RNMBF - Defense Stocks: Consider Taking Profits Before Tide Turns

2023-08-29 21:36:52 ET

Summary

- Short-term bullish narrative for defense stocks due to increased NATO military spending and threats from Russia and China remains mostly intact but is priced in.

- Long-term outlook for defense stocks is impaired due to the lack of overwhelming effectiveness of Western military equipment in Ukraine and economic factors that may impair defense spending.

- Some markets such as the Arab states may be slipping away as the world realigns from a geopolitical point of view.

- Some early signs of a reversal in fortunes include Germany's U-turn on meeting its 2% NATO pledge, which suggests it may be time for investors to consider taking profits on their defense stocks.

Investment thesis: Given the massive depletion of Western and other allied weapons & ammunition stockpiles, due to the need to support the Ukraine war effort, assuming a massive increase in NATO military spending seems to amount to a no-brainer. Furthermore, the Russian & Chinese military threats are seen as a reason to expect NATO members, as well as allies such as Japan and S. Korea, to seek a beefing up of their military capabilities. These are all valid reasons to be bullish on defense stocks. Sales contracts are coming in, and so are the pledges all over the NATO alliance and beyond to increase defense spending. The continued need to provide Ukraine with weapons & ammunition also factors into the equation.

While the short-term bull case for the defense industry looks solid, the longer-term outlook actually looks impaired by it. The sight of multiple systems, ranging from Leopard Tanks to the Patriot air defense system being hit by the Russian military, seems to be shattering the myth of Western military hardware invincibility that was built during the Iraq war and in other places. The lack of Ukraine's ability to impose itself against Russia, despite receiving about $100 billion worth of Western military equipment raises serious questions about what if any advantage any military around the world may gain from acquiring this equipment. NATO members and a few allies may continue to buy, but many others around the world will probably shy away from paying for systems that often sell at a premium.

The negative economic effects of the war and other negative factors are weighing on the ability of the US & allies to continue spending well over $1 Trillion/year combined on defense spending. There are early signs that it is starting to take a toll and some countries are starting to pull back. Taking all the longer-term factors into consideration, any further advances in defense stocks should be seen as an opportunity to take profits, rather than as a signal to buy.

Good news for the defense industry in the short term still translates into modest to no profit growth, broadly speaking of the industry as a whole.

Poland just had its planned purchase of Apache Helicopters approved, for a $12 billion deal. The whole of the former communist part of the EU is in defense-spending fever mode. Soviet-era stockpiles of weapons & ammunition that they inherited from the Cold War era are now gone, donated to Ukraine , and most of them need to be replaced, so the region can be expected to continue spending generously on weapons for the foreseeable future, especially, given the perceived threat of Russia. Lockheed's F-35 program is seeing traction as well, with the likes of Germany , Canada , and others either committing or showing interest.

The old equipment that clogs Western armories is making its way to Ukraine. Denmark & the Netherlands both committed to donating dozens of old F-16 fighter jets, while the broader plan includes them taking delivery of new jets like the F-35. This tends to be the model throughout the NATO alliance, although modern equipment that is still top of the line is also being donated, like Leopard 2 tanks, that European nations intend to replace with new ones. Right now this conflict looks like a true bonanza for US & European weapons manufacturers.

These higher expectations of current and future sales for weapons manufacturers led to significantly higher valuations for these companies.

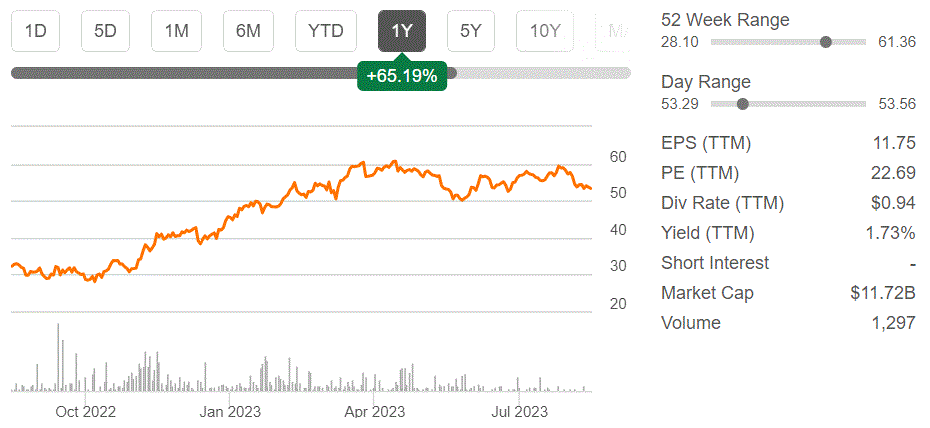

Rheinmetall stock chart (Seeking Alpha)

