DINO - Delek US Holdings: Company Delivers Strong Q1 Performance But May Not Last

2023-05-09 14:11:53 ET

Summary

- Delek US Holdings, Inc. reported very strong Q1 earnings results, driven by large crack spreads that caused significant cash flows.

- The demand for refined products is showing weakness and crack spreads are currently predicted to decline over the remainder of the year.

- This will pressure the company's margins and likely cause the remaining quarters of 2023 to be weaker than the most recent one.

- The company has improved its balance sheet significantly over the past few months.

- Delek US Holdings is currently trading for a reasonably attractive valuation.

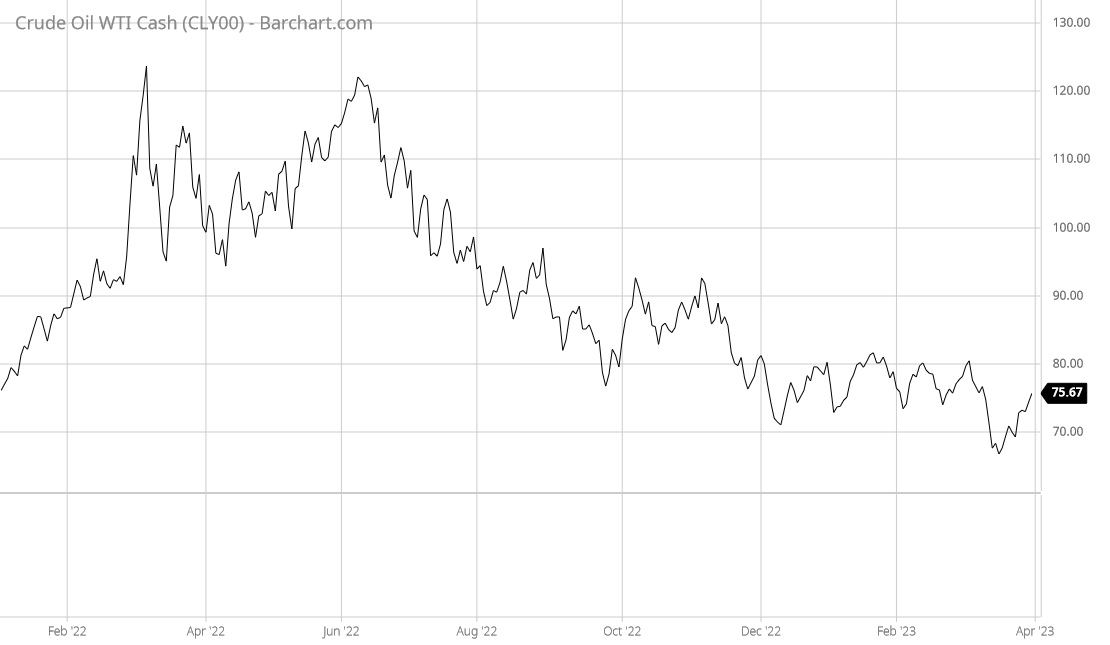

On Monday, May 8, 2023, American refining giant Delek US Holdings, Inc. ( DK ) announced its first-quarter 2023 earnings results. At first glance, these results are quite solid as the company did beat the expectations of its analysts, although revenues were down year-over-year. It is not surprising to see Delek's revenue decline over the period, as it directly correlates with crude oil prices. As everyone reading this is no doubt well aware, crude oil prices were lower in the first quarter of this year than they were in the first quarter of last year. We can see that here:

{kind=link}

As Delek US Holdings, Inc. is a refiner, though, revenue is not as important as the crack spread, which is the difference between the cost of crude oil and refined products. This is ultimately what drives the company's cash flow and profit. Fortunately, the company benefited from a much larger crack spread in 2023 than in 2022, allowing it to show improved cash flow year-over-year. This is not an atypical situation when crude oil prices fall, which is one of the reasons why refiners can be a hedge against falling energy prices in a portfolio.

In my last article on Delek US Holdings, I stated that the company's price appeared to be a bit high relative to its forward earnings growth. That situation appears to have changed, and today the company boasts a fairly attractive valuation. Thus, it might be worth considering Delek US Holdings, Inc. stock today, if only to diversify the upstream exposure that may already be present in your portfolio.

