DKL - Delek Logistics Partners LP Curiouser And Curiouser!

2023-12-30 22:05:20 ET

Summary

- Delek Logistics Partners, LP was benefitting in June from record-breaking oil production, but the share price of Delek Logistics dived since then.

- The company's primary source of income comes from its storage and transportation segment, which operates pipelines, tanks, and offloading facilities.

- Delek Logistics is financially curious to us. Its debt, low gross profit margin, little cash flow from operations, and extraordinarily high dividend payout ratio and yield undergird our Sell assessment.

Red Flag

Delek Logistics Partners, LP (DKL) appears, at first blush, to be an attractive investment opportunity. The U.S. oil and gas energy industry is flourishing . Concomitantly, the Delek share price is down YTD and over the last 12 months. In our opinion, management is not reinvesting enough money in expansion for growth; they are missing an opportunity to capitalize on a national and global recommitment to the exploration and production of oil and gas. Too much cash is being distributed through dividend payouts primarily to other corporations that own ~80% of the outstanding shares.

The share price is a fair value based on P/E and earnings but momentum and growth opportunities are limited. We do not foresee circumstances for the price to move much higher shortly. The risks outweigh the rewards for retail value investors. We rate the stock as a Sell at this time.

Delek Logistics Partners, LP now sports a market cap of $1.86B. It has a P/E of 12.88. Short interest is at a minimal 1.23%. Yet, we are uncomfortable with retail value investors owning a stock with the dividend payout ratio and yield being extraordinarily high. Delek Logistics' dividend payout ratio is over 120% and the dividend yield nears 10%.

The average dividend payout ratio of 101 companies in the oil and gas services and equipment business is 17.58% and the average dividend yield is 1.98%. Delek Logistics gets a D- Factor Grade from Seeking Alpha for profitability. It appears to us that Delek Logistics' treasure is possibly being drained for purposes other than business growth or CAPEX plans. The company's share price is already expensive with a P/E GAAP of 12.82 ( FWD ) compared to the sector median of 10.49. We have seen reports of other analysts maintaining the gap is wider, 12.6x to 8.1x of peers.

Industry and Company Profile

Delek is in the U.S. oil storage and transport business. According to CNN’s report from S&P Global Commodity Insights :

((T))he United States is pumping oil at a blistering pace and is on track to produce more oil than any country has in history… a global record of 13.3 million barrels per day of crude and condensate during the fourth quarter of this year… America is exporting the same amount of crude oil, refined product and natural gas liquids as Saudi Arabia or Russia produces, S&P said.

