DH - Definitive Healthcare: Undervalued Vs. Peers Given Revenue Growth And Margin Expansion

2023-11-14 10:41:59 ET

Summary

- Strengthening fundamentals: Definitive Healthcare shows steady revenue growth at 10% and expanding adjusted EBITDA margins.

- CRPO growth is slowing to a controlled rate and stabilizing, which indicates the end of client churn that took place over past 2 years.

- Valuation outlook: Fair price potential around $9.0, signaling a 25% upside from current $7.18.

Introduction

Definitive Healthcare Corp. (DH) is a lesser-known company in the Healthcare Technology & Distribution sector (often referred to as Healthcare IT), which offers a predictable cash flow stream and a transparent business model. It may be a suitable investment for those trying to add some indirect exposure to the healthcare sector with lower volatility and limited concentration risk associated with any specific healthcare name.

{kind=link}

from company website

Company Overview

Definitive Healthcare Corp. provides commercial data and intelligence to companies looking to sell products and services into the healthcare industry. The Definitive Healthcare platform combines provider sales data and market analytics, which allows customers to develop insights on market size, competitive positioning, and marketing strategies for their products, and physicians most appropriate to target, among other things. Some of the core customers are drug and medical device manufacturers, life sciences companies, diversified non-healthcare companies, and healthcare vertical companies (some examples are Lenovo, Medtronic). As of November 2022, the company had more than 3,000 total customers.

The company is often compared against peers such as Doximity ( DOCS ) and HealthEquity ( HQY ), whose financials are influenced by similar factors. However, DH's offerings are quite unique.

While Doximity concentrates on communication tools for medical professionals and HealthEquity specializes in managing health savings and spending accounts, Definitive Healthcare stands out by providing comprehensive data, analytics, and market intelligence to a broader audience in the healthcare industry for strategic decision-making, rather than collaboration and networking. The unique nature of Definitive Healthcare's services is evident when clients, facing budget constraints, suspend subscriptions, as there is no comparable alternative offered by competitors. Notably, these clients often return to the service when their budgets allow, underscoring the unmatched value provided by Definitive Healthcare in the market.

Investment Rationale

Definitive Health can be considered a leader in the healthcare commercial intelligence space. Although years 2022-23 have been challenging for smaller health companies in terms of navigating tighter budgets, and having to allocate them elsewhere, recently the churn among them has evened out and enterprise customer growth should improve in the next few years. This positions DH for stable grown and predictable increasing cash flows.

Below we discuss some of the main reasons for a positive investment opinion.

Revenue and EBITDA margin growth projections

During last earnings ca ll ( 3Q’23 ) , management provided the following financial metrics:

- Total revenue for Q3'2023 was $65.3 million, which represents 14% year-over-year growth, and adjusted EBITDA was $21.7 million, which translates into a 33% margin. Revenue and adjusted EBITDA for the quarter were both above the high end of the guidance ranges for the quarter.

{kind=link}

Author's calculations, YCharts, SEC filings

Note: adjusted EBITDA is used in discussion throughout the earnings call and this article, and there is a significant difference between adjusted EBITDA and GAAP-conforming standard EBITDA. Both are reported in the company’s SEC filings and a reconciliation is explained, stating that adjusted EBITDA excludes non-cash, non-recurring expenses or items unrelated to core operations, and therefore not representative of ongoing operational performance. Examples of such items are equity-based compensation, acquisition, integration, and restructuring expenses, goodwill impairments. Specifically, it excludes a goodwill impairment expense of $284.7 MM in 2023. Without this adjustment, EBITDA reading is significantly worse (-249MM vs +21MM) and no margin expansion discussions make sense, as margin would be -381%.

However, it is common practice to use adjusted EBITDA and adjusted EBITDA margin to provide useful measures to investors to assess operating performance and to enable comparison with operational results of peers.

- Increase in the number of enterprise customers (those spending over $100K on the platform) by 5% quarter-over-quarter, the first such occurrence since 4Q. Currently 555 enterprise customers.

-The company is committed to limiting expenses in order to drive significant outperformance in the adj. EBITDA margin. This quarter, adj. EBITDA margin of 33% is 4.7% above last year’s margin rate. Definitive Health remains early in its lifecycle and should have a long path of double-digit top line growth and margin expansion.

Current remaining performance obligations stabilizing

As mentioned by the company leadership during the same call, one of the best forward growth indicators for DH is CRPOs, or current remaining performance obligations. CRPO is a financial metric used in accounting for companies that deal with long-term contracts and subscriptions. It represents the aggregate amount of revenue from existing contracts, that a company expects to recognize in the future for performance obligations that are unsatisfied or partially satisfied (thus not yet recognized as revenue). It gives investors and analysts an idea of the company’s future revenue streams.

An increase in CRPOs might indicate a growing backlog of contracted work or services, or a strong demand for the company's products or services, potentially leading to future revenue, which could be seen as a positive sign. However, excessively high CRPOs might also indicate challenges in meeting those obligations or potential strain on resources.

