SAR - Deep Fishing For Bargains: High Yields From BDC Bonds

2023-06-22 07:35:00 ET

Summary

- The rate hiking cycle is near the end.

- The Fed's hawkishness has caused great companies to issue high-yield bonds.

- Business Development Companies have structural rules that prevent over-leveraging.

- BDC bonds are a great buying opportunity.

Co-authored by Beyond Saving.

Today we take a broad look at bonds issued by BDCs (Business Development Companies) and then focus on Gladstone Investment Corp. (GAIN) and recommend their newly issued 8% baby bond:

Gladstone Investment Corp. 8.00% Notes Due 8/01/2028 ( GAINL )

- Issued May 2023.

- Callable on or after: August 1, 2025.

- Ex-dividend July 13, 2023, payment on August 1st. Because GAINL is a new issue, the initial interest payment will be for only two months, ~$0.34, and then $0.50 per quarter thereafter. ( Unfortunately, some brokers and third-party sources will incorrectly base the yield calculation on the lower amount).

- Be aware in your research. The ticker symbol GAINL was previously used for a GAIN preferred that was redeemed in 2021. You may come across some history or misinformation related to the old preferred.

Introduction

With the Fed "pause" and inflation continuing to cool, it is becoming increasingly likely that we are at, or extremely close, to interest rate peaks for this cycle.

The Fed's hiking over the past year has been the most aggressive hiking cycle since the Volcker Fed. As a result of the Fed's aggressive hiking, we have seen new high-yielding investment opportunities.

With any debt investment, there are a number of factors that determine the price. The "risk-free" rate, represented by U.S. Treasuries, is the ultimate alternative for debt investors and typically represents a baseline that impacts the rates on all debt. One common way to understand debt investments is that they should be valued as the risk-free rate plus a risk premium. The higher the perceived risk, the large the "risk premium" an investor should receive. So when a bond's price goes down, either the "risk-free" rate is going up, or the perceived risk is increasing. Conversely, we would expect a bond's price to go up when either the risk-free rate goes down or the perceived risk decreases.

So with the peak of the rate hiking cycle imminent, the risk-free rate is likely to flatten or go down. This will create an upward bias on bond prices from here. Furthermore, over the past year, we've seen bonds issued by companies that don't have higher risk but have much higher coupons than the bonds these companies issued in the past. This is solely due to the risk-free rate being higher. Now is the time to lock in these high coupons before rates decline and prices rise.

BDC Baby Bonds

At HDO, we have been huge fans of the common shares of BDCs. The typical business model for a BDC is to borrow debt at a fixed interest rate and lend at floating interest rates. As a result, rising interest rates have been fantastic for their earnings. Investors like us have been rewarded for our positions with rising dividends, supplemental dividends and special dividends as several BDCs have seen record-breaking earnings.

Yet, while BDCs are experiencing the best performance they have ever seen, the cost of their debt has been rising. For example, Gladstone Investment Corp. 4.875% Notes Due 11/01/2028 ( GAINZ ) was issued in August 2021 with a 4.875% coupon. GAINL was issued in May of 2023 with an 8% coupon.

This means that investors who bought GAINZ in 2021 received $48.75/year for each $1,000 invested. Investors who are investing in 2023 receive $80.00/year for each $1,000 invested. This increase in interest is primarily, if not solely, caused by the Federal Reserve's hiking cycle. Investors should take advantage by adding these opportunities to their portfolios now.

BDC Bonds Have Protections

"BDC" is a voluntary tax classification that companies can opt to have. For the company, it is a tax-efficient structure that allows them to avoid most Federal taxes by qualifying as a Regulated Investment Company ("RIC"). In order to qualify as a BDC, there are certain restrictions, such as a requirement to pay out most of their taxable income to investors. That requirement is why high-yield investors like us love the common shares. However, it is worth noting that there are also some restrictions that benefit debt investors as well.

When we buy bonds in a company, we will look at its balance sheet and determine if the coupon being offered is sufficient to justify the risk that the company might not be able to pay it back in the future. This is great, except for one small problem - balance sheets are not static. Most balance sheets that are a trainwreck waiting to happen were at one time quite nice. Like a college student with an 800 FICO score, what you see today might not be what you see in four years. Companies can keep issuing new debt, make bad decisions and get into trouble.

