WMT - Deep-Value Opportunity To Invest In High-Yielding Non-Cyclical Stocks

2023-08-23 00:37:15 ET

Summary

- Non-cyclical stocks offer steady growth and reliability, attracting investors during economic downturns.

- Rising interest rates and inflation pose a risk to stocks, making bonds with "durable" interest rates an attractive option.

- Consumer staples stocks have underperformed in 2023 but may see a turnaround due to potential inflation risks and rising oil prices.

- Kraft Heinz and Conagra Brands are high-yielding deep-values that could produce triple-digit total returns over the next 10 years.

Non-cyclical stocks are the stock of companies that tend to have a steady business throughout all phases of the economic cycle.

Steady often means unchanging, but in today's environment, it means steady growth for most consumer staples businesses. Not high growth or accelerating growth in most cases but steady growth.

The kind of growth that you can rely on. The kind of growth that isn't driven by the whims of politicians or the bureaucrats that serve them but by consumers.

Oddly, non-cyclical as their businesses may be, the stock prices are as cyclical as they come. These stocks don't have the flash or bang of a high-growth name or market leader like NVIDIA ( NVDA ), so they fall out of favor with investors when times are good, and growth stocks blossom.

When times are bad investors tend to flock to these names for safety. The reliability of non-cyclical business models and the dividends that come with them are attractive when interest rates are rising, inflation runs hot, and the fear of rising oil prices has the Fed's finger on the interest rate trigger.

Think about this, 6 of the 49 stocks that qualify as Dividend Kings in 2023 are Consumer Staples ( XLP ). That's more than 10% of the most-trusted dividend stocks that consistently grow their yield.

Non-cyclical and consumer staples stocks are solid income-producing investments, but you have to buy them at the right times.

The time is right to buy consumer staples stocks ...

The downside of non-cyclical stocks is that they underperform the broad market over the long term. The XLP lags the SPY ( SPY ) by more than 300 basis points over the last ten years on an annualized basis, but that does not include the dividends.

The dividend issued by non-discretionary and consumer staples, in particular, can help offset the difference.

If you can buy these stocks on dips or at lows, they can produce significantly greater total returns. When they can be bought at rock-bottom prices, the total returns are often counted in triple digits.

As they say, the best tip is to buy low and sell high, but it's always hardest to buy when the market is down.

Consumer Staples has had a hard time in 2023. The tech-driven market melt-up left them in the dust and down about 1.0% YOY compared to nearly 15% for the S&P 500 in mid-August.

This situation is about to change.

The FOMC Minutes Alter The Outlook

The market melted-up in a summer rally because the recession we've all been waiting for didn't materialize. The problem is that the conditions which were supposed to lead to the recession are still in place, and the FOMC is still hiking rates. The minutes from the July meeting confirmed an outlook that I forecasted just days before they were released; there is an upside risk to the inflation outlook.

The most significant risk is the oil price which is set to rise. OPEC+ has the oil market tilted in favor of higher prices which won't change without significantly reduced demand targets.

The demand outlook has some sketchiness, but two things can be counted on. The first is that OPEC+ will continue to tighten supply and support prices as they can. The 2nd is that China will prop up its economy somehow; the question is when and how much.

The takeaway is that the FOMC may hike rates more than once again this year and as many as several times before the rate-hiking cycle is over, which is bad news for stocks.

Discounting the risk to the financial sector, the risk of recession, and weakening earnings power for S&P 500 companies, rising rates present a significant headwind to stocks. It's hard to put money into stocks when you can get more than 5% on a 1-year T-bill . Stocks come with risk, and this year the risk is above average.

Consumer Staples have a below-average beta, or risk, compared to the S&P 500. The beta for 9 of the top 10 holdings of the Consumer Staples ETF is below 1.0, the average is 0.63, and the single outlier is Target ( TGT ), which has a problem. It can't compete in the current environment and is losing ground to Walmart ( WMT ), grocery stores, and off-price retailers.