{kind=link}

As we can see, Rheinmetall ( RNMBY ) trades at a pretty high forward P/E of almost 23. It implies that expectations are for robust growth going forward. Its latest quarterly numbers suggest that sales growth has been decent at over 7% over the past year. Net profits declined because profit margins declined from 7% to 5%. The growth story is therefore not necessarily entirely evident a year into the Ukraine war, and as I shall explain, things might get worse.

A similar situation can be observed with other weapons manufacturers such as Lockheed ( LMT ) as well as BAE ( BAESY ). They have a forward P/E of under 17 and under 16 respectively. Lockheed's net earnings declined just slightly in the latest quarter, compared with the same quarter in 2022. BAE, stands out, having seen a steep increase in earnings for the first half of this year of about one-third compared with the same period of 2022. It remains to be seen whether BAE will continue to buck the trend set by its peers, or whether its results were more of an outlier, which is set to rejoin the herd. Overall, it can be said that at least so far, the Western defense industry, though it has seen a fair amount of growth in revenues, has not seen a spectacular increase in profits, which might explain the arguably high P/E ratios we are seeing.

A growing list of negative pressures on Western weapons sales going forward.

As a way to better focus on the main issues facing various markets for the Western defense industry, I chose to break it down into three main ones. The United States, the EU, and the rest of the world.

- United States is facing out-of-control fiscal deficits.

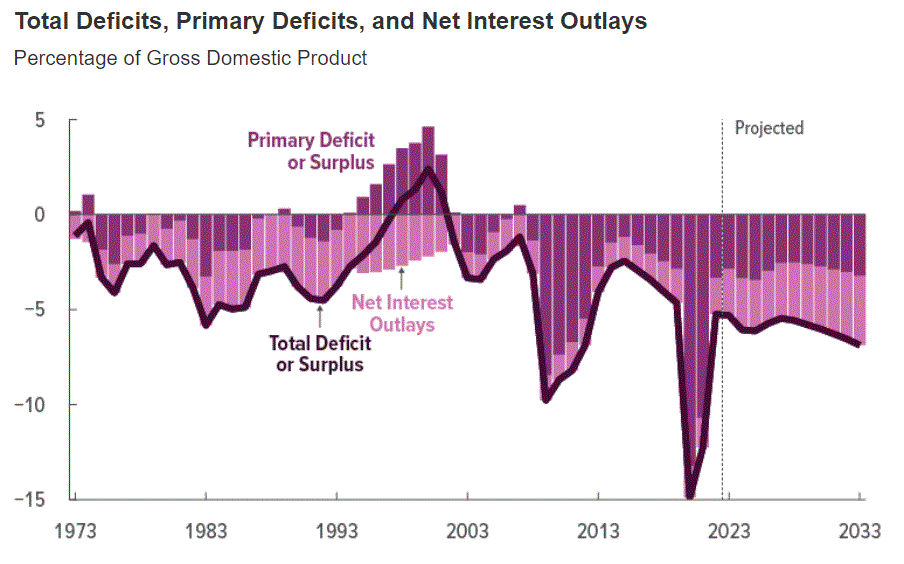

The CBO is forecasting a gloomy outlook for the US fiscal situation, with deficits widening to as much as $2.7 Trillion/year a decade from now.