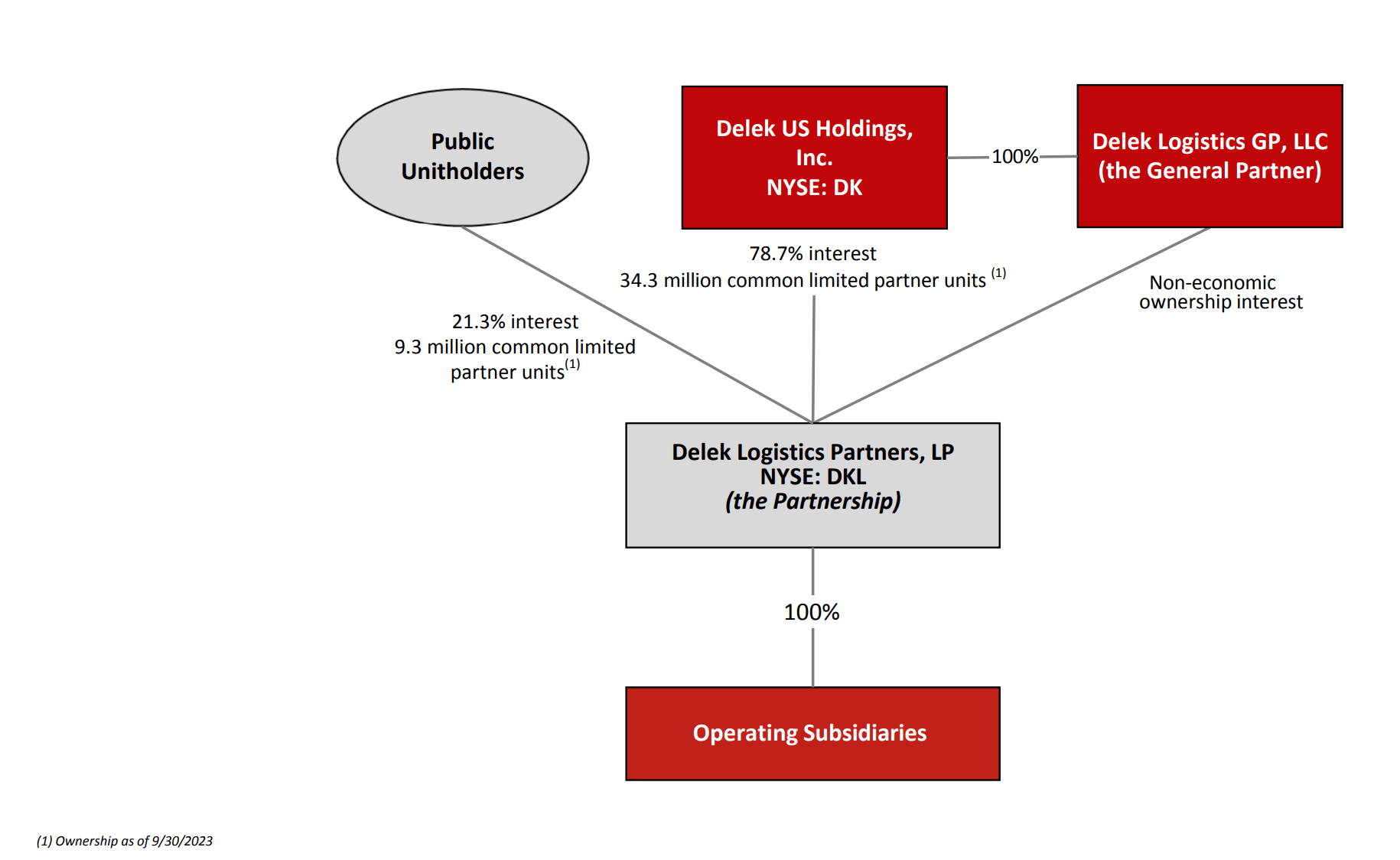

Delek Logistics GP, LLC acts as the general partner of the company. Delek Logistics Partners, LP operates through four segments: Gathering and Processing, Wholesale Marketing and Terminal transfers, Storage and Transportation, and Investment in Pipeline Joint Ventures. The Storage and Transportation segment is the company's primary source of income. It operates pipelines, tanks, and offloading facilities of crude oil and natural gas for processing, water disposal and recycling, storage services, and crude oil transportation. Products are sold to third parties and transported from terminals through pipelines in Texas, Tennessee, Arkansas, and Oklahoma.

The Storage and Transportation segment operates holding tanks, offloading facilities, trucks, and ancillary assets. Investments in Pipeline Joint Ventures own a portion of three joint ventures that have constructed separate crude oil pipeline systems and related ancillary assets servicing third parties primarily in the Permian Basin and Gulf Coast regions.

Delek Logistics Partners, LP was incorporated a decade ago. The company is linked to Delek Group Ltd. ( DELKY ), controlled by Yitzhak Tshuva. His real estate and energy conglomerate floated the IPO of Delek Logistics Partners LP, a wholly-owned subsidiary in 2012 of Delek US Holdings, Inc. ( DK ), on the New York Stock Exchange.

Business Management Map (Delek Logistics Slides)

{kind=link}

Ownership and Financials

A worrisome factor for us contributing to our investment assessment is nearly 80% of the shares are owned by other public companies. Insiders own 1%. The public owns ~9% of outstanding shares. Institutions own 11.3% of the shares. Since March ’23, corporate insiders sold more shares than they bought; they sold $17K in the last 3 months.

Highlights of the Q3 ’23 company earnings report reflect the upturn in America’s oil and gas production and sales: the company's $0.80 EPS beat estimates by $0.02, revenue of $275.82M beat estimates by +$14M but revenue in Q3 ’23 was lower than Q3 ’22. Net income from all segments was $34.8M and Q3 EBITDA was a record high of $98.2M. Management took particular note in the transcript of the meeting released on Seeking Alpha that Q3 '23 represents "43 consecutive quarters of distribution growth with a recent increase to $1.045/unit."

