DELHY - Deliveroo: Not Bad But Not Enough Reason To Buy

Summary

- Food delivery app Deliveroo has seen a sharp drop of 63% over the past year. Numbers like orders and gross transaction value look weaker too, because of a high base.

- But its revenues, while slightly dated, continued to be strong in the first half of 2022. Its gross profit margin improved as well.

- Its reduced guidance, a challenging year ahead, and a P/S in line with the consumer discretionary sector indicate limited potential upside.

With a price decline of 63% over the past year, Deliveroo ( DROOF ) is among the worst-performing companies in the stock markets I've covered recently. I think this is for a range of reasons, including market weakness during the past year, which has been particularly unkind to consumer discretionary stocks and ADRs. Post-pandemic prospects for food and grocery delivery companies are also less buoyant. But some of it also has to do with the perception of a slowdown in growth.

High base effect on latest figures

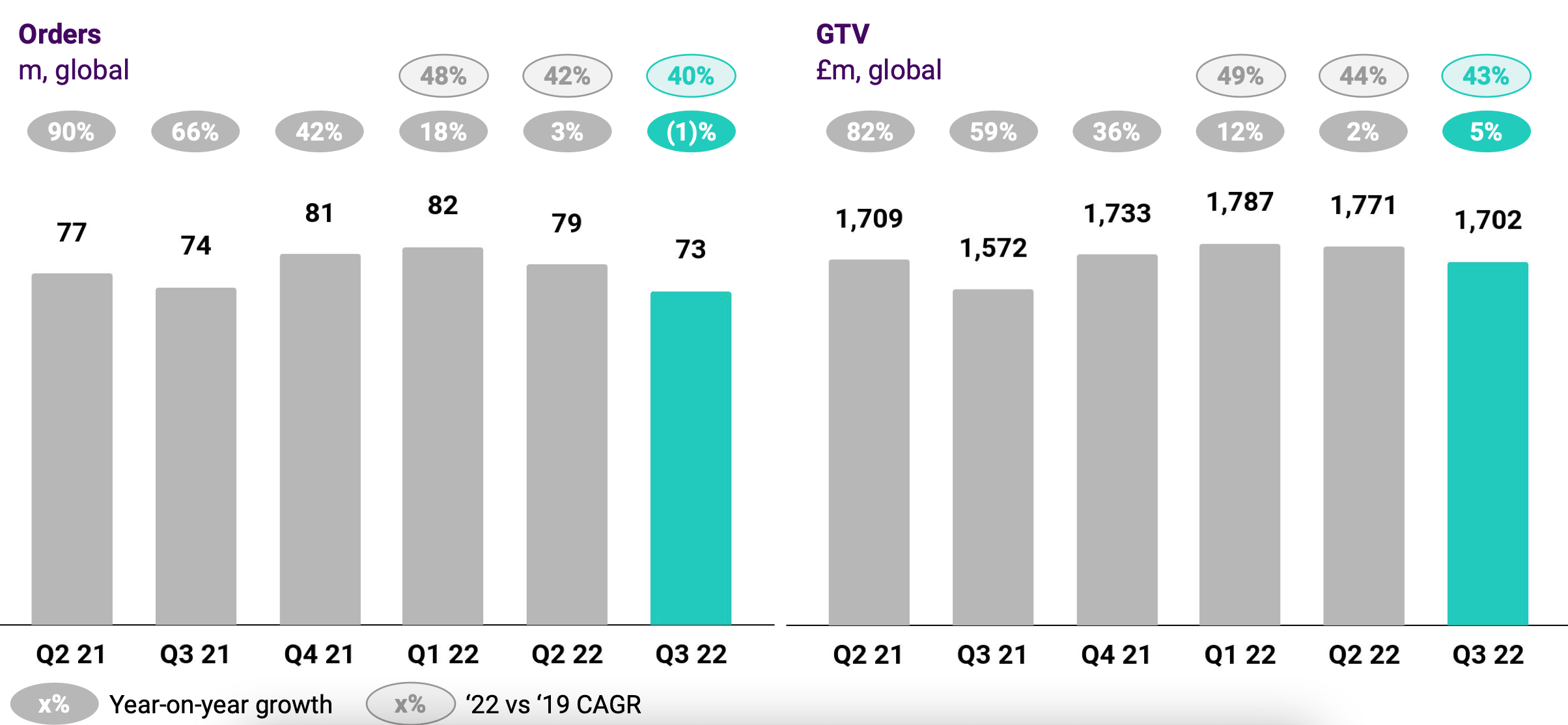

Consider its latest trading update for the third quarter of 2022 (Q3 2022). Gross transaction value [GTV], which is the total value of sales made net of refunds, rose by 8% year-on-year (YoY) to £1.7 billion and is up by 7% for the nine months of 2022 (9M 2022) at market exchange rates. This is a significant slowing down in growth from both Q3 2021 when it saw 59% growth. It can of course be argued that we were out of the lockdown then, but it did spill over into the quarter and people were still cautious about stepping out.

In any case, on the face of it, it is a big drop. Further, the number of orders has shrunk by 1%, the first time a decline has been seen in the last five quarters, which reflects a post-lockdown fall in demand. At 73 million they are the lowest in absolute terms they have been since too.

{kind=link}

The details show a different story

However, while these figures are important, they are hardly the full picture. For instance, the company offers a comparison from Q3 2019, which was the last year before the pandemic. This indicates significant improvement. GTV has grown by a very healthy 43% growth in Q3 2022 at constant currency since then. Order numbers are also up by 40% from there.

