MAA - Dear Santa: All I Want For Christmas Are A Few Good REITs

2023-11-30 07:00:00 ET

Summary

- I decided to write Santa a letter this year.

- Hopefully, he will put me on the nice list (as opposed to the naughty list).

- I would love to find out what's on your list?

- I will be writing a follow-up letter to Santa with the "naughty REITs."

If I was going to write a letter to Santa Claus this year, I know exactly what I’d write.

Dear Santa,

I hope you’re doing well, staying warm, and getting ready to eat a gazillion and three cookies in just a few short weeks.

You always want to start off strong, often by acknowledging whoever you’re addressing before you make your request. It’s the considerate thing to do, for one thing, and can also lead to much more effective outcomes.

I’m writing to you today to give you my Christmas wish list. If you really do know when I’m sleeping and when I’m awake, as the song says, you might already know this since so much of my waking time is spent working on these assets. But in case you don’t, I’d really appreciate a handful of good real estate investment trusts.

Because, really, what else would I ask Santa for?

Maybe five or six REITs? I don’t want to get greedy. I’m sure you’ve got a lot of presents to put together, but I also know you’re a discerning man. You no doubt recognize the sector’s overall strong balance sheets and bargain valuations.

Thank you so much for all you do, Santa, and I look forward to seeing your response.

Sincerely,

Brad Thomas

Signed, sealed, and delivered to the North Pole.

I’m Going for the Green This Christmas

I know some of you are laughing at that letter, and not because of the Santa aspect. At this point in 2023, you might be more willing to believe in Ol' Saint Nick than worthwhile real estate investment trusts aka REITs.

I get that. I don’t agree with it. But I do get it.

I also get that there are certain people I’m just not going to convince article to article. As much as I’d like to get everyone on board the real estate investment trust train – particularly right now when the situation is what it is – I recognize reality.

Still, for those who will listen, I’ll keep tooting this horn until I’m blue in the face. Or, considering the season, perhaps Christmas green.

Again, I don’t care if that’s an unpopular opinion. Which it undoubtedly is.

Take the Black Friday Benzinga article titled “ Analysts Slashing Price Targets During a Quiet Week .” Do you know what stocks analysts were slashing?

REITs.

“Analysts were busy sharpening their Thanksgiving knives” on at least four of them. Here’s the exact writeup on one:

“ NETSTREIT Corp. ( NTST ) is a Dallas-based retail REIT with 547 properties across 45 states… NETSTREIT reported its third-quarter operating results on Oct. 25. Funds from operations (FFO) of $0.31 per share beat the analyst estimate of $0.29 and FFO of $0.30 per share in the third quarter of 2022. Revenue of $33.96 million not only beat the estimate of $32.2 million but was $35.8% higher than revenue of $25.01 million in the third quarter of 2022.”

Even so, Michael Gorman of BTIG just lowered its price target from $23 to $19.

And, again, that wasn’t an isolated sector event.

Nobody likes REITs right now.

My Kids Are Getting Green This Christmas

In all honesty, I shouldn’t say “nobody.”

Clearly, I do, but – believe it or not – I’m not alone.

Even the Benzinga article that reported on those four REITs ended with this:

“REITs are one of the most misunderstood investment options, making it difficult for investors to spot incredible opportunities until it’s too late.”

Difficult, but not even close to impossible, thanks to statements like this one from Benjamin Graham:

“Paying out a dividend does not guarantee great results, but it does improve the return of the typical stock by yanking at least some cash out of the manager’s hand before they squander it or squirrel it away.”

I quoted him in a recent article, “ REIT Dividends: The Gift That Keeps on Giving ,” following up with this:

“At the end of the day, dividends are all about capital markets discipline .”

And this:

“Keep in mind, unlike ordinary C-corporations, REITs must pay out at least 90% of their taxable income in dividends to shareholders…”

And this:

“Given the attractive quality scored for each of these REITs (listed in this article) and the potential for outsized price appreciation, there’s a very good chance that this gift will be one of the best [Christmas] gifts [to my kids] that keep on giving.”

In short, REITs with strong balance sheets and healthy prospects are almost always going to be worth holding.

If you have them in your portfolio, they are very, very, very likely to keep paying you dividends quarter in and quarter out (or month in and month out) for a long time to come.

And REITs with strong balance sheets and healthy prospects trading at depressed prices? They’re almost always going to be worth buying for the same exact reasons…

Plus that price appreciation is a cherry on top.

Alexandria Real Estate Equities, Inc. ( ARE ) - Quality Score: 99

Alexandria Real Estate is a life science REIT and is possibly one of the most misunderstood REITs trading today.

The stock is categorized in the office sector, but ARE builds laboratory space for major pharmaceutical and biotechnology companies as well as leading academic institutions which includes names such as Pfizer, Merck, Boston Children’s Hospital, Harvard University, Moderna, and Bristol-Myers to name a few.

The important point is that ARE’s properties are designed for medical companies that develop medicine or perform research & development. Many of these tasks need to be performed in a regulated environment, which should insulate ARE from the threat of the “work-from-home” movement.

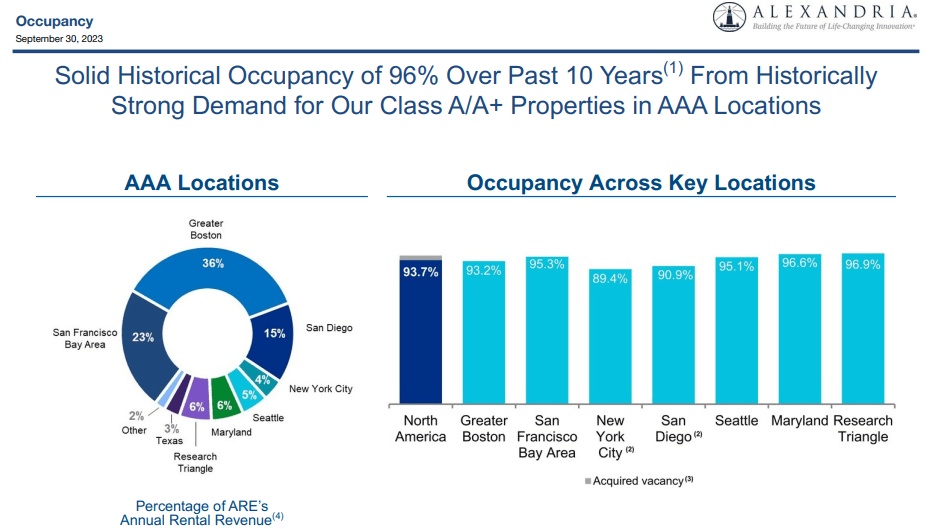

ARE specializes in the development, ownership, and management of life science properties in AAA innovation cluster locations which are primarily located in major markets such as Boston, San Francisco, New York City, San Diego, Seattle, Maryland, and the Research Triangle.

As a percentage of annual rental revenues, Alexandria’s largest market is Boston at 36%, followed by San Francisco and San Diego which make up 23% and 15% respectively.

ARE has a 75.1 million square foot asset base in North America that includes 41.5 million rentable square feet (“RSF”) of operating properties and 33.6 million square feet of properties under construction, in development, or reserved for future development.

At the end of the third quarter, ARE’s North America operating properties had a 93.7% occupancy rate with a weighted average remaining lease term of 7.0 years.

{kind=link}

Quality Score: 99

So what’s so great about Alexandria - why does it deserve a 99 out of 100 on our quality tracker? When analyzing a REIT we look at the business model, growth, yield, and safety. While all of these aspects are critical, the first thing we look at is safety.

