DKL - Delek US Holdings: Big Changes Could Be Coming In 2023 (Rating Downgrade)

Summary

- Delek US Holdings reinstated their dividends during 2022, before subsequently pushing them higher.

- After seeing booming cash flow performance in the second quarter, it was disappointing to see it slump during the third quarter due to inventory headwinds.

- Alas, this is simply par for the course in their inherently volatile industry and looking ahead, the more interesting news is their review of strategic options.

- I suspect this could focus on their midstream subsidiary, Delek Logistics Partners, possibly unlocking cash via divesting their remaining stake.

- Until more information comes to light on this potential big change, I believe that downgrading my rating to hold is now appropriate.

Introduction

When last reviewing Delek US Holdings ( DK ), shareholders had recently seen their dividends reinstated and as my previous article correctly predicted, more was coming with another increase subsequently following during the next quarter. Now that the calendar has flicked over to a new year, big changes could be coming in 2023 with management hiring advisors to review their strategic options.

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

{kind=link}

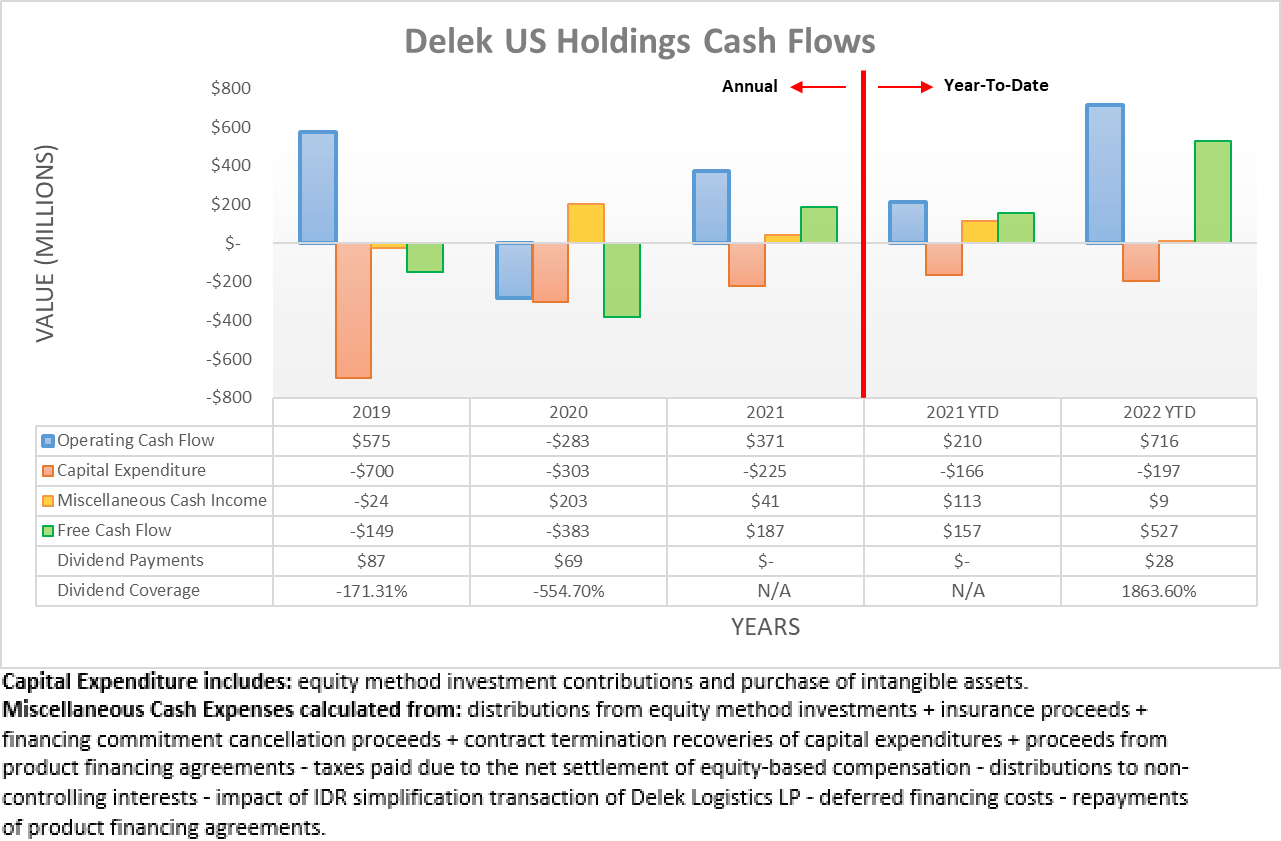

The inherent volatility of their cash flow performance was on full display during the third quarter of 2022 because after seeing their booming operating cash flow during the second quarter, it slumped during the third quarter. As a result of this sudden whipsaw, their operating cash flow during the first nine months only climbed modestly higher to $716m versus the