Wouldn't it be great if you could protect yourself by putting a limit on a company when you buy a bond? Well, with BDCs, you have the big stick of the IRS on your side enforcing a leverage limit. BDCs are not allowed to leverage up beyond 2.0x equity. Since equity can vary quarter to quarter, most BDCs don't get anywhere close to this line. They want to make sure they have enough cushion in the event that valuations crash and their equity declines, like during the Great Financial Crisis. The last thing common shareholders want is for the BDC to be forced to issue equity during those times.

For bond investors, this is wonderful news. Managers are incentivized to keep a decent cushion below 2.0x debt-to-equity, and even at 2.0x debt-to-equity, that implies that asset values would have to decline over 33% before the debt would be at risk. The bottom line, BDCs typically have conservative leverage profiles, and this conservatism is enforced by a power far greater than shareholders - tax laws.

Gain With GAIN

Gladstone Investment Corporation is a BDC that is part of the Gladstone family. Externally managed by Gladstone Advisors, GAIN seeks to provide outperformance by taking significant equity positions in its borrowers. Like many BDCs, GAIN makes senior secured loans with an equity investment alongside. The loans provide a predictable and recurring income stream, while the equity provides an opportunity for large but lumpy returns.

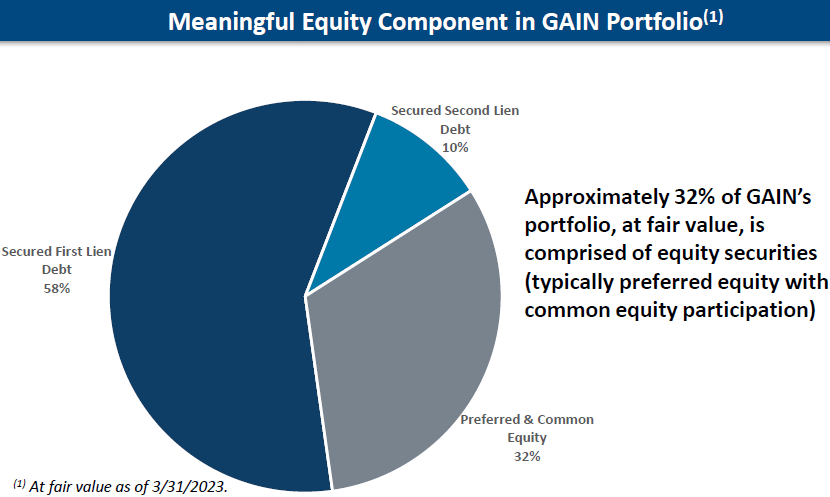

GAIN sets itself apart from peers with a 32% allocation to preferred and common equity positions. This is much larger than the typical 10% plus or minus position we see in most BDCs. Source .

{kind=link}

GAIN focuses on "lower middle market" companies that have EBITDA of $5 to $15 million/year. GAIN invests in companies that are cash-flow positive and are looking to expand.

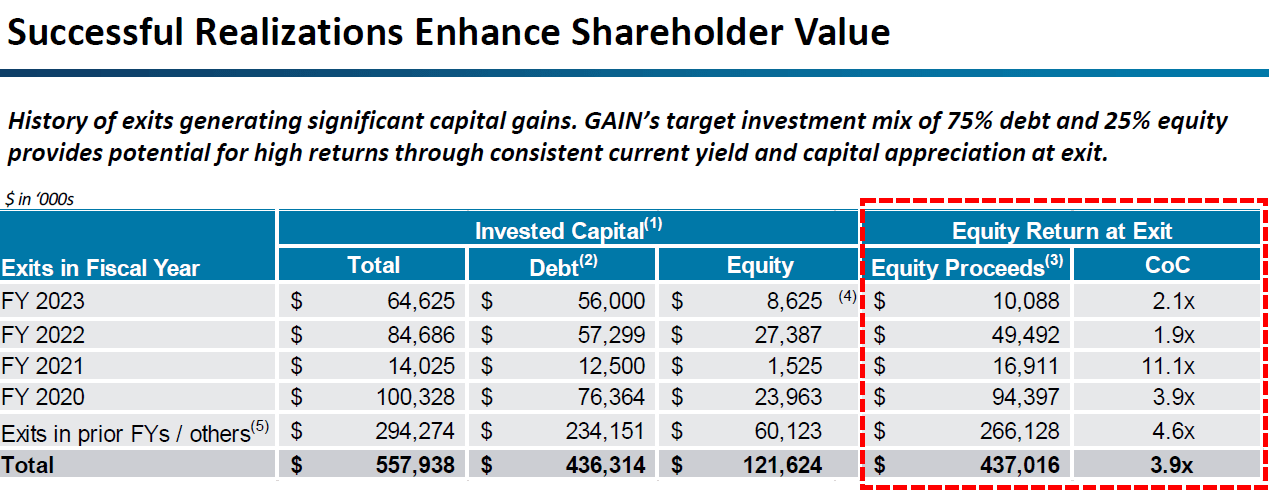

GAIN realizes gains on its equity positions when the borrower recapitalizes or is acquired by a larger peer. GAIN's history is impressive, realizing $437 million in proceeds from equity investments of $121.6 million over the years.

