DINO - Delek US Holdings: Reasonable Results But Price Is A Bit High

Summary

- Delek US Holdings, Inc. reported fairly solid Q4 2022 results, although the market does not appear to agree.

- The company's refining operation benefited from wide crack spreads, which are likely to continue to benefit it over the near term.

- The company's midstream partnership delivered the best results in its history, resulting in a distribution increase that should benefit the company heading into 2023.

- Delek US has substantially higher leverage than its peers, and it appears that the company's debt load is getting worse.

- Delek US Holdings, Inc. appears rather expensive compared to its peers, although it is not bad at all compared to the broader market.

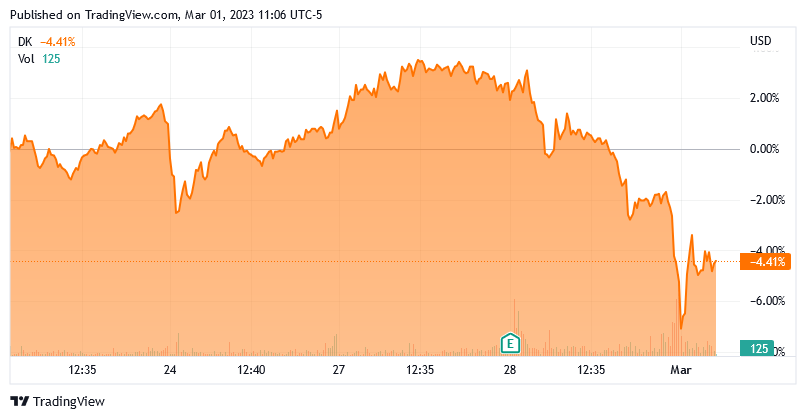

On Tuesday, February 28, 2023, crude oil refining giant Delek US Holdings, Inc. ( DK ) announced its fourth-quarter 2022 earnings results. At first glance, these results were quite solid, as Delek beat the expectations of its analysts in terms of both revenue and net income. However, the market seemed less than impressed, as it bid the stock lower over the course of the day:

{kind=link}

This may not be especially surprising, though, as the company did post a net loss that was significantly greater than last year. However, the headlines are all using the company’s non-GAAP earnings, which were substantially better than in the year-ago quarter. The company’s full-year numbers also came in much better than what it reported in 2021, which probably does not surprise anyone considering that energy prices were on the whole much higher than last year. The market’s overall disappointment could work to our advantage, though, as there are some reasons to believe that 2023 will come in very solid for the company and its valuation is reasonably attractive at today’s level. Overall, it might be worth watching for a good entry point.

Earnings Results Analysis

As my long-time readers are no doubt well aware, it is my usual practice to share the highlights from a company’s earnings report before delving into an analysis of its results. This is because these highlights provide a background for the remainder of the article as well as serve as a framework for the resultant analysis. Therefore, here are the highlights from Delek US Holdings’ fourth-quarter 2022 earnings report :

- Delek US Holdings brought in net revenue of $4.4792 billion in the fourth quarter of 2022. This represents a 44.12% increase over the $3.1080 billion that the company reported in the prior-year quarter.

- The company reported an operating loss of $103.5 million in the reporting period. This compares rather unfavorably to the $25.0 million operating profit that the company reported in the year-ago quarter.

- Delek US Holdings completed the acquisition of 3Bear Delaware Holding for $624.7 million, greatly expanding its midstream partnership, Delek Logistics Partners ( DKL ).

- The company reported an adjusted EBITDA of $220.9 million in the current quarter. This represents a significant 573.48% increase over the $32.8 million that the company reported in the equivalent quarter of last year.

- Delek US Holdings reported a net loss of $118.7 million in the fourth quarter of 2022. This compares quite unfavorably to the $13.4 million net loss that the company reported in the fourth quarter of 2021.

As mentioned in the introduction, the market appeared rather disappointed with these results as it bid the stock down during the trading session following the release. The company’s management was much more pleased with the company’s performance, however. In the earnings press release, CEO Avigal Soreq stated:

“2022 was a record year for Delek US. Market conditions were strong for refining and midstream, and we were well positioned to capture opportunities throughout the year. Refining’s crude utilization rate was 93 percent for 2022. This includes unplanned downtime at the Big Spring Refinery during the fourth quarter of 2022. Our logistics segment ran extremely well all year, its record EBITDA reflects this, as well as the successful integration of the 3Bear assets.”

Admittedly, some readers might simply chalk this up to an executive trying to toot his own horn. After all, we almost never see an executive doing anything but stating how well a given company performed during a conference call.