We would like to see substantial reinvestment in expansion and growth on the part of Delek Logistics to pump up the share price; it is down -7% YTD and about -10% for the last year. Meanwhile, the SPDR® S&P Oil & Gas Equipment & Services ETF ( XES ) share price is up 13.4% YTD and +11.3% for the year. The SA Quant Rating for the ETF is Buy. We believe the ETF selling at ~$85 per share, down from its 52-week high over $100 each, is a better opportunity for retail value investors than Delek Logistics at this time.

In our opinion, Delek Logistics has been benefitting from being at the right place at the right time operating in the right industry. But the share price does not reflect the good times in the oil/gas energy services business. And if not now, when?

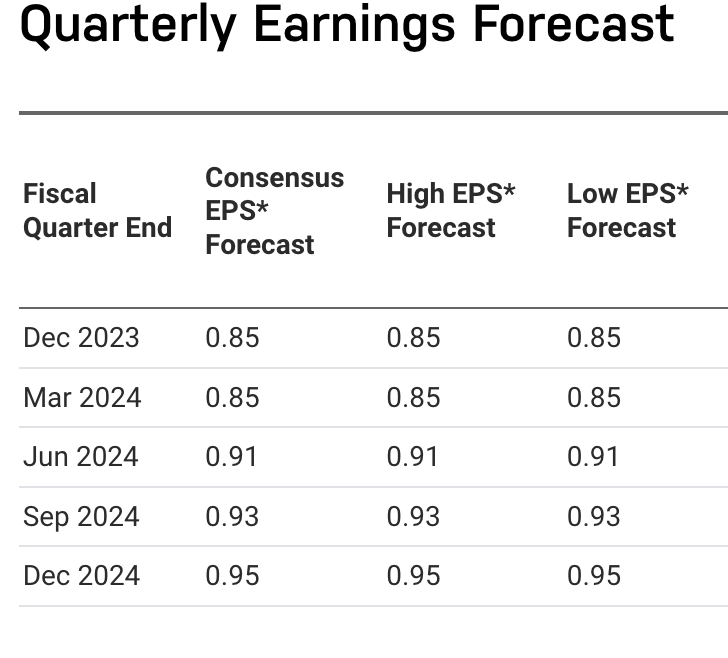

Looking forward, the consensus reported by NASDAQ.com is, and we concur, that the EPS will slip about 9% to ~$0.91 from $0.98 Y/Y. We estimate that Q4 ’23 EPS will not top $0.85. The company reported lower-than-estimated EPS in 6 of the last 9 quarters. Perhaps that is why insiders have been predominantly selling shares more than buying over the last 3 months; 2 of the 3 hedge funds that owned the stock sold out before the share price dived from $57.82 in June '23 to $42.48 after Christmas. We expect the next earnings report on or about February 21, 2024.

{kind=link}

Good Valuation Grade, Low Volatility, Shaky Dividend

The consensus among 9 Wall Street analysts Seeking Alpha surveyed rates Delek a Hold to Strong Buy. 4 others lean to Sell to Strong Sell. However, SA recently issued a warning to investors that the stock is at high risk of performing badly because “The company has Levered FCF Margin ((TTM)) of -18.89% while the Energy sector median is 5.81%.”

Cash from Operations stands at $5.3M versus the sector median of $7127.59M. The stock gets an F Factor Grade for valuation metrics of price-to-cash flow and middling grades for price-to-sales (TTM and FWD). A primary drawback to higher profitability is the low gross profit margin of almost 35% compared to +47% for the energy sector median.