{kind=link}

For common shareholders, this track record has led to many supplemental dividends. Whether GAIN can maintain this track record is a very important consideration for those looking at buying common shares. For the baby bonds, it's nice to see that GAIN has been monetizing these equity positions, but we don't want to rely on it. Fortunately, we don't have to.

With a more aggressive investment strategy, GAIN maintains an even more conservative debt strategy.

GAIN Q1 2023 Presentation

We can calculate debt/equity by taking the $297.7 million in debt and divide by NAV (shareholder equity) which is $439.7 million, equals 0.676x debt-to-equity. Even if we assumed the equity positions GAIN owns were worth $0, debt-to-equity is still below 1.5x.

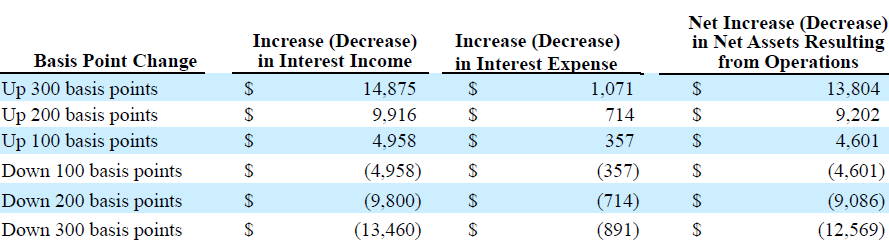

Debt investors in GAIN can have a lot of confidence that the assets are worth significantly more than the debt, even in a distressed environment. Meanwhile, GAIN has significant coverage for its interest expense, with Net Investment Income ("NII") covering interest expense by 3.3x last year. That could be expected to compress initially as interest rates decline, causing interest received to decline, but 3.3x is more than ample cushion. For example, according to GAIN's 10-K, if interest rates were cut 300 bps tomorrow, net investment income would decline by $13.4 million/year. Source .

{kind=link}

Even with that, GAIN's NII would cover its interest expense a healthy 2.6x.

The bottom line is that GAINL is offering a high coupon, while GAIN's business is very healthy, and the margin of safety for bond investors is very high. The coupon being much higher than the older bonds is a reflection of rising rates, not rising risks. With interest rates near peak, now is the time to buy!

Other BDC Bond Opportunities

Consider these alternatives as well:

- Capital Southwest Corporation 7.75% Notes due 2028 ( CSWCZ ) - A newly issued baby bond from Capital Southwest ( CSWC ) that will start trading soon. We love the common equity for CSWC; the baby bond is a great option to step up in the capital structure.

- Saratoga Investment Corp., 8.125% Notes due 12/31/2027 ( SAY ) - An attractively priced baby bond from Saratoga ( SAR ). We recently realized gains in the common shares. We saw SAR as one of our riskier BDC common equity holdings. We would be perfectly comfortable holding the bonds with an 8%+ yield.

- Prospect Capital Corp. 2028 Notes 3.437% (CUSIP 74348TAW2 ) - PSEC traditional bonds are trading at a huge discount to par, providing an opportunity to get a 9% yield to maturity, that is a lot more than the 3.437% yield investors were willing to accept when they were issued! If you are interested in building a traditional bond portfolio, these are a great investment grade bonds to add.

Conclusion

It is a fantastic time to be building a fixed-income portfolio, and we can thank the Fed for the opportunity. However, we also want to be aware that there is a risk of a recession starting within the next year, making it crucial that we invest in opportunities that can withstand the heat.

BDC bonds are a great place to look. While BDCs will experience headwinds from a recession like any other business, the legal leverage limitations imposed on BDCs prevents them from getting too far out of line. Then when the Fed reacts by cutting interest rates, the risk-free rate will decline, and the value of bonds with 8% coupons will rise significantly. We will have the option of realizing gains to invest elsewhere or just holding and collecting our income until maturity.

For further details see:

Deep Fishing For Bargains: High Yields From BDC Bonds