DLVHF - Delivery Hero: Economic Headwinds And Operational Challenges

2023-07-25 11:20:17 ET

Summary

- Delivery Hero, a global online food delivery company, is facing slowing growth and poor margins, despite its high market share and partnerships with leading food brands.

- We believe margin issues will continue in the coming years, with analysts' forecast breakeven on a NIM basis in FY25.

- Delivery Hero's market position is likely defensible but it cannot leverage its market leading position to improve margins.

- Relative to others in the industry, we believe the company is underperforming. This implies there are better options for gaining exposure to the industry.

Investment thesis

Our current investment thesis is:

- Delivery Hero has some strong qualities, such as its high market share in several geographies, partnerships with leading food brands, and technological capabilities.

- However, we are concerned that growth is beginning to slow with order numbers softening (with economic conditions further compounding this) and the high level of competition.

- The biggest issue, however, is the poor margins. The industry has not shown a route to sustainable profitability for many of its largest players. Costs are being cut and scale economies are helping, but we are struggling to see how attractive levels will be achieved.

Company description

Delivery Hero ( OTCPK:DLVHF ) is a leading global online food delivery company headquartered in Berlin, Germany. The company operates a digital platform that connects consumers with a wide range of restaurants and food providers. With operations spanning multiple continents, Delivery Hero has established a strong presence in various markets, offering convenient and efficient food delivery services to millions of customers worldwide.

Share price

Delivery Hero's share price has significantly underperformed the market, losing value since it was listed. The initial gains were a result of positivity in the industry, with high growth implying a lucrative future. This has subsequently changed, as underlying financial concerns imply difficulties ahead.

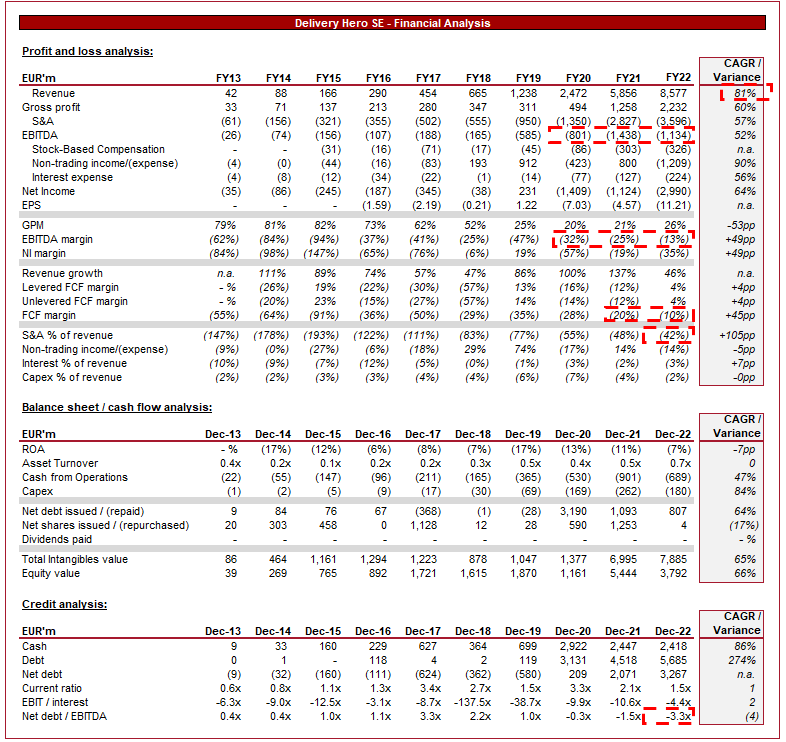

Financial analysis

{kind=link}

Delivery Hero Financials (Capital IQ)

Presented above is Delivery Hero's financial performance for the last decade.

Revenue & Commercial Factors

Delivery Hero's revenue has grown by an incredible 81% rate in the last 10 years, with no single fiscal year below 20%. This trajectory is a reflection of both organic and inorganic growth, as the business expands its services in core geographies, as well as new markets.

Business Model

Delivery Hero's business model revolves around facilitating food delivery through its innovative platform. The company operates as an intermediary between consumers and restaurants, providing a seamless online ordering and delivery experience.

Delivery Hero has gained market share through the development of a user-friendly online platform and mobile application, allowing consumers to browse menus, place orders, and track deliveries. This rapid trend of delivery app usage has been born from a demand for convenience, with consumers willing to pay a small fee for access to restaurants.