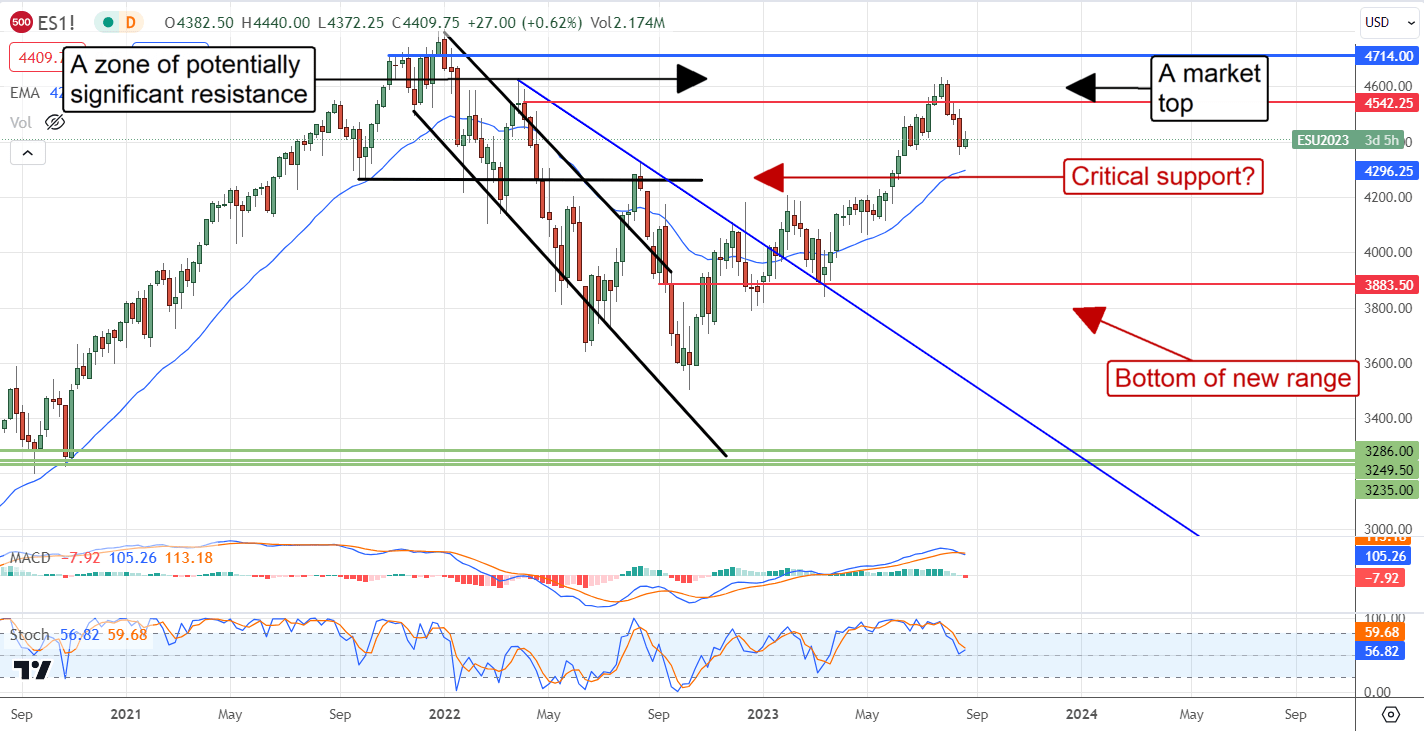

Volatility Fell to a Multi-Year Low This Summer: What Is The Market Thinking?

The VIX ( VIX ), the market's fear gauge, fell to the lowest level since the COVID-19 pandemic began over the summer. The index low coincides with the weeks in early February 2020, just before the big crash. With interest rates still hot and the FOMC on track to hike rates again, you have to ask yourself what the market is thinking now.

The answer may be, "Duh, what was I thinking," given the latest twist in the FOMC outlook. That sentiment is seen in the VIX and the S&P 500, which now show signs of respective bottoms and tops.

{kind=link}

TradingView /Screenshot/Own work

The top in the S&P could be a significant 1 or the first signs of a much bigger top yet to form. The next major hurdle for stocks will be the PCE price index, due at the end of August. That report will not likely show a significant increase in inflation, at least not 1 associated with higher oil prices, and it may allow the market to resume its uptrend, but the risk of correction will grow.

Eventually, the market will have a rude awakening with the FOMC and higher rates.

The CME FedWatch Tool continues to show the market mispricing the Fed's intention, the state of inflation, and the outlook for oil prices. As it is, the market assumes only a 35% chance of a single hike, and it thinks there could be a cut by the end of the year. I don't think so, not unless oil prices subside.

So, the market is heading for a hard ceiling if it hasn't already hit it. If it isn't at 4634.50, that ceiling is likely at an all-time just above 4,800. The question is how deep the pull-back will be, which could be considerable.

