COGT - Deciphera Pharmaceuticals: Encouraging Sales Growth For Qinlock But Risk/Reward Remains Unattractive

Summary

- Shares have lost three quarters of their value over the past three years but logged a 60% gain in the past 12 months.

- Qinlock sales are steadily growing in 4th line GIST with potential to see off-label use in earlier lines of therapy given favorable tolerability profile.

- Vismeltinib in TGCT has produced promising data to date but would be competing against generic imatinib which could be quite difficult.

- While broad combination strategy for ULK1/2 inhibitor DCC-3116 is interesting, it has shown no monotherapy activity in phase 1.

- I cannot recommend purchase of DCPH, as risk/reward profile does not look attractive at this time.

Shares of oncology kinase-inhibitor specialist Deciphera Pharmaceuticals (DCPH) have lost three quarters of their value over the past three years. However, during the past 12 months they've risen by over 60%.

Aside from technical stability over the past couple quarters, I also was drawn to this name due to a strong Q3 report (product revenue up 49% with Qinlock sales accelerating) and clinical momentum (especially ULK1/2 inhibitor DCC-3116 moving into multiple combination cohorts including with MEK and KRASG12C).

Let's dig deeper to determine if this one could merit entry in our Core Biotech (commercial-stage) portfolio.

Chart

{kind=link}

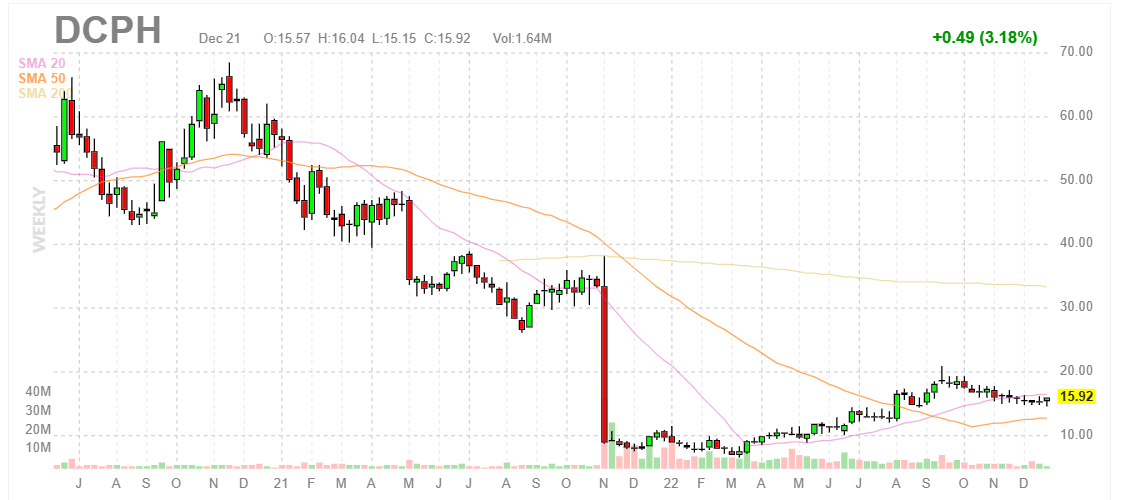

Figure 1: DCPH weekly chart

When looking at charts, clarity often comes from taking a look at distinct time frames in order to determine important technical levels and get a feel for what's going on. In the weekly chart above, we can see shares peaking above $60 back in late 2020 and from there steadily trending downward to $30 in late 2021. From there, gap down below $10 was a result of Qinlock failing its phase 3 study in late-stage GIST (was intended to expand label to 2nd line setting and put the drug on path to blockbuster status). Gradual rebound to current range (around the $15 level) appears merited given recent progress both commercially in GIST as well as in the clinic for vismeltinib.

Overview

Founded in with headquarters in 2003 (280 employees), Deciphera Pharmaceuticals currently sports an enterprise value of ~$800M and Q3 cash position of $371M providing them operational runway for ~1.5 years.

There are currently ~67.4M shares outstanding and last round of dilution took place in April with $163M raised in secondary offering. Keep in mind this offering included pre-funded warrants to purchase 9.7M shares.

At JMP Fireside Hematology & Oncology Summit Fireside Chat , President and CEO Steven Hoerter notes that the company was founded based on their deep insights into kinase biology and the entire portfolio is comprised of medicines that have come out of their own research engine. Qinlock is approved and they are advancing several first and potentially best-in-class candidates in the clinic.