This industry has exploded due to an increasing consumer preference for online food ordering and delivery services, driven by convenience and changing lifestyles. The pandemic accelerated this trend, acting as a test-bed for many consumers, and was likely successful in capturing many long-term users. Our view is that this should continue, although not to the degree of the last 3 years, as many of the key global economies now have access to this service.

Delivery Hero currently operates in over 70 countries, with several brands utilizing its underlying infrastructure.

{kind=link}

Brands / Regions (Delivery Hero)

Delivery Hero generates revenue through commissions on orders placed through its platform and delivery fees. Additionally, the company may charge restaurants for marketing and promotional services to enhance their visibility on the platform. For this reason, the company's focus is on increasing the volume of sales, allowing the business to generate returns through scale.

Operationally, the company has built a robust logistics infrastructure, including a fleet of delivery drivers and partnerships with third-party delivery service providers. This network ensures timely and reliable delivery of food orders, importantly, in an efficient manner. Its relationship with Restaurants is critical, as many agree exclusive rights with a delivery business. For this reason, the ability to capture a large market share is dependent on the options provided to consumers.

Some of its peers have experimented with subscription services, seeking to reduce the volatility of long-term revenue. The value proposition has yet to be sufficiently developed in our view and it reflects in the uptake of these subscriptions. The issue is that consumers would happily pay monthly for free delivery but this is the one thing the apps cannot give to consumers.

Currently, the company is primarily focused on the restaurant industry, although similar to its peers, it has begun expanding into groceries. The value proposition is strong, as although consumers can get goods delivered, there is usually a minimum spend and a few days wait. This further expands the total market size, increasing the growth potential.

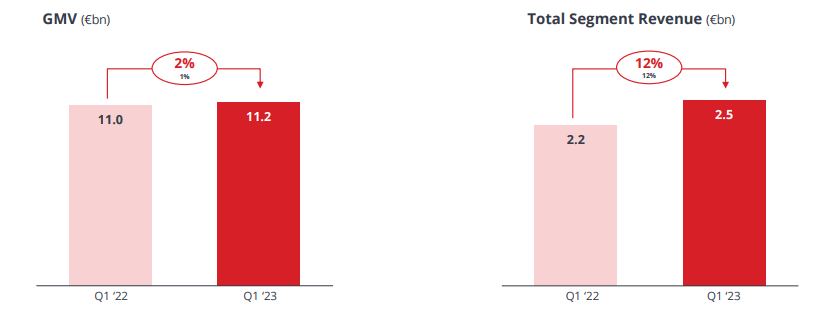

Delivery Hero's growth looks to be slowing, with GMV up 2%. This is primarily due to a decline in Asia, with GMV down (6)%. This is somewhat muddied by the timing of pandemic re-openings but nevertheless is a concerning change.

{kind=link}

GMV/REV (Delivery Hero)

This is reflected below, with a noticeable correction following the pandemic peak in late 2021. This was an inevitability but it remains unclear as to where levels will normalize.

Active customers (Delivery Hero)

Order frequency (Delivery Hero)

Delivery Hero's development in South Korea in particular is commendable, reiterating the business has strong capabilities and go-to-market strategy.

Active customers South Korea (Delivery Hero)

Innovation from Delivery Hero comes in the form of "DMart", which is described as quick commerce. The company operates stores that hold thousands of products, allowing the business to provide everyday products quickly and conveniently.

DMart (Delivery Hero)

Growth for DMart continues to be strong, although it is slightly concerning to see the QoQ gains slow. This implies there are not necessarily diversification benefits between the two segments, moving in lockstep. Further, with the business still losing money on a GPM level in conjunction with this, the concern is that Delivery Hero has compounded its margin issues (which we will discuss later).

{kind=link}

DMart (Delivery Hero)

Delivery Hero operates in a highly competitive food delivery market, facing competition from both established players and emerging startups. Key peers include Uber Eats ( UBER ), Just Eat ( OTCPK:JTKWY ), Deliveroo ( OTCPK:DROOF ), DoorDash ( DASH ), Postmates, and Grab ( GRAB ). Most lucrative geographies (high population, wealthy citizens, etc.) have at least 2 of the leading global businesses operating in the market. For this reason, it is critical to provide a timely and cost-attractive service, alongside a range of restaurants.