By that I mean we first look for a strong balance sheet and low dividend payout ratio before examining earnings growth or yield. One thing you’ll notice is that all of the companies discussed in this article have fortress-like balance sheets and excellent debt metrics.

ARE is no exception with a BBB+ credit rating and exceptional debt metrics including a total debt and preferred stock to gross assets ratio of 27%, a net debt and preferred stock to adjusted EBITDA of 5.4x, and a fixed charge coverage ratio of 4.8x.

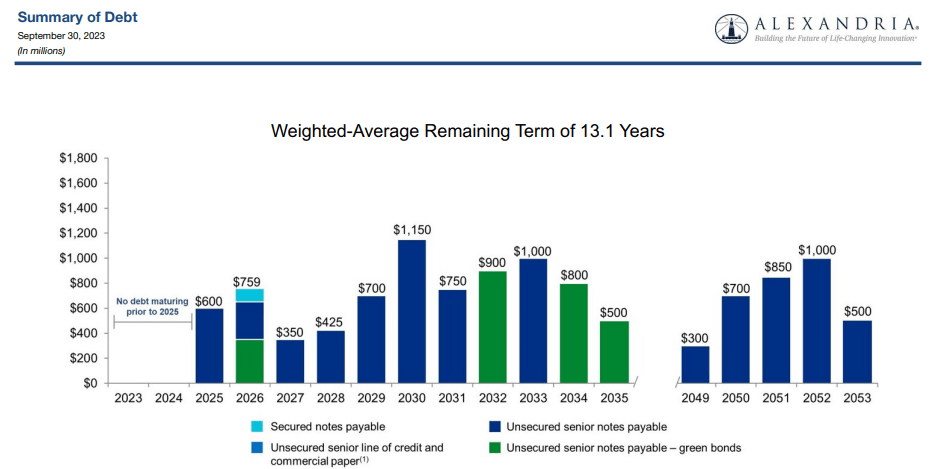

Their debt is a 99% fixed rate with a weighted average interest rate of 3.70% and a weighted average term to maturity of 13.1 years. Additionally, ARE has a ton of dry powder with $5.9 billion in liquidity and no debt maturities prior to 2025.

{kind=link}

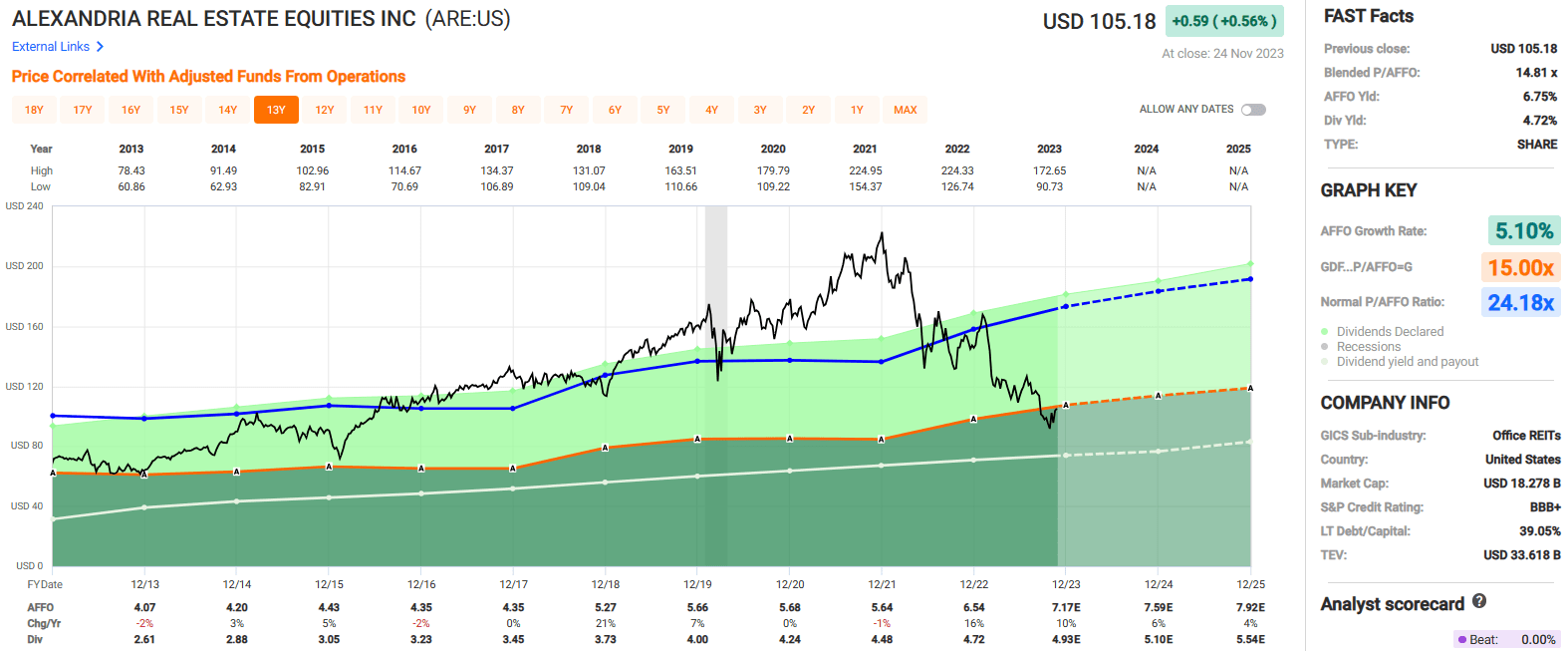

On top of its strong balance sheet , ARE has delivered a blended average adjusted funds from operations (“AFFO”) growth rate of 5.10% over the past decade and analysts expect AFFO per share to increase by 10% in 2023, and then increase by 6% in 2024.

ARE pays a 4.72% dividend yield and has an excellent track record of dividend growth with an average dividend growth rate of 8.62% over the last 10 years.

The dividend is secure with an AFFO payout ratio of 72.17%, and currently, the stock is trading at a significant discount with a P/AFFO of 14.81x, compared to their 10-year average AFFO multiple of 24.18x.

With Alexandria you get one of the strongest balance sheets in the industry, solid AFFO growth, strong dividend growth, a high yield with a low payout ratio, and a discounted valuation.

We rate Alexandria Real Estate a Strong Buy.