{kind=link}

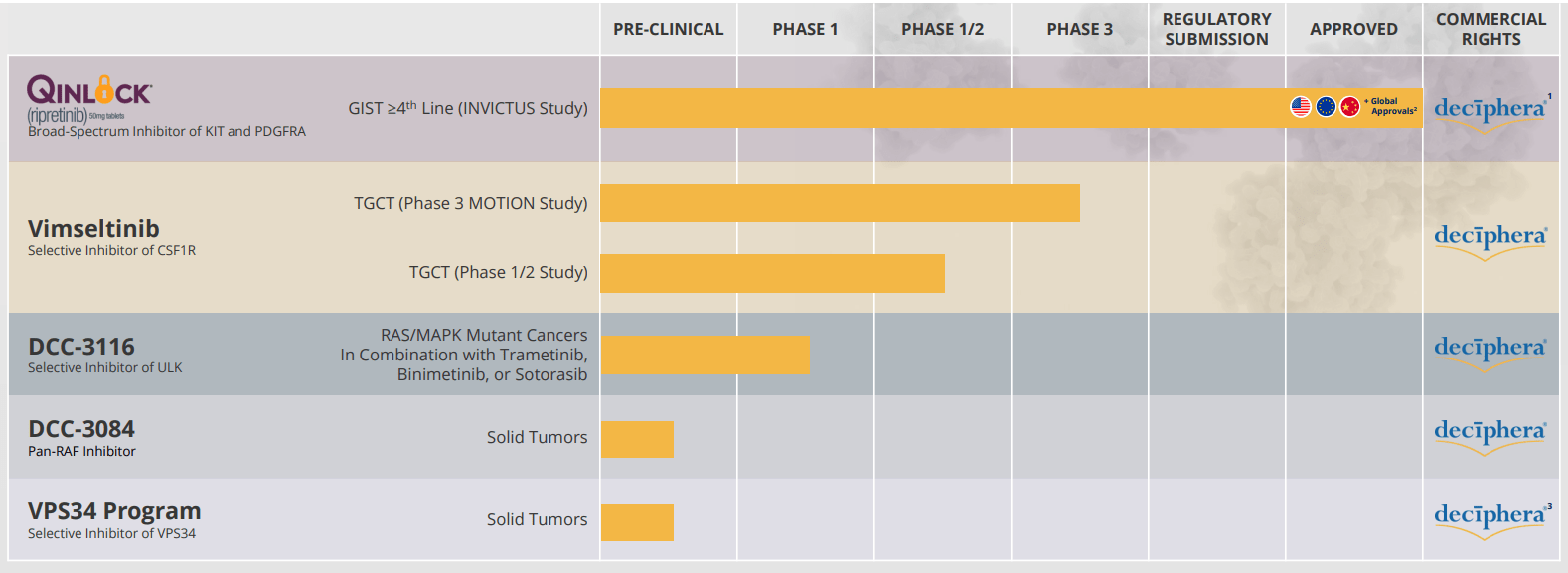

Figure 2: Pipeline

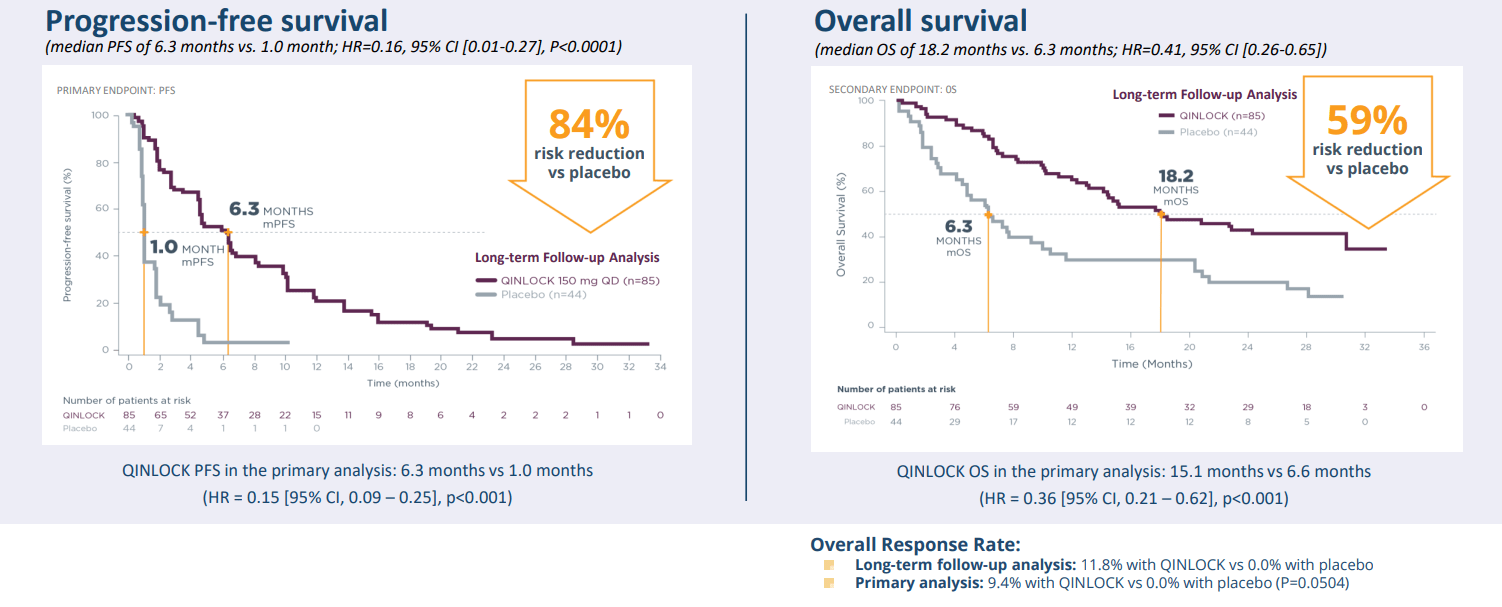

Qinlock was approved a couple years ago in the US for 4th line GIST and is now approved in eight other jurisdictions around the world. Focus in 2022 has been on geographic expansion including gaining EU approval. Qinlock sales continue to exceed analysts' low expectations and the majority of 4th line GIST patients are receiving the opportunity to be treated with Qinlock. Modest growth in the US comes from the topline (unit growth and price growth over time are the two key contributors and expected to continue). Management expects to continue to eke out share gains and I appreciate how they keep our expectations grounded with conservative phrasing such as "limited growth." Phase 3 INVICTUS study showed they tripled overall survival in this 4th line patient population and again there was high unmet need in this setting before Qinlock was approved.

{kind=link}

Figure 3: Clear standard of care for 4th line GIST

In the US they have 30 reps in the commercial organization (field sales team and related personnel). They received approval in Europe at the end of last year and launch sequence here is different due to pricing and reimbursement processes. They launched in Germany first, are generating revenue in France and from there are looking to open up access in Italy, Spain, UK, etc. Over the next 18 to 24 months these additional markets will achieve improved price and reimbursement. In EU they have 25 people today and are looking to add to headcount only as needed. the drug has been licensed to Zai Lab ( ZLAB ) in China where they are responsible for commercialization.

{kind=link}

Figure 4: Qinlock total product revenue showing decent growth year over year

For CSF1R inhibitor vismeltinib they reported updated data at ESMO a couple months ago. Vismeltinib showed promising POC data in TGCT (Tenosynovial Giant Cell Tumor) in terms of durability and response rate. For the latter, ORR was 69% across all phase 1cohorts, 53% in phase 2 cohort A and 46% in phase 2 cohort B. Management believes data shows best-in-class potential and notes there's only one approved treatment for these patients (pexidartinib with black box warning and REMS for potentially fatal hepatotoxicity).

