BTU - Deleveraged And Oversold Peabody Energy Is Now A Compelling Long

2023-05-23 12:14:54 ET

Summary

- Peabody Energy stock is oversold and coming into a support level which indicates that the stock may be ready for a bounce.

- Peabody has made good strategic moves with its recent energy windfalls by paying down debt and deleveraging.

- Financial performance has been robust and the stock is likely undervalued.

- Trading below book value, BTU stock provides savvy investors a nice platform for selling puts to earn yield and minimize risk.

Peabody Energy ( BTU ), a leading player in the coal industry, has recently experienced a significant pullback in its share price. Technical indicators suggest that the stock is oversold and poised for a rebound. In addition to the potential for a significant bounce, the company has also made several recent strides in paying down debt and improving financial stability, presenting an attractive opportunity for income-seeking investors. By employing a short put strategy, we can capitalize on this situation while minimizing risk and generating a big chunk of income. With a high probability of success at over 80%, it seems like a great time to get involved in the name.

Financial Results

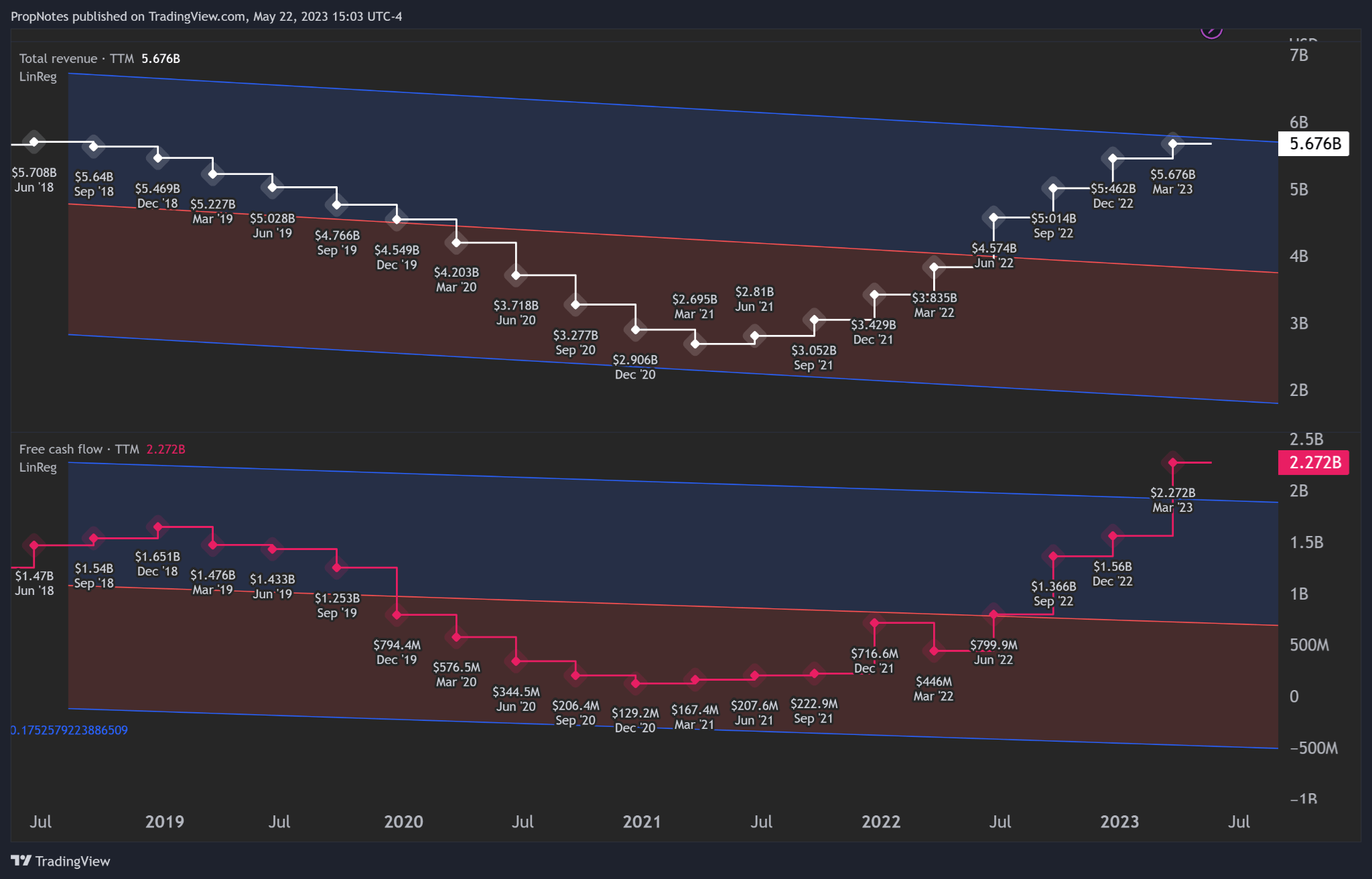

In its most recent quarter, Peabody reported strong financial results. Revenues grew by 97% YoY to $1.36 billion , primarily driven by strong global demand for energy. While coal is politically unpopular, it is still needed in many parts of the world to keep the lights on, including parts of the United States.

Peabody was also able to keep quarterly costs in line, as it ended the period by reporting over $412 million in operating income.

This recent performance has been part of a larger upswing the company has recently seen in terms of top and bottom-line performance:

{kind=link}

As global energy demand has rebounded post-pandemic, the company has produced robust results. While it's unclear how long this boom will last, the company is making the right moves with retained earnings.

On that point, Peabody's liquidity position is quite solid with the company boasting a current ratio of 2.1 and a quick ratio of 1.7. The big thing to note here is that for the longest time, Peabody had a large long-term debt burden of nearly $1.5 billion. In a smart capital allocation move, the company reduced this debt materially to under $300 million with proceeds from the recent performance.

This substantial deleveraging should allow the company much greater operational flexibility in the future, along with greater capital return capabilities. While the market is valuing the company's terminal cash flows at basically nothing due to concerns about coal's long-term place in the global energy mix, the stock is trading below book value, indicating that the market may be overly bearish on the company's future prospects.

Combined with the deleveraging, this undervaluation provides savvy investors a nice platform for selling puts.