previous $586m they had already generated during the first half. At least if nothing else, thanks to their modest capital expenditure, it was still sufficient to lift their free cash flow to $527m versus $463m across these same two periods of time, respectively. Plus, the resulting $64m during the third quarter alone had no issues providing very strong coverage to their dividend payments of $28m.

{kind=link}

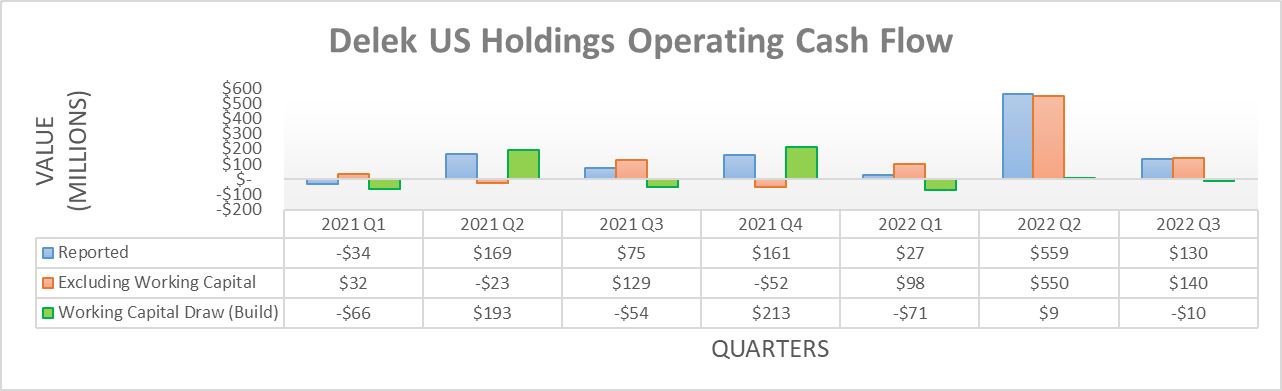

When viewed on a quarter-to-quarter basis, the dramatic change is more easily visible with their reported operating cash flow during the third quarter of 2022 crashing to $130m, which is a fraction of their previous result of $559m they generated only one quarter prior. Even if excluding their working capital movements, these underlying results were still not materially different at $140m and $550m, respectively. Quite disappointingly, it means their underlying result during the third quarter of $140m was also back around where it was one year prior at $129m.

Interestingly, this slump during the third quarter of 2022 extended into their accrual-based financial performance with their adjusted EBITDA landing at $135.8m, compared to $101.9m one year prior during the third quarter of 2021. When looking into their results, management attributed this slump during the former to $225.1m inventory headwinds, as per their third quarter of 2022 results announcement . Where their results for the recently ended fourth quarter of 2022 remain a mystery for another few weeks and more importantly, so too do their results for the year ahead as 2023 is likely to see another bumpy ride given the prospects of a recession on the horizon.