The combination of interest rate risk, FOMC risk, diminished earnings outlook, and the allure of safe-haven Treasuries could combine to make a deep correction. A move to critical support at the 150-day EMA is worth 2.7%; a fall to the bottom of the established range will top 12%.

An Equity-Like Return From Bonds

Bonds are an alternative to equities, which is unquestionable, but there is an added attraction with the peak of the rate cycle approaching.

According to a recent report from Vanguard, investors who buy into longer-dated maturities with "more durable" interest rates could see equity-like returns over the coming years. Bonds tend to do well after the rate-cycle peaks.

Nonetheless, with a fed funds rate well into restrictive territory, the potential remains for equity-like returns in fixed income when policy rates eventually normalize. For bond investors, that would be like an upgrade to first class."

But there is a downside to the bond trade. You can buy the Ten-year and get roughly 4.25% for ten years, which is less than the S&P will average, or when rates fall, you can sell the bond at a profit after pocketing a year or 2 of interest. But what then? You'll have to reinvest. By then, the oh-so-lucrative bond trade will be played, and stocks will have likely moved higher.

This makes it more critical to stay invested in equities and do it wisely. You can get an equity-like return from a long-dated bond with little risk, but those returns are still limited compared to what deep-value high-yielding consumer staples like Kraft Heinz ( KHC ) and Conagra Brands ( CAG ) can produce.

Finding Value In A Down Sector

The consumer staples sector is down, and it may fall further due to the valuations of some of the companies. Among the takeaways from the sector regarding valuation relative to the S&P 500 are...

- "Fair value" for the sector is roughly 22X to 26X earnings. The bulk, about half, of the most commonly traded consumer staples, including Procter & Gamble ( PG ), PepsiCo ( PEP ), and Walmart ( WMT ), are in this grouping. This makes them expensive relative to the broad market by 50% or more.

- The yield on a "fair value" consumer staple stock is in the low 2.0% to 3.0% range. This is above the S&P 500 average, which is nearly 1.5%. This is a reason the group trades at an elevated valuation.

- The broad group has a wide range of valuations, with the lowest trading near 12X earnings and the highest above 30X.

- There is an inverse relationship between the yield and value. The higher-valued stocks pay lower yields, while the higher-yielding tend to trade at lower valuations. Dips in share prices are often met by buyers looking to get higher average yields at lower average prices.

Kraft Heinz Is A Deep-Value With The Highest Yield

I've written about Kraft Heinz many times and will continue to do so until the investment thesis plays out or I am proven wrong. The short story is that scandal rocked the House of Cheese following its merger with Heinz resulting in a deep-value opportunity.

The company is now years into its turnaround and is operating in a lean condition with eyes on international expansion. The stock trades at a ridiculously low 11.6X its earnings while doing so, and it pays the highest dividend in the sector, not counting the tobacco stocks.

The yield is high, over 4.5%, and will be compounded by an earnings-driven stock price increase over the next ten years. The valuation suggests there might also be a price-multiple expansion in the works. Trading below 12X earnings, it could double in value while rising in price and delivering triple-digit total returns.

Highlights from the Q2 2023 earnings report:

- YOY revenue growth falls to 2.6% from 7.3% in the prior quarter.

- Margin outpaces consensus estimates.

- Guides 2023 for organic revenue growth of 4% to 6%, or 6% to 8%, adjusted for last year's 53rd week.

- AGM to expand 150 to 200 basis points.

- Raises earnings guidance.

