DDHLF - DDH1: Event-Driven Snappy 25% Upside In Highly Resilient Business

2023-06-26 08:56:05 ET

Summary

- It was just announced that DDH1 will be acquired by Perenti in a cash and stock deal, mostly in stock which could be to the benefit of DDH1 holders.

- DDH1 remains substantially undervalued at the implied price compared to similarly sized drilling contractor peers in other developed markets.

- Low liquidity and concerns of a chunky Oaktree disposal have been problems for the DDH1 stock since it listed, a problem which will be resolved as part of Perenti.

- In the short term, Perenti will likely reprice as the deal is rich with synergies and accretive, which will stimulate DDH1's price since its purchase consideration includes acquirer stock.

- With transaction closure expected in October, DDH1 shareholders can see the low-valued DDH1 earnings gain a multiple bump as part of a larger and more liquid Perenti for 25%+ upside.

DDH1 ( OTCPK:DDHLF ) is a stock we've held in the portfolio for a while now, providing some years of ample and growing dividends as well as capital appreciation undergirded by its solid and relatively commodity-agnostic contract drilling business.

It has just been announced that Perenti ( OTCPK:AUSDF ) is acquiring DDH1 in a cash and stock deal, primarily in stock. Perenti has traded down on this news and therefore so has DDH1, but we believe markets will quickly acknowledge that DDH1 is being acquired at a headline accretive and more importantly fundamentally low valuation, and even with dilution, the earnings being added come at an undervalued price - in other words that this transaction actually adds value to Perenti shareholders by being a bargain buy.

The value of DDH1's earnings are likely to be better appraised as part of Perenti since DDH1 was stuck with a liquidity discount and also block sale concerns around the large holding maintained by Oaktree since before it was listed. DDH1 has always been valued at almost half the PE and EV/EBITDA multiple of Major Drilling ( MDI:CA ), which is a very close peer in scale and services, and DDH1 is cheap compared to all the other contract drilling services too. Perenti has more liquidity and is a substantially larger business with 50% more net income than DDH1.

As markets appraise the high synergies and low valuation of the DD11 deal (which might take a while because the presentation links on the DDH1 website went down for a while after market close) we think DDH1 shareholders can benefit from Perenti's repricing since that would directly increase DDH1's implied purchase price due to the largely stock deal. If markets start to respect the synergy potential and the value capture from folding DDH1 into their liquid and ASX 300-included company, that value would be unlocked if DDH1 earnings are valued at Perenti's overall PE multiple, or similarly in line with DDH1's peers, as part of Perenti overall. shareholders including Oaktree already stated their intention to support the deal so it's likely to go through, and if it weren't to go through, DDH1 is a resilient and dividend paying business that you'd anyway like to own, with the chance of getting an even better price in the future once private markets and sponsor activity starts picking up again. Since this is event driven, market participants have a clear horizon for this investment, and a 25% upside in less than half a year would be excellent.