Even though nothing can be done to resolve the inherent volatility of their industry, at least their capital expenditure guidance for 2023 is not too high at circa $350m, which in turn should help produce free cash flow. Elsewhere, it seems their share buybacks are poised to ramp up higher than the mere $40m of share buybacks conducted during the third quarter of 2022, as per the commentary from management included below.

"With that said, going forward, we are looking to continue with the buyback aggressively well into 2023."

-Delek US Holdings Q3 2022 Conference Call.

When conducting the previous analysis, it outlined their new share buyback program that totals $400m and thus as only 10% was completed during the third quarter of 2022, it leaves $360m for the recently ended fourth quarter and further into 2023. They plan on conducting these "aggressively" and thus unless their cash flow performance rebounds much higher, they will likely consume most of their free cash flow, if not its entirety. Whilst I am not necessarily a fan of aggressive share buybacks for a volatile company, at least their lower outstanding share count should see their dividends pushed even higher in 2023 and beyond. Apart from this business-as-usual outlook, more interestingly, it seems that big changes could be coming given their decision to explore strategic options to unlock value, as per the commentary from management included below.

"We hired a head of corporate development and engaged banker to advise us on strategic options. We will communicate our plan to the market once complete."

- Delek US Holdings Q3 2022 Conference Call (previously linked) .

Whilst I do not wish to publish pure speculation, I nevertheless feel there is a strong possibility of their strategic options centering around their subsidiary, Delek Logistics Partners ( DKL ). As anyone following the midstream industry would have noticed in the last two years, there were many players either merging together, being acquired by a larger competitor or reacquired by their parent company. In my eyes, this places their subsidiary in the crosshairs and following their acquisition of 3Bear Energy that diversified Delek Logistics Partners, I would not be surprised to see their stake divested, thereby setting it free to operate completely on its own accord. This would also unlock cash for Delek US Holdings, plus also remove the consolidated debt of their subsidiary and overall, simplify their company. That said, it is too early to tell and in the meantime, if any readers are interested in the outlook for Delek Logistics Partners, please refer to my other article .

