VNORP - Debunking The Mystery Behind REIT Preferreds

2023-08-02 07:00:00 ET

Summary

- During this Fed tightening cycle, preferred stocks have declined significantly below par value which is normally $25.

- Buying preferred stocks at below par can represent an excellent total return opportunity as the current dividend yield is high relative to treasuries and other bonds.

- Also, there's the potential for price appreciation if the securities return to par.

The legendary investor Benjamin Graham was not a fan of preferred shares as he said,

"…really good preferred stocks can and do exist, but they are good in spite of their investment form, which in an inherent bad one."

Graham's dislike for preferred shares is warranted as explained,

"The typical preferred shareholder is dependent for his safety on the ability and desire of the company to pay dividends on its common stock."

Preferreds are somewhat of hybrid classification as Graham explained,

"…the preferred stock carries no share in the company's profits beyond the fixed dividend rate. Thus, the preferred holder lacks both the legal claim of the bondholder (or creditor) and the profit possibilities of a common shareholder (or partner)."

I like preferreds, especially right now, and that's why our team is providing more picks within this mysterious slice of the capital stack.

During this Fed tightening cycle, preferred stocks have declined significantly below par value which is normally $25.

Buying preferred stocks at below par can represent an excellent total return opportunity as the current dividend yield is high relative to treasuries and other bonds, and there is the potential for price appreciation if the securities return to par.

It can be a good idea to use active management (like an ETF) when deciding how to select fixed income securities as managers can seek diversification and address the issues unique to fixed income securities that are not as relevant to equity common stocks.

Preferred stock can offer attractive investment opportunities in this market which is why a well-positioned portfolio is recommended. Especially now, in a high interest rate environment where exposure to the commercial real estate market is undervalued.

Preferred Stocks Vs. High Yield Bonds

Both preferred stocks and high yield bonds have experienced a decline in value during the Federal Reserve's tightening cycle.

However, it's worth noting that preferred stocks have underperformed high yield bonds and are currently presenting an appealing relative valuation.

Since Dec. 31, 2021, the S&P Preferred Stock Total Return Index (SPPREF) has underperformed 7.80% when compared to the Bloomberg U.S. Corporate High Yield Index (JNK).

Moreover, preferred stocks with equivalent credit ratings are trading at an average premium of 1.20% above high yield bonds (refer to the table below).

Preferred stocks generally exhibit attractive credit characteristics as most preferred stock issuers are publicly traded companies committed to upholding their credit ratings. These companies tend to employ strategies such as issuing equity, selling assets, or reducing common dividends to maintain their credit quality.

iREIT®

Portfolio Positioning

An additional advantage of preferred stocks, compared to high yield bonds, is that many preferred stocks transition from fixed rates to floating rates after a period of five years .

In today's interest rate environment, with the yield curve inverted, this can provide a large immediate increase in income upon the conversion.

After conversion, the increases/decreases will be more modest as the Fed adjusts the Fed Funds rate.

As an example of the magnitude of the initial bump, SCE Preferred H ( SCE.PH ) converts from a fixed coupon of 5.75% to 3-month LIBOR + 2.99%. At 3-month LIBOR as of 4/10/2023, this equates to a current yield moving from 6.90% to 9.80%, or a more than a 40% increase to its dividend.

Historical Track Record

Reviewing performance, active preferred stock funds have performed notably well over the past five years despite the difficult macroeconomic environment backdrop of low interest rates, COVID-19, and rapidly rising rates, and regional banking stress.

Opportunity within REIT Preferreds

When evaluating public investments involving real estate, we believe that you should conduct a thorough assessment of both the REIT's quality and the underlying assets.

Additionally, we carefully consider the optimal position within the capital stack for investment, as many REITs offer common equity and preferred equity investment options.

Given uncertainties in commercial real estate, particularly in specific subsegments, some investors may understandably exhibit hesitancy towards common equity investment.

