DE - Deere & Company: The Problems You Experience When Buying At Extreme Valuations

2023-08-29 13:34:39 ET

Summary

- Deere & Company failed to deliver satisfactory shareholder returns even as the business continued to deliver.

- Ongoing industry tailwinds are now at risk and based on previous cyclical downturns, the stock is not yet a bargain.

- Shareholders should keep a close eye on the company's ability to retain its pricing power as volume growth is likely to stall.

The past few years have been nothing but spectacular for Deere & Company ( DE ). The business performed exceptionally well and it fully capitalized on industry tailwinds and increased spending in the agricultural sector.

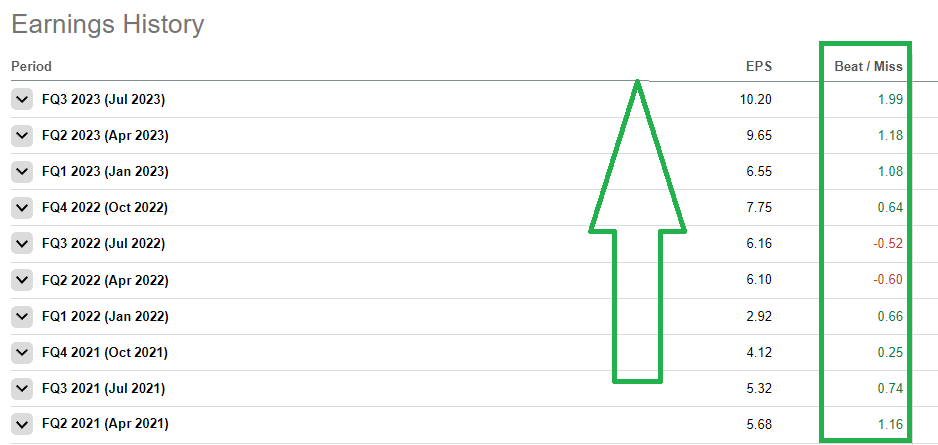

Since I first covered the stock in early 2021, the quarterly earnings per share number has nearly doubled and the company has consistently beaten the consensus estimate in every quarter, except for two.

{kind=link}

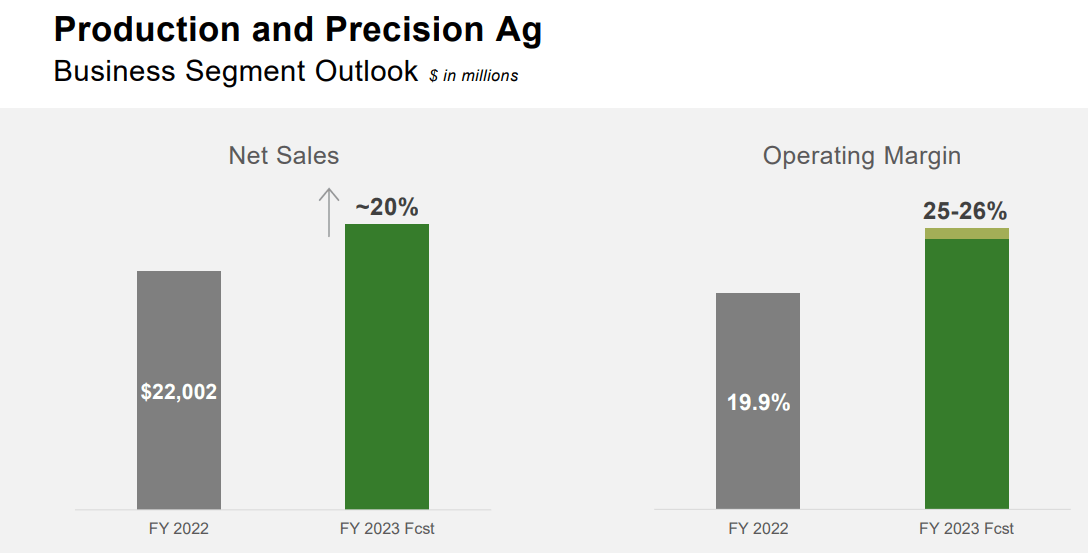

Management guidance for the rest of the current fiscal year across all business units also remains strong, with the largest segment - Production and Precision Ag expected to close the year with significant revenue growth and margin improvement.