{kind=link}

Figure 5: Best-in-class profile in TGCT for vimseltinib

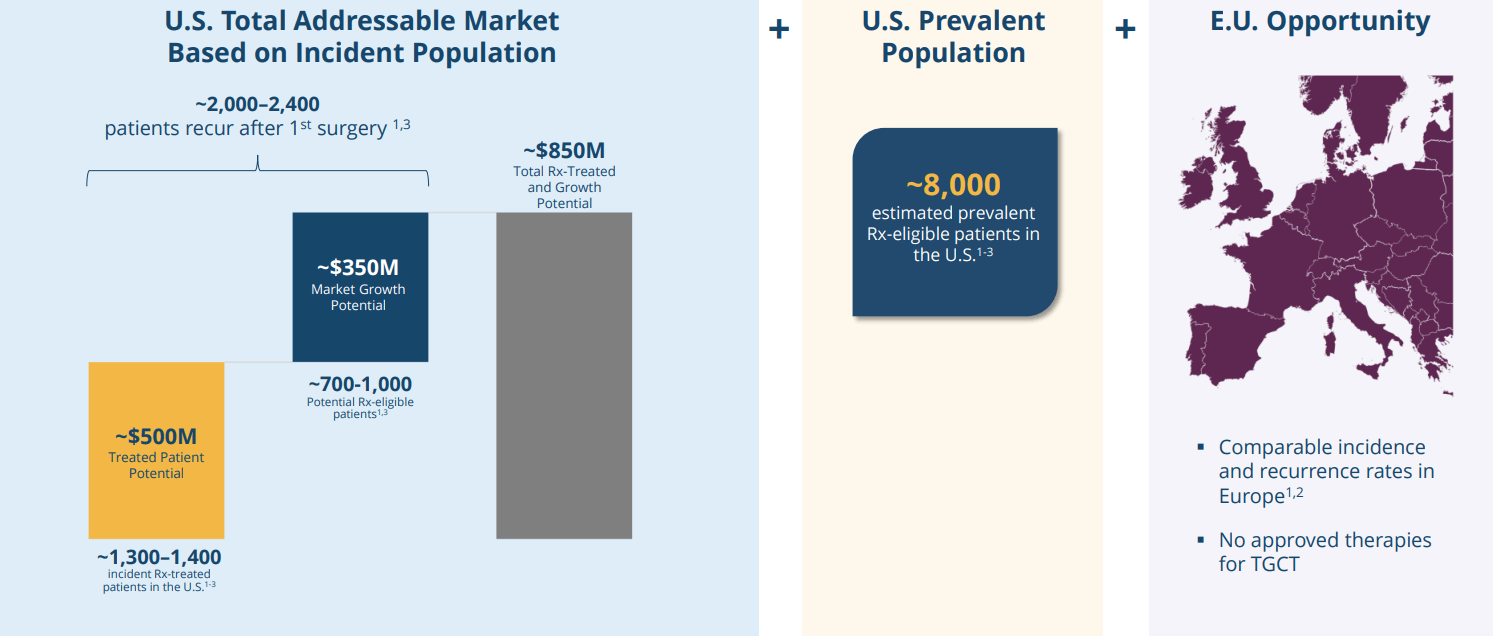

There are no approved treatments in Europe. These patients have normal life span, but these tumors cause significant morbidity (pain and mobility issues). Expected label for vismeltinib, if approved, would be for patients who are not amenable for surgery. Robust analysis of medical claims in the US shows 1,300 to 1,400 new patients each year who receive systemic treatment. Out of that group, 70% of them are receiving off-label imatinib and this represents the floor of the opportunity. They also know there are 700 to 1,000 patients each year in the US who relapse after their first surgery who could be eligible for systemic treatment. None of this accounts for a prevalent pool of patients getting suboptimal treatment who could be eligible for systemic treatment.

{kind=link}

Figure 6: TGCT global opportunity

The company intends to provide an enrollment update very shortly and are very pleased with pace of enrollment so far, which is reflective of unmet medical need here. Prior in phase 1 study they enrolled 40 patients over just 6 months. Primary endpoint of study is response rate at 6 months, so add 6 months from last patient in and a couple months for data cleaning and analysis before topline results are reported. Vismeltinib is likely to be their second approved drug and there is 30% overlap between prescriber base (doctors who treat with Qinlock and also treat TGCT).

As for ULK1/2 inhibitor DCC-3116, they reported initial phase 1 data also at ESMO showing the drug candidate was well-tolerated, PK was dose-dependent and solid target engagement across all dose levels tested. Safety profile so far has been quite good with majority of adverse events being Grade 1 or 2 in nature (except for asymptomatic Grade 3 ALT increases, which were reversible). Maximum tolerated dose was not reached either.

As ULK is an initiating factor for autophagy, the idea is to selectively inhibit it in RTK, RAS and RAF-mutant cancers. Preclinical data provides a rationale for combination with RTK inhibition (think osimertinib and afatinib), for KRAS G12C inhibition (sotorasib and adagrasib) and with MEK inhibition (trametinib). While these mutations being targeted account for 70% of human cancers, as we all know it's quite a leap from mice to replicating such promise in humans for these potential combinations.

