DCPH - Deciphera Pharmaceuticals Pipeline Is Underwhelming

2023-10-26 10:29:06 ET

Summary

- Our estimates show that Qinlock 2L KIT exon 11+17/18 mutation indication sales guidance is unlikely to be achieved due to fractional incidence.

- Deciphera Pharmaceuticals is expecting a Phase III MOTION trial topline readout this quarter, which is unlikely to be impressive.

- We believe that DCC-3116 and autophagy, in general, might prove to be an ineffective treatment choice in MAPK mutation tumors.

- We predict further dilution in at latest 2024, due to limited cash runway and expanding operations.

Editor's note: Seeking Alpha is proud to welcome AR Capital Menagement as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Summary

The self-proclaimed 'biotech visionaries' seem optimistic about Deciphera Pharmaceuticals' (DCPH) immediate prospects, anticipating a series of significant catalysts. However, at ARCM, our in-depth analysis of the upcoming readouts and the value of currently marketed drugs suggests a more tempered outlook. In our opinion, the new Qinlock sales guidance, especially considering the incidence of exon 11+17/18 mutation, is bordering on the ambitious side. The anticipated topline data for their investigational CSF1R inhibitor might not meet expectations and lead to increased selling pressure. Their ULK inhibitor, which targets autophagy, has shown limited anti-tumor effects in monotherapy, though it does have a favorable safety profile. The role of autophagy in tumors, as presented in existing literature, is varied and not fully understood, leading to widespread skepticism. Previous clinical trials with autophagy inhibitors, particularly in combination therapies for CRC/NSCLC/PDAC, have often been inconclusive. For those reasons, we anticipate that the upcoming Phase I trial results will show only moderate efficacy. We expect Deciphera to maintain its operations until the end of 2024. Consequently, in our opinion, a potential dilution of up to 200M shares, as highlighted in their Q2 2023 earnings, is likely due to an Open Market Sale Agreement. In light of these insights, ARCM predicts notable selling pressure on DCPH stock in the near future.

Introduction

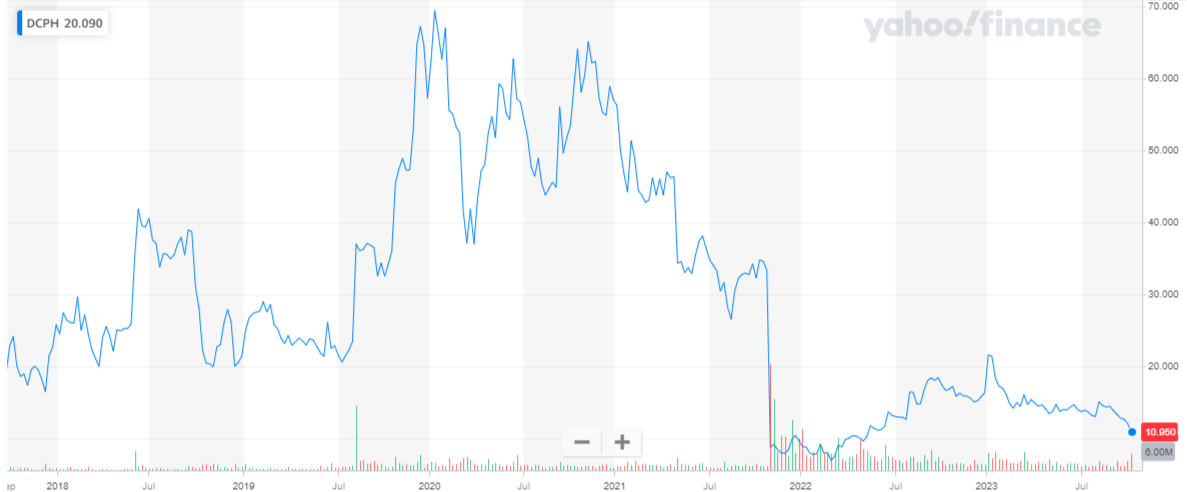

Deciphera Pharmaceuticals, trading under the ticker DCPH, operates as a commercial-stage biotech entity, primarily targeting the small molecule oncology sector. Established in 2003 by Dr. Daniel L. Flynn (who stepped down on August 1st, 2023) DCPH transitioned to a publicly traded entity in March 2017. From its initial IPO priced at $20 per share, the company's value has since seen a decline, with shares currently trading in the low teens.

{kind=link}

Figure 1 - Deciphera Stock Chart ( Yahoo.com )

Despite the drop in value, DCPH maintains a robust market capitalization nearing ~$1B. With a singular approved product in their portfolio, the company's pipeline remains integral for its future.