{kind=link}

After such a strong multi-year business performance, one would reasonably expect that Deere's shareholders would have been rewarded with significant and above-market returns. Unfortunately, however, since March of 2021 DE has appreciated by a mere 4% and even underperformed the broader market.

That was the exact reason why I warned that shareholders buying into the stock in early 2021 would face poor returns going forward, even if the business continued to perform well. Fast forward two and a half years and this is now reality.

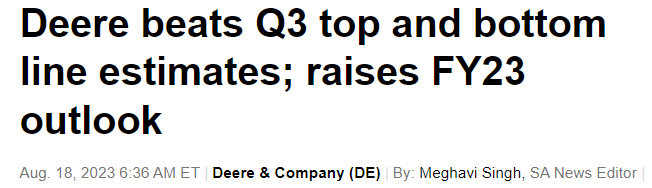

On top of all that, just last week the company reported yet another strong quarterly results and the share price did not react materially on the news.

{kind=link}

After years of shareholder returns and actual business performance going in separate directions, it has now become clear that the share price was running way ahead of fundamentals a few years ago.

With the gap between the two narrowing down, the stock appears far more attractive now than it was in early 2021. Having said that, I still have a hard time turning bullish on Deere.

Cyclical Peaks And Margins

One very useful graph that gives us a good reference point of where Deere's share price is trading is the one comparing the company's operating margin versus the price-to-sales multiples on a time series basis. Over time, the two variables exhibit a strong relationship, once we properly account for peaks and troughs in the business cycle.