{kind=link}

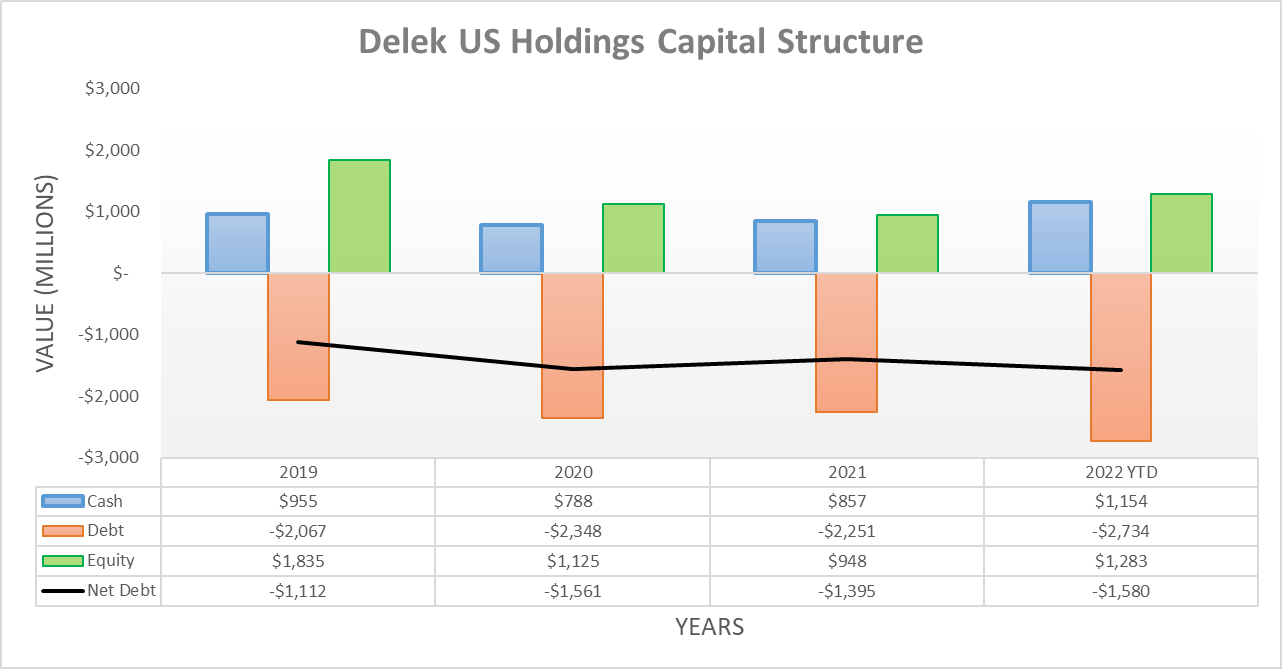

Following their net debt jumping higher during the second quarter of 2022 as they closed their 3Bear Energy acquisition, it was essentially flat during the third quarter, which ended with net debt of $1.58b versus the former that ended with net debt of $1.573b. As for the recently ended fourth quarter and going forwards into 2023, the inherent volatility of their cash flow performance makes it impossible to pinpoint where their net debt will land, although given their plans for aggressive share buybacks, it is difficult to imagine their net debt dropping to any material extent, unless they divest Delek Logistics Partners.

