RYDAF - Delek Logistics Partners: An 8.30%-Yielder That Is Worthy Of Consideration

Summary

- Delek Logistics Partners, LP is a midstream company that primarily provides services to Delek US Holdings.

- The partnership has remarkably stable cash flows and has grown its EBITDA in each of the past seven years.

- The partnership acquired 3Bear last year, which reduces its reliance on Delek as a source of revenue.

- Delek Logistics Partners has more leverage than I really like to see, but it is really not that bad.

- The 8.30% yield is sustainable and the company constantly increases it, helping to overcome inflation.

Delek Logistics Partners, LP ( DKL ) is a midstream drop-down master limited partnership that primarily operates to support the operations of refining and downstream giant Delek US Holdings, Inc. ( DK ). Drop-down partnerships used to be fairly common in the energy sector, as they provide a way for a larger energy company to recoup their capital expenditures incurred in the construction of midstream assets while still retaining most of the cash flows. However, these entities have become much less common since the pandemic-related lockdowns, and now Delek Logistics Partners is one of the few that are left.

The company's business model is very similar to that of other midstream companies, which is nice because of the characteristics that it possesses. In particular, the company has remarkably stable cash flows, which allows it to pay out an attractive 8.30% forward distribution yield. The company also has some growth prospects, which may actually be strengthened somewhat given the growing demand for fuel, which I discussed in a few recent articles (see here and here ). The company still has reasonable prospects even in the absence of growth, which is likewise nice considering the hostility of the Federal Government to new pipeline construction right now.

Overall, Delek Logistics Partners looks like it could be a reasonable company to include in an energy income portfolio, but let us research it further in an effort to verify that.

About Delek Logistics Partners

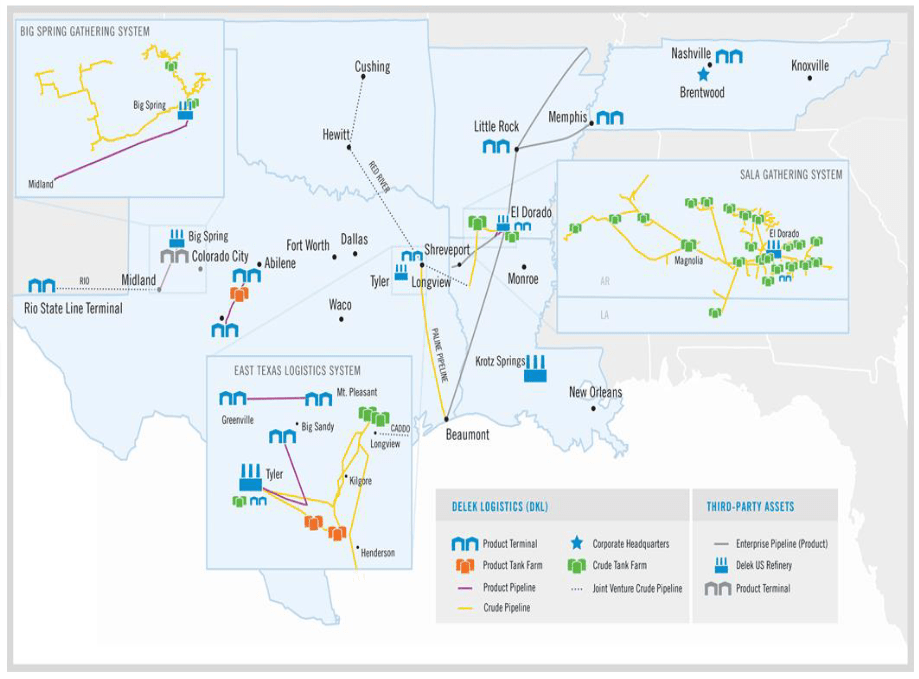

As stated in the introduction, Delek Logistics Partners is a drop-down master limited partnership ("MLP") that operates a fairly extensive network of midstream assets throughout Texas and the surrounding states:

{kind=link}

In total, the company has 805 miles of crude oil and refined products pipelines, a 600-mile crude oil gathering system in Arkansas, a 200-mile gathering system in the Permian Basin, and ten million barrels of crude oil storage capacity. Admittedly, this is nowhere near the size of a giant midstream partnership like Energy Transfer LP ( ET ), but it is still nothing to sneeze at.