{kind=link}

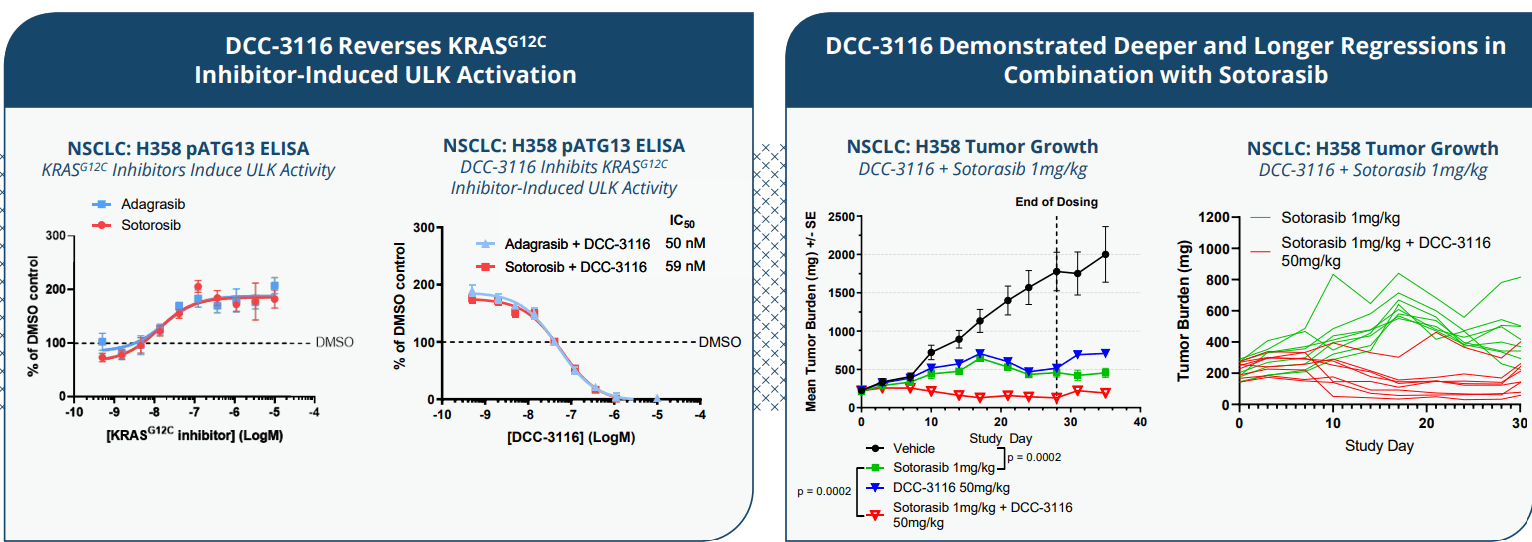

Figure 7: DCC-3116 inhibits RAS pathway inhibitor-induced ULK activity and shows deeper tumor regressions with sotorasib combo

I thought the regressions in combination with KRAS G12C especially looked quite good (not merely incremental as other potential combination partners' slides show, see slide 18 of ESMO slides ). Currently the company seeks to find recommended phase 2 dose for each combination, from there moving into expansion arms that could represent efficient pathways to market. For trametinib combo, these include 2nd line PDAC (KRAS-driven), 3rd to 5th line NSCLC (RAF/RAS driven) and 3rd line+ CRC (RAF/RAS-driven). For sotorasib combination, they will look at 2nd to 4th line NSCLC (KRAS G12C driven). For binimetinib combo, the idea is to first explore 2nd to 3rd line melanoma (NRAS-driven).

On a more skeptical note, they did not see signs of single agent activity (not that it was expected). It will be interesting to see if combinations live up to the promise of preclinical data ( see full slides here ), but again I maintain a skeptical eye until I see the results given lack of monotherapy activity.

Lastly, this year the company unveiled its potential best-in-class RAF inhibitor DCC-3084. BRAF Class I, II and III as well as fusion represent areas of monotherapy focus (unlike their ULK1/2 inhibitor). Also, there could be an opportunity for combinations in patients with RAS mutations.