Technicals

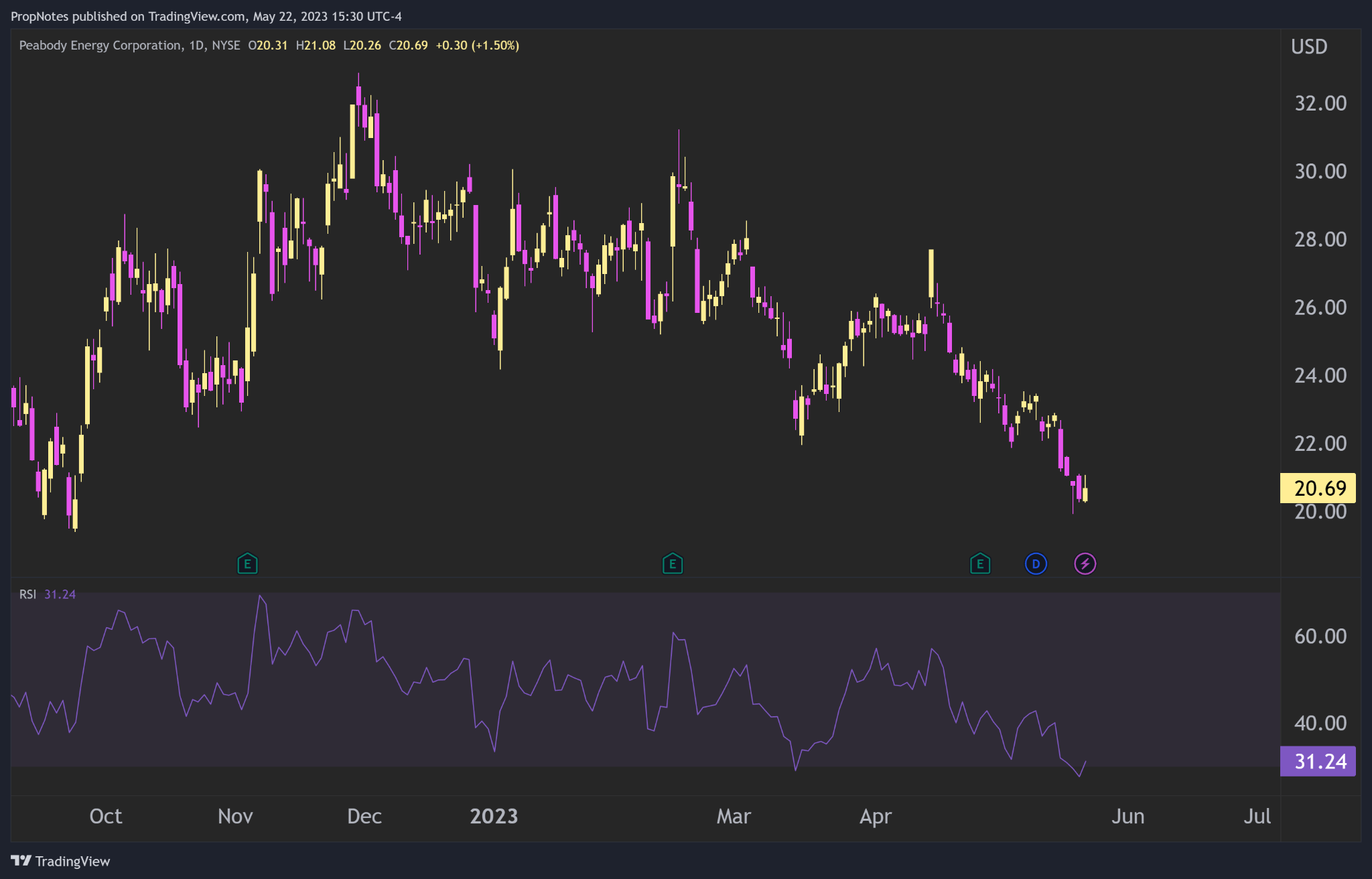

A closer look at Peabody Energy's stock chart reveals that a number of technical indicators suggest that the stock is currently oversold. The 14-day Relative Strength Index ((RSI)) has dipped below, and is now hovering just above, 30, indicating that the stock is in oversold territory and could be due for a bounce:

{kind=link}

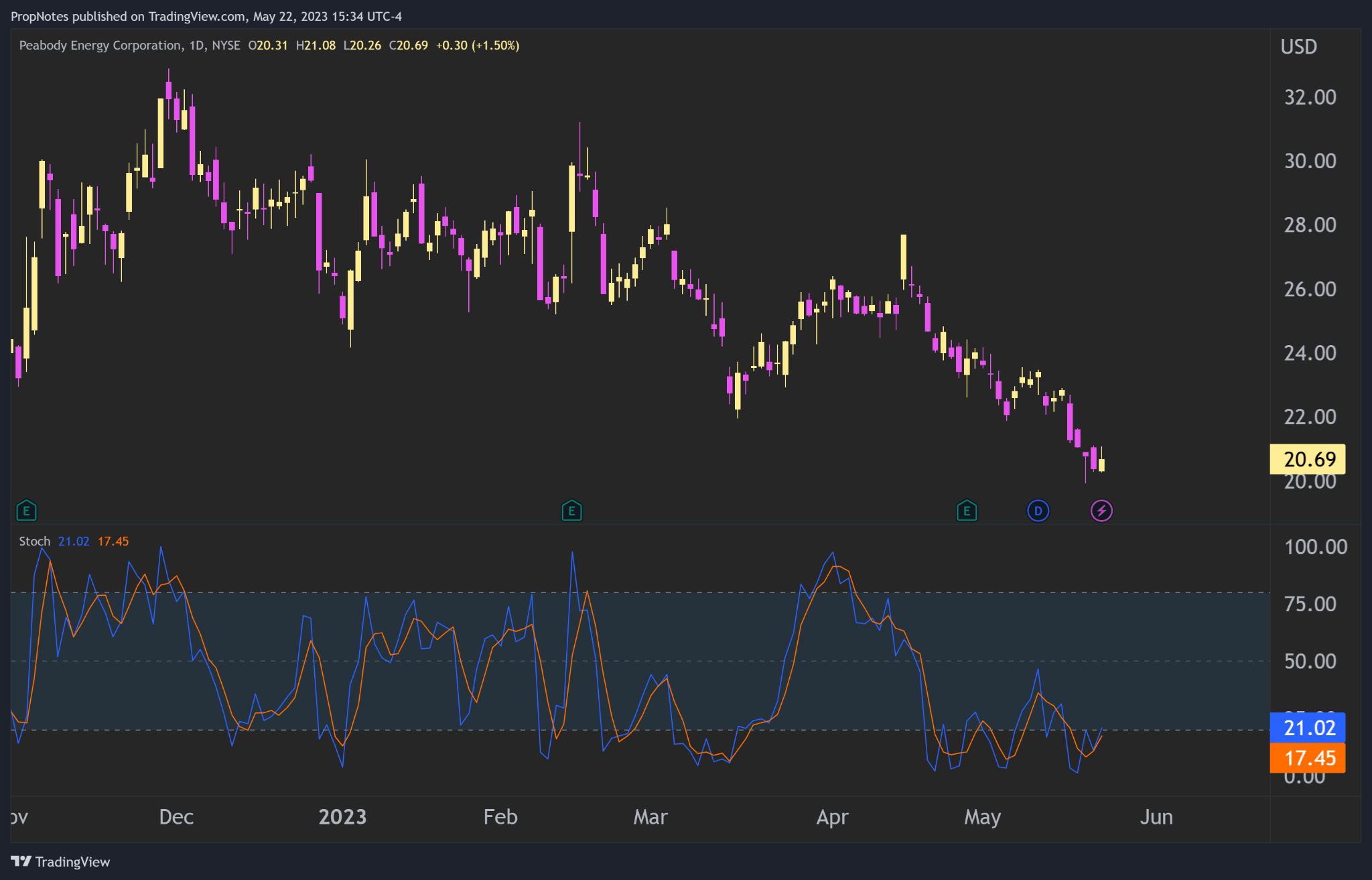

Additionally, the stock's stochastics are also hovering in the oversold range, further supporting the notion that selling pressure may be exhausted:

{kind=link}

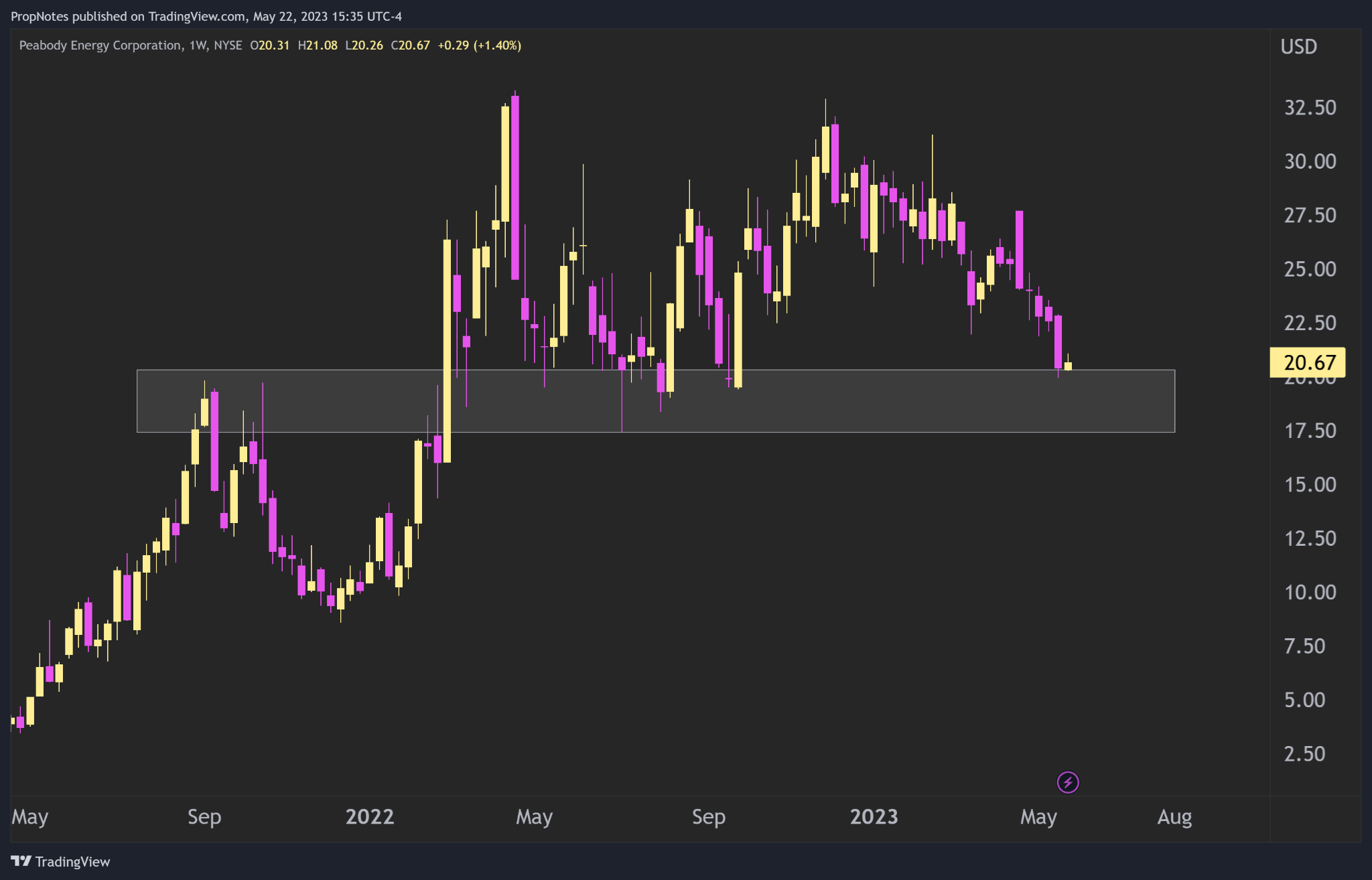

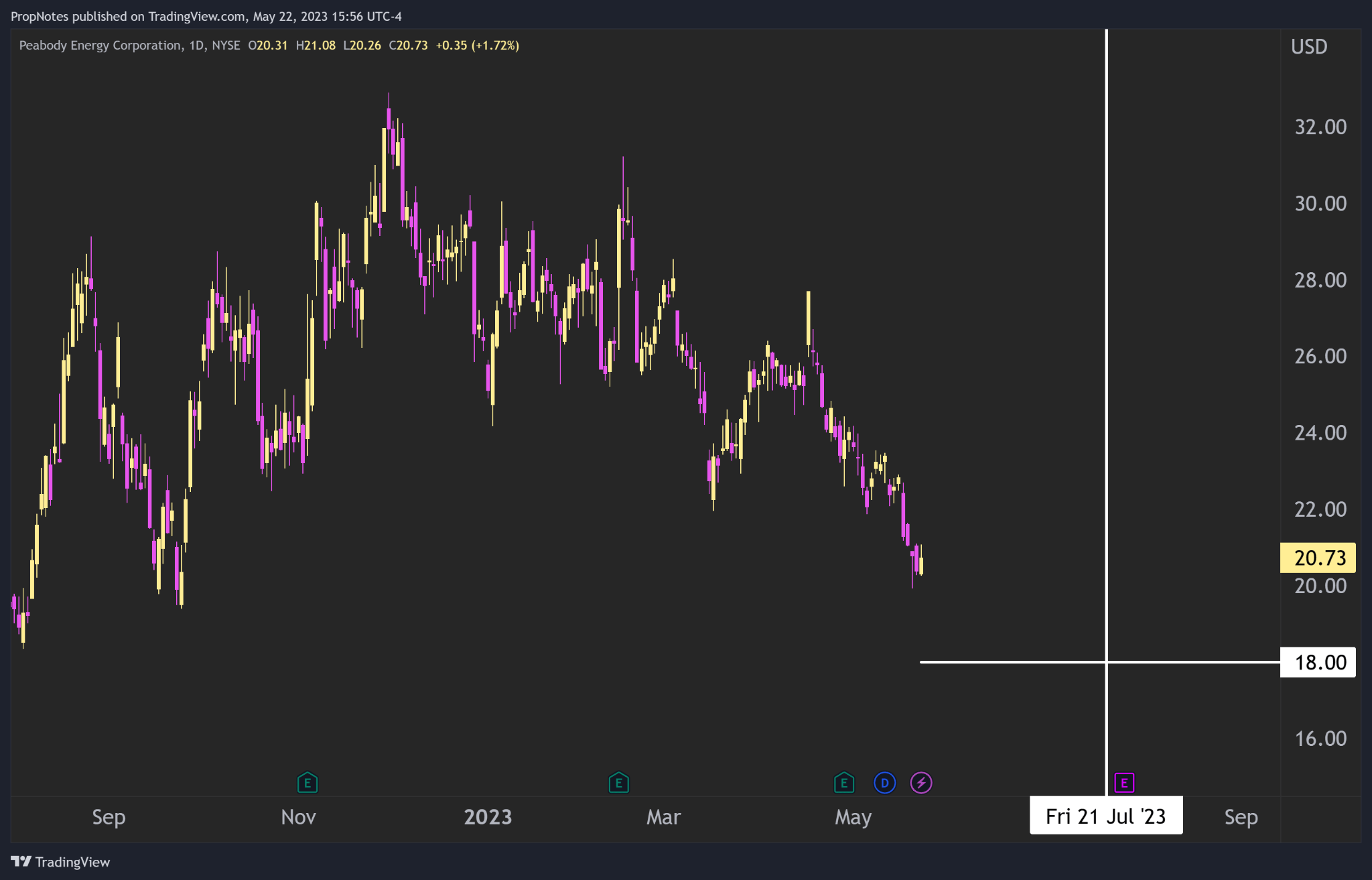

Last but not least, the stock is trading into a significant level of support between $17.50 and $20 per share, which can be seen here:

{kind=link}

Taken together, these technical readings and levels indicate that sellers are likely becoming exhausted, which could allow for buyers to step in and cause a rebound in the stock price.

The Trade

With the strong recent performance, improved balance sheet, and oversold condition, Peabody Energy looks like a perfect candidate for selling puts, as it's difficult to precisely time when the stock may bounce.

For those who haven't done a trade like this before, selling a put is basically committing to purchase a stock at a certain price (strike price), sometime between now and a certain date, if the option is assigned. Typically, options are only assigned if the stock finishes below the strike price, as that is when it makes sense to "use" the insurance, from the buyer's standpoint.

In return for standing ready to buy shares, put sellers receive a cash premium that serves as income on the trade.

Functionally, selling a put is very similar to placing a bid for stock, and then getting paid to wait for the order to be filled.