prepared by the author, using data from Seeking Alpha and SEC Filings

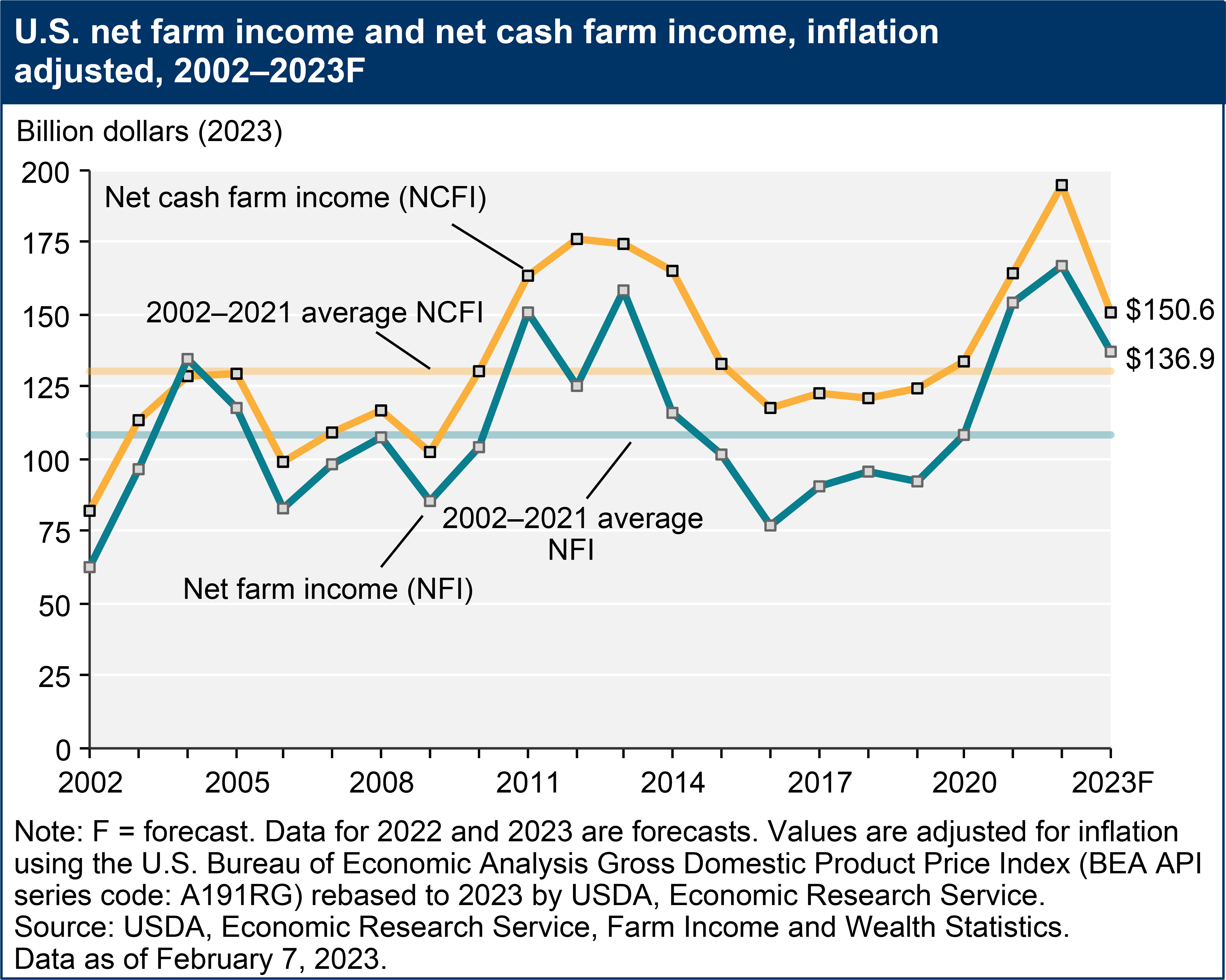

Since Deere operates in a cyclical industry, the 2011-2014 period we see above coincides with the peak in U.S. net farm income (see below). Because the market was expecting a cyclical drop in farmers' income during that period, Deere was trading at much lower sales multiples than its current margins were suggesting.

{kind=link}

As we are now most likely past the cyclical peak in U.S. net farm income, Deere's P/S multiple is once again far lower than the company's current margins suggest.

Net farm income, a broad measure of profits, is forecast at $136.9 billion in calendar year 2023, a decrease of $25.9 billion (15.9 percent) relative to 2022 in nominal (not adjusted for inflation) dollars. This follows a forecast increase of $21.9 billion (15.5 percent), from $140.9 billion in 2021 to $162.7 billion in 2022. After adjusting for inflation, net farm income is forecast to decrease $30.5 billion ( 18.2 percent ) in 2023 relative to 2022.

As a result, DE is unlikely to produce meaningful returns going forward, unless we either experience a sharp and more permanent reversal of U.S. net farm income upwards or the company proves that it could sustain its current margins during a cyclical downturn.

The former scenario is highly speculative and in my view unlikely, but the latter appears to be within the realm of possibility.

Will Price Premiums Last?

Expectations regarding deteriorating net farm income would most likely continue to weigh on Deere's share price. In the meantime, however, Deere's management has done a great job at fully capitalizing on the recent cycle by implementing significant price increases.