{kind=link}

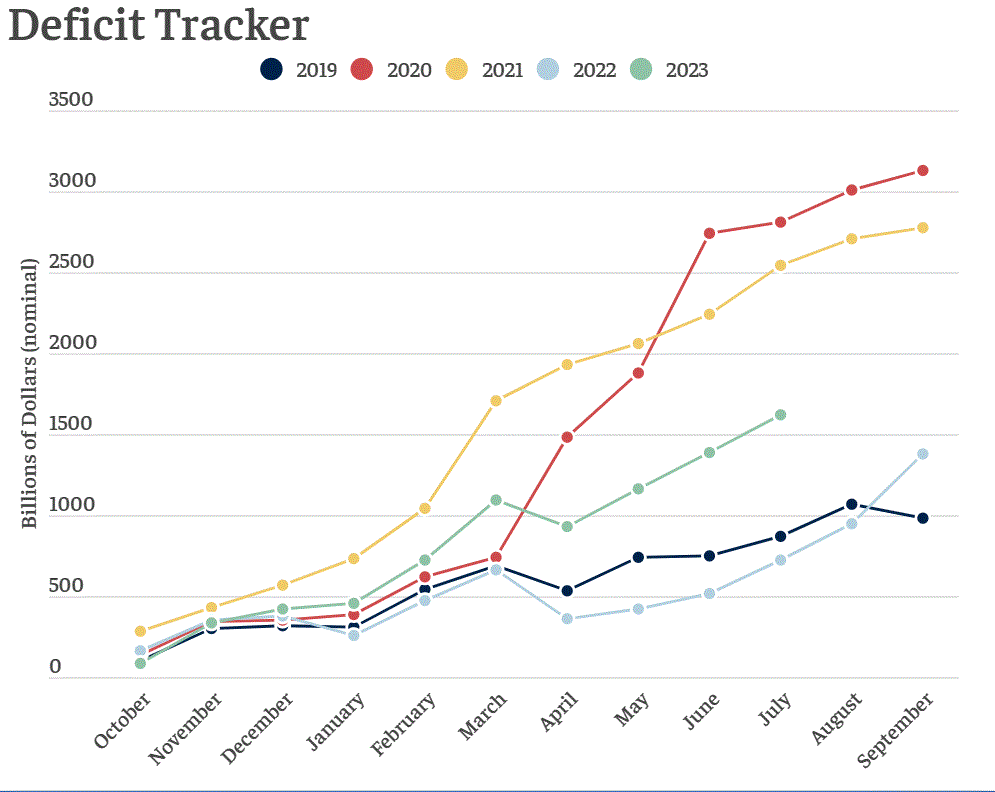

As bad as that may seem, for the current fiscal year, with still a few more months to go, we are already beyond the CBO projection of $1.4 Trillion.

{kind=link}

We are already at over $1.6 Trillion for the current fiscal year, so it is likely that we will see a significant overshoot. It remains to be seen where the full-year deficit will be, but at the moment it looks like it will overshoot spectacularly. This also raises questions about next year and beyond, which at some point, arguably soon will have to be addressed, whether through preemptive political action or perhaps, eventually by the market, first, then by the political class.

The CBO is going on the assumption that defense spending will reach $1 Trillion a decade from now, up from over $800 billion currently. It is by no means a massive increase, which by itself is a reason to be skeptical about the defense industry sales and profits growth narrative. It could be argued that government policies will push that spending much higher, but I do not see the fiscal room to do so. As dire as the CBO projections might be, it seems they are somewhat optimistic potentially, given the current deficit trajectory, as well as arguably other factors such as global and US economic growth within what increasingly seems to be a stagnating long-term economic situation. If anything, we might see some sort of a path being prepared, in geopolitical terms, such as a ratcheting down of tensions, as well as efforts to prepare the public for deep cuts in defense spending. It is far easier to cut defense than it will be to cut Social Security for instance, regardless of how much influence the defense sector might have on the political establishment.

- Europe is economically stagnated and will always be just one harsh winter away from an energy shortage catastrophe.

Former French President, Nicholas Sarkozy was recently quoted as saying that Europe is "dancing on the edge of a volcano", in reference to the Ukraine conflict. He seemed to be focused on the unwelcome aspect of growing tensions with Russia. From an economic point of view, as I have been pointing out, this proxy war seems to have put the EU in perpetual danger, every winter. This coming winter, in particular, I foresee the possibility that a global energy crunch could start in Europe, in the event that both the EU & the US will see colder-than-average winter temperatures. If this is the case, elevated defense spending will become the last thing that European electorates will be willing to tolerate.

As it stands, the EU economy is currently facing stagflation and Germany just signaled that it does not intend to meet its 2% of GDP defense spending pledge to NATO. While many countries, particularly in the Eastern part of the EU are still strongly committed to ramping up defense spending, other countries such as Italy don't have much fiscal room to start splurging on weapons. Even in a best-case scenario, where year after year, Europe will dodge the bullet and will not experience a winter energy catastrophe, it is facing a severe economic crisis, with multiple factors pushing it toward a permanent loss of economic forward momentum. It is hard to imagine how such a European economy will be able to sustain elevated levels of defense spending.