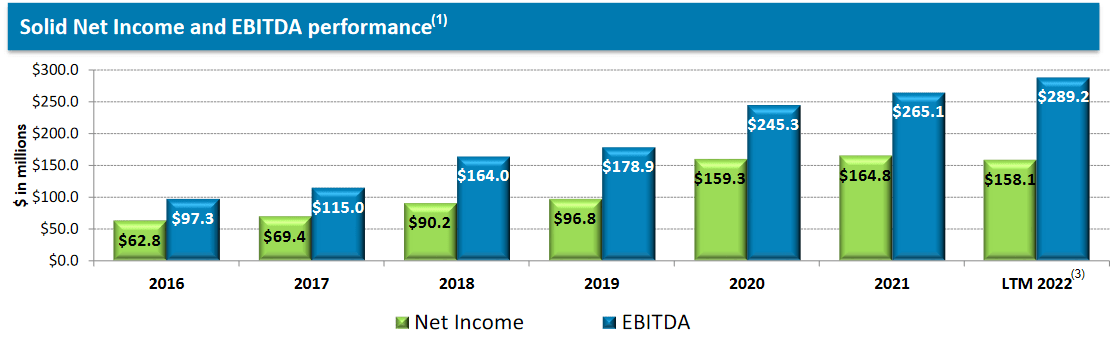

However, the size of the company is not necessarily relevant, since it still boasts many of the characteristics that we typically appreciate with midstream companies. Perhaps the most important of these is that the company has fairly stable cash flows over time. As we can see here, the company has managed to increase its EBITDA in each of the past seven years with no down year:

{kind=link}

The company's net income varied a little bit, but generally, it showed the same trend. As I have pointed out in the past, though, net income is not really a good measurement of performance for a midstream company because they have high expenses related to depreciation and other things that affect net income but do not actually represent cash coming into or leaving the business. EBITDA and Distributable Cash Flow are the relevant metrics that we use to measure the financial performance of a midstream partnership like Delek Logistics Partners. As we can see here, the company's distributable cash flow has also consistently increased over the same time period without a single down year:

Delek Logistics Partners

The fact that Delek Logistics Partners, LP managed to increase its EBITDA and distributable cash flow in 2020 despite the fact that energy prices collapsed is certainly something that anyone will notice. This is a hallmark of the company's business model. Delek Logistics Partners enters into long-term (usually ten years or longer) contracts with its customers under which the customer sends resources through the partnership's infrastructure. Delek Logistics Partners bills the customer based on the volume of resources that are handled by its infrastructure, not on their value. This provides the company with a great deal of insulation against fluctuations in energy prices. We can certainly see this in the two above charts, as crude oil prices varied substantially over the 2016 to 2022 period, yet the company's cash flows were pretty much immune to these fluctuations.

At this point, there may be some readers that point out that the production of crude oil tends to decline during periods of low prices. This is actually pretty common in America's various shale plays because the production can be ramped up or decreased very quickly. We saw this happen in response to the pandemic-related lockdowns and it is one reason why energy production during the first half of 2021 was a lot lower than it was in 2019. As Delek Logistics Partners uses a volume-based business model, we would expect this to decrease the company's cash flows.

However, the partnership has a way to protect itself against this, which is one of the reasons why we did not see the decline that would otherwise be expected. In short, its contracts with its customers contain minimum volume commitments. These clauses specify a certain minimum volume of resources that the customer must send through the partnership's infrastructure or pay for anyway. Therefore, these contractual clauses effectively create a floor that the company's cash flows cannot decline beyond. This is very nice because it provides the company with a stable source of cash flow that it can use to pay the distribution. As of the third-quarter 2022, which is the most recent quarter that the company has reported, these commitments accounted for 67% of the company's gross margin (a similar metric to gross profit):

Delek Logistics Partners

Admittedly, the 67% figure may not sound particularly impressive. After all, that would still represent a fairly significant decrease if all the company's customers were to cut their throughput down to the minimum. However, this has never happened, even through two energy bear markets that occurred over the company's history. As I pointed out in a recent blog post , it is quite unlikely that we will experience another energy market as weak as 2015 or 2020. Thus, it seems pretty unlikely that we will have to worry about the company's customers reducing their transported volumes too much. Overall, it seems that the company's finances should remain fairly stable even in a worst-case scenario.