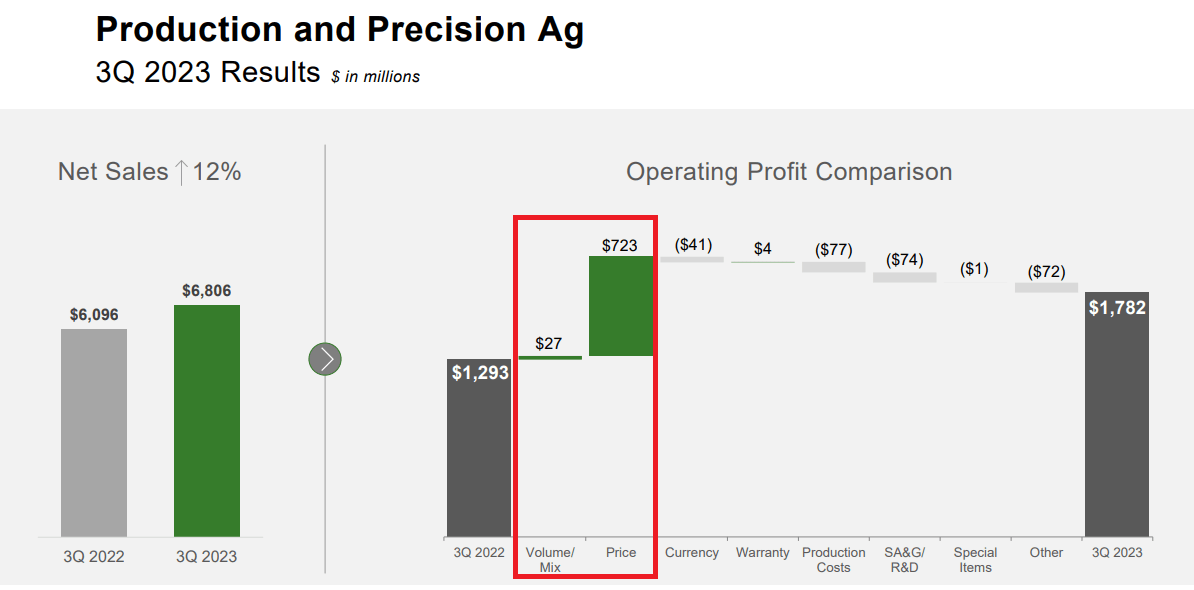

As we see below, higher price realization was the key driver of margins during the latest quarter, at a time of lower shipment volumes and higher fixed costs.

Operating profit improved year-over-year to $732 million, resulting in 19.6% operating margin. The year-over-year increase was primarily due to price realization and was partially offset by higher production costs, lower shipment volumes, and increased SA&G and R&D spending.

Source: Deere Q3 2023 Earnings Transcript

The graph below highlights the crucial role that pricing played during the latest quarter for the company's largest segment - Production and Precision Ag.

{kind=link}

While Deere's production costs continue to increase, so far pricing initiatives are more than enough to offset them and resulted in an unprecedented improvement in gross margin.

The whole topic of Deere's strong pricing power that is driving profitability is hardly a new one and has been a recurring theme on quarterly earnings for a number of years now.

{kind=link}

What caught my attention a few years ago was that the main narrative has been gravitating around the company's innovation in autonomy as a key driver of Deere's strong pricing power within the sector.

{kind=link}

In reality, however, large competitors have also enjoyed significant pricing power in recent years which suggests that this is mostly an industry-wide phenomenon caused by recent supply chain issues.

