DKL - Delek Logistics: Great Distribution Growth But There Are Better Options

2023-10-18 15:43:03 ET

Summary

- Delek Logistics has a great track record increasing its distribution.

- However, it has higher than peer leverage and it's not generating any excess cash after distributions.

- There are better values in the midstream space.

Delek Logistics ( DKL ) has a strong track record of raising its distribution quarter over quarter, but there are better midstream options out there.

Company Profile

DKL is an integrated midstream company that primarily operates in the Permian and Delaware Basins and other select areas in the Gulf Coast region. Its parent company is refiner Delek US Holdings (DK), which owns a 78.8% interest in the partnership.

The company operates in four segments. Its Gathering & Processing segment is its largest and consists of crude gathering systems in the Midland and Delaware basins, as well as over 800 miles of crude and product transportation pipelines. Its Marketing & Terminalling segment, meanwhile, has 10 light product terminals as well as a wholesale and marketing business in Texas, while its Storage and Transportation segment encompasses storage facilities with 10 million barrels of capacity and rail offloading facilities. Finally, the company has three pipeline joint ventures.

Opportunities & Risks

One of DKL’s biggest opportunities is growth around the Delaware Permian, the most prolific oil basin the U.S. The company has been working to diversify away from its parent company, and on that end it has done a good job. Its Gathering and Processing revenue has gone from 30% being from third parties in Q2 of 2022 to 47% in Q2 of 2023.

Its Midland Gathering System has been seeing very strong growth, and then it supplemented that through the purchase of the midstream assets of 3Bear Energy in the Northern Delaware Basin. The assets obtained in the deal included 485 miles of pipelines, 88 million cubic feet per day of cryogenic natural gas processing capacity, 120 MBbl of crude storage capacity, and 200 MBbl/d of water disposal capacity. It also came with ~350,000 acreage dedication and long-term fixed fee contracts. DLK laid out $624.7 million in cash in the deal, paying an expected 6.25x multiple based on 2023 EBITDA estimates at the time.

Volumes on its Midland Gathering System, meanwhile, more than doubled year over year in Q2, while its Delaware Gathering System, formerly the 3Bear assets, were expected to exceed a $100 million EBITDA run rate in Q4.

Discussing its Delaware Permian assets earlier this year , CEO Avigal Soreq said:

“So the [Midland Gathering System] is extremely a good asset. We are very pleased versus what we are seeing. I'm not going to give you a specific number for 2023, but I'm going to give you some highlights around the assets. We do have 325,000 acreage with a line in sight for more. But just organically, we see an increase. Just talking to producers it is a very nice percentage, we’ll exceed the rest of the Permian. We have 25 rigs on that acreage, which is very nice and a prolific number versus the rest of the basin. And we expect it to be very nice growth, we’ll exceed the average of the market during the year, during the rest of the year. … But that asset and that rock is extremely well, and we are very fortunate with that asset and that investment. Around 3 Bear, on the script it was very clear. We see the integration phase complete. We actually changed the name to Delaware Gathering System to reflect that completion of the integration. And we are well positioned to continue the trend to hit our target. So that this is as simple as it could be.”

DKL has been pretty aggressive in raising its distribution, increasing it sequentially for 42 straight quarters.

Nearly 80% of its gross margins are underpinned by MVCs, so it has a pretty clear visibility. However, 55% of that are contracts that will expire within the next year, so that is a risk moving forward.

In addition, the company carries a pretty high amount of leverage at nearly 4.7x. Most midstream companies have settled into leverage of between 3-4x, so DKL’s leverage is higher than most peers. About 46% of its debt is variable, which is a risk in a rising rate environment, and it has nearly $550 million in debt that needs to be refinanced in 2024 and 2025, which likely will be at higher rates.

The majority of its margins also stem from systems that support the Tyler, El Dorado and Big Spring refineries located in Arkansas and Texas. To the extent that there is less refined product demand in the future that impacts these refineries, it would impact DKL.

And while DKL is primarily fee based, it does have some wholesale fuel sales that it makes to third parties. These margins on these sales can move up or down, impacting the company’s results.