A Review of DDH1

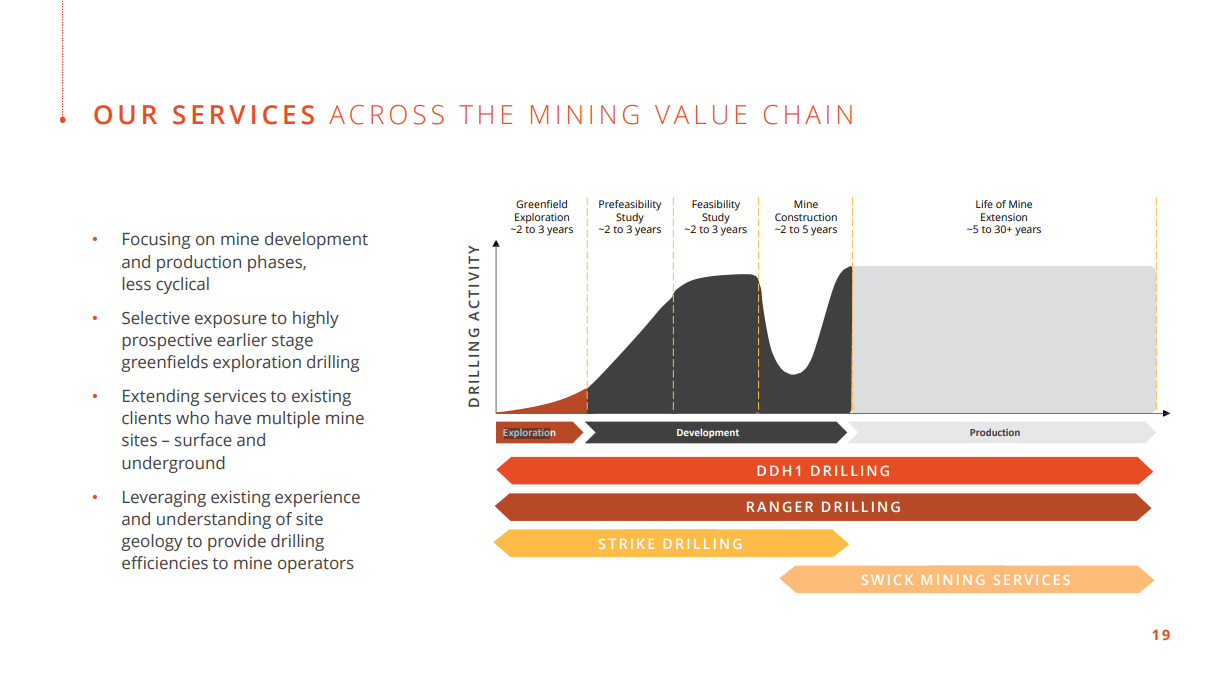

We covered DDH1 some time ago in this article . To review, the company provides contract drilling services, so both the drills and personnel, for the benefit of mining companies. Their drills are designed to go very deep and collect samples that can indicate whether there is a statistical case to mine a certain area, or just to collect routine samples from an area that is already mined. The vast majority of the revenue is made in expansion of mines and other more commodity agnostic or even regulation-mandated reporting activities, while a small proportion is connected to exploration activities that will be more motivated by commodity prices. Drilling activity is the KPI, since DDH1 bills on the use of the drills, and are not compensated based on the outcome of the drilling at all. The main driver of secular growth in the industry is depleting reserves and systematic underinvestment in commodity mining. Gold reserves are depleting, and importing commodity for DDH1, while the gold price is rising as people look to it as a safe haven for investment purposes. Commodities like copper also seem to be at the start of a supercycle connected to the renewables boom, so CAPEX is picking up for those mining projects which includes sampling activity by DDH1.