Competitive Positioning

Delivery Hero possesses several competitive advantages:

- The company has established a leading presence in multiple countries, benefiting from economies of scale and leveraging its global network to expand into new markets.

- Delivery Hero's advanced technology platform, including mobile applications and order management systems, provides a seamless and user-friendly experience for both consumers and restaurant partners.

- Delivery Hero offers a wide range of culinary options, partnering with a large number of restaurants to cater to diverse customer preferences and increase customer loyalty.

Our only concern is that consumers' loyalty is tied to the options available. If an increasing number of leading restaurants take deliveries in-house or choose to move to competitors, Delivery Hero could lose market share.

Economic & External Consideration

Current economic conditions, with high inflation and elevated interest rates, are likely the reason for slowing growth. These factors are inevitably impacting consumer spending behaviors, as individuals seek to cut costs to alleviate financial pressures. Our expectation is for conditions to remain difficult in the coming quarters, as inflationary pressure remains in the West (in particular).

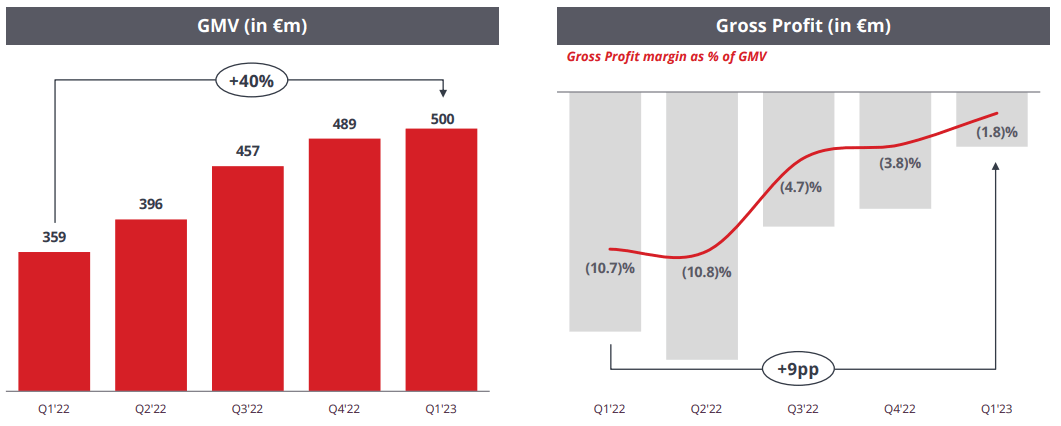

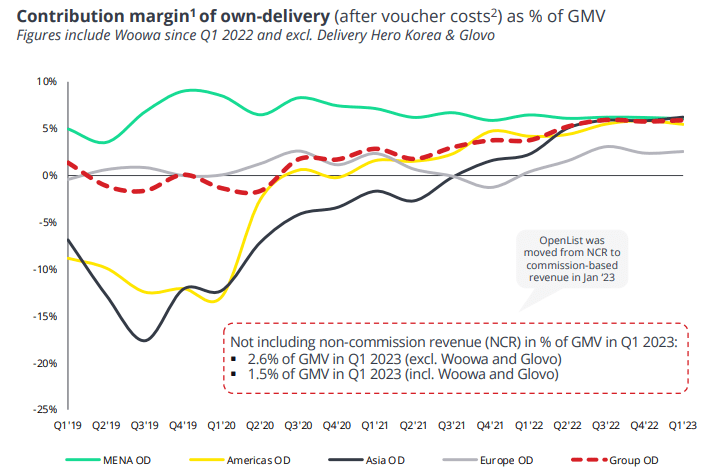

Margins

The biggest issue this industry faces is that it is unprofitable. Delivery businesses are spending significant amounts (or at least were) on customer acquisition while operating with slim margins due to the cost associated with delivery drivers.

Post-pandemic, we have seen an increased focus on the transition toward profitability, as investors have turned incredibly bearish. Delivery Hero continues to struggle with this, with an EBITDA-M of (13)%. Improvements are being made, as the below shows, but it is likely losses will continue, at least in the next year.

{kind=link}

Contribution margin (Delivery Hero)

Adj. EBITDA (Delivery Hero)

The issue the industry faces is that the fundamental dynamics make it difficult to achieve outsized returns. The apps can only squeeze so much from the restaurants and consumers via pricing, while also needing to ensure its delivery drivers are paid a fair amount. This leaves little wiggle room from which to generate a return. In the future, it is likely the use of delivery drones/robots will make this economically feasible but currently we are struggling to see an attractive profitability profile.