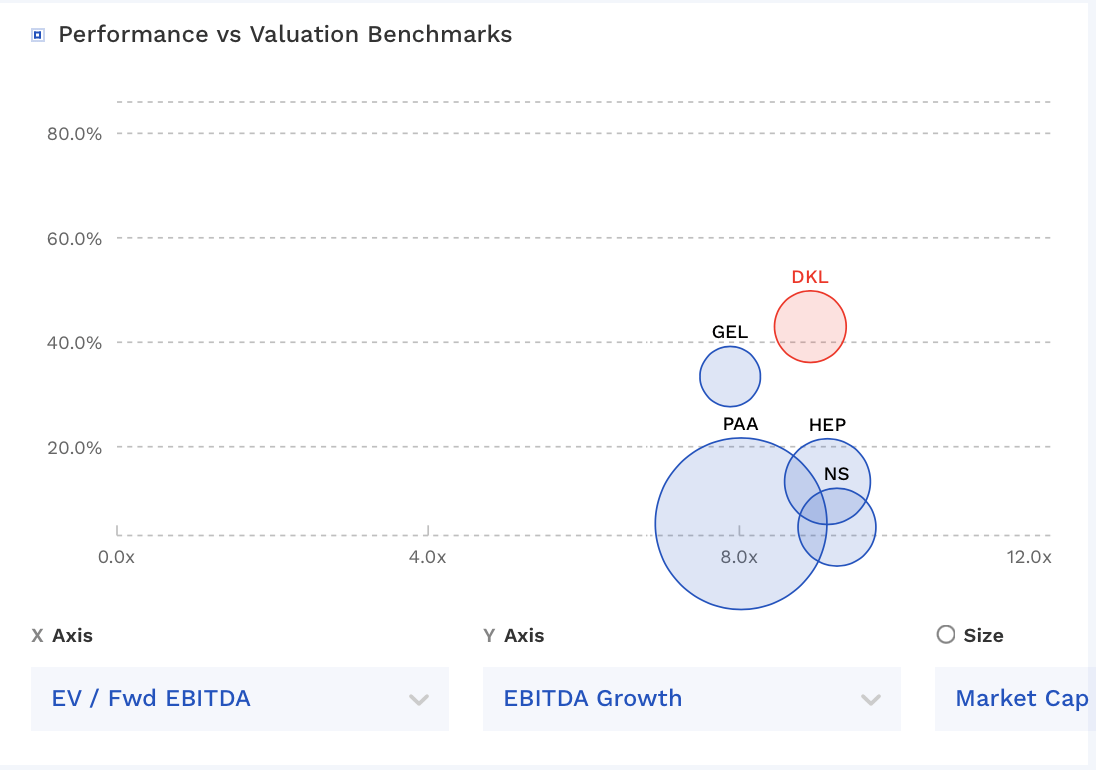

Valuation

Looking at valuation, DKL trades at 8.9x the 2023 EBITDA consensus of $382.0 million. For 2024, it trades at 8.3x the 2024 EBITDA consensus of $409.3 million.

The stock has a yield of about 9.6%. It has a coverage ratio of about 1.34x as of last quarter.

The stock trades in the middle range of valuation compared to its crude-focused midstream peers.

While the company carries a nice 1.34 coverage ratio based on its distributable cash flow, after paying distributions and growth capex, it’s seeing cash outflows. Most midstream companies are now more conscious of this and try to have excess cash after capex and distribution. Through the first six months of the year, FCF after distributions is around -$81 million, and after making some adjustments it would still be around -$22 million.

Given this dynamic, it will be difficult for DLK to lower its already higher leverage. Higher rates on its variable debt are also not helping, with its interest expense nearly doubling year over year. Taken altogether, I don't think the stock should trade at a valuation similar to peers with better balance sheets and FCF metrics.

DKL Valuation Vs Peers (FinBox)

{kind=link}

Conclusion

While investors will be undoubtedly be intrigued by the consistent distribution growth from DKL and the nice growth out of the Permian, I think there are better options in the midstream space. There are also a couple things that I don’t love about the stock. One is that the company carries higher leverage than most its peers. Most midstream companies have fixed their balance sheets over the last several years, and most now carry under 4x leverage. So on that end, DLK is not as attractive. I also don't like how the company is not FCF positive after distributions. Combined, that's not a good combination in my book.

Given DLK’s characteristics compared to other midstream companies at a similar or higher valuation, I’m largely neutral on the name. For more crude-oriented names, I prefer Plains All American ( PAA ), which I last wrote up here .

For further details see:

Delek Logistics: Great Distribution Growth, But There Are Better Options