Earnings Results Analysis

As my long-time readers are no doubt well aware, it is my usual practice to share the highlights from a company's earnings report before delving into an analysis of its results. This is because these highlights provide a background for the remainder of the article as well as serve as a framework for the resultant analysis. Therefore, here are the highlights from Delek US Holdings' first-quarter 2023 earnings report:

- Delek US Holdings received net revenue of $3.9243 million in the first quarter of 2023. This represents an 11.99% decline over the $4.4591 million that the company received in the prior-year quarter.

- The company reported an operating income of $142.8 million in the most recent quarter. This compares very favorably to the $46.7 million that the company reported in the year-ago quarter.

- Delek US Holdings repaid $281.0 million in consolidated debt, bringing its net debt down to $1.910 billion. This represents a substantial improvement over the $2.6424 billion net debt that the company had at the start of the year.

- The company reported an operating cash flow of $395.1 million in the current quarter. That compares very favorably to the $26.8 million that the company reported in the equivalent quarter of last year.

- Delek US Holdings reported a net income of $64.3 million in the first quarter of 2023. This represents a substantial 874.24% increase over the $6.6 million that the company reported in the first quarter of 2022.

It seems certain that the first thing that anyone reading these highlights will notice is that Delek US Holdings generally saw improved financial performance compared to the prior-year quarter, with the notable exception of net revenue. One of the biggest reasons here is that the company's crack spread showed significant improvement year-over-year. Delek US Holdings highlights this in its earnings press release:

"The refining segment Adjusted EBITDA was $230.2 million in the first quarter of 2023 compared with $39.2 million in the same quarter last year. The increase over 2022 is primarily due to higher refining crack spreads, partially offset by lower sales volume primarily resulting from turnaround activities at the Tyler Refinery. During the first quarter of 2023, Delek US's benchmark crack spreads were up an average of 29.6% from prior year levels."

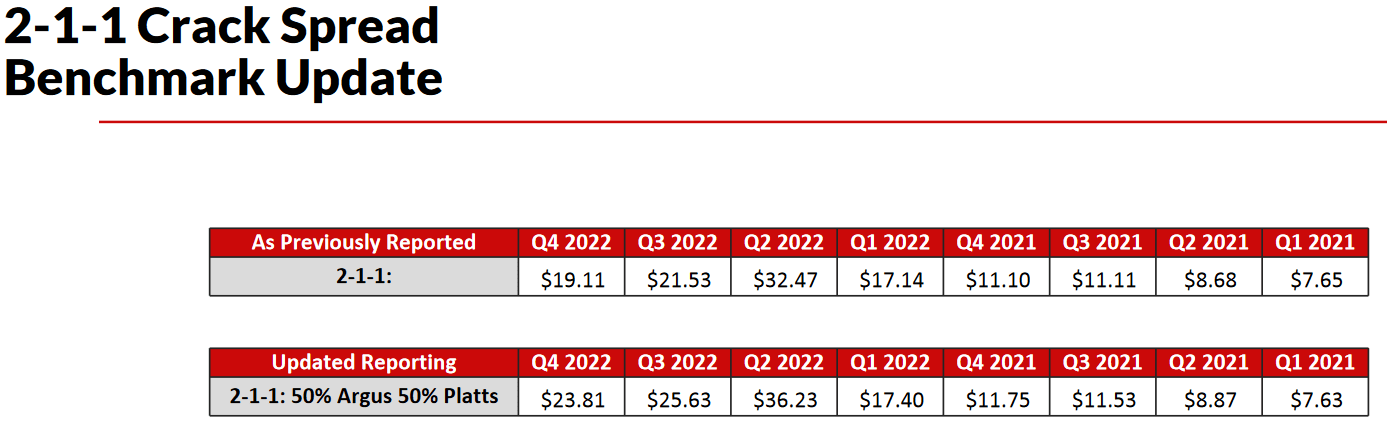

The basic business model of a refinery is to purchase crude oil and convert it into refined products that can be sold to consumers for fuel. The crack spread is the difference between the prices of these two commodities, so it is essentially the profit margin of a refinery. For this reason, the crack spread is the most important thing to look at in terms of analyzing a refinery's profitability. Curiously, Delek US Holdings did not provide its first-quarter crack spreads in the earnings press release. The company's earnings presentation is also silent on the matter, although it does provide the company's 2-1-1 crack spread for the two-year period that ended on December 31, 2022:

{kind=link}

Delek US Holdings did say that its crack spread was up 29.6% from the first quarter 2022 levels. That would imply a crack spread of approximately $22.21 per barrel, which would be the highest level that the company has experienced in the past two years with the notable exception of the second quarter of last year. This is not necessarily surprising, though. As I noted in the introduction, crack spreads frequently increase when crude oil prices decline. This is why gasoline prices do not decline as rapidly as crude oil prices during periods of declining energy prices, such as what we experienced beginning in the third quarter of last year.