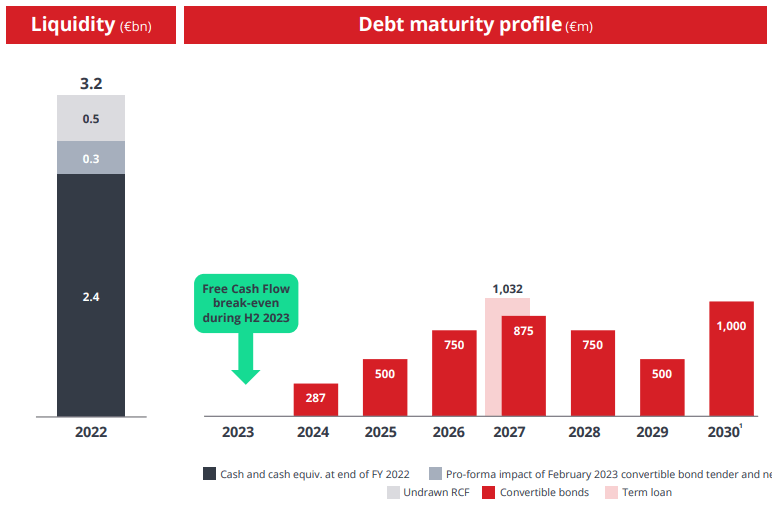

Balance sheet & Cash Flows

Although the business is burning through cash, it has substantial liquidity and no material levels of debt maturing in the next 12-24 months. For this reason, we see no immediate concerns around solvency.

{kind=link}

Debt profile (Delivery Hero)

Outlook

Outlook (Capital IQ)

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are forecasting a slight slowdown in growth into FY25, a reasonable view based on the current trajectory.

Margins are expected to improve in the coming years, although not by a material amount. This is likely based on a reduction in marketing spend relative to revenue, as well as scale economies.

Overarchingly, this looks quite unattractive in our view, especially given the cash spent in order to achieve these levels.

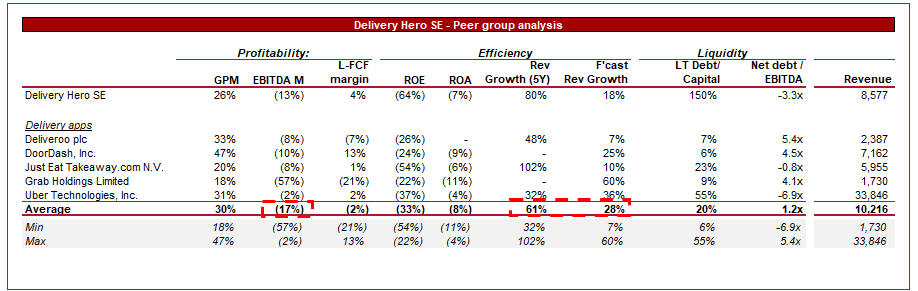

Peer analysis

{kind=link}

Delivery apps (Seeking Alpha)

Presented above is a comparison of Delivery Hero to a cohort of its directly comparable peers. The weak financial performance is a reflection of the struggles the industry is currently facing.

Delivery Hero looks quite unattractive relative to the group in our view. If we exclude Grab's terrible margins, Delivery Hero is currently falling behind in the profitable transition. Further, its forecast growth is below the average.

Valuation

Valuation (Capital IQ)

Delivery Hero is currently trading at 1.7x LTM Revenue and 1.4x NTM Revenue. This is a discount to its peer group.

The discount is warranted given the weak relative performance and the development required to achieve profitability.

Despite this, Delivery Hero and its peers still warrant good value given the large market share they hold across the globe. This is clearly an industry that provides consumers with significant value and so innovation will eventually yield a sustainable business model. Till then, investors need to consider if holding these stocks is worth it.

We think not. Even if a sustainable model is achieved, what will the profitability be? 10% EBTIDA-M? 15%? We do not think this is worth 2-3x revenue today.

Final thoughts

The delivery industry currently feels broken. The economics do not make sense and losses are being incurred at alarming levels. The growth and value proposition are clear, however, which means this is not an industry that will go away overnight. For now, we believe investors are better off avoiding Delivery Hero, as with growth slowing, there is little in the way of positives ahead.

For further details see:

Delivery Hero: Economic Headwinds And Operational Challenges