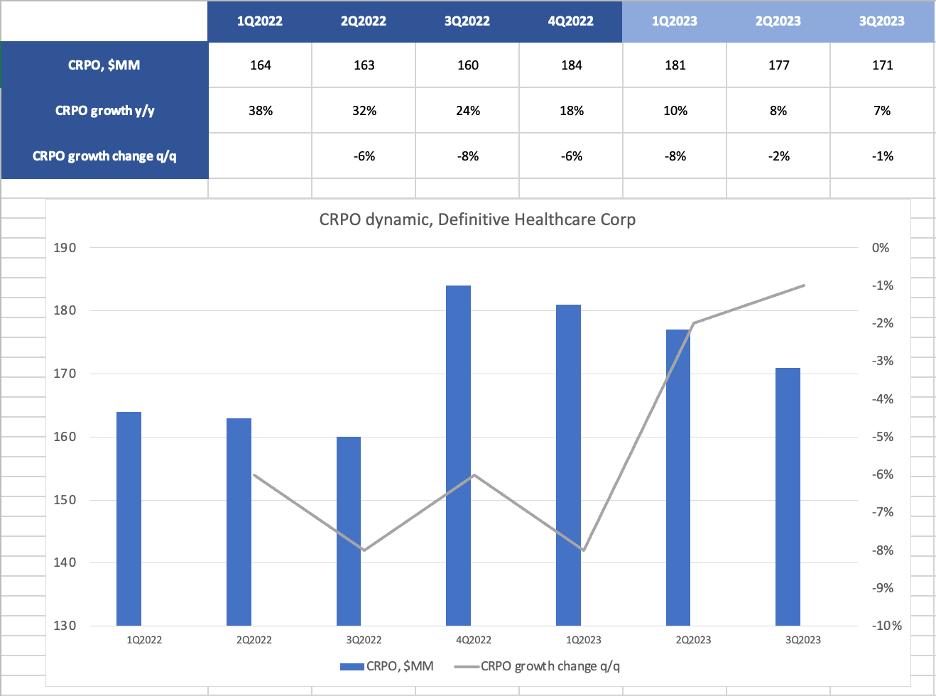

Let’s break down the CRPO dynamic for the last 2 years - refer to the image below to illustrate the following paragraph.

Current remaining performance obligations at DH Corp are growing in the high-single digit range, 7-8% per year. A year ago, they were growing at a much higher rate of 24% but rapidly declining, at a rate of roughly -7% per quarter. The deceleration in the rate of growth has slowed down this year from -7% to only -1.2% and stabilized over the last 6 months. Since the CPROs are now growing at the mid-single digit rate of about 7 or 8%, this indicates a more controlled contract renewal rate, and likely reflects the fact that the remaining customers, who have not churned out during the past year or two, are more resilient and likely to view DH service as less discretionary and more critical to their business. These two factors together suggest a more predictable and stable trajectory for revenues going forward.

{kind=link}

YCharts, authors calculations

Based on these factors, the following valuation / price objective may be appropriate:

Price Objective

Given that the EBITDA margin and growth trajectory of DH is in-line with the median healthcare IT and enterprise software EBITDA growth for 2024, we can use the peers’ averages for valuation.

| DH Corp |

| Healthcare IT peers |

| Enterprise software peers |

| Adjusted EBITDA margin ((AVG)) |

| 27.4% |

| 25.5% |

| 40% |

| Adjusted EBITDA growth rate |

| 15.1% |

| 14% |

| 11% |

| EV/EBITDA multiple |

| 11-12x, lower than peers warrants 14-16x, given faster revenue growth and growing EBITDA margins |

| 13.8x |

| 12x |

Source: FactSet

The Healthcare IT peer group has an avg EV/EBITDA valuation multiple of 13x-14x for calendar year 2024. DH trades at a lower multiple (11-12x EV/EBITDA) and we believe, warrants a slight premium to this multiple, at 16x, given faster revenue growth and higher EBITDA margins.

In Healthcare IT, as mentioned earlier, DH’s closest peers are Doximity ((DOCS)) and HealthEquity ((HQY)). Doximity has better margins and similar growth and trades 16-17x EBITDA while HealthEquity has better growth and slightly higher margins and trades at 15-16x EBITDA. While HealthEquity’s growth rates are better, the business is more cyclical and more mature than Definitive Health. Versus this peer group, a 16x EV/EBITDA multiple seems reasonable.

The multiple of 16x EV/EBITDA would give DH the fair price of around $9.0 up from the current price of about $7.18.

Upside and downside risk factors

One potential upside to company growth lies in the growth of the subscription base, both through new contracts and the retention of existing clients. That, alongside improving macroeconomic conditions, which could bolster the budgets of smaller healthcare companies, would strengthen DH’s position in achieving growth and revenue targets.

Downside Factors

Adverse factors that could impede the achievement of the projected outcomes involve higher-than-expected customer churn rates, extended sales cycles, and increased competitive pressure from other players in commercial intelligence. Additionally, uncertainties in the macroeconomic environment might compel smaller clients to divert their budgets away from the services provided by DH, posing a potential risk to projected outcomes.

Conclusion

Since the growth projections are realistic, despite the company facing challenges with client attrition and closing new contacts, the current valuation clearly presents an investment opportunity. On top of that, the management’s focus on cost efficiency, margin expansion, engaging existing clients by providing more guidance on how to effectively utilize DH’s data intelligence, are all strong factors that characterize this stock favorably.

For further details see:

Definitive Healthcare: Undervalued Vs. Peers Given Revenue Growth And Margin Expansion