Select Recent Developments

On June 16 the company announced the appointment of Kelley Dealhoy as Senior Vice President and Chief Business Officer (served prior as VP US Business Development for Novartis' Pharmaceutical Division).

On Aug. 10 Deciphera announced that the Journal of Clinical Oncology had published results from its INTRIGUE phase 3 study (n=453) of Qinlock in GIST patients previously treated with imatinib. While statistically significant improvement in PFS was not observed compared to sunitinib, Qinlock did show meaningful clinical activity with fewer Grade 3/4 treatment-emergent adverse events and improved tolerability. Specifically, patients in the Qinlock arm reported less deterioration in role functioning and better outcomes on several other key patient-reported outcome measures of tolerability compared to sunitinib. Digging deeper, patients with KIT exon 11 primary mutation demonstrated numerically better mPFS at 8.3 months vs. seven months for sunitinib arm (Hazard Ratio of 0.88). However, in the intention-to-treat population mPFS was eight months compared to 8.3 months for sunitinib. In both analysis ORR was nominally better as well (23.9% vs 14.6% for the former, 21.7% vs. 17.6% for the latter). Of note, patients on sunitinib were three times more likely to develop Grade 3 hypertension and seven times more likely to develop Grade 3 palmar-plantar erythrodysesthesia. Likewise, fewer patients on ripretinib experienced deterioriation in their abilities to work or engage in leisure activities during treatment (also less impact on lives due to skin toxicity).

In September Deciphera announced updated results from the ongoing phase 1/2 study of vimseltinib for the treatment of patients with TGCT not amenable to safety. In addition to response rates, duration of benefit and favorable tolerability profile touched on above, management also highlighted preliminary patient-reported outcome results which found clinically meaningful symptomatic benefit at week 25 compared to baseline for both pain and stiffness.

Other Information

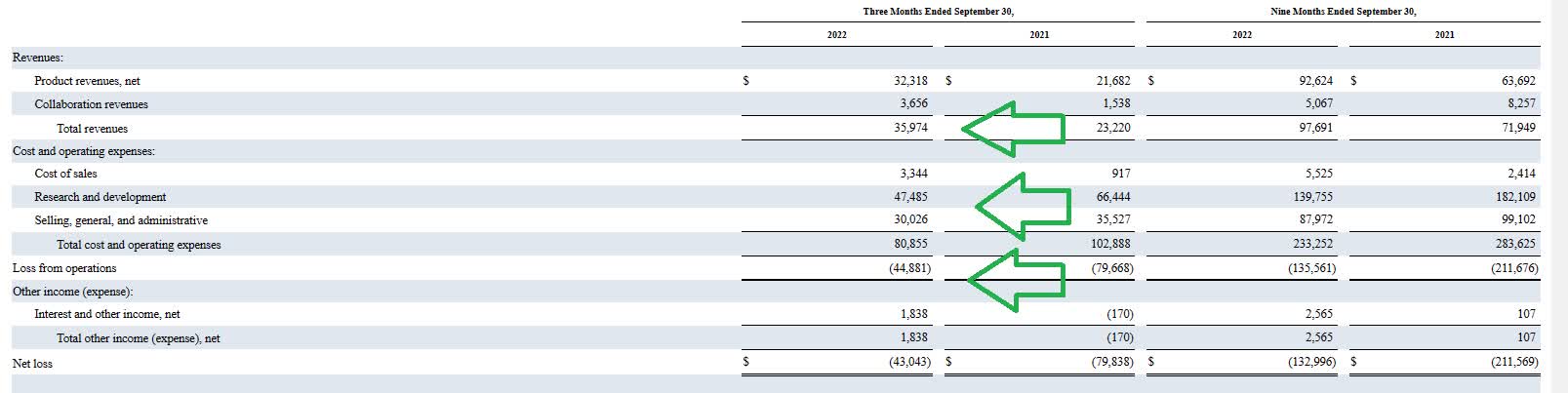

For the third quarter of 2022 , the company reported cash and equivalents of $371M (down ~$22M from prior quarter). Net loss was nearly cut in half to $43M, while SG&A fell by 14% to $30M. Research and development expenses decreased by over 25% to $47.5M. Management guided for runway into 2025 at current burn rate. Prior financing took place at $10/share in April (good sign that share price has risen by 60% since then). Accumulated deficit of $1.187 billion would raise alarm bells for me normally, BUT as noted below I see revenues rising and expenses falling over time.