For this trade, we like the July 21st, 18 strike puts:

{kind=link}

They pay a credit of $0.50 cents per share, which comes out to a tidy 17.3% annualized yield. In return for selling these, traders need to be ready to purchase 100 shares of stock per contract at $18, for $1,800.

If the stock finishes above $18 by July 21st, then put sellers get to keep the premium free and clear.

If the stock finishes below $18 by July 21st, then put sellers get to purchase the stock at a better price than today's fair market value, while still keeping the premium free and clear.

The option market is pricing this option as though it has an ~80% probability of expiring out of the money, which means a very high percentage chance that this trade expires at max profit.

Risks

While the trade idea presents a high probability of success, it's crucial to be aware of the potential risks associated with the trade. Some of the key risks to consider include:

Industry : Peabody, whether we want to admit it or not, is in a dying industry. While the company is doing the best it can in terms of earning profits for shareholders, the day will come when there is simply no demand left for coal. This fact will likely permanently depress the company's valuation and could drive it lower, causing losses.

Macro : Peabody is subject to broader macroeconomic risks, including interest rate fluctuations, economic downturns, and changes in government policies that could impact the fossil fuel sector. Coal is very politically unpopular, and the company could come under fire for various reasons. This could cause losses for traders with long exposure to the company.

Commodity-linked : Peabody's profits ultimately rely on the market for coal, and coal prices. Should demand wane, then it would likely cause losses to investors as the market anticipates reduced cash flows.

Summary

In conclusion, Peabody Energy presents an attractive opportunity for income-seeking investors looking to capitalize on the stock's oversold condition and improved financial footing. By employing a short put strategy, we can generate income, mitigate risk, and take advantage of a potential rebound in the stock price. While the company's long-term viability is in question due to its industry dynamics, there should be more than enough time for investors to earn a solid yield off of the underlying shares using options. With a high probability of success, the trade idea we proposed offers a compelling way to participate while reducing risk.

For further details see:

Deleveraged And Oversold, Peabody Energy Is Now A Compelling Long