In this analysis, we have chosen to share our perspective on DCPH's imminent trajectory. Our primary focus centers on Qinlock, the forthcoming topline readout from the MOTION trial, and the insights from the ULK inhibitor studies. Specifically, our assessment suggests that the sales projections for Qinlock may be leaning toward the optimistic side. Additionally, any surprises from the MOTION trial data are likely to be less than favorable, and we anticipate that the clinical significance of the ULK inhibitor will be minimal.

Pipeline

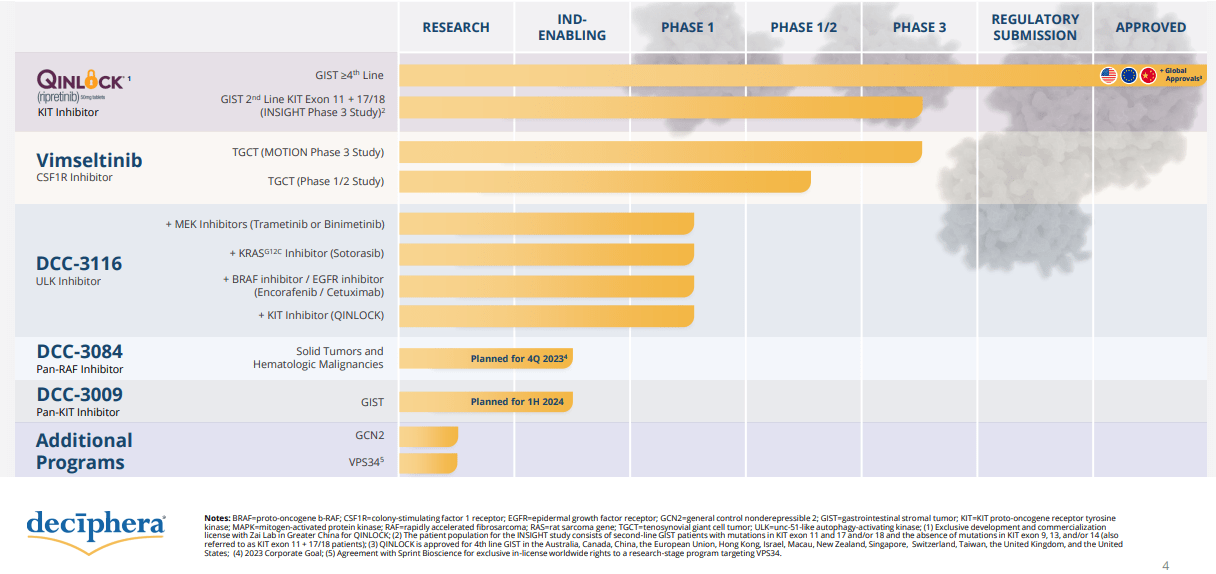

Deciphera holds a portfolio of patents centered around small molecules designed to inhibit kinases that promote cellular proliferation and survival. Notably, their primary targets include the KIT and PDGFRA mediated signaling, inhibited by Qinlock (also known as Ripretinib), and the CSF1R mediated signaling, inhibited by Vimseltinib. Beyond their focus on proliferative pathways, Deciphera is also investigating the role that autophagy plays in tumor inhibition. DCC-3116, an ULK protein kinase inhibitor, is currently in the initial stages of human testing.

Deciphera 2023 October Presentation

{kind=link}

Figure 2 - Deciphera Pipeline (2023 October Presentation)

Deciphera highlighted three compounds, DCC-3084, DCC-3009, and DCPH-9149, that may potentially enter clinical trials. These compounds function as inhibitors and activators within kinase pathways. However, this analysis will not delve into the specifics of these compounds, given that they are still several years away from reaching advanced stages of development.