{kind=link}

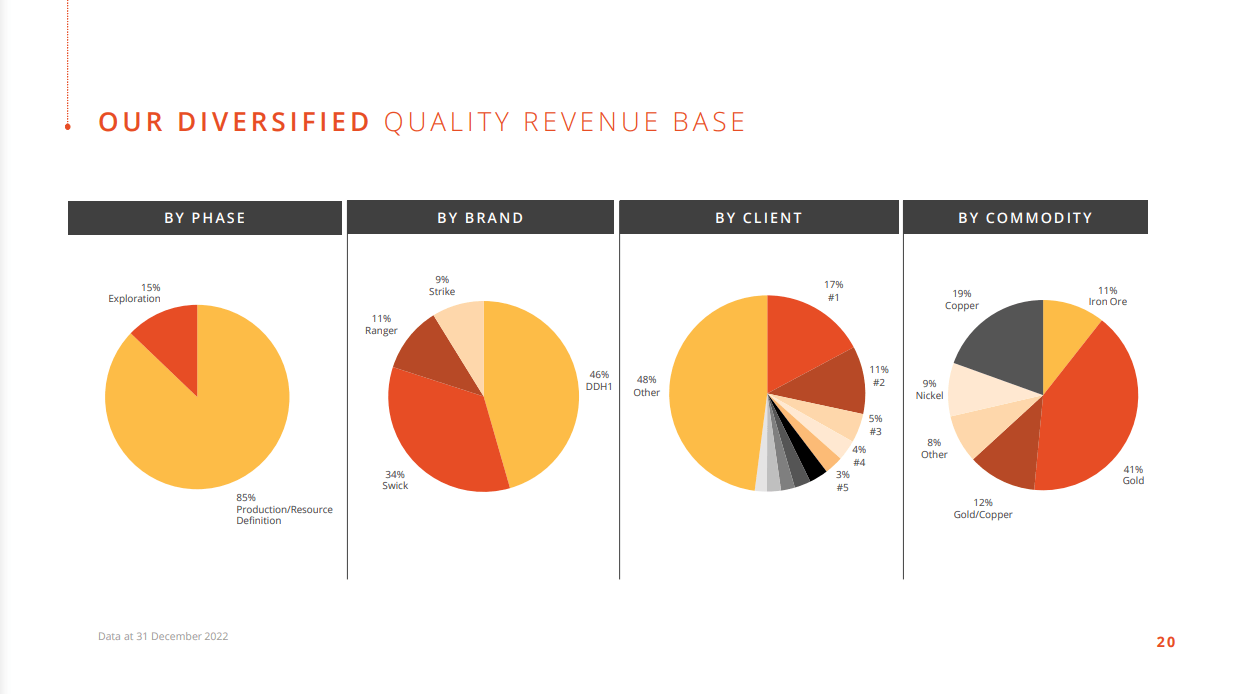

When we covered DDH1, they were primarily exposed to gold miners. While they did merge with Swick which changed their profile slightly (by the way this merger consolidated a cheap <5x EV/EBITDA drilling contractor into the fold), they are able to flex their capacity into whatever commodity is popular at any moment. Their drills can work on sites for a range of commodities with no switching issues. For example, copper has grown meaningfully in the mix.