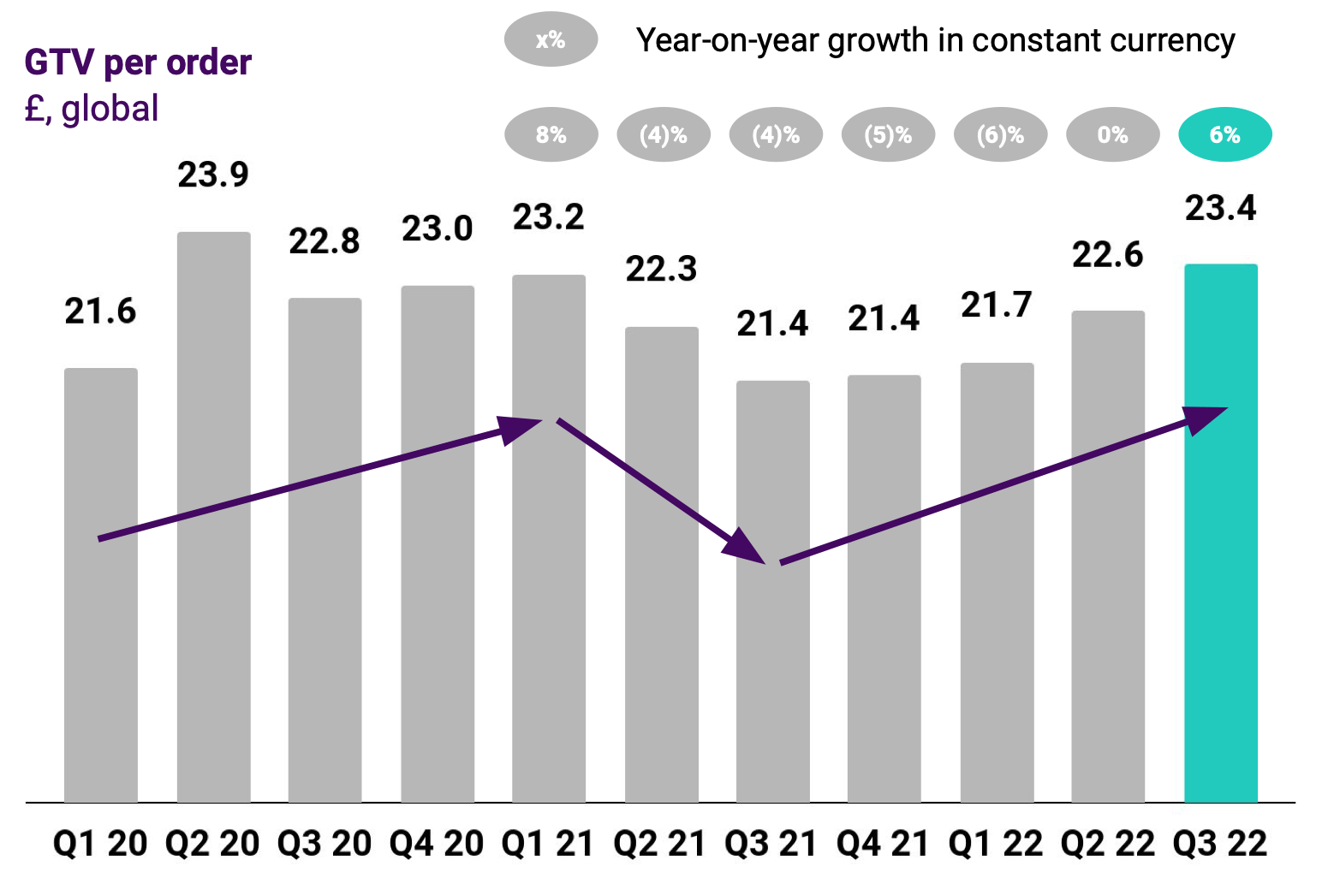

Further, not all its metrics are impacted by the post-pandemic effect. Its GTV per customer at £23.4 is the highest it has been in two years. It has also grown by 6% at constant currency, after five quarters of decline or zero growth. At 3.3, the monthly order frequency also remains largely stable.

{kind=link}

Financials are healthy

Its financial details are a bit dated as of now, but for the period up to the first half of 2022 (H1 2022), the revenue has shown strong growth of 28.5% YoY, keeping up with the growth rates seen even during the height of COVID-19. But here's the real rub. Both orders and total GTV had started slowing down in Q1 2022 and were down to a crawl by Q2 2022. Yet, Deliveroo has been able to sustain its revenue growth.

So how did it manage this growth? Through an increase in commission fees to restaurants, consumer fees and advertising revenue. There are various estimates available on how much commission fees it charges, but the highest puts it at 35% of the restaurant's gross revenue. Advertising revenue rose as it launched an FMCG advertising platform, which adds to revenues from sponsored positioning by restaurants. This is really what at least I am looking for as an investor. Can a company stay financially fit even during challenging times? In this case, so far, the answer is yes.