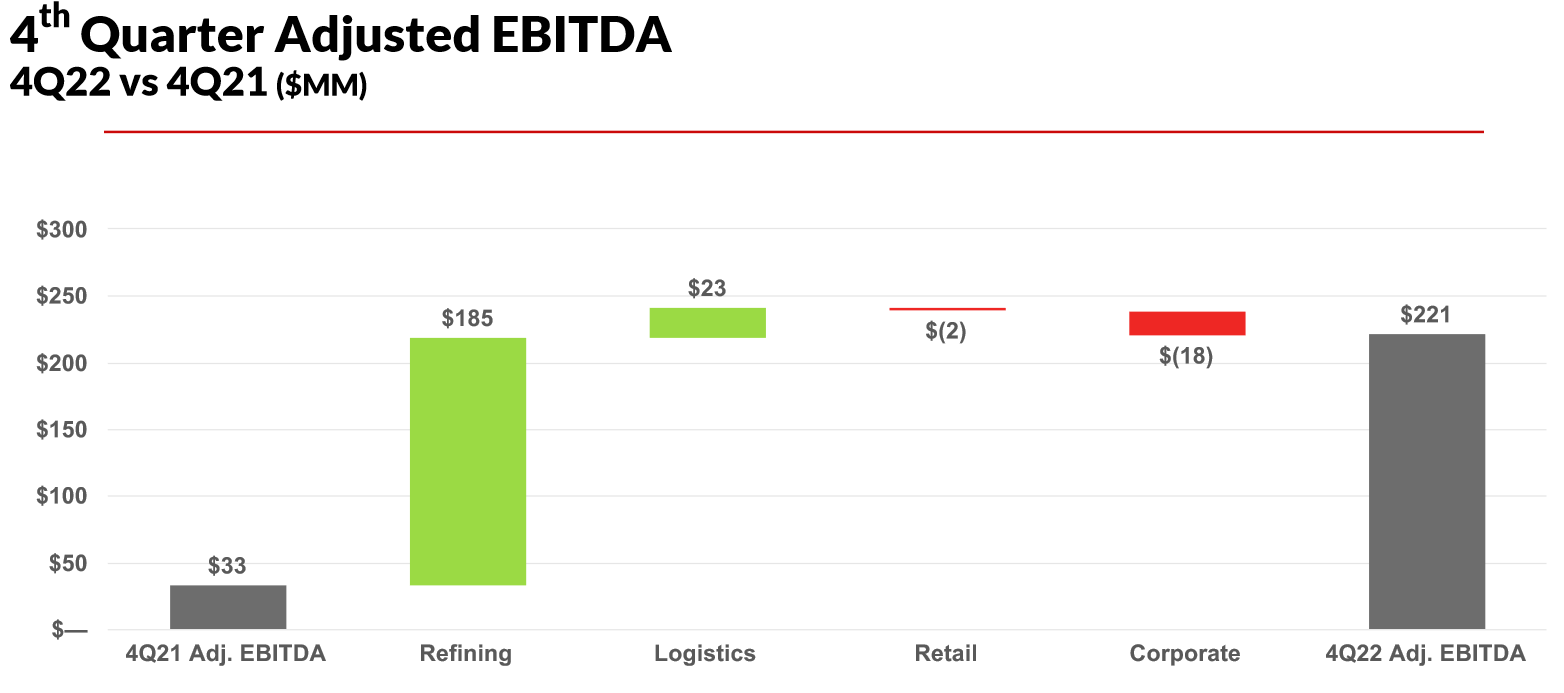

However, there are some reasons to be in agreement with Mr. Soreq. In particular, Delek US Holdings posted very strong year-over-year adjusted EBITDA gains. Adjusted EBITDA is a non-GAAP metric that serves as a proxy for pre-tax cash flow. As stated in the highlights, Delek US Holdings posted $220.9 million during the fourth quarter of 2022, which represents a substantial improvement over the $32.8 million that the company reported in the fourth quarter of 2021:

{kind=link}

We can see that the biggest year-over-year increase came from the company’s refining unit, which benefited from large crack spreads. The 3-2-1 crack spread measures the difference between the purchase price of crude oil and the selling price of gasoline, distillates, and other finished products. It is the core measure of profitability for a refinery. This is because a refinery’s basic business model is to purchase crude oil and sell the refined products that it produces from that crude oil. The larger the crack spread, the more money the refinery has available to cover its expenses and ultimately provide a reward for the shareholders. There are some reasons to believe that the company’s refining unit will continue to deliver a strong performance in 2023.