{kind=link}

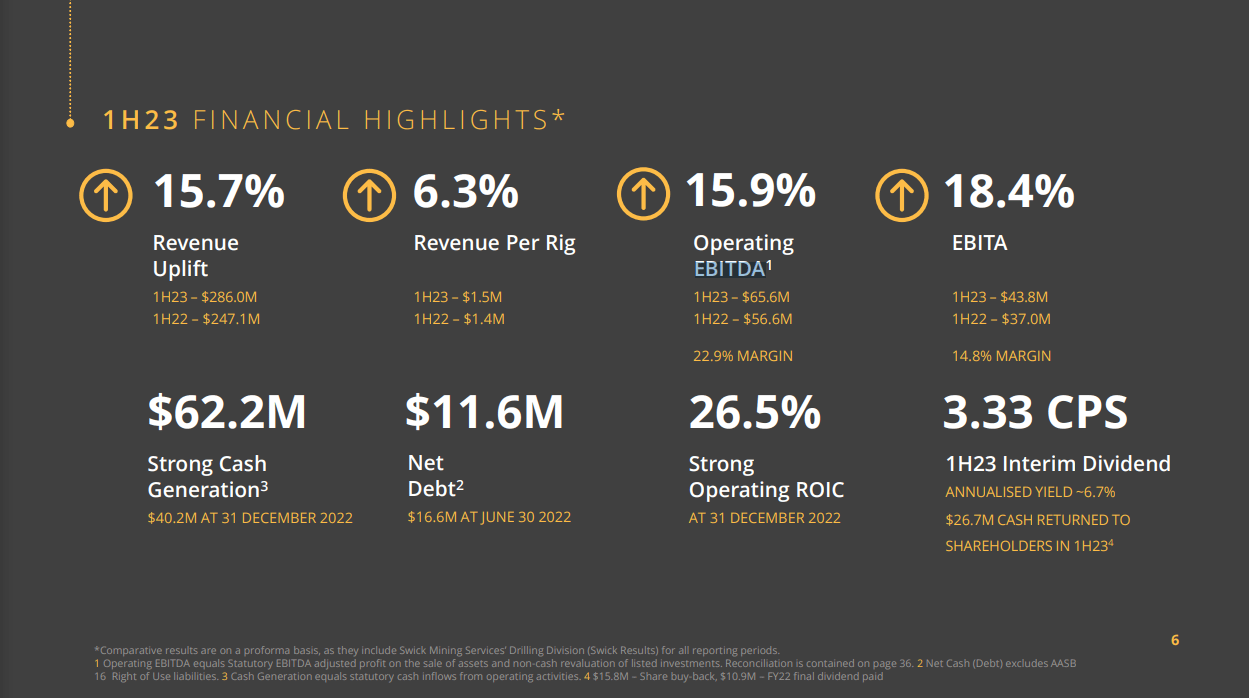

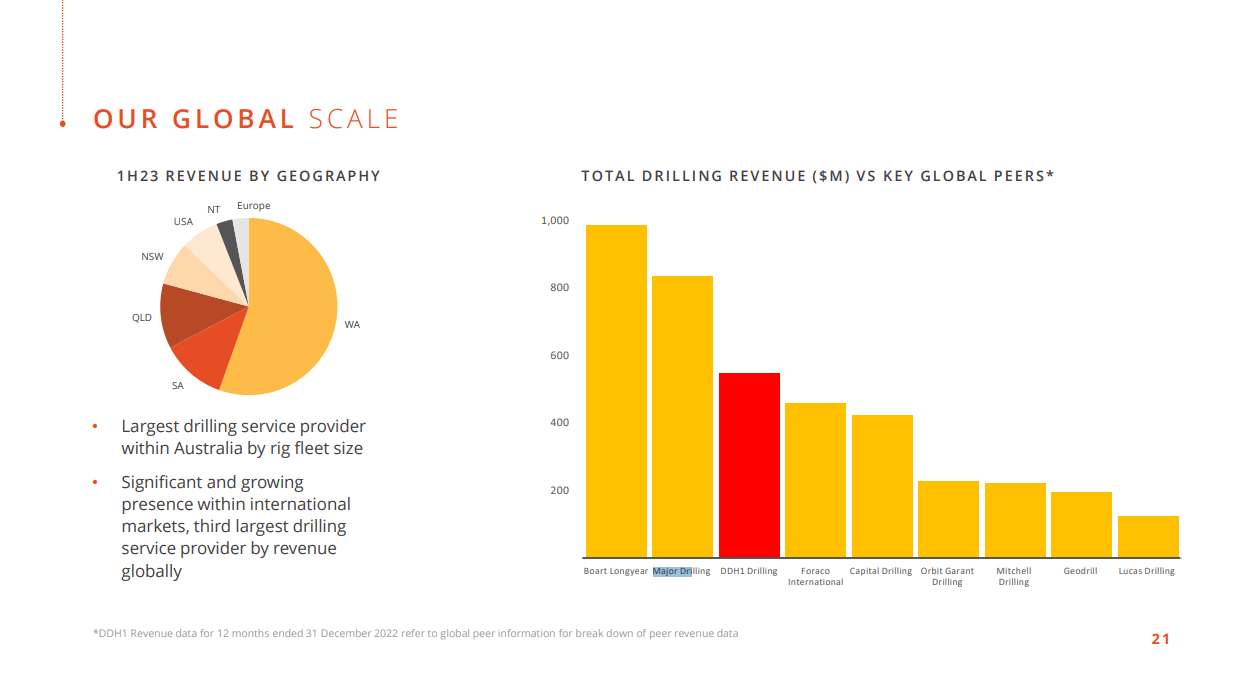

The plurality of their activity is in Western Australia, which is Australia's mining region, but about 10% of their income is international too. The performance has been great. Pricing action as of the H1 2023 reported in February had offset labour inflation, which is a principal consideration for the company since workers in contract drilling get paid quite a lot and have a lot of bargaining power because the conditions are pretty darn difficult. Operating profit grew 16%, same as revenues, and this was driven mostly by drilling activity versus price by about a 2:1 ratio.

{kind=link}

While in the earnings call management did note that miners were slow out the gate to start the expected drilling activity, which softened guidance, DDH1 has updated shareholders as of the Perenti announcement with a disclosure that they expect EBITDA to be basically flat in evolution for the FY 2023 compared to last year, which is good considering the confluence of pressures on economic activity and the reversal in commodity markets - so the commodity agnosticism is demonstrated here.

Margins are great, actually better than Perenti's, and the business is very cash generative at 100% EBITDA to operating cash flow conversion. It trades currently (even at acquisition prices) at less than a 7x PE, and it has a dividend yield that exceeds 7%, although dividends are only a consideration if DDH1 were to continue without being acquired, which seems unlikely at this point. We think this price is extremely cheap, since Major Drilling trades at around a 10x PE on a forward basis versus DDH1's 6x PE on a forward basis. There is similarly almost a 2x difference in the EV/EBITDA multiples as well between the companies, even though DDH1 is absolutely of comparable size, scale, profitability and overall economics.