{kind=link}

Rexford Industrial Realty, Inc. ( REXR ) - Quality Score: 99

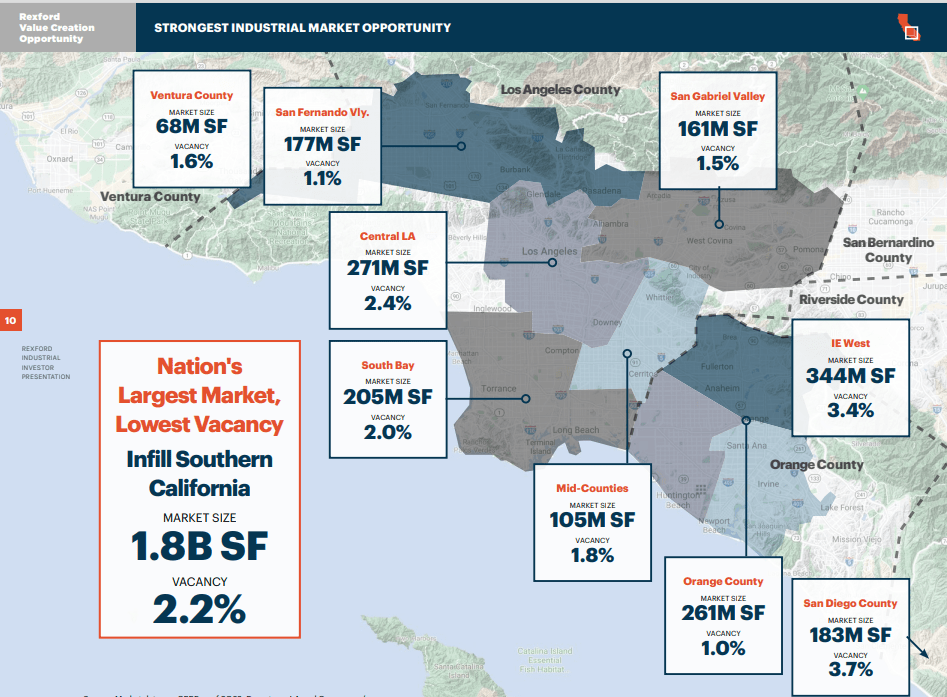

REXR is an industrial REIT with an exclusive focus on industrial properties located throughout infill Southern California (“SoCal”). With its singular focus on the SoCal region, Rexford differentiates its investment strategy from other REITs in the sector that generally have properties spread across multiple states and/or countries.

Rexford’s portfolio is comprised of 371 properties which cover approximately 45.0 million rentable square feet (“RSF”) and have an average occupancy rate of 97.9% as of the end of the third quarter.

REXR operates in 5 major markets within SoCal including Los Angeles, San Diego, Orange, Ventura, and Inland Empire West. Their largest market is Los Angeles which contains 223 industrial properties covering approximately 25 million SF and represents around 55% of their total portfolio’s square footage.

{kind=link}

Quality Score: 99

Rexford Industrial has a quality score of 99 for a variety of reasons. One reason is simply the location of their properties. While REXR is highly geographically concentrated, SoCal is the largest industrial market in the U.S. and the fourth largest market in the world.

Due to natural barriers surrounding the region, SoCal has a scarcity of supply, yet at the same time, the regional economy is larger than many countries with approximately 22 million residents and more than 600,000 businesses.

Due to the consistent supply & demand imbalance, REXR is able to maintain a high portfolio occupancy and achieve outsized releasing spreads, which allows the company to generate strong internal growth.

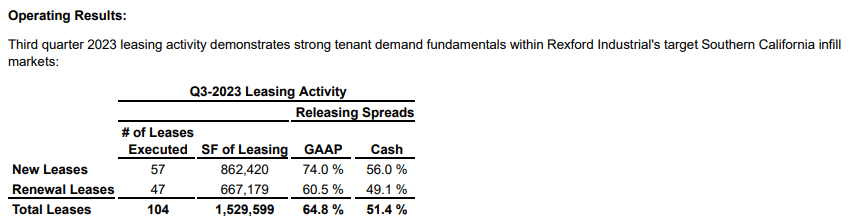

As an example, during the third quarter, REXR’s comparable rental rates for new and renewal leases rose by 64.8% on a GAAP basis and 51.4% on a cash basis when compared to prior rents paid.

{kind=link}

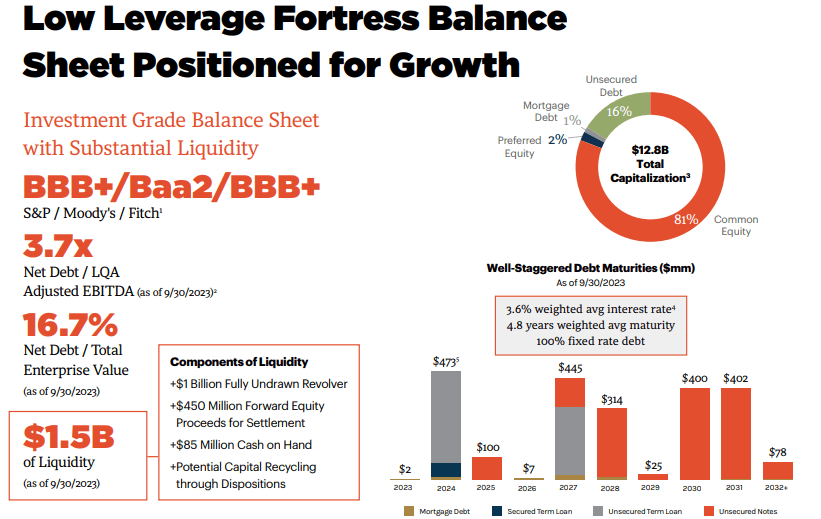

Another reason to love Rexford is its investment-grade balance sheet . The company has a BBB+ credit rating from S&P Global and outstanding debt metrics including a net debt to adjusted EBITDA of 3.7x, a long-term debt to capital ratio of 24.23%, and an EBITDA to interest expense ratio of 7.92x.

Rexford’s debt is 100% fixed rate and has a weighted average interest rate of 3.6% with a weighted average term to maturity of 4.8 years. Additionally, the company has approximately $1.5 billion of liquidity and no significant debt maturities until 2026 including their debt extension options.

