DVA - DaVita: Valuations Forward Growth Unsupportive Of Buy

Summary

- Mixed Q4 results throughout the P&L and per-patient measures.

- Projects flat bottom-line growth in FY23, with further downsides in FCF.

- Valuations aren't supportive of a re-rating or valuation upside.

- Net-net, rate hold.

Investor Summary

DaVita Inc. ( DVA ) reported a mixed set of quarterly results earlier this month, with a number of factors compressing growth in treatment volumes and per-patient metrics. DVA is a long-term cash compounder with interesting unit economics that will likely remain resilient in the event of an economic downturn. However, the underlying treatment domain of chronic kidney disease ("CKD") is evolving, and the company reports it is still facing challenges with COVID-19 and the impact to its patient base. Moreover, we're being asked to pay >10x value and 8x FY23E FCF at current market value, for relatively flat bottom-line growth and a c.$200mm pullback in YoY FCF this year. Net-net, DVA stock has hurdles to overcome to justify a buy rating when there are numerous other selective opportunities available to position against for mid to long-term alpha. I'm not counting the company out, but do rate it a hold for now.

Deeper look at DVA's fundamentals

Across the FY22 period, DVA experienced a downturn in revenue growth due to lingering effects of COVID-19 that subsequently lead to lower treatment volumes. The reduction stemmed predominantly from the mortality rates of the pandemic on CKD patients, and, from what it seems, the epidemiology of CKD itself. I'd note the flow-through of this resulted in lower patient census, and a decrease in new admissions, coupled with an increase in missed treatments – each clamping volume growth. DVA also estimates a compounding effect of these points on long-term volume and revenue growth, along with new patient starts. Further, the CKD populous' elevated mortality rates may also feed into this as another headwind to new admissions and future revenue upsides. For instance, Kovesdy (2022) noted that CKD mortality rates are on the rise, expected to be the 5th rank in cause of death by 2040. Alas, this reduces the tail of treatment-specific returns that will be attributable to DVA over the mid to long-term, including the number of outpatient dialysis centres on its books, by estimation. To this point, by the end of FY22, the company's U.S. dialysis business operated 2,724 outpatient dialysis centres, that served ~199,500 patients, and provided inpatient dialysis to c.820 hospitals. From these figures, the company estimates that it has ~36% market share in the U.S. dialysis industry based on its patient base. Subsequently, ~91% of its FY22 turnover was derived from its U.S. operations, the remainder obtained from its international markets, with a footprint in 11 countries outside of the U.S. ("OUS").

{kind=link}

Fig. (1) DVA U.S., OUS Footprint

Data: DVA 10-K, pp.10

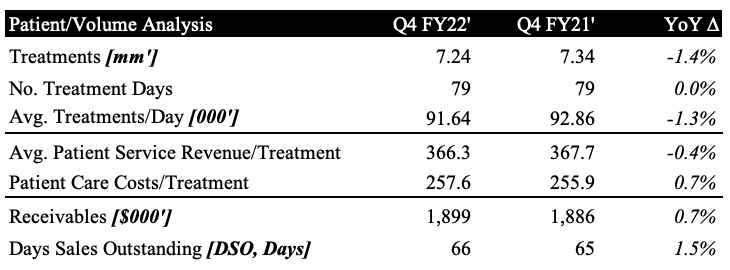

Looking specifically at Q4, the total number of U.S. dialysis treatments was 7.24mm, down 140bps YoY [Figure 2]. Non-acquired treatment growth was 2.1% behind the previous year. The company also opened 6 de novo dialysis centres in the U.S, but closed 58 centres in the same market. OUS, it acquired and opened 3 dialysis facilities respectively. On its centre eliminations, it booked ~$34mm in closure costs, having a $6mm headwind to patient care costs and another $5mm headwind to the G&A line. This pulled through to ~$86mm in full-year expenditure from its closures. Further, the number of treatment days was flat at 79 days, however, secondary to the points raised above, the average patient revenue per treatment slipped back by ~40bps to $366. Days sales outstanding ("DSO") were relatively flat at 66 days, but I'd suggest we need to see some improvement there to increase DVA's cash conversion cycle as receivables also lifted by ~70bps YoY to $1.9mm for the quarter, leading to a c.9% YoY gain in total accounts receivable to $2.13Bn.