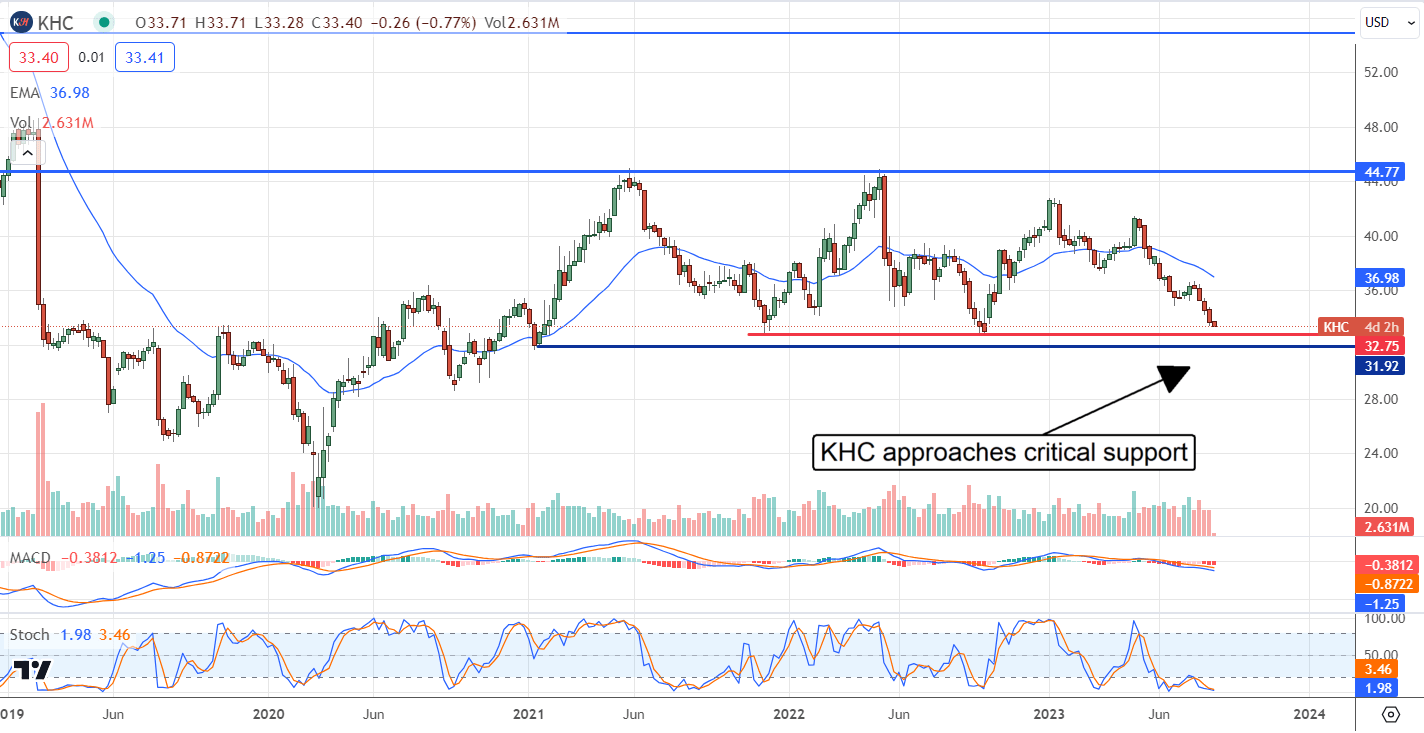

Kraft Heinz's stock price has led the consumer staples group since the 2020 bottom. The market for KHC is approaching a critical support target that has been a floor for the price action over the last 2 years. This level should produce another rebound when reached.

It should also be noted that institutions are buying KHC . Their activity is ramping up in tandem with the 2023 price retreat.

{kind=link}

TradingView/Screenshot/Own work

Visible catalysts for the stock price include the upcoming earnings report due in late October. The company guided a mid-point below the analysts' consensus targets and helped to pressure the stock price. Even so, the analysts have lowered their targets so that consensus underestimates the company's guidance and sets it up for outperformance.

Non-visible catalysts are the dividend and the potential for dividend increases. Kraft Heinz has not mentioned plans to increase distributions, but it is on investors' minds. If and when they do, it will unleash shareholder value.

Kraft Heinz pays out about 55% of earnings compared to 60% to 90% for established dividend growers like Hormel, Clorox, and Proctor & Gamble, so there is room in the cash flow when the board thinks the time is right. Until then, the stock will pay 4.75% annually.

Conagra Brands: Another 4% Yielding Deep-Value

Conagra is similar to Kraft regarding yield and value without the scandal and turnaround story. Its share price has suffered along with the remainder of the sector due to the post-bubble letdown and the current (possibly over) 2023 stock market melt-up. The salient point is that it trades at less than 12X its earnings alongside KHC and pays a dividend worth more than 4.5%.

Conagra's 2Q results were nearly identical to Kraft's, with single-digit growth, mixed performance, and margin strength. The company also guided growth and continued margin improvements supported by pricing actions in 2022. Other report highlights include reduced net leverage and reinvestment in growth initiatives.

