SPXT - Debt: When The Chickens Come Home To Roost

2023-08-03 11:46:22 ET

Summary

- Fitch Ratings threw a curveball at investors by downgrading its rating on U.S. federal debt for the first time since 2011 and only the second time ever.

- This triggered the largest one day sell-off in the NASDAQ since February and also saw volatility spike higher.

- If the chickens are finally coming home to roost around the burgeoning U.S. debt and higher interest rates are in cards for corporate balance sheets, the ramifications could be substantial.

Karma : The delusion of the pretentious; who think the Universe should act as their debt collector. ? Steve Maraboli

Investors seem to have been caught somewhat blindsided by an unexpected downgrade of U.S. debt this week. This came courtesy of Fitch Ratings on Tuesday. Among the factors cited for the downgrade were ' expected fiscal deterioration, a growing debt burden, and the erosion of governance related to its peers '. In response, their new rating is AA+ instead of the coveted and longtime AAA rating. It was the only the second time a major credit rating agency has downgraded its outlook on U.S. federal government debt and the first since S&P Global Ratings took the same action in 2011 following a standoff over debt negotiations.

The market responded with a spike in volatility Wednesday within the S&P VIX Index ( VIX ) as well as a decent size selloff across the major indices. The NASDAQ was off better than two percent while the Dow dropped nearly 350 points. This was the biggest daily drop for the NASDAQ since February. Both the S&P 500 and Russell 2000 also declined nearly 1.4% on the day. Bond investors took the downgrade more in stride sending the yield on the 10-Year Treasury up only five basis points to 4.08% on the day.

It is not hard to see the reasons behind Fitch's downgrade. The federal government now has north of $30 trillion with a T in debt. In the first nine months of its current fiscal year, it added nearly $1.4 trillion to that total, or nearly $150 billion a month. Just over $660 billion is projected to be needed to service the debt in FY2023, and that was with a weighted average interest rate of approximately 2.6%. Federal government debt will reach 113% of GDP this fiscal year compared to a still unhealthy 100% prior to the Covid pandemic.