{kind=link}

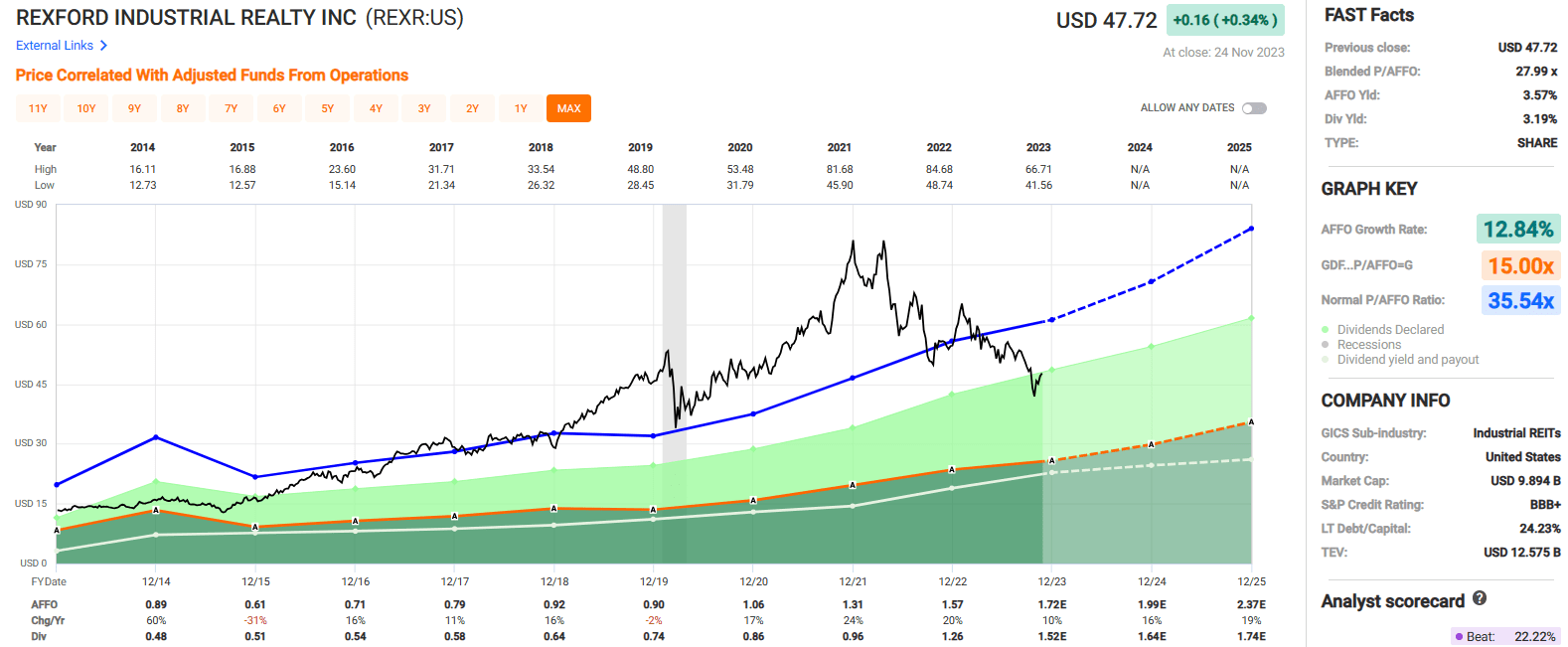

Finally, REXR has a 99-quality score due to earnings and dividend growth the company has delivered over the past decade. Since 2014 REXR has delivered an average AFFO growth rate of 12.84% and analysts expect AFFO growth of 10% in 2023, and then AFFO growth of 16% and 19% in the years 2024 and 2025 respectively.

The company pays a 3.19% dividend yield that is well covered with an AFFO payout ratio of 80.25% and over the past 8 years REXR has had an average dividend growth rate of 13.08%. REXR is currently trading at a P/AFFO of 27.99x, which compares favorably to their average AFFO multiple of 35.54x.

We rate Rexford Industrial Realty a Strong Buy.

{kind=link}

Mid-America Apartment Communities, Inc. ( MAA ) - Quality Score: 99

MAA is a sunbelt-focused multifamily REIT that engages in the development, acquisition, redevelopment, and management of apartment communities located in high-growth regions of the country.

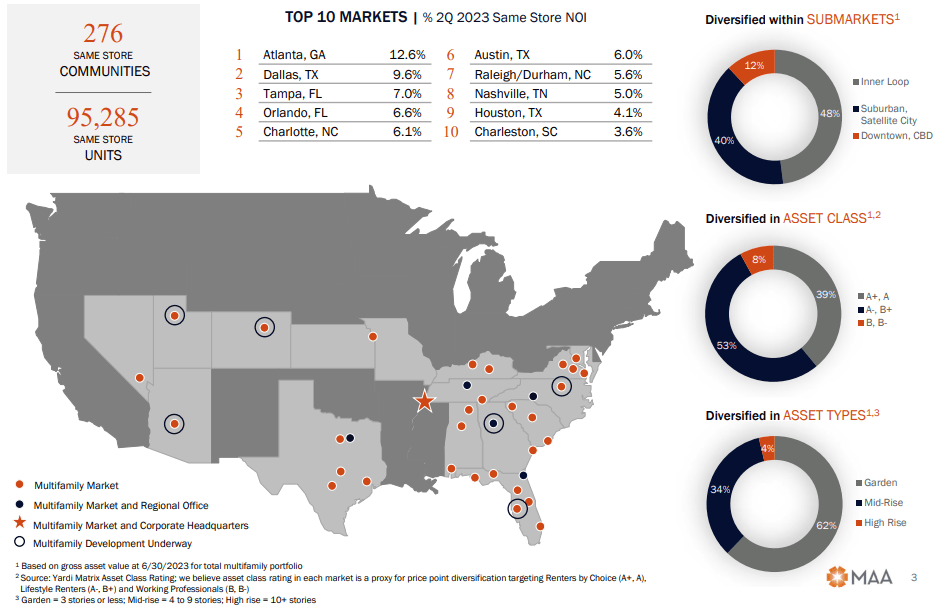

Mid-America’s multifamily communities are located in 16 states & Washington D.C. and contain approximately 101,987 apartment homes with an average physical occupancy of 95.7%. Based on same-store net operating income (“NOI”), MAA’s largest market is Atlanta at 12.6%, followed by Dallas and Tampa at 9.6% and 7.0% respectively.

MAA’s portfolio has a good mix of property types with 53% of their portfolio made up of Class A- or B+ properties, 39% made up of Class A+ or A properties, while the remaining 8% are listed as Class B or B- properties.

At 62%, the majority of MAA’s portfolio consists of Garden Style apartments (3 stories or less), 34% of their portfolio is made up of mid-rise apartments (4 to 9 stories) and only 4% of their portfolio is classified as high-rise apartments.

{kind=link}

Quality Score: 99

Mid-America earns a quality rating of 99 in part due to its sunbelt-driven investment strategy. We really like MAA’s sunbelt exposure as it is very concentrated in the Southeast and Texas, and they have no exposure to residential markets in California.

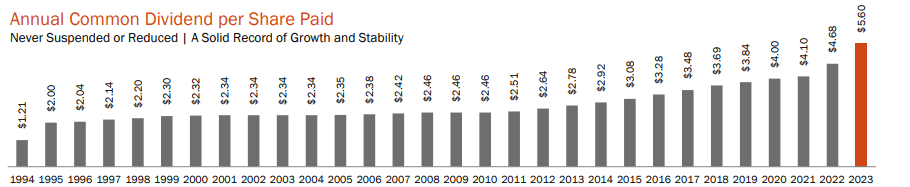

Another thing we really like is MAA’s dividend track record. Since its IPO in 1994, MAA has never reduced or suspended its quarterly dividend and has paid 119 consecutive quarterly dividends over this time period.

{kind=link}

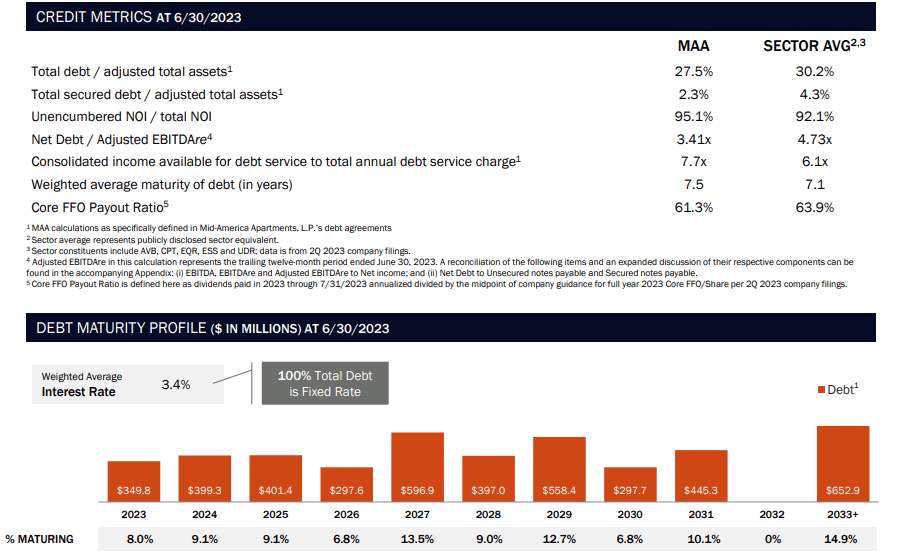

Like the previous companies discussed, MAA has a fortress-like balance sheet and superb debt metrics. They have an A- credit rating from S&P Global that is supported by a total debt to adjusted total assets ratio of 27.5%, a net debt to adjusted EBITDAre of 3.41x, and an EBITDA to interest expense ratio of 8.42x.

Their debt is 100% fixed rate and has a weighted average interest rate of 3.4% with a weighted average term to maturity of 7.5 years.