However, this hesitancy has spread to preferred equity as well, with certain REIT preferreds experiencing unwarranted selloffs . This presents an opportunity akin to throwing the baby out with the bathwater.

When assessing the REIT's quality, it is crucial to discern between a REIT's corporate-level debt and asset-level debt. In doing so, you can avoid potential pitfalls.

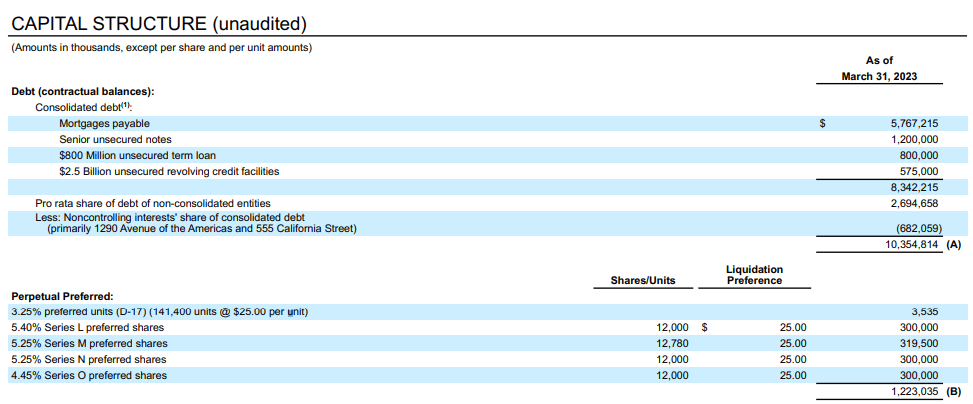

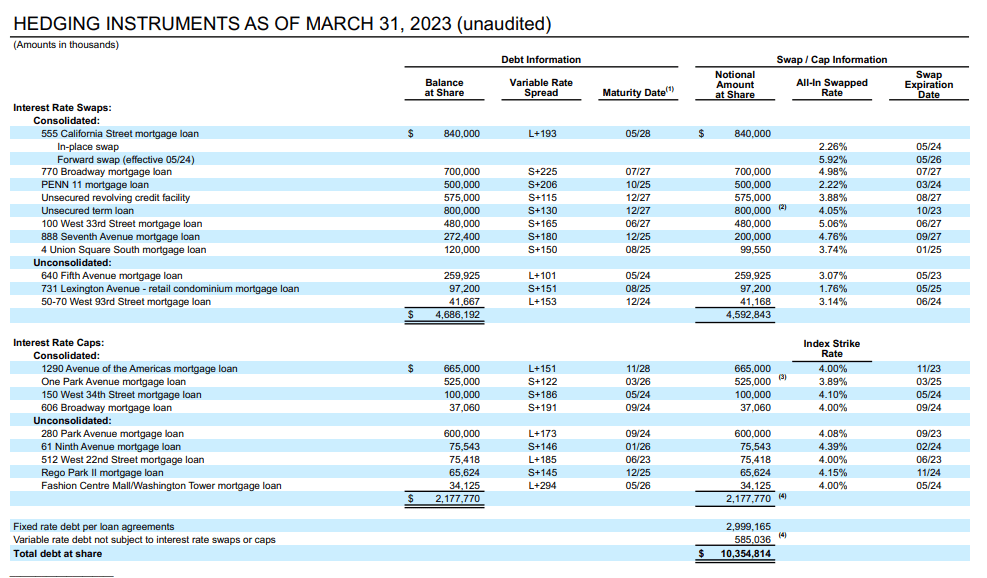

For instance, upon analyzing Vornado's (VNO) real estate portfolio, which encompasses $10.3 billion of debt and $1.2 billion of preferred stock, we find $5.7 billion in mortgage debt secured by underlying buildings.

While headline risks associated with the value decline commercial real estate may be true, we view a diversified REIT's ability to strategically divest from distressed assets and debt associated with them as a positive move. Walking away from a distressed property and its attached debt load benefits preferreds:

{kind=link}

{kind=link}

Vornado's Series M (VNO.PM) shares trade at $15.04 per share and pay a $1.31 per share dividend which translates to a 8.9% yield . The shares are cumulative which means that that even if the company cuts the dividend, it must be paid in the future (unless BK).