{kind=link}

The Acquisition Terms

The acquisition is cash and stock. DDH1 shareholders will receive as a default from Perenti 0.1238 AUD in cash per DDH1 share as well as 0.7111 Perenti shares per DDH1 share. The result in terms of dilution is definite, which is that DDH1 shareholders will end up owning 29% of the combined entity . There is even the option to use a slider between the cash and stock elements of the consideration with limits of a 50 million AUD cash pool for paying out cash to DDH1 shareholders. Since the cash consideration slated as default is already more than 40 million AUD to DDH1 shareholders, there isn't much more space for cash to be paid out as part of the deal, so the slider will primary support shareholders interested in even more Perenti stock.

The big shareholders, including Oaktree and the 13.1% of stock owned by management, are all in favour of the acquisition and Oaktree at least intends to go with the standard cash and stock consideration. Management and major shareholders that have stated their intention to approve the transaction are collectively owning 38% of DDH1, which is very substantial.

The fact that it is a primarily stock deal also means that management is not throwing in the towel in terms of believing that DDH1's intrinsic value is even higher than today's purchase price, just that it may be more easily achieved as part of Perenti. We don't think shareholders will disapprove of the transaction, unless they have a major problem with Perenti's current business which seems unlikely given that they are in the same sphere as DDH1 already in contract mining and mining services, just not pure-play in drilling which is only a subset of the mining service ecosystem. We believe that DDH1 indeed has a better chance of seeing its value realised within Perenti than outside of Perenti.

As of previous close the DDH1 share price is 0.915 AUD, where it was at 0.94 at some point during trading until Perenti's shares declined, reducing the implied DDH1 purchase price.

Valuation

There are two reasons why we believe holding DDH1 from this point forward would be supported by a valuation case. The first is a trading consideration, which is that from within Perenti DDH1 could converge on a valuation like Major Drilling's, or the overall Perenti PE multiple (which is almost the same as Major Drilling where Perenti also operates in a similar sphere of contracted mining and mining service provider), which is what we hoped for DDH1 as a standalone entity. We think this could happen because Perenti is more liquid while DDH1 is not as a standalone stock. Perenti is more institutionally held, since it is in the ASX 300 index . Also Oaktree will own 5.7% of the combined group of Perenti + DDH1, while Oaktree owned 20.13% of DDH1. That 20.13% in standalone DDH1 is a major overhang on a stock with DDH1's liquidity, because it could mean that if Oaktree decided to sell its block of shares the price would be under a lot of pressure for a long time. Because of DDH1's underperformance since IPO a couple of years ago, the chance of seeing Oaktree try to realise its position (held since DDH1 was a private company) once the stock begins to perform better was a real concern. At 5.7% of a liquid and large group like Perenti, these block-holder overhang concerns are much less pronounced, to the point of being negligible.