Additionally, MAA has well laddered debt schedule, full capacity available to them under their $1.25 billion revolving credit facility, and $150 million of cash on hand as of June 30, 2023.

{kind=link}

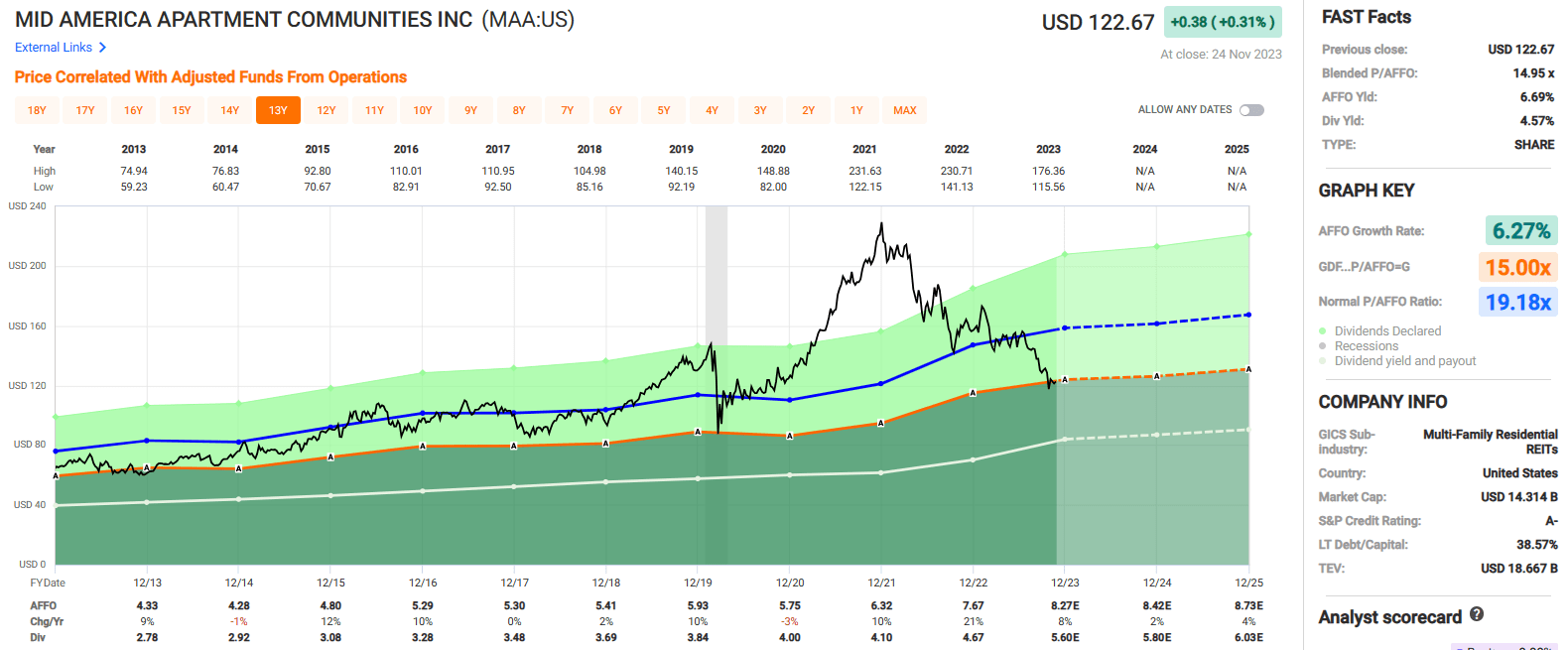

Since 2013 MAA has had an average AFFO growth rate of 6.27% and an average dividend growth rate of 5.92%. The stock pays a 4.57% dividend yield that is very secure with an AFFO payout ratio of just 60.95% and trades at a P/AFFO of 14.95x, compared to their 10-year AFFO multiple of 19.18x.

With MAA you get solid earnings and dividend growth supported by an investment-grade balance sheet and a high yield that is very secure with a conservative dividend payout ratio.

We rate Mid-America Apartments a Strong Buy.

{kind=link}

Prologis, Inc. ( PLD ) - Quality Score: 99

With a market capitalization of over $100 billion, Prologis is not only the largest industrial REIT but is also the largest REIT of any sector. As a point of comparison, the next largest industrial REIT is the previously discussed Rexford Industrial, which has a market cap of approximately $10 billion.

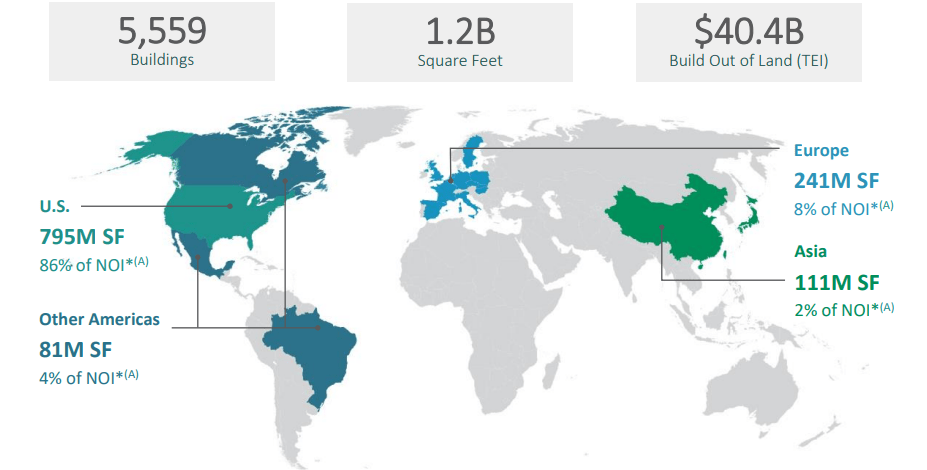

PLD is a behemoth in the industrial space, with a portfolio made up of 5,559 buildings covering 1.2 billion square feet that serve approximately 6,700 tenants across 19 countries on 4 continents.

With $2.7 trillion, or 2.8% of the world's GDP flowing through PLD’s distribution centers, it’s hard to overstate the impact they have on global trade. Prologis has a diversified tenant mix that includes well-established names such as Amazon, BMW, FedEx, UPS, Walmart, 3M, Pepsi, DHL, and Home Depot.

Their largest tenant is Amazon, which made up 5.1% of PLD’s net effective rent in 3Q-23, followed by Home Depot which only made up 1.5% of their net effective rent.

Outside of Amazon, PLD has no significant exposure to any one tenant and only receives 14.6% of their net effective rent from their top 10 tenants combined. At the end of the third quarter, PLD had an average portfolio occupancy of 97.1% with a weighted average remaining lease term of 4.2 years.

{kind=link}

Quality Score: 99

Size and scale matter in real estate and PLD has an abundance of each. The diversity of their revenue stream by tenant, industry, and region improves the visibility of their cash flows which helps their credit ratings and in turn, their cost of capital.

PLD has an investment-grade balance sheet with an A credit rating from S&P Global. As of the end of the third quarter, PLD reported a debt-to-gross real estate assets ratio of 31.0%, a debt-to-adjusted EBITDA of 4.3x, and a fixed charge coverage ratio of 8.1x.

PLD’s debt as a percentage of their total market capitalization was reported at 22.3% with a weighted average interest rate of 2.9% and a weighted average term to maturity of 9.5 years.

Plus, as of their most recent update, PLD had approximately $6.9 billion of liquidity with no material debt maturities until 2026.