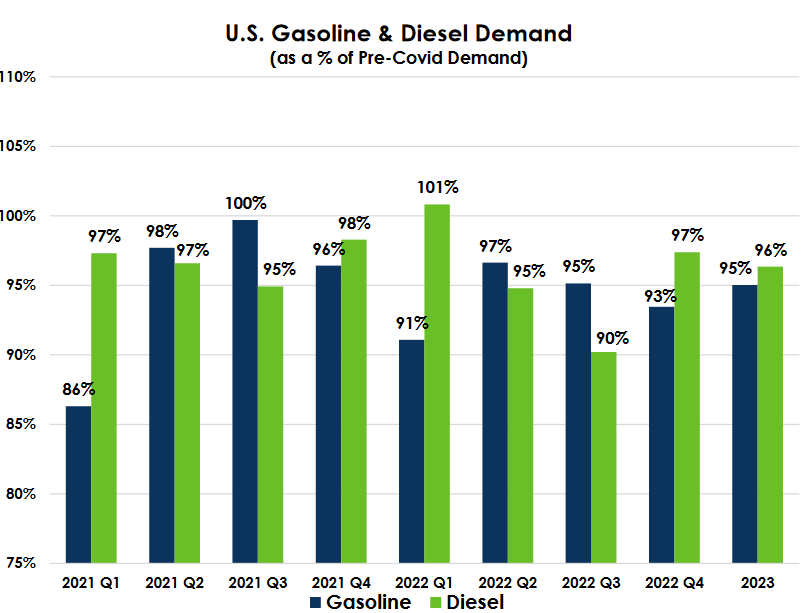

Naturally, as investors, we like to see more than just stability. We like to see growth. This is true for Delek Logistics Partners even though the company's yield is sufficient that we do not really need much growth in order to get an acceptable return. As a drop-down master limited partnership, the company's usual method for generating growth is to purchase midstream assets from Delek US Holdings. The basic point of this is for Delek to get back the money that it spent constructing the assets via the purchase price while still retaining a significant amount of the cash flows due to its ownership position in Delek Logistics Partners. However, Delek itself has not been constructing an enormous amount of midstream assets in recent years. The pandemic was one reason for that. As we can see here, the demand for fuel remains slightly lower than it did back in 2019:

{kind=link}

One obvious reason for this is that many businesses continue to allow or even promote remote work, which reduces the amount of driving that they need to do for business or commuting to their offices. Another reason why the demand for fuel remains lower than prior to the pandemic is that gasoline and diesel prices have been substantially above 2019 levels for the past eighteen months. People tend to reduce their driving when gasoline prices climb for obvious reasons. Anecdotally, my household has been ordering much of what we need so that we can limit our driving to grocery shopping. I am certain that many other households are doing the same thing. As a result of this stagnant demand, Delek has had no reason to increase the amount of crude oil flowing to its refineries or refined products flowing out. Thus, there is little need to construct new infrastructure. The last time that Delek Logistics Partners bought a dropdown asset from Delek US Holdings was in the first quarter of 2020. That shows just how little need there has been for new midstream assets.

That does not mean that Delek Logistics Partners has not had any growth. The company does have the ability to purchase assets from entities other than Delek US Holdings. In April 2022, Delek Logistics Partners announced the acquisition of 3Bear Delaware Holding, which was a midstream company operating in the Permian Basin in New Mexico.