Fig. (2)

Data: Author, adapted from DVA 10-K

{kind=link}

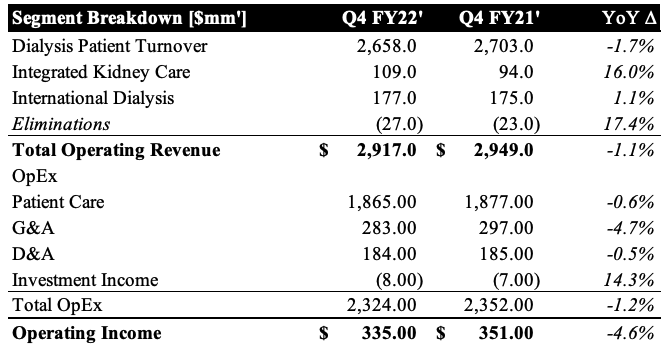

Turning to the numbers, the company booked flat Q4 revenue of $2.9Bn, and pulled this down to operating income of $355mm and adj. EPS of $1.11, the upper end of its guided range. Looking at the GAAP numbers, EPS was $0.61 versus $1.86 in Q4 FY21 on earnings of $68.1mm, a 63% YoY decline. With respect to the specific highlights, I'd note the following:

- Honing in on measures from its U.S. segment, DVA clipped a 1.3% decline in treatments per day, primarily from the factors affecting volumes listed earlier [Figure 3]. As a result, patient care costs per treatment rose by $1.70 YoY, seasonal flu expenses, year-end benefits, and lower fixed cost leverage as treatment volume declined. These effects were partially offset by lower contract labor costs in the quarter.

- Meanwhile, DVA's integrated kidney care ("IKC") business recorded a flat sequential operating income, but was up 16% YoY to $109mm. It also recognized a $15mm reduction in adj. operating income, underlined by a $7mm FX headwind and expenses related to acquisitions in Brazil.

- Notably, DVA did not repurchase any shares in Q4, citing its intention to use excess capital to pay down debt and move toward a target leverage ratio of 3x–3.5x EBITDA. To this point, it paid down $260mm in debt over the 12 months, exclusive of financing costs, with the net debt figure now at $8.7Bn. Alas, net leverage is still at ~4x, at a weighted interest rate of ~4.5%. Around half of this debt is fixed, and 90% is fixed when factoring in cap agreements.

Fig. (3)

Data: Author, adapted from DVA 10-K

{kind=link}

FY23 guidance points to flat upsides down the P&L

DVA management provided clear guidance on the call. It expects flat adj. operating income growth, calling for a range of $1.4Bn–$1.6Bn, looking to pull this down to adj. earnings of $5.45–$6.95 per share. I'd note there are several assumptions underlining these numbers. In particular, the company expects an increase in treatment volume is the "lack of a winter COVID surge" . Hence, any uptick in COVID-19 is likely to compress these growth assumptions, by my estimation.

Moreover, with respect to its U.S. dialysis business, DVA still expects a YoY delta in treatment volume between 0% and negative 3%. On this, it looks to a patient care cost/treatment increase of ~ 250bps, driven by wage growth and inflationary pressures – although it wasn't specific on how inflation was to impact the costs here. It also baked in a $50mm tailwind to operating income as the California ballot initiative spend recognized in FY22 won't be recognized this year. Importantly, with respect to its Medtronic transaction, it expects this to close in H1 this year, on an initial cash consideration of c.$300mm on completion. In terms of its rates sensitivity and leverage, management have projected an interest expense of $425mm at the upper end, finally reaching a net leverage target of 3.6x–3.9x.

Valuation and conclusion

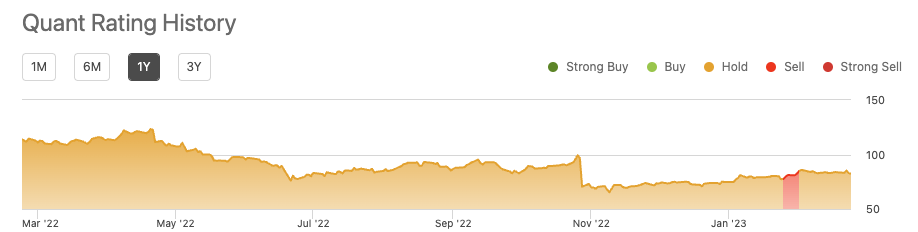

On face value, it could be argued the stock is attractively priced at 13–14.4x non-GAAP/GAAP earnings, a 32–41% discount to the industry. However, it is also priced at >10x book value, meaning the trailing ROE of 74.5% compresses to an investor ROE of just 7.45% if paying that multiple today. This aligns with DVA's 5.8% trailing return on capital as well, well below the company's 5-year average of 6.8%. Looking at the valuation in more detail, we're being asked to pay >14x earnings for flat growth, alas the PEG ratio is at 5.6x – more than 185% ahead of the industry. Hence, we're not seeing value in DVA when factoring all the moving parts to the valuation debate. Taking management's adj. EPS range of $5.45–$6.95, the 13x multiple gets us to a range of $70.8–$90, not sufficient upside potential or margin of safety to advocate for a buy right now. This is further supported by the quant ratings system voting DVA as a hold, as well.

Fig. (4)

Data: Seeking Alpha, DVA, see: "Ratings"

{kind=link}

Net-net, there looks to be a number of hurdles DVA must overcome into the coming periods in order to attract a re-rating to the upside. With flat YoY growth projections, coupled with a hefty premium to its book value, the company looks overpriced in my estimation and warrants a neutral stance. Alas, rate hold.

For further details see:

DaVita: Valuations, Forward Growth Unsupportive Of Buy