Qinlock

Following Qinlock's approval and launch in 2020, it significantly boosted Deciphera's sales, reaching $134M in 2022. Qinlock, often touted as a "success," faced a slight setback when the company's stock experienced a 70% dip in 2021. The crash was due to data readouts that did not quite favor Ripretinib as a second-line treatment for GIST. In an attempt to optimize their assets, the company conducted further analysis of the INTRIGUE trial. They pinpointed a subset of mutations in KIT (exon 11+17/18) that seemed to favor Qinlock, while showing a lackluster response to Sunitinib (mPFS of 14.2 months vs. 1.5 months). Capitalizing on these insights, and in light of the updated Clinical Practice Guidelines in Oncology by NCCN -which now designate Qinlock as the preferred second-line treatment for GIST patients intolerant to Sunitinib-Deciphera launched the Phase III INSIGHT trial, with an estimated study completion date in 2026. Approval appears to be a likely outcome, whereas the anticipated surge in sales remains less certain. DCPH expects the 4L indication to gross 200 million peak annual sales, and to double that upon 2L approval. We believe that as treatment duration extends and geographic expansion occurs the 4L indication could peak close to 200 million, however, it is unlikely that the new 2L indication could double that, even with potential off-label utilization. According to our conservative estimates, patients with exon 11+17/18 mutations constitute approximately 10% of the GIST population , a fraction of the 4L figures, without even considering the potential overlap. Second-line patients experience longer survival, which is expected to lead to longer treatment durations. However, it is hard to fathom that this extension alone could double Qinlock's revenue.

We utilized an NPV model to calculate Qinlock's value under conservative estimates. The primary patents are estimated to expire between 2030 and 2032. At marginal COGS and ~$50M ( realistically it is higher for small biotech ) SG&A figure, the NPV model valued Qinlock between 500-700M$, based on patent expiry dates and a 10% discount rate. This figure does not account for other treatments under investigation by competitors, which might also get approved within that time frame, and prove to have superior/similar efficacy, affecting the sales of Qinlock.

| Year |

| 2024 |

| 2025 |

| 2026 |

| 2027 |

| 2028 |

| 2029 |

| 2030 |

| 2031 |

| 2032 |

| Sales |

| 180 |

| 189 |

| 198 |

| 208 |

| 202 |

| 196 |

| 190 |

| 184 |

| 37 |

| COS |

| 10 |

| 10 |

| 10 |

| 10 |

| 10 |

| 10 |

| 10 |

| 10 |

| 2 |

| SG&A |

| 50 |

| 50 |

| 49 |

| 49 |

| 48 |

| 48 |

| 47 |

| 47 |

| 9 |

| Net Income |

| 120 |

| 130 |

| 139 |

| 150 |

| 144 |

| 139 |

| 133 |

| 128 |

| 26 |

Table 1 - NPV Qinlock, Sales, COGS, SG&A, Net Income [Millions $]

Vimseltinib

Deciphera is anticipated to release the topline data from the MOTION TGCT trial in the fourth quarter of 2023. There are several issues that require attention. The follow-up data for the Phase I/II trial , which was updated in October, has set a remarkably high standard, boasting an objective response rate (ORR) of 46% in patients previously treated with CSF1R inhibitors, 53% in the untreated arm, and an impressive 69% ORR when all cohorts are considered together. However, it is important to note that the MOTION trial is specifically structured to assess the primary endpoint of ORR at the 25-week mark. In 2022 , Deciphera presented results from the Phase I/II trial ( NCT03069469 ), which showed an ORR of 38% at week 25 in cohort A (patients previously untreated with CSF1R inhibitors, n=45), and surprisingly, a 46% in cohort B (patients previously treated with inhibitors, n=11). Considering these findings, we believe that the forthcoming topline data, which will evaluate approximately 80 patients in the treatment arm, is more likely to be within the 30-40% range rather than exceeding the previous 46% figure. The overall sentiment is optimistic, and expectations are that Vimseltinib could become the leading CSF1R inhibitor in its class. As a result, there is limited room for any positive surprises to exceed these already positive expectations. If the efficacy indeed falls within the range we anticipate, it would be similar to the only FDA-approved drug for TGCT, Turalio (generic Pexidartinib), which achieved a 39% ORR at week 25 (n=61). However, it is worth noting that Turalio was linked to serious adverse events related to hepatotoxicity , and is only available via a risk management and mitigation strategy ( REMS) program. Vimseltinib strong case could be its safety profile. Even if the ORR figure does not reach exceptional levels, a safe and well-tolerated profile could indeed make a compelling case for approval. The major disappointment would be if the efficacy falls substantially below expectations. Even in case of a favorable readout, it is important to remember that Vimseltinib would have to compete with Turalio, and more importantly, generic Imatinib. The presence of Imatinib is clearly reflected in the relatively modest sales figures of Pexidartinib, totaling approximately $28M in 2022. This suggests that Vimseltinib may face a challenging competitive landscape with limited upside potential and significant downside risks.