Many income-oriented investors have questions on preferred shares. As I explain, REITs "have some of the best legal contracts - known as covenants - in the investment-grade debt space. They do a bang-up job reporting on them too."

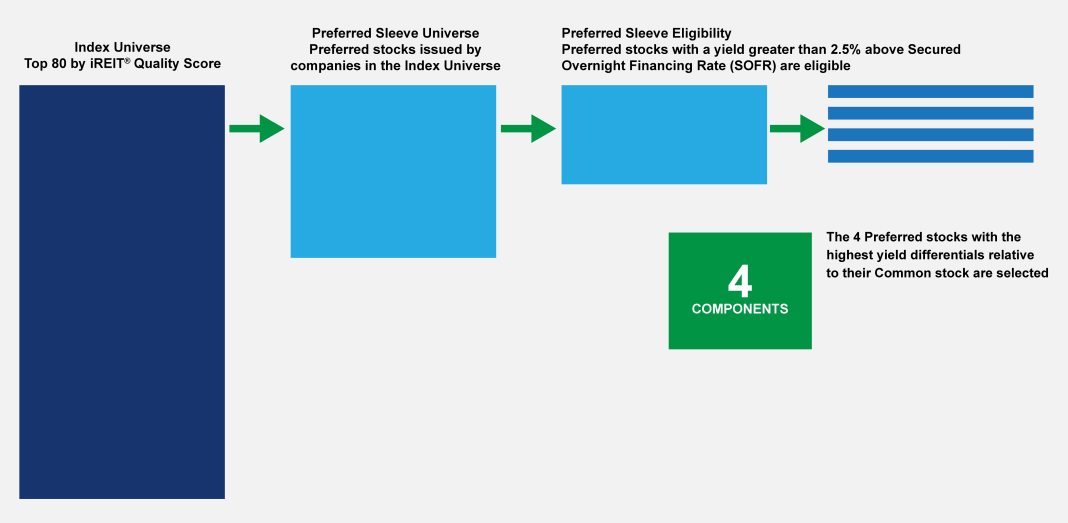

I also decided to sprinkle in REIT preferreds in a new REIT ETF Index. This is how the REIT Index selects the preferred shares in the portfolio:

iREIT®-MarketVector™ Quality REIT Index

{kind=link}

Another way to play preferreds is to consider these two "pure play" preferred ETFs, InfraCap REIT Preferred ETF ( PFFR ) and the iShares Preferred and Income Securities ETF (PFF). Seeking Alpha writer, Juan de la Hoz did a good job breaking down these two ETFs .

I interviewed Jay Hatfield, CEO and fund manager of Infrastructure Capital, a few months ago and he said:

"But just a couple more facts as to why preferreds are great... we think great investments, is that the default rate is very, very low for publicly traded preferreds. We're talking $25, so ones that you can buy directly as well. It's only 0.33% over the last 30 years.

Investment-grade bonds are about 0.1, but high-yield bonds are 3.5. We tend to traffic in more what we call crossover preferreds. The bonds are often investment grade and the preferreds are BB.

But the reason we like that, these are public companies, they're not controlled by like Blackstone ( BX ) or somebody like that. You're not trying to suck cash out of them. Public boards, public CEOs running public companies, they care about their credit. If there is a problem like during the pandemic, and we saw this, they'll issue equity. They'll cut their common dividend but not their preferred, and keep paying."

I agree with Jay and that's the reason I maintain around 10% of my REIT portfolio in preferreds and we also include the preferreds in the REIT ETF Index.

As always, thank you for reading and commenting.

Note: Brad Thomas is a Wall Street writer, which means he's not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: Written and distributed only to assist in research while providing a forum for second-level thinking.

For further details see:

Debunking The Mystery Behind REIT Preferreds