ENB:CC - Defensive 7-8% Yields: Enbridge Vs. Antero Midstream

2023-10-21 09:00:00 ET

Summary

- Earlier this year, we felt that Antero Midstream Corporation had better upside potential than Enbridge Inc.

- However, since then Antero Midstream has significantly outperformed Enbridge.

- We revisit our thesis and compare them side-by-side to see which is the better buy today.

A little over six months ago, we compared two high-yield midstream infrastructure companies in Antero Midstream Corporation ( AM ) and Enbridge Inc. ( ENB ). We concluded at the time that:

For investors looking for a higher yield and a more speculative investment, AM is the better buy. However, for those looking for a well-rounded blue chip that will continue to churn out reliable dividend growth for years to come through thick and thin, ENB is the clear winner.

Since then, AM has delivered on its potential for generating very attractive total returns, while ENB has seen its stock price plummet, though it has continued to churn out stable dividends as we expected:

With such a dramatic change in their stock prices, we are going to check back in on both businesses to see if ENB has become the clear winner in both risk profile and total return potential, or if AM still offers investors better upside potential.

ENB Stock Vs. AM Stock: Business Models

ENB is a leading North American midstream business, primarily concentrating on oil and natural gas assets, but also growing its small renewables portfolio. One of its most significant assets - the Mainline system - controls over 70% of Canada's oil takeaway capacity and connects it to U.S. refineries, making it an indispensable part of North American energy infrastructure. In addition to this asset, ENB also owns substantial natural gas assets, including its recent $14 billion acquisition of several natural gas utilities from Dominion Energy ( D ). As a result, it has now become North America's largest natural gas utility company in addition to its status as a major midstream infrastructure company. After acquiring Dominion's utilities, Enbridge's business mix will be:

- 50% liquids pipelines

- 25% gas transmission

- 22% gas distribution (including the utilities)

- 3% renewables.

This will give it a balanced exposure to both oil and natural gas related commodities while also having an additional avenue for long-term growth via its renewables business.

Something else to really like about ENB's business model is that it is well protected against inflation, commodity price volatility, and macroeconomic downturns. With over 80% of its EBITDA being inflation-protected, 51% of its cash flow coming from long-term take-or-pay contracts, 47% of its cash flows coming from regulated utility or utility-like assets, and over 95% of its counterparties being investment grade, ENB has one of the most stable cash flow profiles in the entire energy industry with less than 2% of its EBITDA comes from assets subject to commodity risk.

With numerous avenues for growth investment available and a very stable and well-diversified earnings base, ENB is well-positioned to continue driving stable growth in shareholder value for years to come.

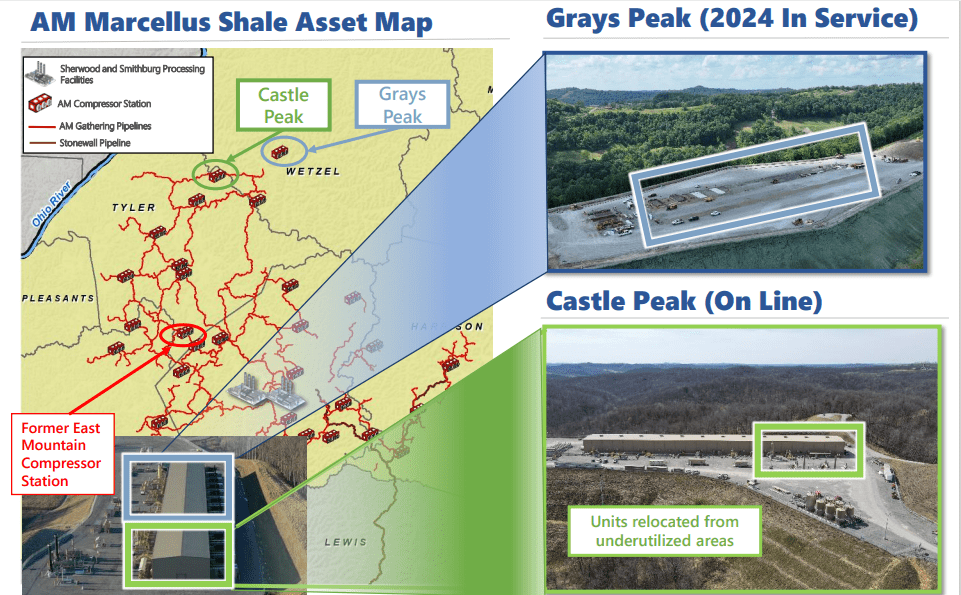

AM, meanwhile, has a much smaller asset footprint than ENB does and largely exists to service one client: Antero Resources ( AR ). At the moment, AM is focused on optimizing its compression and processing utilization and has been steadily increasing its compression capacity utilization along with a recent acquisition of underutilized capacity, resulting in capital-efficient growth. Moreover, their processing capacity has been consistently utilized at 95-100% due to their ability to pivot between Ohio Utica or Marcellus Dry Gas. Their Sherwood and Smithburg Processing Facilities, compressor stations, and gathering pipelines are well-positioned for servicing AR's production and recently AM has relocated units from underutilized areas to the Castle Peak and Grays Peak stations in order to improve operating efficiencies.

{kind=link}

These efforts have been paying off, as AM reported a 10% increase in Adjusted EBITDA year-over-year despite a whopping 31% decrease in capital expenditures in Q2. Moreover, their gathering and compression volumes have increased by 11% and 17% respectively, year-over-year while AM also realized acquisition synergies from two bolt-on acquisitions made in 2022. Moving forward, they are focused on continuing to expand their asset base to drive EBITDA growth, execute flexible just-in-time investments, and deliver a peer-leading Return on Invested Capital of between 17% and 20% while also generating dependable free cash flow net of dividends in order to lay the groundwork for growing shareholder capital returns in the future.