DCC-3116

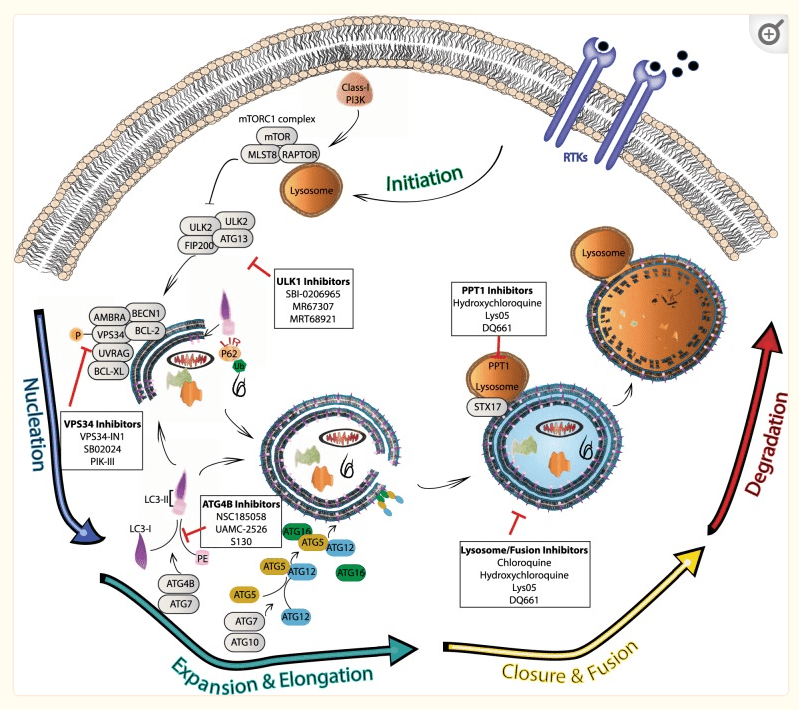

Targeting autophagy in cancer is not a novel approach. Tumor cells are known for utilizing autophagy (a process of degradation of intracellular structures for energy) to fuel their growth. There are five distinct stages of autophagy: Initiation, Nucleation of the Autophagosome, Expansion and Elongation of the Autophagosome Membrane, Closure and Fusion with the Lysosome, and Degradation of Contents. DCC-3116 targets the initial phase of autophagy, specifically inhibiting ULK protein kinase. Although the fundamental concept appears straightforward, in reality, the mechanism and its broader cellular interactions are quite intricate and not thoroughly comprehended. Certain studies suggest that autophagy can have a dual role in cancer, wherein it may inhibit tumor growth under specific conditions, such as the cellular environment, the genetic factors, and the stage of the tumor. It highlights the complexity of autophagy's role in cancer biology . Many preclinical trials have been carried out using various autophagy inhibitors, and these studies have consistently demonstrated promising results. Deciphera is evaluating their inhibitor in patients with pancreatic ductal adenocarcinoma ((PDAC)), non-small cell lung cancer (NSCLC), and colorectal cancer ((CRC)) who have solid tumors with mutations in the MAPK pathway. The monotherapy data from the phase I trial indicated that DCC-3116 alone is not potent enough to elicit a significant response, with stable disease ((SD)) being the best OR observed.

Like DCC-3116, hydroxychloroquine (HCQ) , an anti-malarial drug with autophagy inhibitory properties, has shown promise in preclinical studies as a potential treatment for tumors associated with the MAPK pathway . Nonetheless, under human testing, HCQ efficacy has come into question due to its limited impact. For instance, the phase II trial ( NCT01273805 ) in 20 pancreatic adenocarcinoma patients did not yield significant results for monotherapy HCQ. Clinical trials examining the use of autophagy inhibition in combination with other small molecules have also produced variable, underwhelming outcomes. The recent phase II trial ( NCT04735068 ) involving HCQ and Binimetinib in NSCLC (n=9) failed to demonstrate significant antitumor activity. Efforts to test EGFR mutant NSCLC patients with Erlotinib vs. Erlotinib + HCQ regimens (n=76) ( NCT00977470 ) did not result in improved progression-free survival ((PFS)), and the trial did not reach statistical significance. Another trial in CRC ( NCT03215264 ) combining HCQ, Entinostat, and Regorafenib (n=20) did not report objective responses. In addition, a phase II trial ( NCT02316340 ) that compared HCQ + Vorinostat with Regorafenib in CRC patients found that autophagy inhibition was less effective than the standard of care. Lastly, a phase II trial in advanced pancreatic cancer ( NCT01506973 ) assessed the efficacy of Gemcitabine and nab-Paclitaxel with or without HCQ (n=112), but the combination with the autophagy inhibitor did not improve the primary endpoint of overall survival at 12 months.