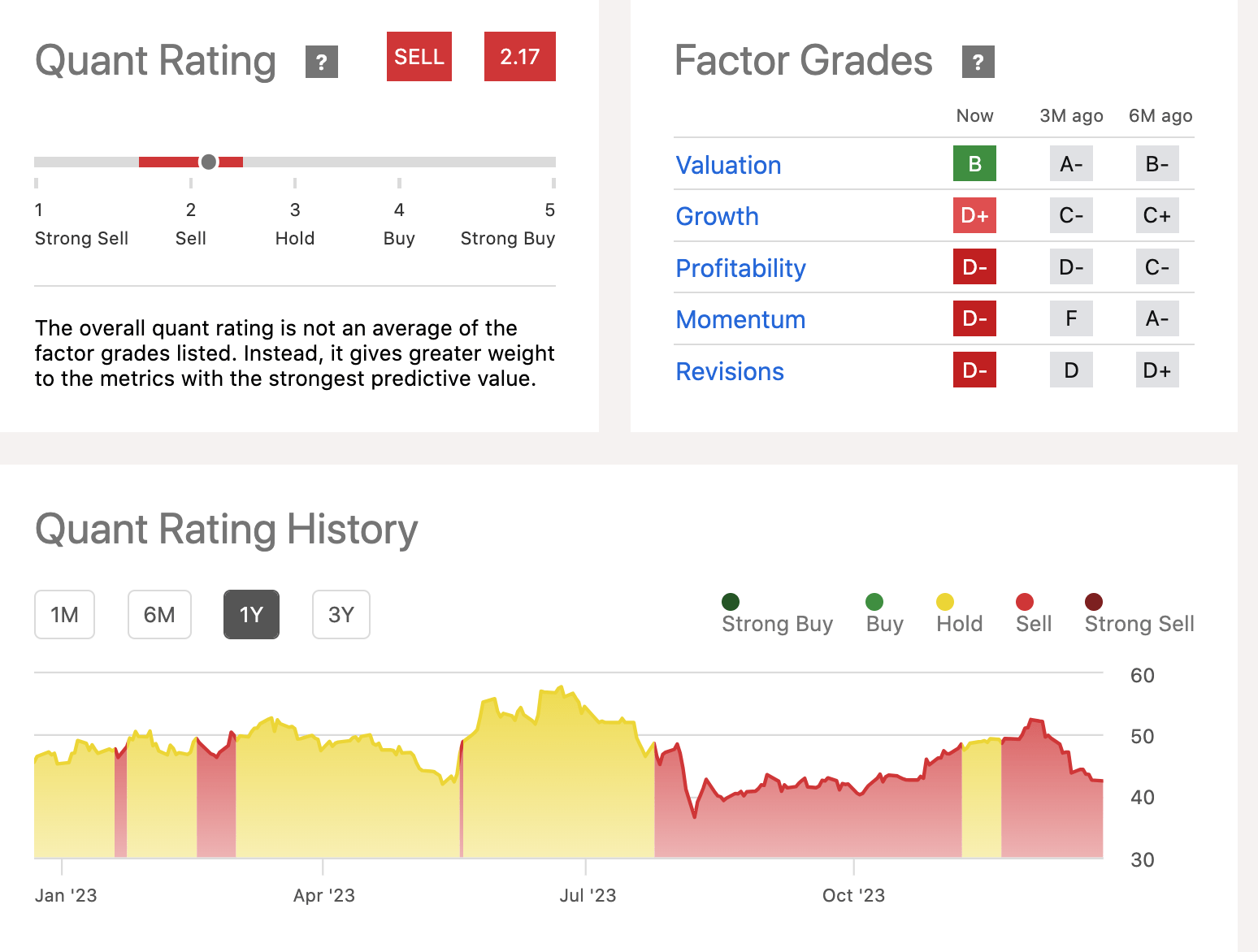

The SA Quant Rating has not painted a pretty picture for Delek Logistics this past year:

Quant Rating & Factor Grades (Seeking Alpha)

{kind=link}

Two positive factors that can entice retail value investors are the stock’s Levered/Unlevered Beta at 0.26, suggesting the shares are significantly less volatile than the market. Second, Delek Logistics offers a big dividend yield ((FWD)) of 9.81%.

We are less certain the company will hold to its 122.4% dividend payout which certainly plays to the benefit of Delek U.S. Holdings. Additionally, the capital structure of Delek Logistics is shaky: total debt is $1.76B, and cash on hand and equivalents is a scant $4.18M. Added annual revenue growth of +8% will come in part from the 2022 acquisition of an oil and gas exploration company for $625M. Earnings and cash flow do not, in our opinion, cover the dividend yield or interest payments on the debt. Its debt-to-equity ratio is -1,251.5%, though short-term assets of $117.64M exceed liabilities totaling $85.36M.

Takeaway

Delek Logistics holds too much debt; its gross profit margin is too low, and cash flow from operations is low. The dividend payout ratio and dividend yield seem unjustified to us and are perhaps unsustainable. We do not see this stock as a positive opportunity for retail value investors. For the sake of transparency, we have to share that one analyst pegs Delek’s fair price valuation at +$54 each. We do not envision Delek Logistics as a path to compounding wealth in the long run for retail value investors. Risk takers can Hold on but we rate the stock a Sell opportunity while the oil industry is hot.

For further details see:

Delek Logistics Partners, LP Curiouser And Curiouser!