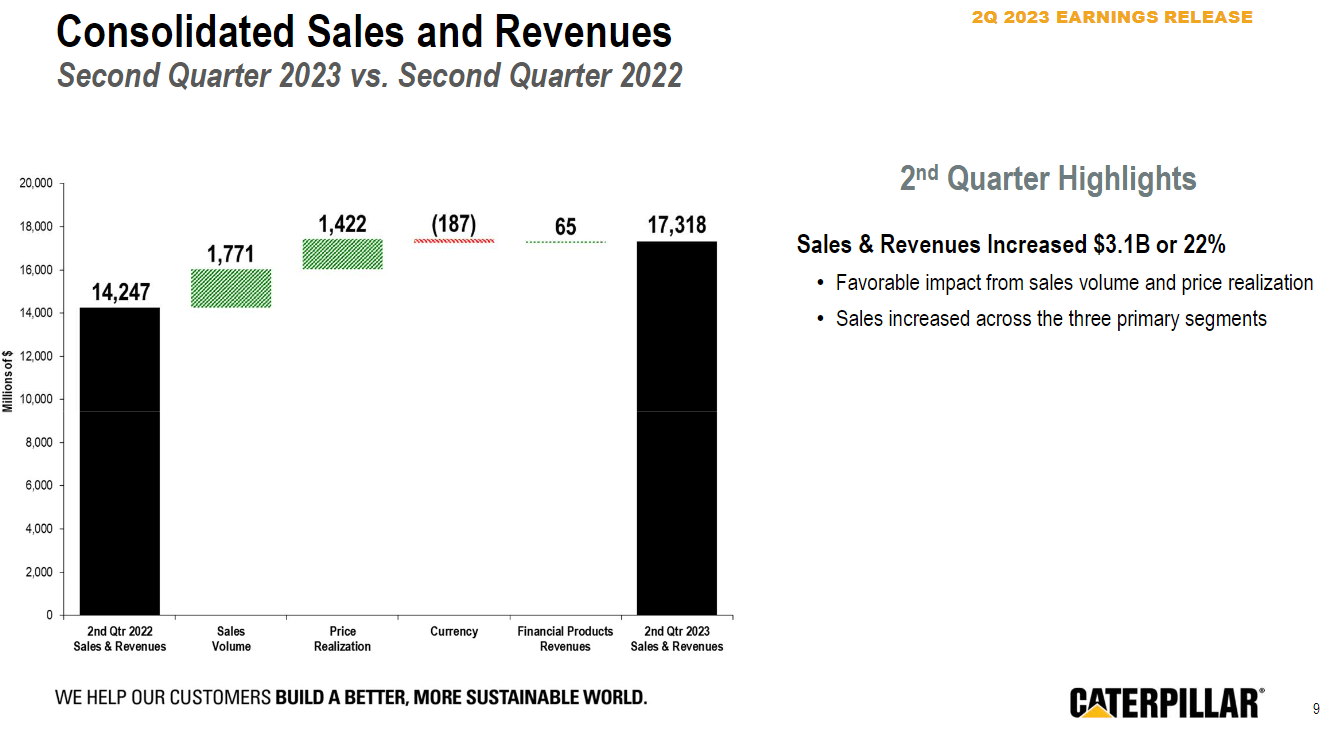

Caterpillar ( CAT ), for example, recently reported yet another record quarter in profitability that was also largely driven by pricing.

In the second quarter of 2023, sales and revenues increased by 22% to $17.3 billion. This was primarily due to higher sales volume and price realization.

Source: Caterpillar Q2 2023 Earnings Transcript

{kind=link}

CNH Industrial ( CNHI ), which is a direct competitor to Deere, has also been making significant progress in gross profitability in recent years. Consequently the gross margin gap between the three aforementioned companies has narrowed down significantly following the pandemic.

When we breakdown Deere's asset turnover, we notice that since 2020-2021 period, inventory and fixed asset turnover have been going in separate directions. This is a direct result of unprecedented demand for Deere's products which brought capacity utilization to record high levels and also resulted in higher inventory requirements as order backlog increased.

prepared by the author, using data from SEC Filings

So far it appears that this trend would continue for at least one more quarter as the company closes on its fiscal year 2023 (see below). Beyond that, however, there is a lot of uncertainty as U.S. net farm income falls and higher interest rates squeeze economic activity.

Ag fundamentals continue to remain healthy, with a full order book and positive customer sentiment supporting a strong finish to fiscal year 2023. Meanwhile, Construction & Forestry remain sold-out for the remainder of the fiscal year with robust shipments driven by strong retail demand and rental re-fleeting.

Source: Deere Q3 2023 Earnings Transcript

Deere investors should keep a close eye on the company's ability to retain its pricing power as volumes come down. In the graph below, we could see that we are now most likely past the peak in pricing tailwinds for the company's margins in its largest segment, but the impact on volume/mix is now likely turning negative.

prepared by the author, using data from Deere Investor Presentations

That is why, the impact of pricing over the next few quarters will be of great importance for Deere's ability to sustain its high gross margin in a lower growth environment.

Investor Takeaway

After failing to deliver satisfactory shareholder returns, Deere now appears as a bargain based on the company's recent profitability improvements. However, there is a solid reason why the company now trades at much lower multiples than it used to just a few years ago. On top of fading industry tailwinds, Deere's record-high margin is likely to come under pressure over the coming quarters as volume growth stalls and fixed costs continue to increase.

For further details see:

Deere & Company: The Problems You Experience When Buying At Extreme Valuations