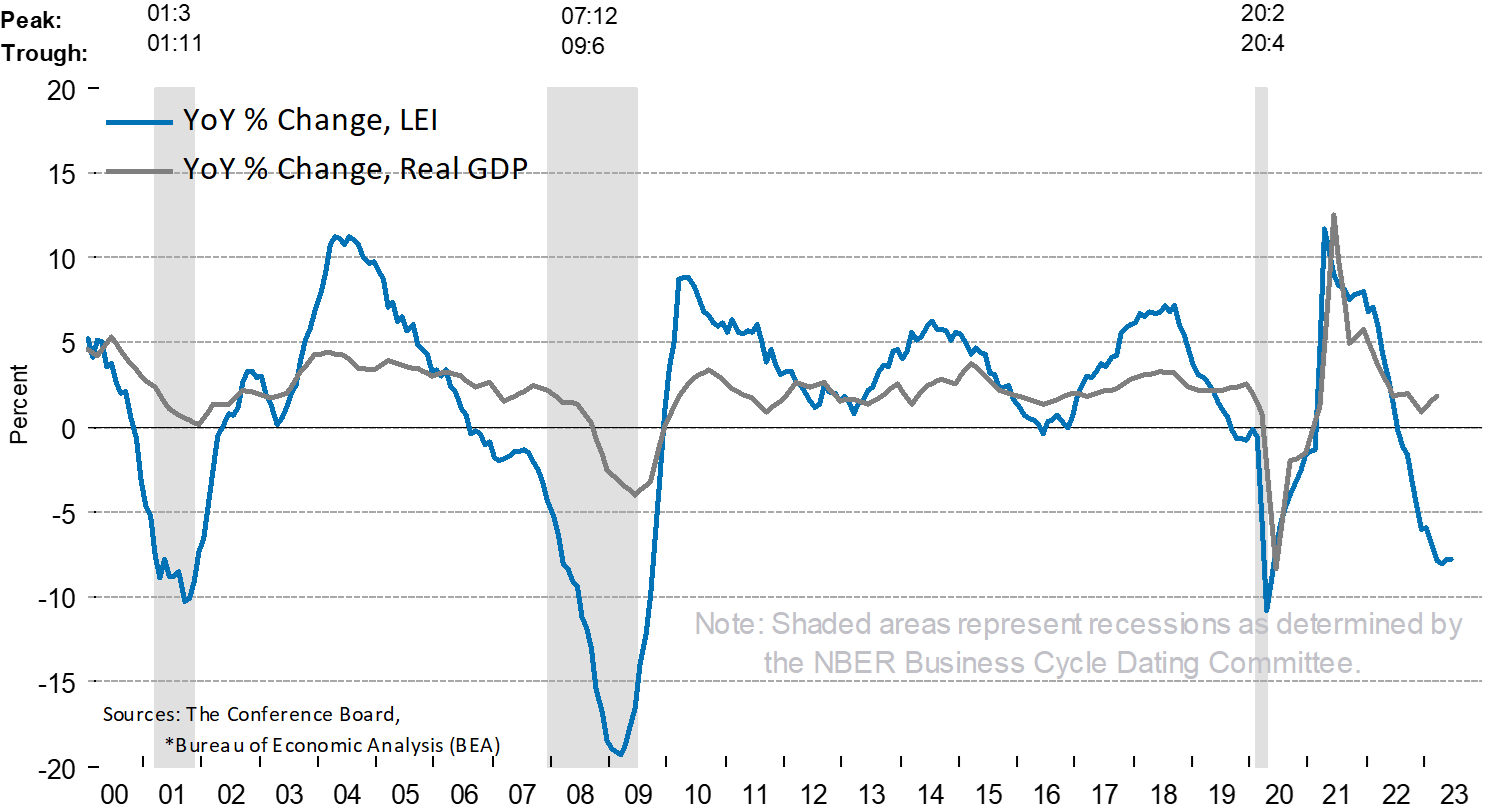

This puts the Federal Reserve between a rock and a hard place. Not squashing inflation completely will keep in place interest rates that will make servicing the nation's debt beyond challenging, if not unserviceable. Keeping interest rates at this level or hiking them further most likely pushes the nation into the recession. While that would lead to higher federal spending on things like unemployment benefits and lower tax revenue, it would reduce interest rates and the cost of servicing the federal debt. I believe the Fed will choose that latter path and trigger an economic contraction, in turn causing the markets to sell off further. Frankly, if one looks at the current hugely inverted yield curve and 15 straight months of declines in the Leading Economic Indicators, I will say a recession is already in the cards.

{kind=link}

However, to avoid what could be a political topic which will dissolve into mostly a discussion on what party is mostly responsible for the nation's current debt load, I want to talk about the ramifications of higher interest rates on the private sector. I feel investors have been underweighting these impacts significantly within their views on equities and the economy.

Investors and corporations were treated to nearly 15 years where the Fed Funds rate was at or near zero. Those days are gone and while interest rates would decrease in a recession, they will still be significantly higher than what the economy has seen over the past decade and a half in my opinion. As I noted in this recent article , property owners have been able to finance various types of commercial real estate generally in a range of four to six percent up until the Federal Reserve started its most aggressive monetary policy since the early 80s. Now loans on these same properties are generally running in the eight to 12% range.