Why would DCC-3116 demonstrate a substantial reduction in combination therapy? This could be attributed to the fact that the two inhibitors disrupt the pathway at distinct stages.

Jean M. Mulcahy Levy, et al. 2020

{kind=link}

Figure 3 - Jean M. Mulcahy Levy, et al. 2020

DCC-3116 operates within the non-lysosomal component of the pathway, in contrast to HCQ, which inhibits the formation of lysosomes. This difference in their modes of action could potentially offer an advantage, although there is a mix of opinions on this matter . There is preclinical data indicating that inhibiting non-lysosomal autophagy can lead to the upregulation of alternative autophagic pathways in target cells , potentially rescuing them from cell death. Although we do not anticipate that targeting the non-lysosomal part of the pathway will have a negative impact on the outcome, this discovery underscores the limited comprehension and intricate nature of the mechanism involved. Furthermore, multiple sources have reported an augmented infiltration of T-regulatory cells in conditions of reduced autophagy, which could result in an overall decline in immunosurveillance. This might impact the organism's ability to combat cancerous cells effectively . We anticipate that the top-line readouts will reveal limited to no improvement in the condition, and there is a possibility, as observed in previous HCQ combination trials (a common concern with combination therapy), of an increase in toxicity.

Cash Burn And Dilution

As of Q2 2023, Deciphera holds a net cash reserve of approximately $389M. Extrapolating from recent cash burn rates ($50M in Q1 and $49M in Q2) and considering the company's newly launched trials, we project that Deciphera may consume at least an additional $100M by the end of this year and approximately $200M or more in 2024. These figures indicate a significant reduction in their cash position, especially as the company continues to expand its clinical and legal operations while also focusing on sales growth and geographic expansion. The potential need for future investments in research and development and associated selling, general, and administrative costs could require further funding.

At present, Deciphera has 85M outstanding shares. In May 2023, the company entered into an Open Market Sales Agreement, which allows for the sale of up to 200M shares through "small" transactions under Rule 415(a)(4) at market pricing. If all 200M shares were sold, it would result in approximately a 20% dilution.

Taking these factors into account, there is a compelling case for a decline in Deciphera's stock price in the upcoming months to be made. If the MOTION trial data turns out to be weak, with ORR lower than that of TURALIO, it could lead to a substantial decrease in the stock price, possibly in the teens or even tens of percentage points. In our view, with the expected dilution from the sale of additional shares, it is likely that the price could further decline into single digits. Looking ahead to the anticipated DCC-3116 data in 2024, if the results prove to be disappointing, there's a risk that the stock could plummet to or below our estimated value of Qinlock, which is estimated to be approximately 5 to $6 per share.

Conversely, if the MOTION trial data yields strong results, we believe it is likely that the stock will experience a short-term increase. However, this upward momentum may be short-lived, as the potential success of Vimseltinib appears to be largely priced in, considering the competitive market and the likelihood of sales being smaller than initially projected. This could become more apparent as 2024 progresses. There is a possibility that the DCC-3116 data demonstrates better efficacy than our initial forecasts, leading to a rise in the stock price. However, it is essential to recognize that Deciphera's efforts to secure approvals in the 2L, 3L, and 4L settings typically involve smaller patient populations than primary indications. Consequently, we do not expect Deciphera to have unlimited upside potential but rather a more modest one.

Conclusion

Deciphera Pharmaceuticals is a company that invested in new medicine for the treatment of tumors and achieved partial success. Nonetheless, from a stakeholder perspective, they have not delivered amazing results. While the company has an approved product with growing sales, it might be overestimating its potential. On top of that, we anticipate the upcoming readout to be unlikely to positively surprise analysts. The phase I pipeline is targeted at a mechanism that is poorly understood and in our opinion is unlikely to have clinical significance, based on available data. The likely further dilution and cash burn representing a significant portion of the market capitalization is another factor that could elicit selling pressure on the stock in the near future. If the pipeline fails to deliver the promised results, we believe that the company will be worth close to half of its current market cap, based on our Qinlock forecasted sales. Considering all factors at play, Deciphera Pharmaceuticals seems to be a promising short, with little upside.

Disclosure: We are short DCPH and may reverse, hedge, liquidate, or otherwise modify our position at any time without notifying Seeking Alpha. While our research is considerable, there are always publications that we might not have accounted for, which could affect our judgment.

For further details see:

Deciphera Pharmaceuticals Pipeline Is Underwhelming