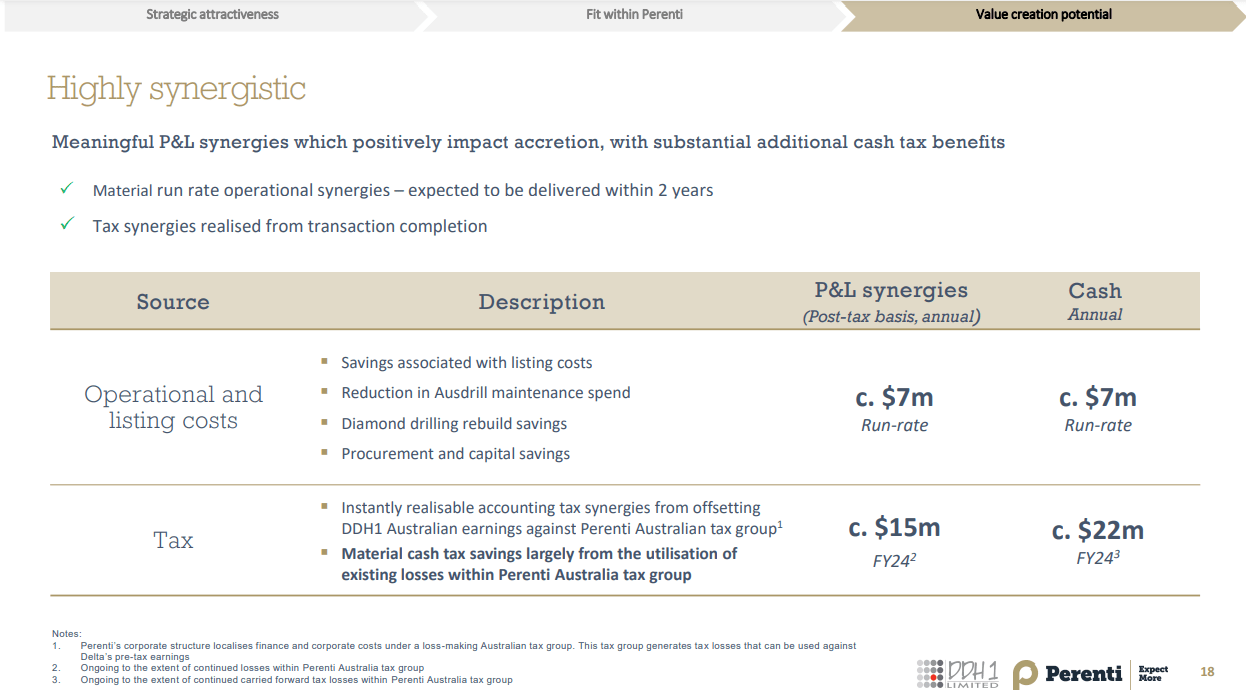

The second reason is simply to do with synergy considerations . In the acquisition presentation a very conservative synergy slide is presented with no demand-side synergy assumptions. Because of loss making corporate groups in Australia under Perenti, tax losses from this group can offset DDH1 earnings (which are primarily Australia-based) to create tax savings out of the Australian Perenti tax benefits. These tax benefits are less useful for Perenti as it currently stands, since Perenti is much more internationally exposed than DDH1.