{kind=link}

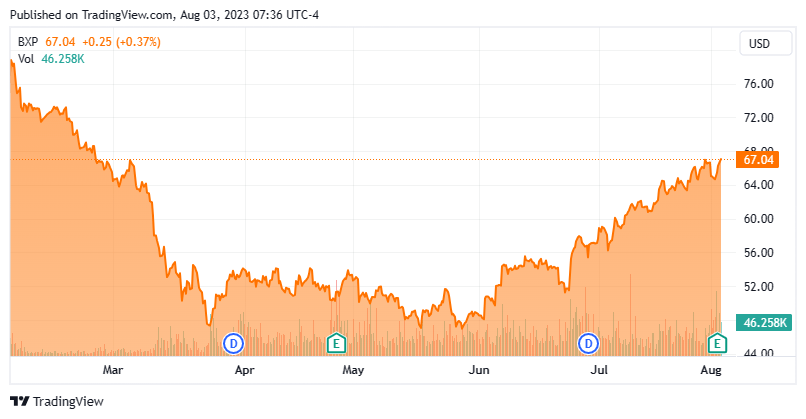

As these debt rolls over, interest expense to cover those obligations is going to become much more onerous. Let's take Boston Properties, Inc. ( BXP ) whose shares have rebounded nicely in recent months. This large REIT owns and manages a portfolio of approximately 190 properties that are concentrated in six gateway markets that includes Boston, San Francisco, Washington D.C., Los Angeles, New York, and Seattle. Most of these properties are office buildings.

About 35% of the company's exposure is in Boston but it has approximately 45% exposure to troubled San Francisco and New York City combined. As Brad Thomas points out in a recent article , the company is well run, and its properties are just over 90% leased. What caught my eye, however, is the company has nearly $15 billion in total debt and ' with a weighted average term to maturity of five years and a weighted average interest rate of 3.81% '.

What happens if interest rates stay elevated for an extended time and Boston's debt eventually has a weighted average interest rate closer to 7%? That is an approximate $450 million boost to annual interest expense for a REIT that had just less than $300 million of Funds from Operations or FFO and just over $100 million in net income in the second quarter .

I am not picking on Boston Properties, I could easily do this type of quick analysis on myriad REITs or for any company that has a good slug of debt on its balance sheet that needs to be refinanced in the coming years. If treasury yields continue to go up and volatility moves higher, I could easily see BXP test its lows from a few months ago when the U.S. experienced its second, third and fourth largest bank failures in its history.

Approximately 40% of my portfolio is allocated to covered calls positions. Most of these are around companies with pristine balance sheets, not surprisingly. Let's highlight one of these as an example. That would be Exelixis ( EXEL ) . This midcap oncology concern has an approximate market cap of $6.5 billion. The company is nicely profitable and is seeing revenue growth in the low to mid-teens. The company just beat top and bottom-line expectations with is second quarter earnings report . More importantly, the company ended the quarter with approximately $2.1 billion in net cash and marketable securities on its balance sheet. And this was after buying back $127 million worth of its own stock during the quarter. Talk about a ' fortress ' balance sheet!

Approximately 50% of my portfolio is in 3-month and 6-month treasury bills. They pay nearly 5.5%, significantly above the 10-Year treasury yield and this is a great use of cash right now. I also have no desire to loan Uncle Sam money for a decade at this point. Well-known billionaire fund manager Bill Ackman just announced a new short position against 30-Year Treasuries it should be noted.

Completing my portfolio allocation as the chickens seem coming home to roost around the massive debt that has been run up on the nation's credit card, 6% to 8% of my portfolio is in the cash and the rest is in out of the money bear put spreads against the Invesco QQQ Trust ETF ( QQQ ) and SPDR® S&P 500 ETF Trust ( SPY ) , as well as some of the names in the overvalued Magnificent Seven . One of these trades is around Tesla, Inc. ( TSLA ) which I highlighted in this recent article .

It is not the sexiest portfolio allocation admittedly. However, as the NASDAQ was having its worst day in nearly six months yesterday, my portfolio was down less than 0.01% on the day. About as close to breakeven as one can get.

We have become a society of indulgent consumers resulting in rapidly increasing debt both personally and as a nation . ? L G Durand

For further details see:

Debt: When The Chickens Come Home To Roost