PLD - IR

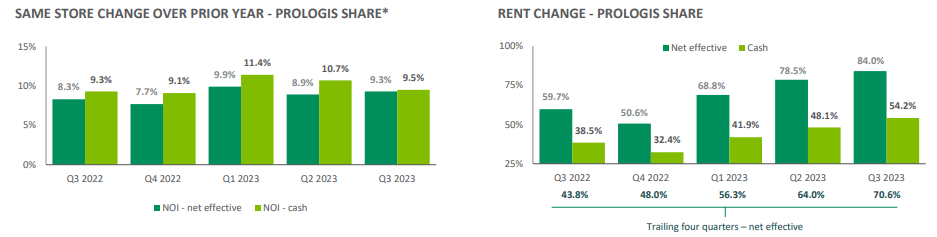

In addition to its fortress-like balance sheet, PLD has delivered considerable growth over the past decade. Much of the recent growth can be attributed to PLD’s releasing spreads and same-store net operating income growth.

In 3Q-23, PLD reported same-store NOI growth of 9.5% on a cash basis and rent change of 54.2% on a cash basis.

Currently, PLD is able to achieve internal growth without any reliance on capital markets by capturing the value embedded in their lease mark-to-market.

{kind=link}

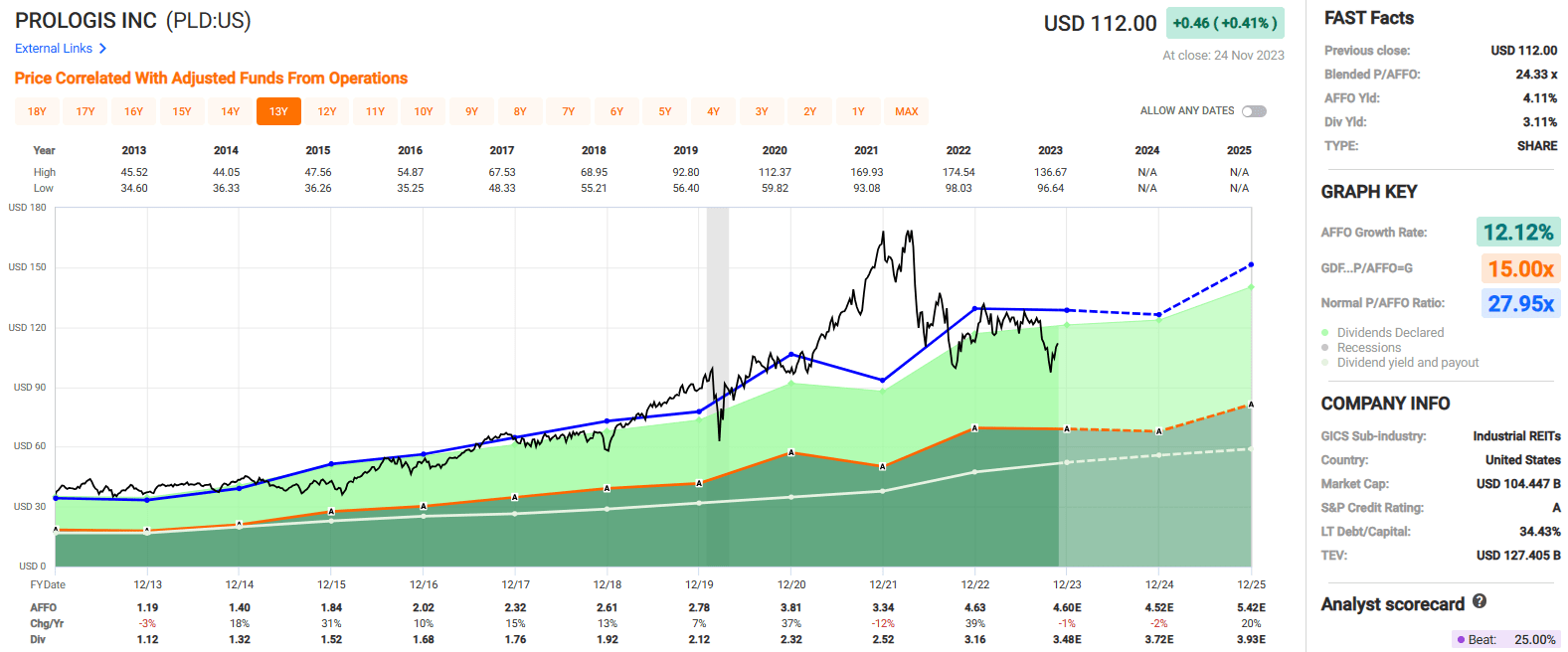

Over the past decade, Prologis has delivered an average AFFO growth rate of 12.12% and an average dividend growth rate of 11.13%.

The stock pays a 3.11% dividend yield that is very secure with an AFFO payout ratio of 68.27% and trades at a P/AFFO of 24.33x, which compares favorably to their 10-year average AFFO multiple of 27.95x.

We rate Prologis a Strong Buy.

{kind=link}

Realty Income Corporation ( O ) - Quality Score: 97

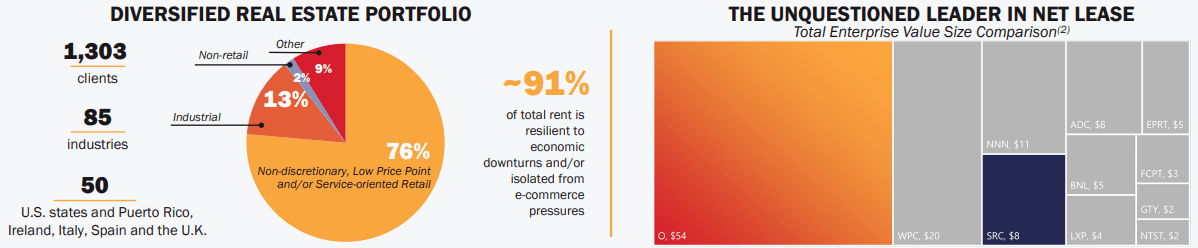

Realty Income, also known as “The Monthly Dividend Company,” is a net lease REIT that invests in single-tenant, free-standing commercial properties that are leased to over 1,300 tenants primarily on a triple-net basis.

Realty Income’s portfolio includes more than 13,250 commercial properties which are located in all 50 states, as well as international properties located in the United Kingdom, Spain, Italy, and Ireland.

Currently, 82.6% of Realty Income’s portfolio consists of retail properties, 13.1% consists of industrial properties and 2.6% consists of gaming properties. The portfolio composition and the total property count will change once the acquisition of Spirit Realty, Inc. ( SRC ) closes, which is expected to occur during the first quarter of 2024.

The SRC acquisition is expected to add approximately 2,064 properties to Realty Income’s portfolio and change the portfolio composition by reducing retail properties to 79.9%, increasing industrial properties to 15.1%, and reducing gaming properties to 2.2% of their total portfolio.

At the end of the third quarter, Realty Income reported a portfolio occupancy of 98.8% and a weighted average remaining lease term of roughly 9.7 years.

{kind=link}

Quality Score: 97

Realty Income has a quality score of 97 on our rating tracker. I know some of you out there think it should be 99, but 97 is still pretty good.

Realty Income has a defensive business model with properties that are insulated from ecommerce and recessions such as grocery and convenience stores.

As a matter of fact, grocery and convenience stores are their 2 largest industries and combined make up approximately 22% of Realty Income’s annual contractual rent.

In addition to having a defensive business model, Realty Income has an investment-grade balance sheet with an A- credit rating and excellent debt metrics including a net debt to pro forma adjusted EBITDAre of 5.2x, a long-term debt to capital ratio of 39.81%, and a fixed charge coverage ratio of 4.5x.