There are a few reasons for this, including the fact that the refinery is selling refined products that were made when oil prices were higher in such an environment. There are other factors that can affect the crack spread too, including the supply and demand for gasoline and other refined products. Unfortunately for Delek US Holdings, there are some signs that gasoline demand is declining right now as consumers attempt to stay afloat in a weakening economy that continues to be plagued with food price inflation and rising rates on revolving lines of credit. The futures market appears to agree with this assessment as it is currently predicting falling crack spreads over the remainder of 2023:

{kind=link}

When we combine this with the fact that numerous indicators are pointing to a near-term recession, which typically weakens gasoline demand, the company may struggle to maintain its performance at the level that we saw during the first quarter.

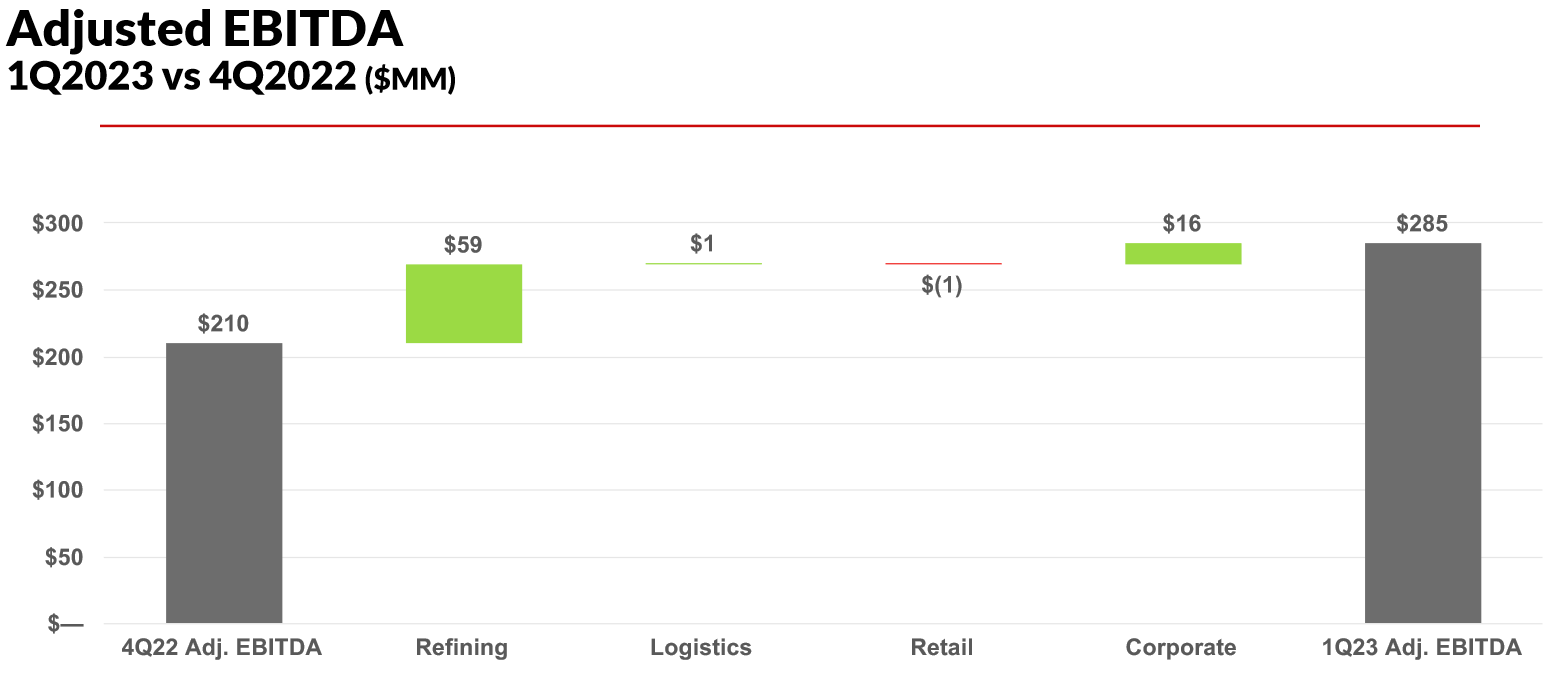

This is particularly important for Delek US Holdings because the company makes the overwhelming majority of its money from its refining operations. In the first quarter, Delek US Holdings reported an adjusted EBITDA of $284.6 million, $230.2 million of which came from the refining operation. Thus, the refining business accounts for fully 80.89% of the company's pre-tax cash flow. In addition to this, nearly all of the quarter-over-quarter growth that we see in the company's results came from the refining operation:

{kind=link}

Thus, the very real possibility of a declining crack spread, and a near-term recession reinforces the conclusion that this may be the best quarter that the company sees for the remainder of this year. This is disappointing, but as we will discuss in just a moment, Delek US Holdings made significant strides at improving its balance sheet over the past few months so that should help improve its ability to weather whatever economic troubles could be coming.

Financial Considerations

It is always important to analyze the way that a company is financing its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. This is normally accomplished by issuing new debt and using the proceeds to repay the existing debt, which can cause a company's interest expenses to increase in certain market conditions. As of the time of writing, interest rates are at the highest levels that we have seen since 2007, so that is a very real risk today. In addition to this risk, a company must make regular payments on its debt if it is to remain solvent. As such, an event that causes a company's cash flows to decline could push it into financial distress if it has too much debt. As it seems likely that Delek US Holdings' crack spread and cash flow will decline over the next few quarters, this is something that we should keep in mind today.