Unlike Kraft, Conagra has increased its distribution over the last few years. The company pays out roughly 50% of earnings and increases at a 10% CAGR, which appears sustainable. Once it turns around, this is an added tailwind for the CAG market and a potential catalyst for a price-multiple expansion should the company accelerate distribution growth.

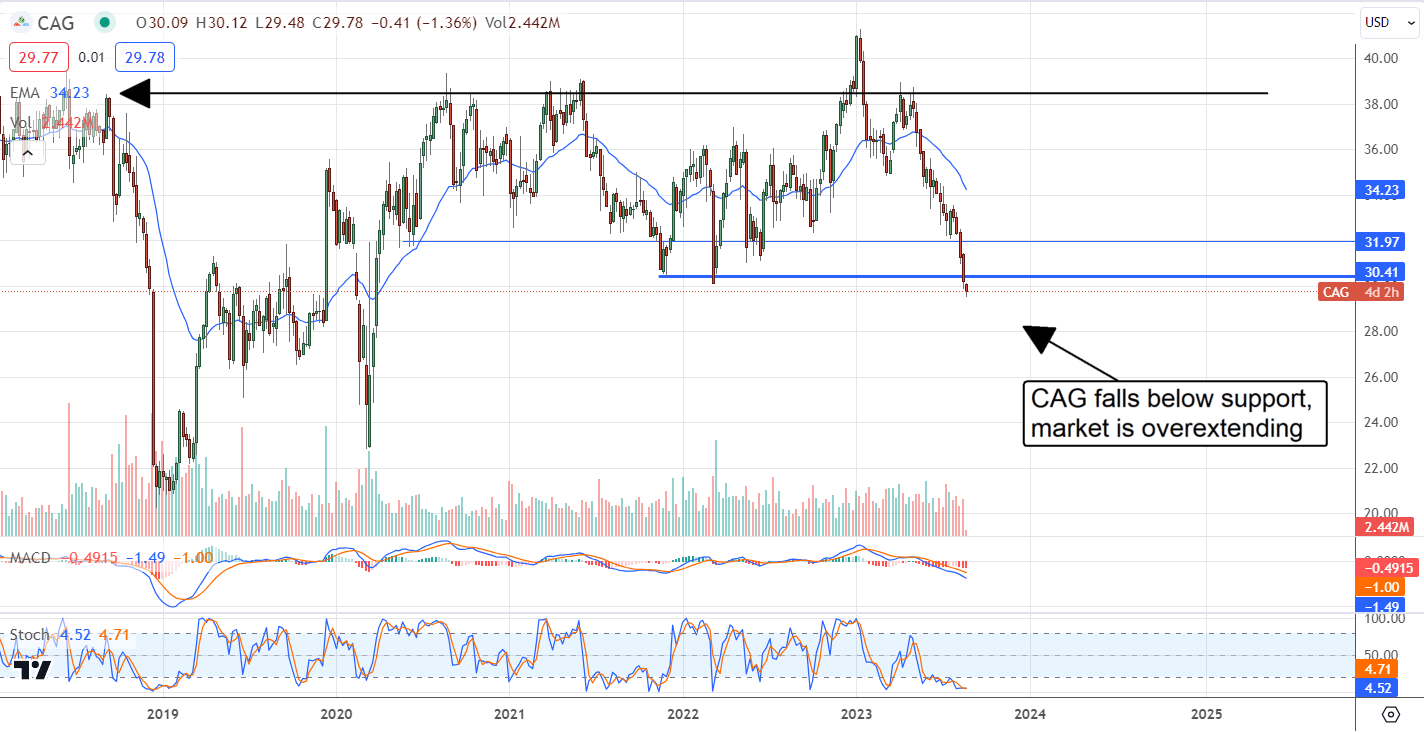

The price action in CAG shares hit a new low in August but appears to be overextending. Catalysts for the market are the PCE report when it is released or the Q3 earnings reports due in October.

{kind=link}

TradingView/screenshot/own work

Summary ...

- Non-cyclical business models offer sustainable and reliable returns for investors.

- Non-cyclical stock prices are as cyclical as any stock on the market, and many are trading at significant lows.

- Stocks like KHC and CAG offer deep value and high yield within a high-yielding sector and will outperform over the long term.

- The market is mispricing inflation and the FOMC; these stocks could come back into favor sooner rather than later.

- The mid to long-term outlook for KHC and CAG is for triple-digit total returns.

For further details see:

Deep-Value Opportunity To Invest In High-Yielding Non-Cyclical Stocks