Their debt is 96% unsecured, 93% fixed rate, and has a weighted average term to maturity of 6.6 years.

{kind=link}

While Realty Income has a defensive business model and an impressive balance sheet, I’d say the company’s best feature is its consistency and dependability.

Realty Income has generated positive AFFO per share growth in 26 out of the last 27 years and has delivered a 5% median AFFO growth rate since 1996. It is this consistency that has allowed Realty Income to declare 640 consecutive monthly dividends over its 54-year operating history and increase its dividend for 29 consecutive years.

O - IR

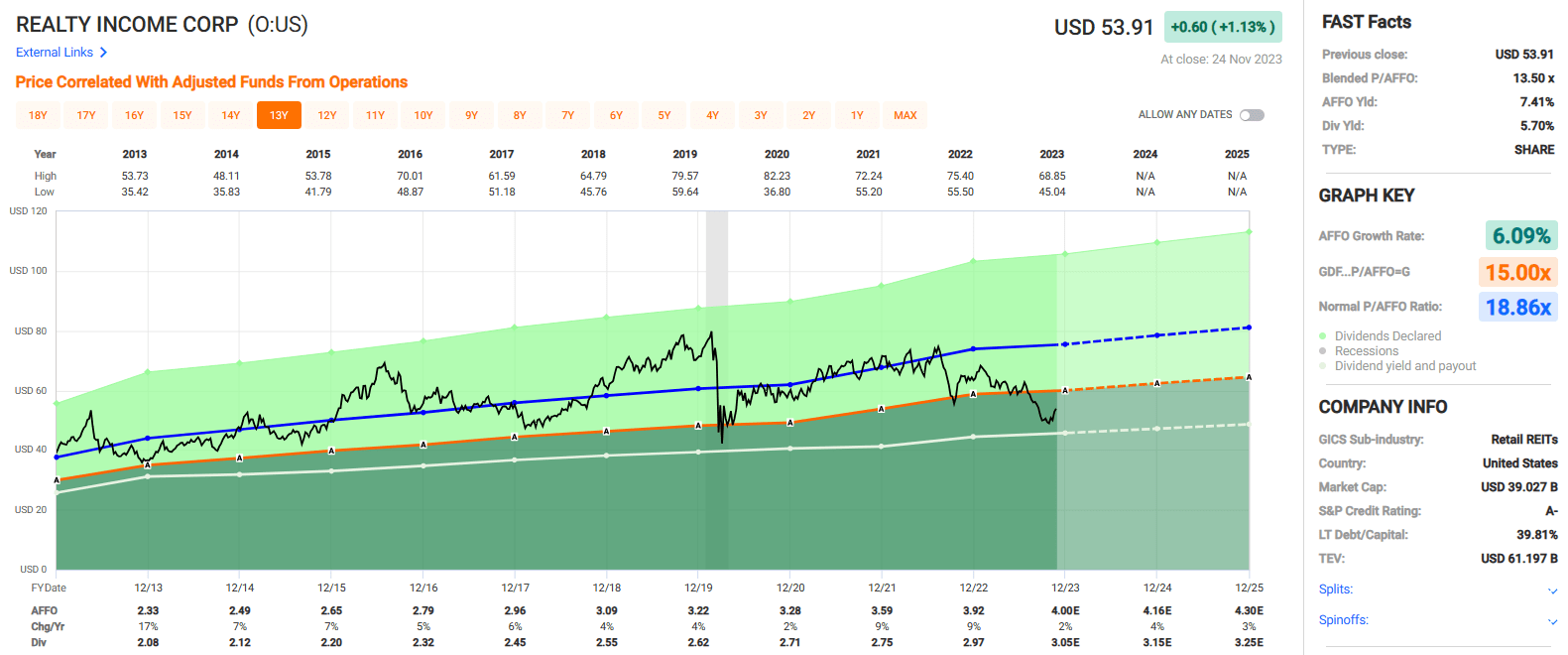

Realty Income is a Dividend Aristocrat that was formed in 1969 and went public in 1994. Over the last decade, Realty Income has delivered an average AFFO growth rate of 6.09% and an average dividend growth rate of 5.76%.

Currently, the stock pays a 5.70% dividend yield that is well covered with an AFFO payout ratio of 75.69% and is trading at a P/AFFO of 13.50x, compared to its 10-year average AFFO multiple of 18.86x.

We rate Realty Income a Buy.

{kind=link}

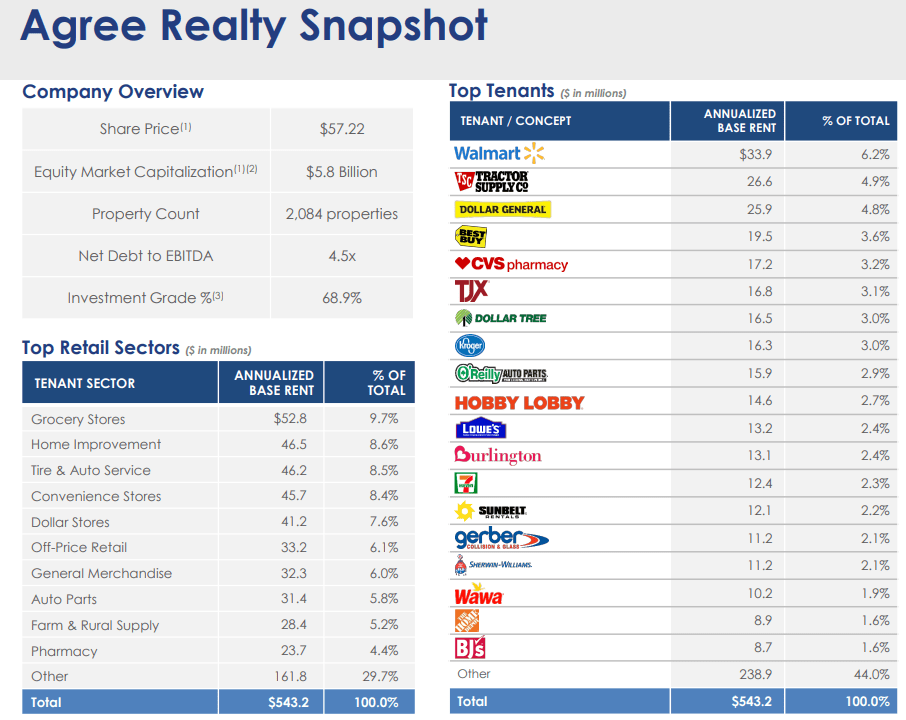

Agree Realty Corporation ( ADC ) - Quality Score: 96

Like Realty Income, Agree Realty is a net-lease REIT that has a high-quality portfolio, a fortress-like balance sheet and pays monthly dividends.

ADC is much smaller with a market cap of just under $6.0 billion (compared to Realty Income’s market cap of ~ $39 billion) and its portfolio is more of a pure-play on retail properties than Realty Income’s, but on the whole, the two net lease REITs have a lot of similarities.

Agree Realty has a defensive business model with tenants that primarily operate in industries that are resilient against e-commerce and recessions. ADC's top retail sectors include grocery stores, home improvement, auto service, and convenience stores while their top tenants include well-known retailers such as Walmart, Tractor Supply, Dollar General, and Kroger.

One thing that really stands out about Agree Realty is the quality of their tenant base as 68.9% of their annual base rent comes from investment-grade tenants.

As of the end of the third quarter, ADC’s portfolio was comprised of 2,084 properties covering roughly 43.2 million SF across 49 states and was 99.7% leased with a weighted average lease term of approximately 8.6 years.