- The Ukraine conflict shattered the Western military tech superiority myth.

Following two Iraq wars since the end of the Cold War, where the Iraqi army, which was heavily reliant on Soviet technology was easily defeated on both occasions, a sense of Western military invincibility emerged as a post-Cold War paradigm. This paradigm may have been true until recently. The picture emerging so far this year, as Ukraine continues to fight as a de-facto proxy combatant, mostly dependent on Western weapons is one that in my view shatters that paradigm.

Overall, though reportedly highly motivated, the Ukrainian army seems to be failing in defeating the Russians. We saw several Western weapons systems, ranging from drones to the HIMARS , being reportedly neutralized whenever Russia employs electronic warfare capabilities. We see that Russian Lancet drones are taking out highly rated Leopard 2 tanks, just as well seemingly as they can take out an old Soviet T-72. In other words, Leopard 2 tanks may decimate any opponent fielding T-72 tanks, but the realities of war as showcased by the Ukraine situation suggest that such encounters may be rather rare, as both sides are more likely to see their tanks destroyed by drones, light anti-tank weapons, missiles, mines and so on.

Rheinmetal's Iris-T anti-aircraft systems are also reportedly falling prey to the same drones. The famous Patriot air defense system also seemingly failed to shine, when it was allegedly targeted by a Russian hypersonic missile. While Western weapons superiority is still arguably intact, they now look far less invincible than they once did.

The straight answer to whether the continuing Ukraine war is and will be good for the Western defense industry and its shareholders might seem to be a resounding "yes". I doubt however that military analysts advising the Indian, UAE, Saudi, and other governments around the world will look at the detailed performance of Western systems and be as eager to recommend them for purchase as they might have been a few years ago. Even if they do, it is more likely that it will come with recommendations to drive a bargain or look for cheaper alternatives, since these weapons are now less likely to be considered must-have systems for achieving superiority over potential enemies.

It should also be noted that formerly dependable customers for Western weapons systems, such as Saudi Arabia and UAE are now arguably slipping away as exclusive markets for us, given that they were both recently admitted into the BRICS group. In the run-up to this event, China managed to get an Iran-Saudi rapprochement deal, before both were admitted into the group. This rapprochement arguably lessens the pressure on Arab states to build up their defense capabilities, which might shrink the regional market for weapons systems. Furthermore, Arab states might start to buy Russian, Chinese, and even some Iranian systems, which will further shrink the demand for Western weapons in the area. My personal view is that outside of NATO, a few close major allies in the Pacific area, such as Japan, Australia & Taiwan, demand for Western weapons is set to decline this decade.

Investment implications:

In response to the initial assumptions that the Ukraine war will usher in an era of global defense spending growth, the defense companies I mentioned have seen a decent advance in their stock price. Rheinmetall's stock price more than doubled since then. Lockheed saw an increase of almost 20% in its stock price, while BAE stock saw an appreciation of over 50%. There is to date no evidence that any of these companies are set to see a corresponding long-term bump in profits. BAE has shown some promising results in this regard, but I believe it can easily be reversed in the longer term. They seem to be priced for growth that just isn't likely to materialize in the long term.

Taking stock of all major markets available to the Western defense industry, broken down into three different entities, the most promising potential market, namely the US market is itself a less-than-promising prospect. The CBO projection of $1 Trillion/year in military spending a decade from now is less than 20% higher than current levels in nominal terms. Prospects of significantly higher spending in the EU on the military look increasingly bleak, despite the current war fever mindset we are seeing. The EU economy cannot sustain it in the long term. As I already highlighted, outside of the NATO-centered alliance, prospects are actually worsening for the Western defense industry.

There is not much in my view that can provide a further boost to Western defense stocks, broadly speaking. Some company-specific details may emerge that could nudge any individual company higher. There are also potential pitfalls. For instance, Lockheed's F-35 project could still take a hit, if, for instance, irrefutable evidence were to appear of Russian or Chinese air defense systems being able to effectively deal with its stealth capabilities. From a broader perspective, those who wisely invested in defense stocks in the run-up to the Ukraine war might consider this to be a good time to take some profits. For those who are looking to buy, this is the classical "opportunity" to buy high and potentially end up having to sell low.

For further details see:

Defense Stocks: Consider Taking Profits Before Tide Turns