NGMS - Deep Sail Capital Partners Q4 2022 Investor Letter

Summary

- Deep Sail Capital is a Delaware-based pooled investment vehicle. Our mission at Deep Sail Capital is to compound the capital of our Limited Partners over long periods of time while being mindful of tax implications.

- For the fourth quarter of 2022 Deep Sail Capital Partners returned 6.9% net of fees while averaging 76% net long exposure.

- As many market participants have pointed out, if we head into a recession in 2023, it will be the most telegraphed recession in modern history.

Investors,

For the fourth quarter of 2022 Deep Sail Capital Partners (the “Fund”) returned 6.9% net of fees while averaging 76% net long exposure. For the full year 2022 the Fund returned -32% net of fees while averaging 83% net long exposure. Please consult your individual capital account statements for your individual net returns.

{kind=link}

In the fourth quarter, the fund slightly outperformed our benchmarks. The main driver of our relative outperformance in Q4 was driven by strong performance from the short portfolio which contributed 10% in Q4, due to many of our short positions declining significantly. The long portfolio had a mixed Q4, and I took the opportunity to harvest tax losses which should offset all the short-term capital gains we generated in the short portfolio this year.

Market Commentary

In the fourth quarter, the market grappled with the "soft landing vs. hard recession" debate. This debate reminds me a bit of 2007/2008 and 2012, when different outcomes materialized. As many market participants have pointed out, if we head into a recession in 2023, it will be the most telegraphed recession in modern history.

Forecasting the exact outcome of markets in the future is an incredibly difficult task. The main issue is that the future is very path dependent and responsive to all inputs. Inputs impacting the future are ever evolving which can include consumer sentiment, business confidence, employment, global situations, labor issues, fiscal policy, and a myriad of other inputs. The problem is that even the act of forecasting and publishing your forecast can impact the path of the future. The future is path dependent; even low-probability events can manifest in unusual and intriguing ways. Because of this, I try to keep a probabilistic view of future outcomes and position the fund to be successful in all potential outcomes.

So to get back to the original question, are we headed for a soft landing or a hard recession? I'd say it's probably around 60/40 right now, slightly weighted toward a soft-landing scenario due to consumer balance sheets and employment being in the best shape they've ever been. Real estate is destined to decline in 2023 with the new higher and longer rate regime at the Fed. That will provide a bit of a reverse wealth effect that will compound the reverse wealth effect we have already seen with public markets. Any consumer debt-driven industry should be materially impacted in this rate environment. Used cars, boats, RVs, Furniture, and any major consumer purchase relying on debt will be impacted. Furthermore, inflation will put pressure on consumer spending as the costs of food, energy, and staples consume more of their paychecks.

It is clearly a time to be cautious and avoid any companies that have significant debt or rely heavily on consumer debt to fuel their sales. I've built the funds short and long portfolios around this cautious outlook on markets.

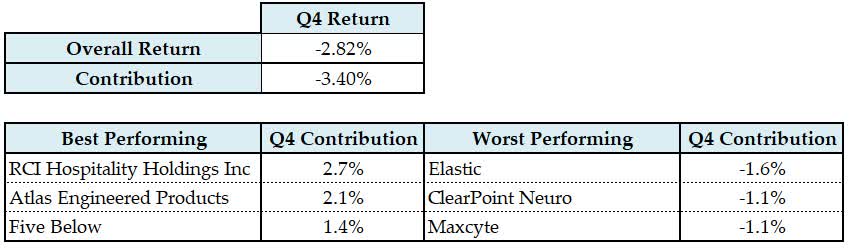

Long Portfolio Summary

{kind=link}

The fourth quarter was a mixed quarter for the long portfolio. RCI Hospitality Holdings ( RICK ) and Atlas Engineered Products ( APEUF ), our two largest positions, performed well throughout the quarter, increasing by 42% and 44%, respectively. Several of our small cap positions were down 15% or more in Q4, including all the Cell & Gene Therapy (CGT) picks and shovels that I described in the Q3 Investor Letter. Our thesis on these CGT pick and shovel companies remains unchanged, and we added to them opportunistically in the fourth quarter.

The fund closed six positions and opened four long positions in Q4. We selectively closed positions in Q4 to harvest tax losses and reallocated that capital to our cheapest and most attractive positions. Most notably, we opened a large position in NeoGames S.A. ( NGMS ), an "iLottery" (internet lottery) gaming company. We believe iLottery is an attractive, growing end market globally, and that NeoGames is extremely well positioned to take advantage of this growth.

Existing Position: Leatt Corp

Leatt Corp. ( LEAT ) (pronounced: "Lee At") is a design and distribution company in the field of protective gear for motocross and mountain biking, including neck braces, helmets, gloves, chest protection, and apparel. I recently appeared on the podcast Chit Chat Money to discuss my long thesis for Leatt.

Below is a summary of the fund’s long thesis on Leatt:

High Quality Business Model: Leatt is a technology and design company. The technology and patents are all in house. They have created & patented two major industry safety technologies since their founding. The first is the Leatt Neck Brace, and the second is called 360 Turbine Technology, which is used in their helmets. The helmet technology is important, as the alternative helmet technology was developed and is licensed by MIPS from Sweden.