{kind=link}

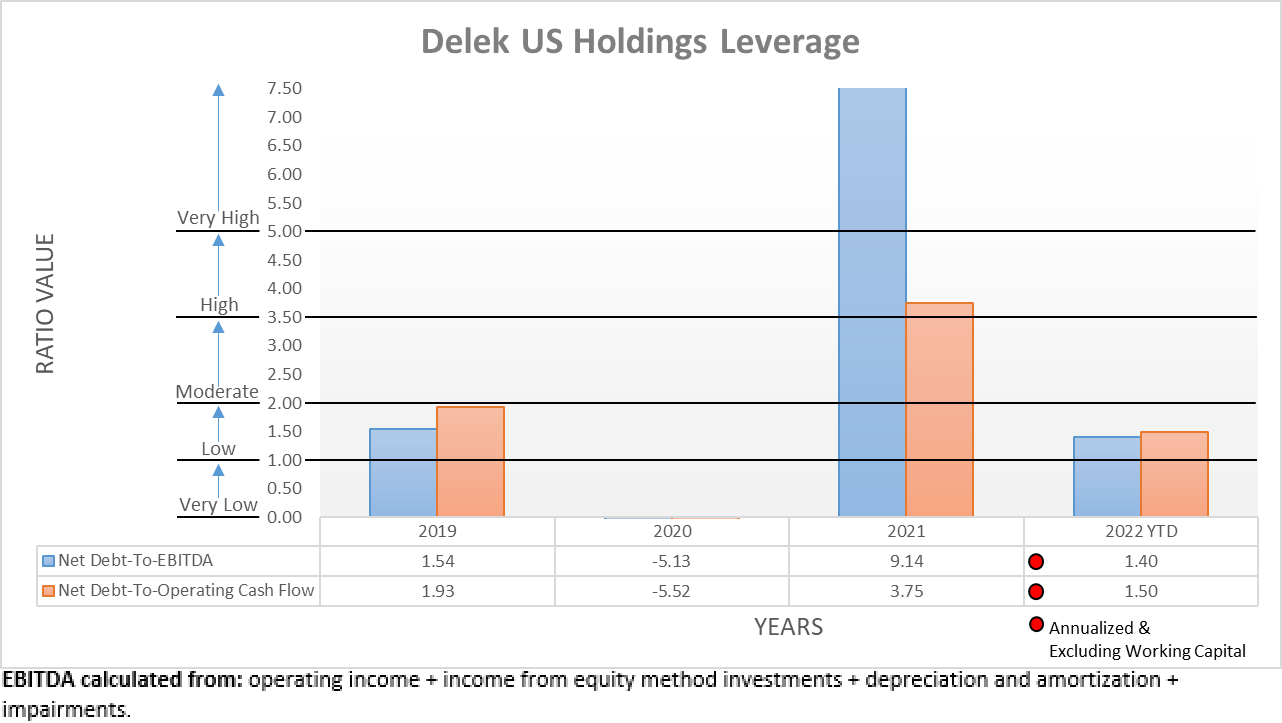

Since their financial performance softened during the third quarter of 2022 and their net debt remained essentially flat, it was not surprising to see higher leverage. As a result, their respective net debt-to-EBITDA and net debt-to-operating cash flow are now 1.40 and 1.50, which are both modestly above their previous respective results of 1.12 and 1.21 following the second quarter. That said, they remain around the middle of the low territory of between 1.01 and 2.00, which is quite handy because I suspect 2023 will see these rise given the aforementioned outlook for their net debt and the likelihood of softer operating conditions compared to their booming levels earlier in 2022. At least they are starting from a solid base and thus even if these were to double, it would not necessarily create unmanageable risks, nor significantly derail their shareholder returns.