One metric that we can use to analyze the company's financial structure is the net debt-to-equity ratio. This ratio tells us the degree to which a company is financing its operations with debt as opposed to wholly-owned funds. It also tells us how well a company's equity can cover its debt obligations in the event of bankruptcy or a liquidation event, which is arguably more important.

As stated in the highlights, Delek US Holdings had a net debt of $1.910 billion at the end of the first quarter following the debt reductions that the company engaged in using its strong cash flow during the quarter. The company had a shareholders' equity of $1.1243 billion as of the same date. This gives the company a net debt-to-equity ratio of 1.70 currently, which is a substantial improvement over the 2.23 ratio that the company had at the start of the year. However, the company's net debt-to-equity ratio is still substantially higher than many of its peers:

| Company |

| Net Debt-to-Equity Ratio |

| Delek US Holdings |

| 1.70 |

| Valero Energy ( VLO ) |

| 0.22 |

| Marathon Petroleum Corporation ( MPC ) |

| 0.51 |

| Phillips 66 ( PSX ) |

| 0.37 |

| HF Sinclair ( DINO ) |

| 0.22 |

One thing that we note here is that a few of Delek US Holdings' peers saw their ratios get worse over the past quarter. In fact, only Delek US Holdings, Valero Energy, and HF Sinclair saw quarter-over-quarter improvements. However, Delek US Holdings still appears to employ a substantial amount of leverage to finance its operations relative to its peers. This could be a sign that the company is overly dependent on debt, which could represent an outsized risk to its investors.

However, Delek US Holdings' total consolidated debt includes the debt of its midstream partnership, Delek Logistics Partners ( DKL ). This entity employs substantially more leverage than the refining business, which increases the company's reported leverage above that of its peers that do not have such an entity on their consolidated balance sheets. If we exclude this, Delek US Holdings had a net debt of $212.8 million at the end of the first quarter of 2023. This gives the company a net debt-to-equity ratio of 0.17 for just the refinery operation, which is very reasonable compared to the company's peer group.