{kind=link}

Quality Score: 96

Agree Realty earns a quality score of 96 due to the quality of their properties and tenants, their defensive business model, the consistency in their earnings, and an outstanding balance sheet.

As previously mentioned, ADC has a high-quality tenant base and receives approximately 69% of its annual base rent from investment-grade tenants. Their business model is defensive in that they target properties used in industries that are insulated from e-commerce and general economic downturns.

ADC’s earnings over the past decade have been very consistent. In each year since 2013, ADC has increased its dividend and delivered positive AFFO growth, even in 2020 during the pandemic.

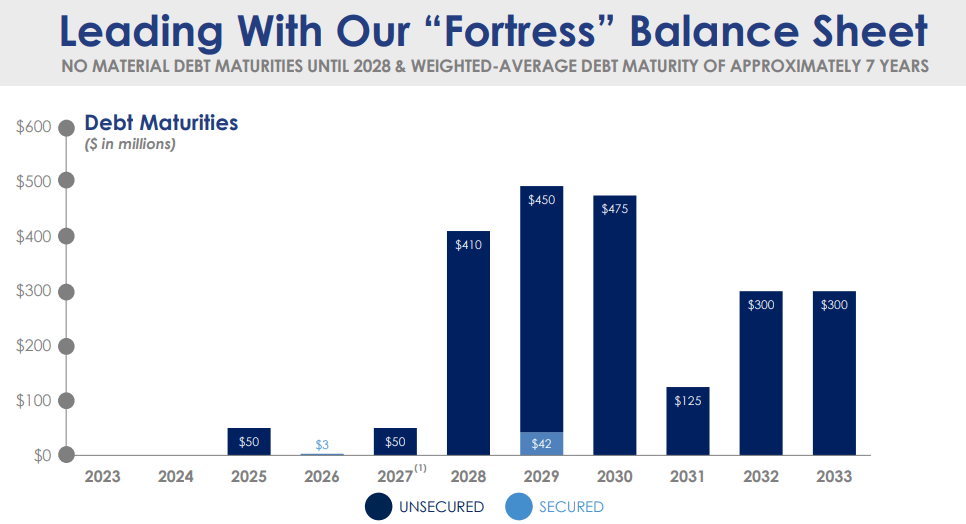

Finally, ADC has an investment-grade balance sheet with a BBB credit rating and excellent debt metrics including a net debt to recurring EBITDA of 4.5x, a long-term debt to capital ratio of 30.42%, and a fixed charge coverage ratio of 5.1x.

Additionally, their debt has a weighted average term to maturity of roughly 7 years, the company has no significant debt maturities until 2028, and as of the end of the third quarter, ADC had total liquidity of $957.4 million.

{kind=link}

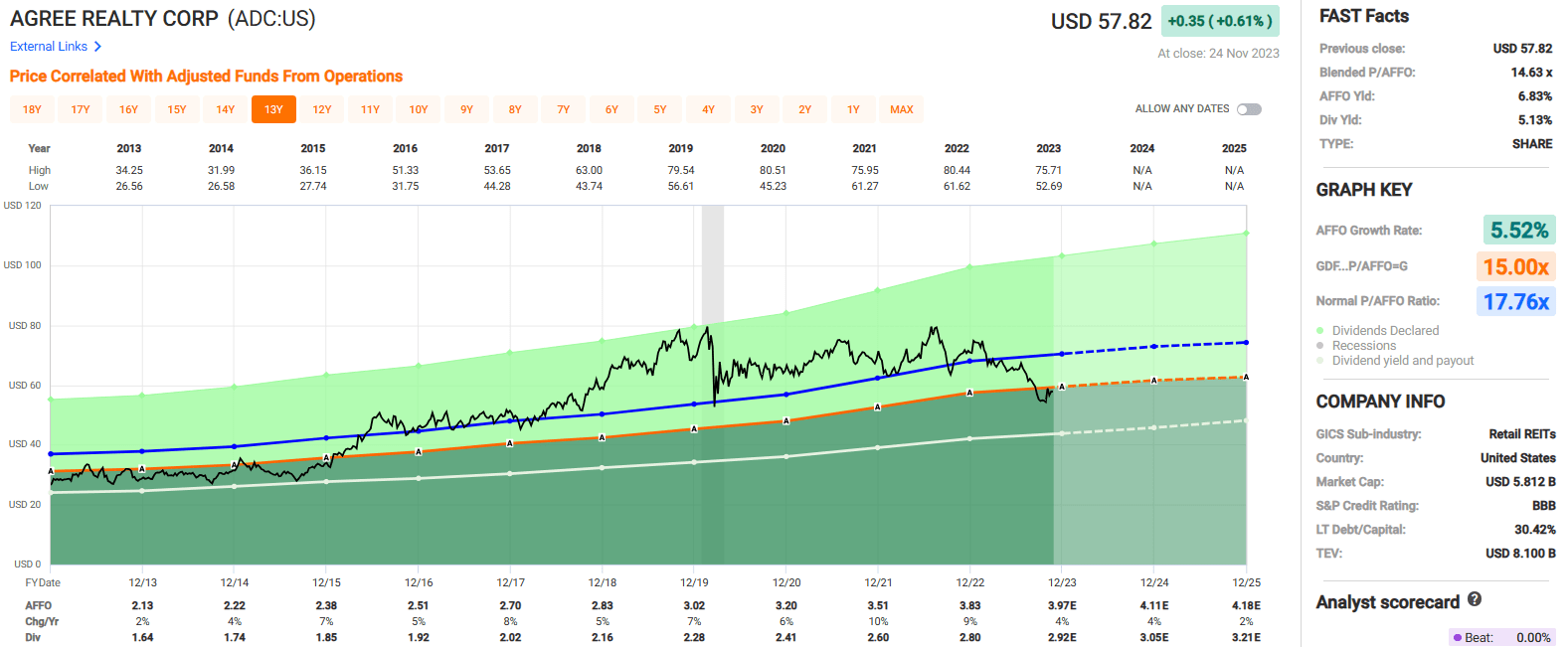

Over the past ten years, ADC has had an average AFFO growth rate of 5.52% and an average dividend growth rate of 5.79%.

Analysts expect moderate AFFO per share growth over the next several years with AFFO projected to increase by 4% in both 2023 and 2024.

The stock pays a 5.13% dividend yield that is well covered with an AFFO payout ratio of 73.24% and currently trades at a P/AFFO of 14.63x, compared to their 10-year average AFFO multiple of 17.76x.

We rate Agree Realty a Buy.

{kind=link}

Happy Holidays!

I hope you enjoyed my holiday-themed article.

As the most-followed writer on Seeking Alpha, you should have known about my passion for REIT investing.

As much as I love REITs, I love diversification more.

Legendary investor Sir John Templeton said,

“The only investors who shouldn’t diversify are those who are right 100% of the time.”

As I explain in REITs For Dummies ,

"I recommend a balanced approach that involves figuring out sector targets based on your own personal risk tolerance. Try buying into different property types, sorting through them based on key demand drivers.

If you really like technology as a larger category, for instance, you can diversify your REIT selections by owning shares of technology-driven REITs: cell towers, data centers and industrials (warehouses).

You can easily spread capital across these categories, providing good diversification while benefiting from the forces of three separate business efforts: 5G, cloud computing and e-commerce."

I wish everyone a safe, healthy, and prosperous holiday season.

Happy SWAN Investing!

For further details see:

Dear Santa: All I Want For Christmas Are A Few Good REITs