Overall, ENB's asset portfolio is nearly impossible to beat in the midstream space given its size, strategic positioning, and very conservative cash flow profile. That being said, AM's management has been doing a commendable job with maximizing the value of its small asset portfolio by growing EBITDA even while slashing capital expenditures. As a result, while AM's risk profile is clearly higher than ENB's, we think that AM has an impressive business model in its own right that is generating exceptional returns on invested capital.

ENB Stock Vs. AM Stock: Balance Sheets

ENB's credit rating of BBB+ speaks for itself and is largely the product of the business' utility-like cash flow profile. An added benefit of its substantial regulated earnings is that it supports having higher leverage on its balance sheet compared to many of its peers, thereby juicing returns on equity. Moreover, ENB is in the fortunate position of having locked up the vast majority of its debt at fixed interest rates, with maturities extending for many decades, giving it a predictable and low debt cost of capital for years to come at a time when long-term interest rates are soaring.

AM, meanwhile, has a mere BB credit rating, which is more than a full letter below ENB's. That said, it does have a positive rating on that credit rating, implying that an upgrade could be coming soon. AM has made significant strides in recent quarters by increasing its free cash flow generation and using it to pay down debt aggressively. As a result, AM's leverage ratio has been reduced to 3.5 times, down from 3.7 times at the end of 2022 and the company is progressing aggressively towards its target of achieving a leverage ratio of 3.0 times or less by sometime in 2024. Once it achieves this objective, AM should be in excellent position to increase capital returns to shareholders given that its free cash flow continues to grow as AM drives EBITDA growth while slashing capital expenditures as much as possible.

Overall, both businesses appear to be on solid financial footing. ENB once again is given the advantage here due to the very lengthy terms at which it has locked in most of its fixed rate debt as well as its BBB+ credit rating. However, AM's low leverage ratio and commitment to continue reducing it further indicates that it is also in sound financial shape.

ENB Stock Vs. AM Stock: Dividend Outlook

When it comes to dividend outlooks, both dividends are quite well covered by cash flows at the moment. ENB is expected to cover its 2023 dividend with free cash flow by 1.03x and AM is expected to cover its 2023 dividend with free cash flow by 1.29x. While ENB's coverage ratio may appear tight, on a discounted cash flow ("DCF") basis, the coverage ratio is closer to 1.5x as it is investing aggressively in additional growth projects.

Looking ahead, ENB is expected to grow its dividend in-line with DCF per share growth, which management anticipates coming in at a 3-5% CAGR. As a result, investors should view ENB as a slow but steady dividend grower, with low risks of a dividend cut given the resilience of its cash flows and the strength of its balance sheet , but with fairly limited upside as well given that its cash flows are so stable, and its large size and the nature of its business model limit the pace of growth as well.

Meanwhile, AM shareholders should not expect any dividend growth through 2024, but after that, there is an excellent chance that AM will begin to grow its dividend once again. While it is hard to know the pace of such growth, the large buffer of free cash flow that is already present on AM's cash flow statement indicates that it should be able to grow its dividend at a pace that exceeds per share free cash flow growth if it so chooses. Given that analysts expect free cash flow to grow at a ~5% CAGR through 2027, we could see AM growing its dividend at a 5-7% CAGR beginning in 2025.

ENB Stock Vs. AM Stock: Valuation Analysis

First and foremost, it is important to keep in mind that ENB has numerous advantages over AM that justify it commanding a superior valuation:

- Its asset portfolio is of much higher quality. Its regulated assets in particular generally command a premium valuation to contracted assets. Moreover, its counterparties are almost all investment grade, and it has a much better diversified set of assets and counterparties than AM, which is beholden to a single counterparty.

- It has a much stronger credit rating, which implies a lower risk profile and better access to capital.

- It has grown its dividend every year for 28 years and has delivered attractive total returns over the long-term in contrast to AM, which has suffered from a steep dividend cut not too long ago and has underperformed the midstream sector over the long-term:

With that being said, let's have a look at their current valuations:

| Valuation Metric |

| AM |

| ENB |

| Dividend Yield |

| 7.3% |

| 8.2% |

| EV/EBITDA |

| 9.2x |

| 11.4x |

| EV/EBITDA (5-Yr Avg) |

| 8.7x |

| 12.5x |

While AM is still technically cheaper than ENB by a wide margin based on an EV/EBITDA basis, ENB's dividend yield is a whopping 90 basis points higher than AM's and its EV/EBITDA is discounted to its historical average whereas AM's currently trades at a premium to its own historical average. As a result, in our view, ENB is currently cheaper than AM is.

ENB Stock Vs. AM Stock: Investor Takeaway

Overall, we like both of these midstream companies as ENB has a strong long-term track record and an impressive array of assets that is getting even more impressive with its acquisition of several new regulated natural gas utilities. AM, meanwhile, has been executing very well on its business plans to drive improved free cash flow generation and deleverage its balance sheet .

That being said, in our view ENB is hands down the better risk-adjusted buy right now given its vastly superior portfolio of assets, far better credit rating, higher dividend yield, more predictable dividend growth profile, and discounted EV/EBITDA relative to its history. As a result, we rate it a Strong Buy and AM a Hold.

For further details see:

Defensive 7-8% Yields: Enbridge Vs. Antero Midstream