Delek Logistics Partners

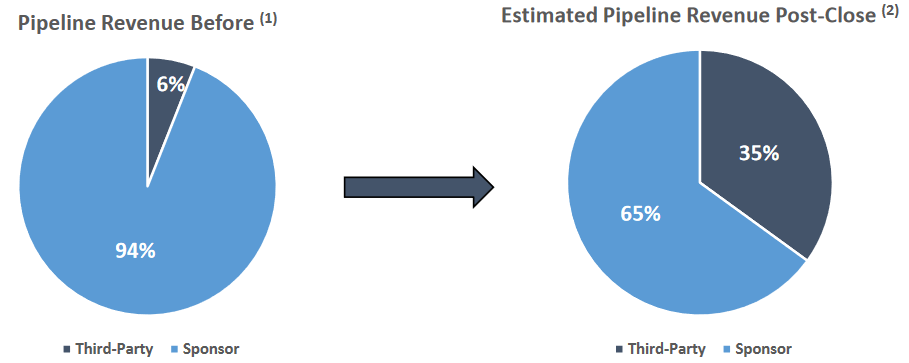

The acquisition, which closed in June, significantly increased Delek Logistics Partners' revenue that comes from customers other than Delek US Holdings. In fact, Delek accounted for 94% of the partnership's pipeline revenue prior to this acquisition. 3Bear had eighteen contractual customers that are now customers of Delek Logistics Partners. This reduced the company's revenue from Delek US to 65% of its total:

{kind=link}

This is a good thing for a number of reasons. The most important of these is that it is generally not a good idea for any company to be too dependent on a single customer for its revenue. This is because any financial problems suffered by that customer could then flow through to the company that depends on it. Ideally, we do not even want to see a single company accounting for 65% of the partnership's revenue but admittedly this is not unusual. For example, Rattler Midstream (RTLR) is highly dependent on Diamondback Energy ( FANG ), while Equitrans Midstream ( ETRN ) is highly dependent on EQT Corporation ( EQT ) for its revenue. Third-party business is always a good thing, though, and the fact that Delek Logistics Partners is reducing its reliance on Delek US Holdings is something that we should appreciate as investors.

Financial Considerations

It is always critical that we look at the way that a company finances itself before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. This is typically accomplished by issuing new debt and using the proceeds to repay the existing debt. As a result, a company's interest expenses may increase following the rollover depending on conditions in the market. This is something that is quite important to remember today as interest rates have been climbing fairly rapidly over the past year and will almost certainly continue on that trajectory for a while.

In addition to this risk, a company must make regular payments on its debt if it is to remain solvent. Thus, an event that causes a decline in cash flow may push a company into insolvency if it has too much debt. Although midstream companies like Delek Logistics Partners tend to have remarkably stable and recession-resistant cash flows, bankruptcies have occurred in the sector so this is still a risk that we should not ignore.

One metric that we can use to evaluate a company's financial structure is the net debt-to-equity ratio. This ratio tells us the degree to which a company is financing its operations with debt as opposed to wholly-owned funds. In addition, it tells us how well a company's equity will cover its debt obligations in the event of a liquidation or bankruptcy event, which is arguably more important.

As of September 30, 2022, Delek Logistics Partners had a net debt of $1.4534 billion compared to negative $114.3 million of shareholders' equity. This is not a particularly attractive scenario as it indicates that the company's liabilities exceed the value of its assets. The company would obviously not fare particularly well if its finances get stressed. Investopedia describes the risks of this situation thusly,

"Negative shareholders' equity could be a warning sign that a company is in financial distress or it could mean that a company has spent its retained earnings and any funds from stock issuance on reinvesting in the company by purchasing expensive property, plant, and equipment. In other words, negative shareholders' equity should tell an investor to dig deeper and explore the reasons for the negative balance."

Delek Logistics Partners is not alone among midstream companies in having negative shareholders' equity. As I pointed out in a previous article , Shell Midstream Partners had negative shareholders' equity back in 2019. Although that company no longer exists, it was able to carry its debt fairly successfully even through 2020. Although that company was ultimately completely purchased by Shell ( SHEL ), its financial structure was not the cause of its end as an independent company. Delek Logistics Partners' negative shareholders' equity comes mostly from the company reinvesting all of its funds from unit issuance on purchasing its assets that then had their value decline due to depreciation. By itself, this is not really a problem in this case.