{kind=link}

Figure 8: Quarterly numbers going in a good direction as revenues increase and expenses fall

Qinlock net product revenue rose 49% to $32.3M with total revenue coming in at $36M. The company also announced that the Journal of Clinical Oncology published results from the INTRIGUE study, and there exists a growing hope of off-label use in certain instances versus sunitinib in earlier lines of therapy given improved tolerability profile.

As for the conference call , management highlights the promising start for DCC-3116 as initial exposure increased in a dose proportional manner and demonstrated target inhibition at all dose levels tested. They extended the 100 milligram to 300 milligram BID dose cohorts with additional patients to further characterize drug profile and after enrolling 10 more patients, still did not reach maximum tolerated dose (thus chose 50 mg BID as starting dose level for combination cohorts). There are two combination cohorts with MEK inhibitors, one with trametinib, another with binimetinib as well as one cohort with sotorasib and improved KRAS G12C inhibitor. The strategy here is to combine DCC-3116 with a broad range of partner drugs across multiple mechanisms of action to be able to treat a large number of cancer patients.

As for institutional investors of note , Redmile Group has been adding to its position and owns 8.10% stake. Deerfield has been doing the same and owns a 9.5% stake. Armistice Capital's position looks unchanged at a 5.9% stake. Brightstar Associates added to its stake and owns over 18M shares!

As for leadership, I consider it a significant green flag the management team and board of directors appears stacked with highly experienced pharmaceutical veterans. President and CEO Steven Hoerter served prior as Chief Commercial Officer at Agios Pharmaceuticals. Chief Scientific Officer Daniel Flynn is actually founded the company in 2003 (I'm a fan of founder-led firms, assuming they continue to execute across all areas of the business). Others in leadership team hail from Alnylam Pharmaceuticals, Tesaro, Acceleron, ImmunoGen, GSK and Novartis, to name a few. Board of Directors includes former heads of Pfizer and Array Biopharma (bought out by Pfizer for $11.4B).

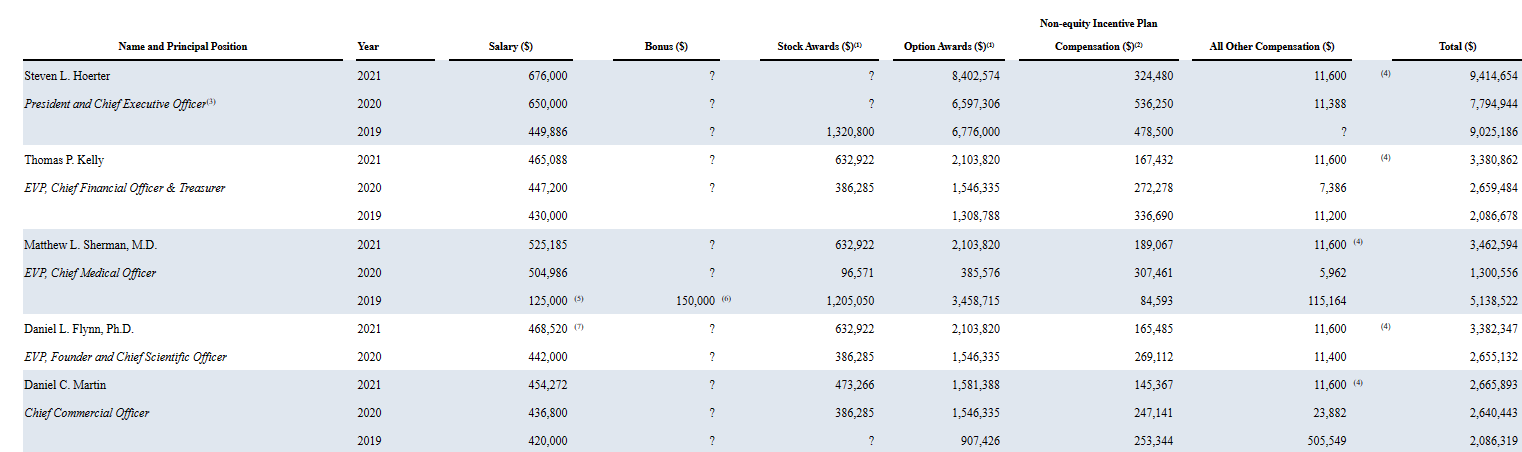

Moving on to executive compensation, cash portion of salaries appears reasonable for a company of this size with a solid balance sheet. Level of option awards is on the high side, especially for CEO at over $8.4M (otherwise reasonable for the rest of leadership team).

