There’s no way of predicting if or when dialysis becomes outdated. Experts say Semaglutide is not a miracle drug . Billions in market cap wiped out across companies over something less than a miracle drug doesn’t seem indicative of efficient markets, but of a rare opportunity for active managers.

There's fringe risks to DaVita, such as litigation, cost inflation, and payer mix shift. But, the only meaningful risk in the near term would be complete technological disruption via artificial kidney. This also appears unlikely, however, The Kidney Project is hoping to have a commercially artificial kidney by 2030, meanwhile KidneyX is still issuing research teams small grants . Without being a leading expert in kidney care or having a crystal ball, investment is one of the best indicators of the practicality of an emerging technology. The size of these projects seems relatively small thus far, which doesn't signal disruption is imminent. This means dialysis and kidney transplants might be the only viable options well into the future.

While 7x FCF is extremely cheap, even in the higher current rate environment, debt causes more dramatic swings in equity valuations when duration is called into question. 7x FCF is only the true multiple if the business lacks existential threats. The odds are low but not 0% as discussed. Even so, the relationship for equity holders and bond holders is not 1:1, which is why bond holders place more emphasis on EBITDA over FCF or earnings. Given a business finds itself in dire straits, interest, taxes, and growth capital expenditures won't be relevant to bond holders being made whole in a short period of time.

While the current valuation of DaVita seems heavily in the favor of equity holders generating outsized returns, a discussion of the downsides, particularly as related to leverage, is necessary to keep equity holders vigilant. Even seemingly slam dunk investments must be scrutinized with a fine tooth comb. As the saying goes, there's no free lunch, so it's important to keep the other side top of mind when tracking an investment. Those not purchasing DaVita today are likely bothered by the leverage and perceived durability.

But given the now depressed share price, and FCF guidance raises translating to higher EBITDA to bring the business to a more comfortable leverage range, management should be firing up the buybacks again shortly.

Conclusion:

The negative commentary around GLP-1s and DaVita’s falling share price seems like it’s straight out of the twilight zone. Daniel Drucker, whose early research on Gila monster venom inspired GLP-1 drugs, has more balanced approach to the rise of GLP-1 s:

“It will only scratch the surface of the problem in the population that needs to be healthier.”

The benefits to happiness and economic prosperity of an increasingly healthy populace would be significant. But value investors must invest in the world we have today, rather than the world we may have in the future. Investing is about profits and probability, given DaVita's stable business, cash flow should remain flattish without meaningful disruption. This should allow the business to return significant amounts of capital to shareholders which typically results in a higher share price.

Editor's Note : This article was submitted as part of Seeking Alpha's Best Value Idea investment competition , which runs through October 25. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

DaVita: Simple And Compelling After Sell-Off