{kind=link}

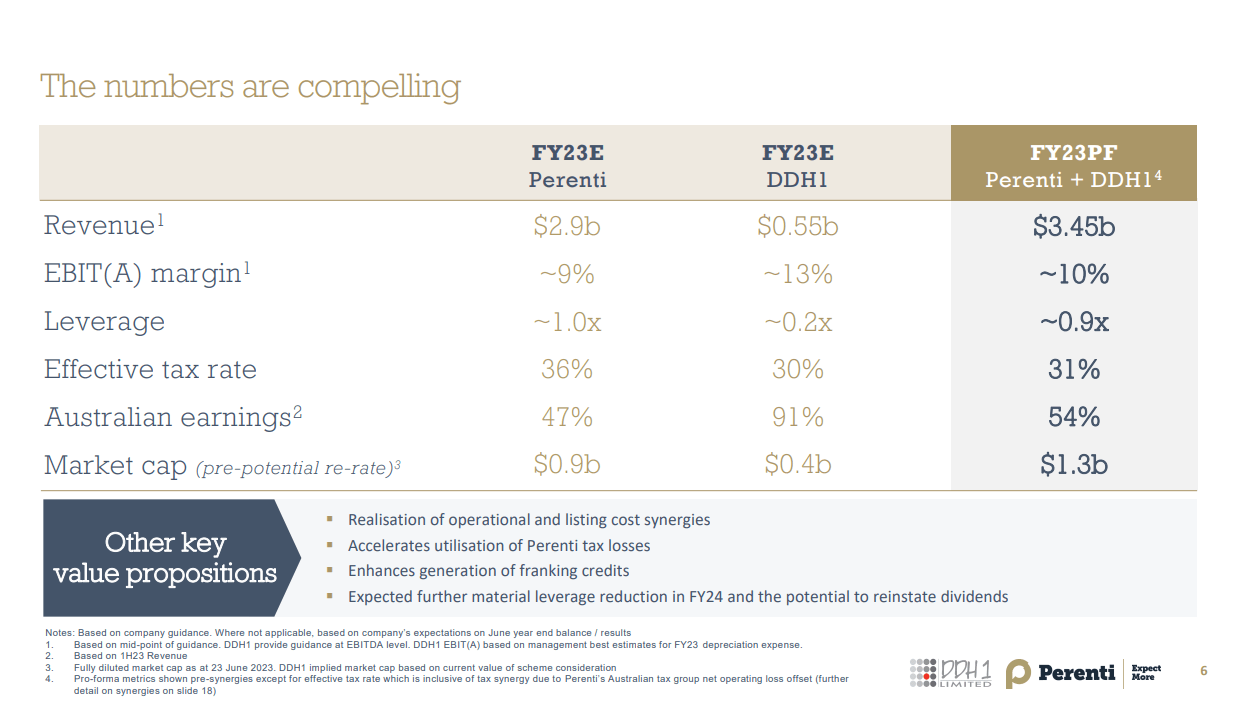

Tax benefit utilisation is the majority of the synergies at 15 million AUD annually. Then there are some cost side efficiencies gained of sharing listing costs and other stuff related to larger scale and shared backend. 22 million AUD is the proposed annual run-rate synergies on a post-tax basis, so right into the bottom line. Considering DDH1 earned 35 million AUD in net income, and Perenti 40 million AUD in 2022, synergies bump a simple proforma of the combined entities net income by 33% from 2022 figures.

{kind=link}

So what about valuation? Considering Perenti's average price over the last few days excluding the previous trading session, the price implied for DDH1 is 1.01 AUD per share, where it is currently 0.915 AUD. Taking an Expectations Investing (Rappaport and Mauboussin) approach, The fact that Perenti lost value on the notion that it would combine with DDH1 implies expectation of negative PV of synergies. The annual synergies per year are potentially 33% of the market cap that Perenti lost just today, so it doesn't really make sense to see these sorts of declines considering that the synergies will be on a run-rate basis more or less in perpetuity, assuming no major Australian tax changes. Perenti traded down likely as a consequence of the announcement being a major event and a significant change in the company's profile, and the fact that a dilution will happen. Moreover, the links to the merger materials went down for almost an hour around the previous session's close, so materials may not have disseminated very much. With passing jitters, we think as a very conservative case the price implied for DDH1 by 5-day moving average of Perenti's stock already makes sense, and gives about 10% upside assuming a mean reversion by Perenti.

But we can make a clearer case using combined market caps. Assuming run-rate synergies, the combined earnings can be calculated and then the current Perenti multiple could be applied across all the earnings. Perenti and Major Drilling are similarly valued on a PE basis, so this would assume the revaluation case where DDH1 had been discounted for liquidity and ownership factors as a standalone entity, with those negative factors no longer applying once acquired. We assume the capital structure would more or less be a blended version of the two companies (where in reality it will likely be something more optimal and more value accretive) for the market cap approach.

Valuation, two methods (VTS)

Ultimately, it is clear that DDH1 is bringing in half as much earnings as Perenti but at almost half the price multiple of 6x PE, and that if DDH1's contribution became valued in line with Perenti's current overall multiple after they are combined, there would be upwards of a 25% upside for DDH1 buyers holding onwards through the combination from the 0.915 AUD price. Similarly, you could get to almost the same valuation by just valuing DDH1 independent of the combination by the Major Drilling multiple as shown in the second valuation approach.

Bottom Line

While major shareholders already almost composing the majority of the shareholder base are in favour of the transaction, even if for some reason the transaction didn't go through, you would still own a company paying a 7%+ dividend at a great earnings yield. With favourable economics and resilience leading to flat EBITDA forecasts by DDH1 despite economic difficulties for the FY 2023, another strategic or financial sponsor would probably eventually come around to realise a higher multiple for DDH1 shareholders more in line with peers - once M&A and PE markets come back to life. With secular trends in CAPEX cycles for gold and copper mining, it is unlikely DDH1 will run out of business, and as a large base of new mines open there will be a larger base for their recurring revenue from expansion and periodic sampling activity. This business is relatively lower risk and comes at an undervalued price compared to highly comparable peers, and the fact that Perenti shareholders haven't been quick on the uptake after the announcement gives buyers looking at DDH1 a chance at a good, but possibly very time sensitive upside.

For further details see:

DDH1: Event-Driven, Snappy 25% Upside In Highly Resilient Business