As I discussed in a recent blog post , the crack spread has been quite large over much of 2023 so far. This is a clear indication that gasoline supplies are quite tight. Delek noted this in the earnings conference call. Thus, the company’s refinery operations should prove to be very profitable this year unless that changes. This is unlikely to happen barring a recession.

As I have mentioned in various previous articles, upstream exploration and production companies have been hesitant to increase production despite the high energy prices, which means that there is unlikely to be more oil available to be refined into finished products. It would not really matter, however, since the nation’s refineries are already running at very close to peak capacity, which limits production. Thus, the supply of gasoline will likely remain fairly tight unless the demand for it drops significantly. After two years of COVID-19 lockdowns and fear, people are thus far seemingly not deterred by the fact that gasoline prices are higher than they were prior to the pandemic. They are continuing to execute their travel plans regardless of the cost. A recession may change that, but it is unlikely that anything short of such an event will. Thus, we will probably see large crack spreads for a while, which should benefit Delek US Holdings at least over the first half of 2023.

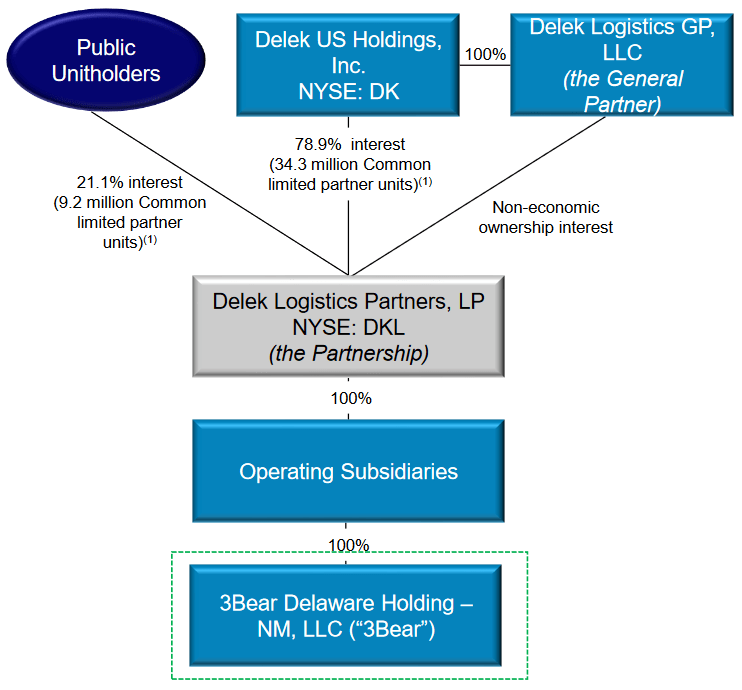

Delek US Holding’s refinery operation accounted for 82.35% of the company’s fourth-quarter 2022 adjusted EBITDA and it is the operation for which Delek is most well-known. As such, the company is generally considered to be a refiner. However, it is more than simply that. The company owns 78.9% of the limited partnership units of Delek Logistics Partners, which is a midstream partnership primarily operating throughout the states of Texas, Oklahoma, Louisiana, and Arkansas:

{kind=link}

Delek Logistics Partners announced fairly solid results earlier this week, which was also alluded to in Delek US Holdings’ conference call. In fact, as mentioned in the quote from Mr. Soreq earlier, the partnership reported its highest EBITDA ever due partly to its acquisition of 3Bear Delaware Holdings. I discussed that acquisition in a previous article on the partnership, so the important thing here is that it contributed positively to Delek US Holdings’ results. As a result of the strong performance by the partnership, the parent company reported an additional $23 million in fourth-quarter adjusted EBITDA compared to the level that it had last year. This reflects the fact that Delek Logistics Partners owns 34.3 million common limited partner units, which pay the company $34.986 million quarterly in distributions at the current rate (the distribution that it received in the fourth quarter was $33.957 million). This is essentially pure cash flow to the company, as it has no particular expenses incurred in generating these distributions. It is exactly the same as if you or I were to purchase that many common limited partner units in the company. The fact then that the partnership increased its distribution by 3% in January should serve the company well going forward as it provides it with a very cheap source of cash flow growth.