{kind=link}

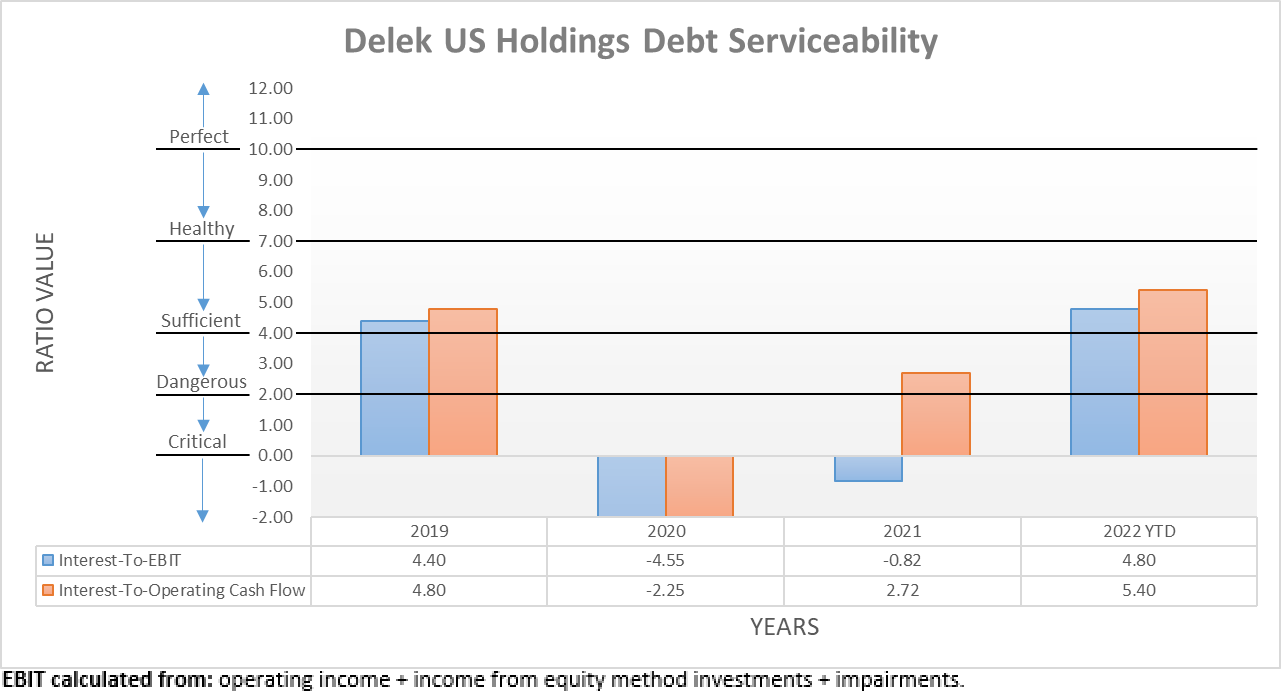

Similar to their leverage, their debt serviceability also took this same path during the third quarter of 2022, which is not surprising. To this point, their interest coverage when judged against their EBIT produces a result of 4.80, which is noticeably lower versus their previous result of 6.91 following the second quarter. Thankfully this remains healthy, which is also the case when their interest coverage is judged against their operating cash flow that produces a result of 5.40. Even if these were to slide lower during 2023 as their record-setting financial performance earlier in 2022 further dissipates, this solid base should at least see their results remain sufficient at 2.00 or above.

{kind=link}

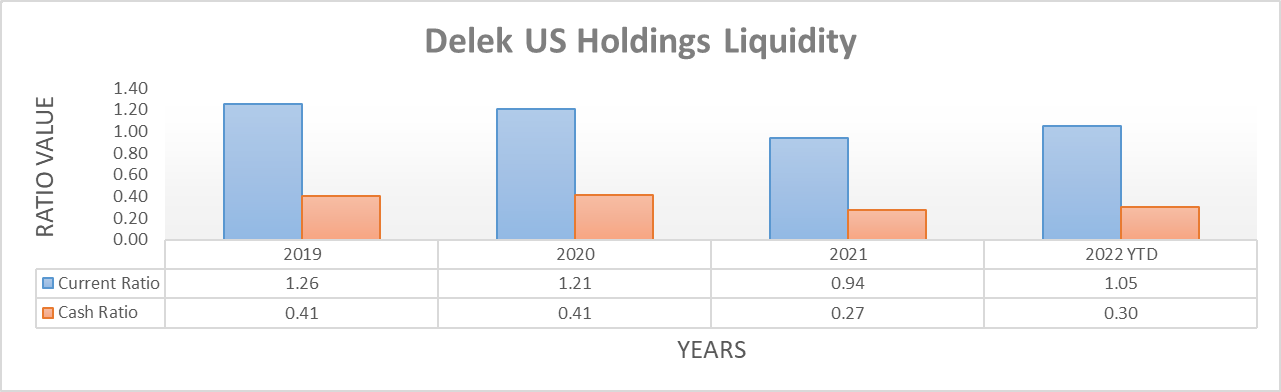

Unlike their leverage and debt serviceability, their strong liquidity was broadly unchanged during the third quarter of 2022, as evidenced by their respective current and cash ratios of 1.05 and 0.30, which are very similar to their previous respective results of 1.08 and 0.29 following the second quarter. If not for their sizeable cash balance, it would be concerning to see their credit facility maturing as soon as March 2023, although they have consistently avoided tapping this source of liquidity and thus it does not necessarily matter whether it is renewed. Excluding debt held by their Delek Logistics Partners subsidiary, the only debt hurdle on the horizon is not until 2025, when their large $1.234b term loan falls due in March and whilst this will require refinancing, they have plenty of time. If interested in the debt maturities held by their subsidiary, please refer to my other previously linked article.

Delek US Holdings Q3 2022 10-Q

Conclusion

In my eyes, aggressive share buybacks should foretell higher dividends as their outstanding share count sinks lower during 2023. Whilst positive, the inherent volatility of their industry will continue driving total returns for shareholders and given the gloomy economic outlook, it seems that if nothing else, a bumpy ride is ahead. More interestingly, it will be important to see what strategic options are highlighted and thus in light of this prevailing outlook, I now believe that downgrading to a hold rating is appropriate whilst sitting back and waiting to see what comes of this review.

Notes: Unless specified otherwise, all figures in this article were taken from Delek US Holdings' SEC filings , all calculated figures were performed by the author.

For further details see:

Delek US Holdings: Big Changes Could Be Coming In 2023 (Rating Downgrade)