Dividend Analysis

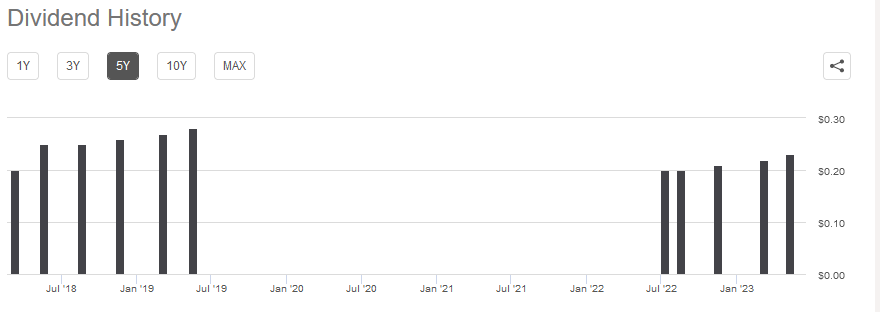

In reaction to its strong cash flow during the first quarter, Delek US Holdings raised its dividend to $0.23 per share quarterly ($0.92 per share annually), which gives the stock a reasonably attractive 4.27% yield at the current price. While this is a reasonably attractive yield that easily beats the 1.57% yield of the S&P 500 Index (SP500), Delek US Holdings has been very inconsistent about its payout over the years. As can clearly be seen here, the company's dividend has been all over the place over the past five years:

{kind=link}

We even see a period of time in 2020 and 2021 during which the company paid no dividends at all. This is not entirely surprising as the pandemic and related lockdowns did create a great deal of uncertainty in the energy sector that has only now begun to be resolved. The company still probably will not endear itself to income-focused investors due to its past history, but it is still nice that it is giving out a reasonable yield right now given all the uncertainty in the economy and broader market environment.

As is always the case though, it is critical that we ensure that the company can actually afford the dividend that it pays out. After all, we do not want to be the victims of a dividend cut since that would reduce our incomes and almost certainly cause the company's stock price to decline.

The usual way that we judge a company's ability to afford its dividend is by looking at its free cash flow. The free cash flow is the amount of cash that was generated by a company's ordinary operations and is left over after the company pays all its bills and makes all necessary capital expenditures. It is therefore the money that can be used for things that reward the stockholders, such as paying down debt, buying back stock, or paying a dividend. In the first quarter of 2023, Delek US Holdings reported a levered free cash flow of $741.2 million, which was by far the highest level that the company has had in the past two years. As of March 31, 2022, the company had 84,569,103 common shares outstanding, so the declared dividend costs the company $19,450,893.70 quarterly. The company's free cash flow is easy enough to cover that, so we probably do not have to worry too much about a dividend cut here.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a refinery operator like Delek US Holdings, one metric that we can use to value the company is the price-to-earnings growth ratio. This ratio is a modified version of the familiar price-to-earnings ratio that takes a company's earnings per share growth into account. A price-to-earnings growth ratio of less than 1.0 is a sign that the stock may be undervalued relative to its forward earnings per share growth and vice versa. As I pointed out in a recent blog post though, pretty much everything in the traditional energy sector appears to be undervalued relative to its forward earnings growth, so the best way to use this metric is to compare Delek US Holdings to its peers in order to see which company currently offers the most attractive relative valuation.

According to Zacks Investment Research , Delek US Holdings will grow its earnings per share at a 5.17% rate over the next three to five years. This gives the stock a price-to-earnings growth ratio of 0.91 at the current price, which indicates that it may be undervalued today. This is a bit of an improvement over the 1.05 ratio that it had the last time that we looked at the company, which is a sign that the valuation is improving. Here is how Delek US Holdings' valuation compares to its peers:

| Company |

| PEG Ratio |

| Delek US Holdings |

| 0.91 |

| Valero Energy |

| 0.76 |

| Marathon Petroleum Corporation |

| 0.87 |

| Phillips 66 |

| 0.33 |

| HF Sinclair |

| 2.48 |

This confirms my previous statement that most things in the traditional energy sector are undervalued today. The only company on this list that does not appear to be undervalued is HF Sinclair. Unfortunately, Delek US Holdings does not have the most attractive valuation of its peers, despite the fact that the company does still appear undervalued. However, as already stated, Delek US Holdings has a midstream partnership that provides it with a source of steady cash flows. This gives it a bit of an advantage over some of its peers as it should allow the company to sustain some of its cash flow regardless of what happens in the economy. As a near-term economic slowdown appears likely, this is an attractive characteristic.

Conclusion

In conclusion, the first quarter of 2023 was a very good quarter for Delek US Holdings as a large crack spread resulted in very strong cash flows from its refining operation. Unfortunately, it does not appear that the company will be able to maintain this performance over the remainder of the year as slowing refined product demand and a possible recession will apply pressure on its margins. The company has strengthened its balance sheet to better weather this possibility and it appears that the stock is somewhat undervalued today, so Delek US Holdings, Inc. still might be worth considering for investment though.

For further details see:

Delek US Holdings: Company Delivers Strong Q1 Performance, But May Not Last