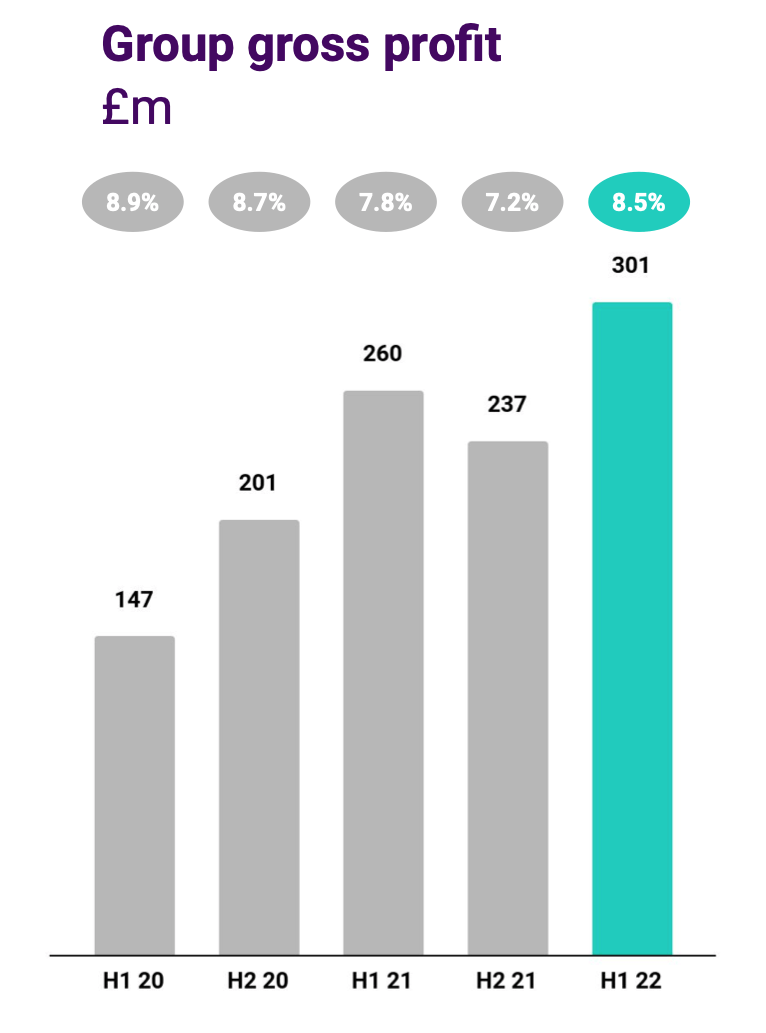

Next, its gross profit margin has also improved. The margin, which it reports as a percentage of GTV, as opposed to the usual norm of reporting it as a percentage of revenue, is up to 8.5% in H1 2022 compared to 7.8% in H1 2021. It's naturally much higher in terms of revenue at 29.7%, up from 28.7% last year. But that's where its story on profits ends. With operating expenses at a fairly high 45.3% of revenues, it has so far reported operating losses.

{kind=link}

As per its guidance, it does expect to reduce its adjusted EBITDA loss as a percentage of GTV to 1.5-1.8% in 2022 from 2% last year. It's targeting to break even sometime next year or in early 2024. In other words, Deliveroo has been a growth investment in the past and continues to remain so for now.

A red flag

The one red flag however with regard to growth is the reduction in guidance for GTV growth for the second time in 2022. Initially, it had a guidance of 15-25%, which was reduced to 4-12% and has now come off further to 4-8%. Going by its financials, though, that doesn't necessarily have to mean much for its revenue growth. In fact, considering the fact that Q4 of any year can be a seasonally better year, its revenues might just come in robust for H2 2022 as well.

Fairly valued

That said, its market multiples don't suggest much possibility of a price uptick considering that its price-to-sales (P/S) ratio is at 0.9x, which isn't much lower than the 0.93x for the consumer discretionary sector. It is however, somewhat lower than the 0.98x for Just Eat Takeaway ( JTKWY ) and 1.8x for Delivery Hero ( DLVHF ). But then they have also shown much stronger revenue growth of over 50% for H1 2022 as well, which explains their higher multiples. This year can also be hard on delivery services providers, considering that consumers are expected to continue cutting back on discretionary expenses, thanks to the state of the economy. I'd take this into account when thinking of investing in Deliveroo, especially as its price is showing little momentum.

What next?

In total, it isn't a bad company by any stretch. If anything, its performance is quite decent. I also like its nimbleness in strategy to sustain revenue growth and even grow its gross margins. The food and grocery delivery market has promising prospects , and it can continue to make gains because of that. It has ongoing issues with regard to the terms of delivery workers , but that seems to be more of an industry-wide issue than just a company-specific one.

I do believe that if it continues to report strong sales figures, as do its peers, its price might rise from the current levels. It has fallen to less than a third of where it was in April 2021. At the time the sector would have stood out for its sales growth even as many others languished. Even then, it has fallen quite a bit from last year, when we were well out of the pandemic in most parts of the world.

I'd be on the lookout for its releases. And if they are good, wait for Deliveroo to catch momentum and then decide on whether to buy it. Until then, I'd hold off.

For further details see:

Deliveroo: Not Bad But Not Enough Reason To Buy