Ultimately, the company's ability to carry its debt is more important than its financial structure. The usual way that we judge a midstream partnership's ability to carry its debt is by looking at its leverage ratio, which is also known as the net debt-to-EBITDA ratio. This ratio essentially tells us how long (in years) it would take the company to completely pay off its debt if it were to devote all of its pre-tax cash flow to that task. As of September 30, 2022, this ratio stood at 4.35x based on the company's trailing twelve-month EBITDA. This is reasonable as it is well below the 5.0x ratio that analysts generally consider to be sustainable and acceptable. However, the best midstream companies have managed to get this ratio below 4.0x over the past year or two if they were not at that level prior to the pandemic. That is also the level that I like to see because it adds a margin of safety to the investment.

Delek Logistics Partners' management has given no indication that it will attempt to reduce this ratio going forward, so this company is probably a bit riskier than our top picks here at Energy Profits in Dividends in terms of its leverage. However, it is by no means a poor choice as the leverage ratio is not really high per se.

Distribution Analysis

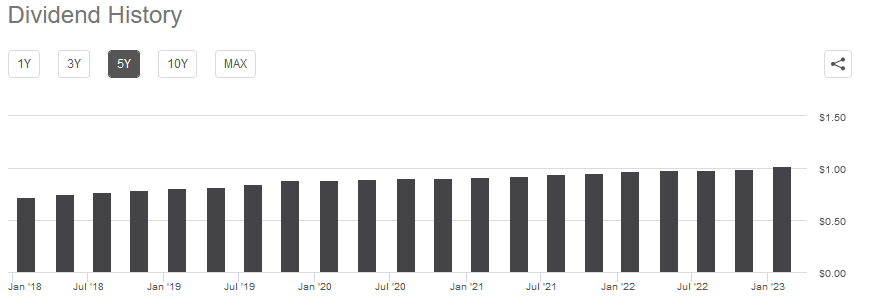

One of the biggest reasons why we purchase midstream companies like Delek Logistics Partners is the high distributions that they tend to pay out. Delek Logistics Partners, for its part, is certainly not an exception to this as the company yields an impressive 8.30% at the current price. Delek Logistics Partners also has a long history of steadily increasing its distribution at least annually (but usually a few times per year):

{kind=link}

The partnership's track record is much better than most other midstream partnerships in this respect. In particular, the company actually increased its distribution twice in 2020, which was a year that saw several peers reduce their payouts. The fact that the partnership is committed to growing its distribution is something that is very nice to see during inflationary periods like the one that we are in today. This is because inflation is constantly reducing the number of goods and services that we can purchase with the distribution that we receive from the company. The fact that the company pays out more money with the passage of time helps to offset this effect and maintains the purchasing power of the distribution.

As is always the case, it is important to ensure that the company can actually afford the distribution that it pays out. After all, we do not want to find ourselves the victims of a distribution cut since that would reduce our incomes and almost certainly cause the company's unit price to decline. The usual way that we judge a midstream company's ability to pay the distribution is by looking at its distributable cash flow. The distributable cash flow is a non-GAAP metric that theoretically tells us the amount of money that was generated by a company's ordinary operations and is available to be paid to the limited partners.

In the third quarter of 2022, Delek Logistics Partners reported a distributable cash flow of $65.639 million. That was sufficient to cover the distribution 1.62 times over. Analysts generally consider anything above 1.20x to be sustainable over the long term. I am, as usual, more conservative and like to see this ratio above 1.30x in order to add a margin of safety to the distribution. Clearly, Delek US Partners easily meets even my more stringent requirements. The company can probably sustain its distribution so there is nothing to worry about here.

Conclusion

In conclusion, Delek Logistics Partners, LP is a little-followed drop-down midstream master limited partnership that has some potential to play a role in any income portfolio. Delek Logistics Partners, LP's history of consistent distribution growth is particularly nice to see, particularly since it does not appear to be having any difficulty maintaining it. The firm's leverage is admittedly a bit higher than we like to see, but it is not out of line with some of its peers and it should be able to carry the debt given its cash flows. Overall, Delek Logistics Partners, LP is an 8.30% yielder that is worth consideration.

For further details see:

Delek Logistics Partners: An 8.30%-Yielder That Is Worthy Of Consideration