Leatt does all its own distribution. They outsource all their manufacturing to subcontractors in China, so they don't need any capex or expenses related to manufacturing. Because they own their own distribution, they have a lot of inventory in transit on their balance sheet. Their products are sold through regional distributors and specialty Motocross stores.

The Leatt brand is synonymous with safety as they were the first to develop and market a neck brace. They put a large emphasis on safety and design. Brand-wise, they now have an offering of a full "kit," including neck braces, chest protectors, helmets, boots, goggles, and apparel. Because 50% of Motocross riders use a Leatt Brace, the majority of the industry is familiar with the brand, making it much easier to cross sell helmets and apparel. They recently have been making a big push with marketing campaigns globally to increase brand awareness for their entire kit.

Gross margins are in the 40s, and ROIC is in the 30–40% range. Their margins have been consistent for the last 4–5 years, and I expect they can continue forward at around these margins for a long time.

Outstanding Management: Leatt is run by the founder, Dr. Chris Leatt (head of R&D, who develops all new products), and longtime CEO, Sean Macdonald. They have no need to raise capital; they have self-funded their new distribution center in the USA and built their inventory levels to support significant revenue growth over the next few years. Management has said they won't need to raise capital for anything and should start generating more cash as they scale their distribution channel to a reasonable level in 2022.

Substantial long term growth prospects: This huge market share in neck braces is a huge advantage when it comes to cross selling other gear. When someone is buying gear, they want it all to match, and they want it to look cool. So, if they have a specific-colored neck brace, they want to match the rest of their gear to it. That’s part of the cross sell, which is why Leatt outperformed the industry in 2022. Their helmets really took off once they started to sell helmets with the 360 Turbine Technology, which launched in early 2022.

There are two types of Moto helmets: those that use MIPs technology and are used by Fox, Thor, Bell, and others, and those that use proprietary crash technology, such as Leatt and 6D. Companies with proprietary technology have better margins and set themselves in a different category than MIP-licensed helmets. Leatt has a mid-single digit market share in helmets, but it basically doubled in 2022 with the release of their new helmets with 360 Turbine technology, which are supposed to be safer than MIPS tech, per research released by Leatt.

Reasonable Valuation: We believe Leatt is extremely cheap as we believe it can grow revenues by 20–30% over the next few years. It currently trades at 5x EV/EBITDA on LTM and 8x PE. I do think that with a strong holiday season coming up, they could do over $3/share in EPS in 2022, with a current market price of about $19/share.

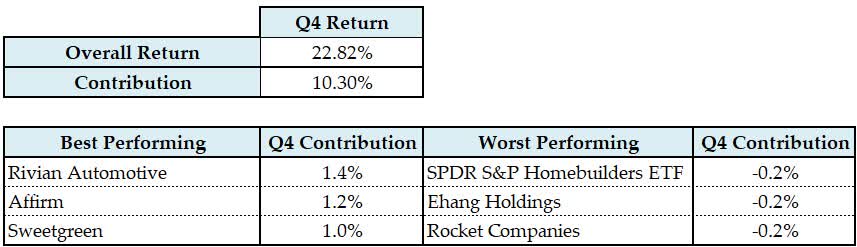

Short Portfolio Summary

{kind=link}

The short portfolio significantly outperformed our benchmarks in Q4. "Junk" stocks performed particularly poorly in Q4, with many heavily shorted companies declining by over 30%. As we mentioned in our Q3 investor letter, we are very focused on avoiding short squeezes in this environment.

We continue to keep short positions in companies in the electric vehicle and alternative energy industries, as well as companies that are moonshots (no revenue companies with big ambitions) or failed SPACs. With the recent quick rise in interest rates, we have added material short exposure to industries that rely on consumer debt and homebuilders.

Top Holdings & Current Exposure

{kind=link}

At the end of the Q4 the fund held 22 long positions and 27 short positions. The fund ended the quarter with an exposure of 118% long and 35% short or a 75% net long exposure.

Sincerely,

Deep Sail Capital LLC

| Disclaimer Deep Sail Capital LLC (“Deep Sail Capital”) is an investment adviser to funds that are in the business of buying and selling securities and other financial instruments. This information is provided for informational purposes only and does not constitute investment advice or an offer or solicitation to buy or sell an interest in a private fund or any other security. An offer or solicitation of an investment in a private fund will only be made to accredited investors pursuant to a private placement memorandum and associate subscription documents. Past performance is no guarantee of future results. “Deep Sail Capital Partners” returns in this document are shown as Gross Returns. For Net Returns of fees and expenditures figures please reach out to the fund manager at the email info@deepsailcapital.com . “Deep Sail Capital LLC” name was changed on April 7 th 2022 from the previous name “Organon Capital LLC”. “Deep Sail Capital Partners LP” name was changed on April 6 th 2022 from the previous name “Westropp Funds LP”. “Strategy Since Inception” refers to the Strategy inception date of July 2016. Deep Sail Capital Partners LP’s predecessor incubator fund, “Westropp Funds LP” pivoted from a Value Investment style to a Growth at a Reasonable Price (GARP) style fund on that date. For more details on this transition or the calculation behind the “Strategy Since Inception” returns please reach out to the fund manager at info@deepsailcapital.com . |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Deep Sail Capital Partners Q4 2022 Investor Letter