The strong performance of both the refining operation and the midstream partnership was partially offset by weakness in the company’s retail operation. This is a business consisting of approximately 248 gasoline stations and convenience stores located mostly in West Texas and the American Southwest. This unit only generated an adjusted EBITDA of $7.8 million in the fourth quarter compared to $10.0 million in the prior-year quarter. The company claimed that this was due to lower margins and lower sales volumes. The fact that the stores had lower sales volumes is difficult to rectify with the tight gasoline supplies that we are seeing currently throughout the United States, but it is possible that we are simply seeing less gasoline consumption in that particular area of the nation. Regardless, the decline in cash flow here was much less than the increases that we saw in the company’s other businesses. Overall, this was a very solid quarter for Delek US Holdings.

Financial Considerations

It is always critical that we analyze the way that a company finances its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. This is usually accomplished by issuing new debt and using the proceeds to repay the existing debt. That can cause a company’s interest expenses to increase following the rollover, depending on the conditions in the market. This is something that could be a very big deal today considering the rising rate environment in the United States and elsewhere. In addition, a company must make regular payments on its debt if it is to remain solvent. Thus, an event that causes a company’s cash flows to decline could push it into financial distress if it has too much debt. That is something that could be a significant risk for a company like Delek US Holdings due to the volatility that we frequently see in energy prices.

One metric that we can use to evaluate a company’s financial structure is the net debt-to-equity ratio. This ratio tells us the degree to which a company is financing its operations with equity as opposed to wholly-owned funds. In addition, the ratio tells us how well a company’s equity can cover its debt obligations in the event of a bankruptcy or liquidation event, which is arguably more important.

As of December 31, 2022, Delek US Holdings had a net debt of $2.3844 billion compared to shareholders’ equity of $1.0695 billion. That gives the company a net debt-to-equity ratio of 2.23 today. Here is how that compares to some of the company’s peers:

| Company |

| Net Debt-to-Equity |

| Delek US Holdings |

| 2.23 |

| Valero Energy ( VLO ) |

| 0.31 |

| Marathon Petroleum Corporation ( MPC ) |

| 0.46 |

| Phillips 66 ( PSX ) |

| 0.35 |

| HF Sinclair ( DINO ) |

| 0.23 |

As we can clearly see, Delek US Holdings is substantially more levered than its peers. This is something that I pointed out in my last article on the company and it remains true today. Unfortunately, the company’s net debt-to-equity ratio increased substantially between the third and the fourth quarters, which is a very real point of concern. It could also be a sign that the company is using too much debt to finance itself, which exposes investors to extra risks if the economy goes sour.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a sub-optimal return on that asset. One metric that we can use to value a downstream energy company like Delek US Holdings is the price-to-earnings growth ratio. This ratio is a modified version of the more familiar price-to-earnings ratio that takes a company’s forward earnings per share growth into account. A price-to-earnings growth ratio of less than 1.0 is a sign that the stock may be undervalued relative to the company’s forward earnings per share growth and vice versa. However, as I pointed out in various previous articles, pretty much everything in the traditional energy sector appears undervalued today so the best way to use this metric is to compare Delek US Holdings to its peers in order to see which company offers the most attractive relative valuation.

According to Zacks Investment Research , Delek US Holdings will grow its earnings per share at a 5.17% rate over the next three to five years. This gives the company a price-to-earnings growth ratio of 1.05 at the current price. Here is how that compares to the company’s peers:

| Company |

| PEG Ratio |

| Delek US Holdings |

| 1.05 |

| Valero Energy |

| 0.92 |

| Marathon Petroleum Corporation |

| 0.26 |

| Phillips 66 |

| 0.34 |

| HF Sinclair |

| 0.53 |

This is certainly interesting. As we can see, Delek US Holdings currently appears to be rather expensive compared to its peer companies. Given the higher debt load relative to its peers, it should be trading at a cheaper price to account for the risk, but it is not. This could be because the company’s growth rate is expected to be somewhat lower than the other companies listed here. With that said, Delek US Holdings is by no means particularly expensive compared to pretty much anything outside of the traditional energy sector but it might still make sense to wait until the price comes down before buying in.

Conclusion

In conclusion, the market was not particularly impressed with Delek US Holdings, Inc.’s fourth-quarter results, but there were actually quite a few things to like here. In particular, the company posted one of the best quarters in its history, as a wide crack spread resulted in large refining profits and the company’s midstream partnership delivered record cash flows. However, Delek US Holdings, Inc. is a fairly heavily levered compared to its peers and appears to have a higher valuation. As such, Delek US Holdings, Inc. is probably best added to a watchlist and purchased if the stock price declines from today’s levels.

For further details see:

Delek US Holdings: Reasonable Results But Price Is A Bit High