{kind=link}

Figure 9: Executive compensation table

As for IP, Qinlock has five issued US patents covering composition of matter, method of use and drug product claims (expirations between 2030 and 2040). Additional foreign patents expire in the same timeframe and four pending US provisional applications could extend expiration to 2042. For vimseltinib, they own two issued US patents expiring covering composition of matter and method of use claims (expirations between 2034 and 2040). Additional pending applications are expected to expire between 2034 and 2039. For DCC-3116, three pending US applications cover composition of matter and methods of use claims (expected to expire in 2040).

As for other useful nuggets from the 10-K filing (you should always scan these in your due diligence as many companies like to sweep undesirable elements under the rug), in terms of competition the company reminds us that current standard of care for GIST is 1st line imatinib, 2nd line sunitinib (upon imatinib progression), regorafenib for 3rd line followed by Qinlock after the patient has received prior treatment for 3 or more kinase inhibitors. Cogent Biosciences' ( COGT ) is going after 2nd line GIST in the PEAK phase 3 portion (bezuclastinib sunitinib combination) and if data there is impressive as I expect, it could limit Qinlock's off-label use in earlier lines of therapy. Other big pharmaceutical companies developing treatments for GIST include Novartis (NVS), Pfizer (PFE) and Bayer to name a few. For vimseltinib in TGCT, they could face competition from other companies developing antibodies or small molecules targeting CSF1R including Abbisko Therapeutics, AmMax, Daiichi, SynOx and HutchMed. As for DCC-3116, Endeavor Biomedicines and Erasca are also advancing treatment programs targeting ULK.

Playing devil's advocate, I don't think vimseltinib in TGCT will be given much credit until it proves itself with commercial sales growth (has promising efficacy and especially tolerability profile but will be competing against generic imatinib which could be quite difficult). Also, while DCC-3116 is targeting KRAS and related cancers in a unique manner, there were few signs of monotherapy activity so burden of proof rests on combination cohorts. Initial data showed O% response rate with 29% disease control rate (about as unexciting as it can get).

Final Thoughts

To conclude, with enterprise value of $800M here, I think that the company is fairly valued for its current prospects in GIST (slow, steady growth) and future opportunity in TGCT (again, a big ask to compete against generic imatinib). What makes the story more interesting for me is the combination cohorts for ULK1/2 inhibitor DCC-3116 with KRAS G12C, MEK and RTK inhibition. Preclinical data shows deep, durable remissions in a variety of well-established cancer models and revaluation substantially higher would be merited if this gets repeated in human trials.

For readers who are interested in the story and have done their due diligence, I cannot recommend DCPH at this time as the risk/reward does not seem favorable at current levels.

Valuation would be more attractive if shares pull back below the 200-day moving average in the low teens. Likewise, the story would be worth revisiting if DCC-3116 combo cohorts show signs of efficacy. It remains to be seen if they can tease out a signal of early activity in dose-escalation or have to wait until indication-specific expansion cohorts in 2024.

As for risks involved, the company has two to three years of cash but I would not be surprised to see further dilution (secondary offering) in 2H 23 to be on the safe side. Disappointing phase 3 readout for vimseltinib (unlikely but possible) would weigh on share price, as would lack of efficacy for DCC-3116 combination cohorts. Competition from big pharmaceutical companies and other peers is a key concern, including off-label imatinib in TGCT, up and coming treatments for GIST such as bezuclastinib from Cogent Biosciences (limiting off-label uptake for Qinlock in earlier lines of therapy) and many other aspiring partners (novel targets being tried out) in the KRAS and RAS space. Lack of monotherapy activity for DCC-3116, while arguably expected, still adds another layer of risk going into the combination cohorts.

Author's Note: I greatly appreciate you taking the time to read my work and hope you found it useful. While I post research on many companies that interest me, in ROTY (clinical stage) and Core Biotech (commercial stage) portfolios I own just 15 or fewer names in order to focus on stories that are highest conviction for me.

For further details see:

Deciphera Pharmaceuticals: Encouraging Sales Growth For Qinlock But Risk/Reward Remains Unattractive