GRABW - Delivery Hero: Further Pain Ahead Before Any Hope Of Upside

2024-01-16 09:00:00 ET

Summary

- Delivery Hero’s top line growth has been stepping down from attractive levels, as the industry transitions to cost-cutting and price hikes to finally deliver margin improvement.

- Delivery Hero’s progress has been slow but appears to be on the cusp of adj. EBITDA positivity, although remains a long way from attractive margins.

- We expect growth to slow to high single-digits, while margin improvement beyond in the coming 3 years will be difficult due to the limited scope for an improvement to unit.

- Delivery Hero does have strong market share and we consider this its key characteristic. The industry requires consolidation, with its market share making it a leader.

- Delivery Hero stock is trading at a steep premium to its directly comparable peers, implying further potential downside despite its ~44% decline since Jul23.

Investment thesis

Our current investment thesis is:

- The delivery industry remains unattractive in our view. We have covered many stocks in the sector and see the same issues with all businesses. The fundamental unit economics do not work without multiple losers. This has not changed.

- Delivery Hero, and its peers, are progressing toward profitability, but this is slower than expected and is unlikely to reach attractive levels in the next 5 years (if ever).

- We believe the combination of slower growth and small-margin improvement will not be sufficient to justify an investment currently.

Company description

Delivery Hero SE (DLVHF) is a leading global online food delivery company headquartered in Berlin, Germany. The company operates a digital platform that connects consumers with a wide range of restaurants and food providers. With operations spanning multiple continents, Delivery Hero has established a strong presence in various markets, offering convenient and efficient food delivery services to millions of customers worldwide.

Share price

We last covered Delivery Hero in Jul23 , rating the stock a sell. Since then, the share price has declined ~44%, having already declined ~2% since it was listed several years prior. This continued downward trajectory is a reflection of further financial weakness which we will highlight in this paper.

In our prior analysis, we dived deep into the unit economics of the food-delivery industry and Delivery Hero’s business model, believing it to be fundamentally broken in the long-term, with limited visibility as to how success can be achieved without change. For a detailed analysis of Delivery Hero’s business model, and its industry, see this paper .

Financial analysis

{kind=link}

Presented above are Delivery Hero’s financial results on a half-year basis, as is reporting custom in Europe.

Recent performance

Despite the growing negative sentiment around Delivery Hero, the company has maintained impressive growth in absolute terms, with top-line growth of +124%, +55%, +40%, and +27% in its last four half-years.

The trajectory has clearly softened and continues to step-down, however. The industry continues to have high competition, with most firms (including Delivery Hero) transitioning focus to margin improvement, contributing to softening marketing spend that is inevitably hitting growth. Further, the industry is “mainstream” in Europe and Asia now and so market capture can only extend so far without consolidation.

The company’s growth is increasingly being driven by the development of its business model (price vs. volume) as Management desperately seeks to transition this business into a profitable company through scale. This has involved the introduction of Advertising for Restaurants (something we have been suggesting for many years), adjustment to unit economics to extract higher revenue, M&A, and the launching of related businesses such as DMart.

Delivery Hero’s GMV illustrates this, as it has grown +11.3% in H1’23, compared to revenue growth of +27%. This is heavily weighted toward Europe, which has grown by over 100%, in large part due to the acquisition of Glovo (Management has interestingly not applied a pro-forma adjustment, contributing to an overstatement in growth). Once done, GMV growth declines to ~3%. Its core market, Asia, has experienced a (6)% decline in GMV and a (2)% decline in Revenue, illustrating the negative impact of its driving margin improvement.

We are not overly impressed by the progress Delivery Hero has made. Margin development remains slow while growth is decelerating at a compounding rate. The company is increasingly being referred to in two parts by Management, “Profitable Platform Business” and “Unprofitable Platform Business”, which is harder to accept when the company is net losing money. Asia, which represents ~36% of revenue, currently has an adj. EBITDA margin of ~3%. The only other profitable segment is MENA, which represents ~24% of revenue. This means a significant ~40% of its revenue (Europe, Americas, and Integrated Verticals) is currently still unable to generate positive cash flows. Despite this, Delivery Hero has successfully ticked into the Adj. EBITDA positivity in H1.

Management has provided flash-trading for Q3, which broadly aligns with the trends we have observed during H1. The company’s revenue has outperformed again GMV for the factors mentioned above, up +9% vs. +2%. Growth was led by Europe +18% and MENA (+22%), while Americas (-0%), and Asia (-4%) struggled. Delivery Hero is experiencing intense competition in Asia following an initially impressive market share capture. We believe this needs to be monitored further, but has been on a clear downward trend since mid-2022.

The concern, however, is that growth has now fallen into the single digits. This reiterates the issue we have previously flagged. If Delivery Hero does reach profitability, it will likely come at the cost of any attractive growth (>10%). Thus investors are essentially left with single-digit margins.

Food Delivery Industry

The food industry has experienced a rapid shift in investor sentiment during the last 2 years, with rates increasing and growth slowing, contributing to parties no longer willing to finance losses.

This has contributed to a stalemate of sorts across many geographies (notwithstanding the potential issues such as in Asia), as competitors equally cut costs, find efficiencies, and lift prices. This has meant a degree of stabilization in market share. We consider this beneficial for Delivery Hero, as it is a leading player in a number of countries.

{kind=link}

Further, this has been highly beneficial for those who raised debt/equity prior to the change in economic conditions. Again, Delivery Hero is in a strong position with respect to this, boasting ~€2b in cash and nothing raised since H1’21.

Both these factors position Delivery Hero to be just that bit more aggressive relative to its peers, incrementally gaining market share while making comparable progress toward profitability objectives.

As stated in our prior analysis, consolidation or bankruptcies are required to shift this industry into a sustainable trajectory. We are already seeing the initial stages of this, as businesses cease aggressive expansions into new countries while exiting markets they cannot gain a sufficient foothold in. There are far too many players we feel, contributing to a lose-lose situation as players undercut each other. This relative advantage Delivery Hero finds itself in positions the company to be the “last man standing” (not from a literal perspective).

Economic & External Consideration

Economic conditions across much of the West have been muted, as inflations continue to step-down while rates remain elevated. This continues to restrict the expansion of consumer spending due to cost-of-living issues, although wage inflation and stick unemployment have meant a recession has been avoided (thus far). Asia and MENA have fared much better, although admittedly face geopolitical concerns and rising tensions in various pockets. Both factors are broadly reflected in Delivery Hero’s growth trajectory.

Looking ahead, we suspect economic conditions will be much of the same in H1’24, potentially stepping down, with an improvement likely in H1’25. H2’24 will be a critical period in our view, primarily due to the risk of a recession in the USA increasing. Europe, and then most of the World, usually follows in the USA’s steps and so we could easily experience a deterioration in demand.

Margins progression

At its current run-rate, we believe Delivery Hero will reach Adj . EBITDA positivity in FY23, while remaining in single-digits during the coming 5 years. The concern we have is how the company kicks on beyond this level, noting adj. EBITDA is not a recognized metric beyond implying FCF positivity is imminent.

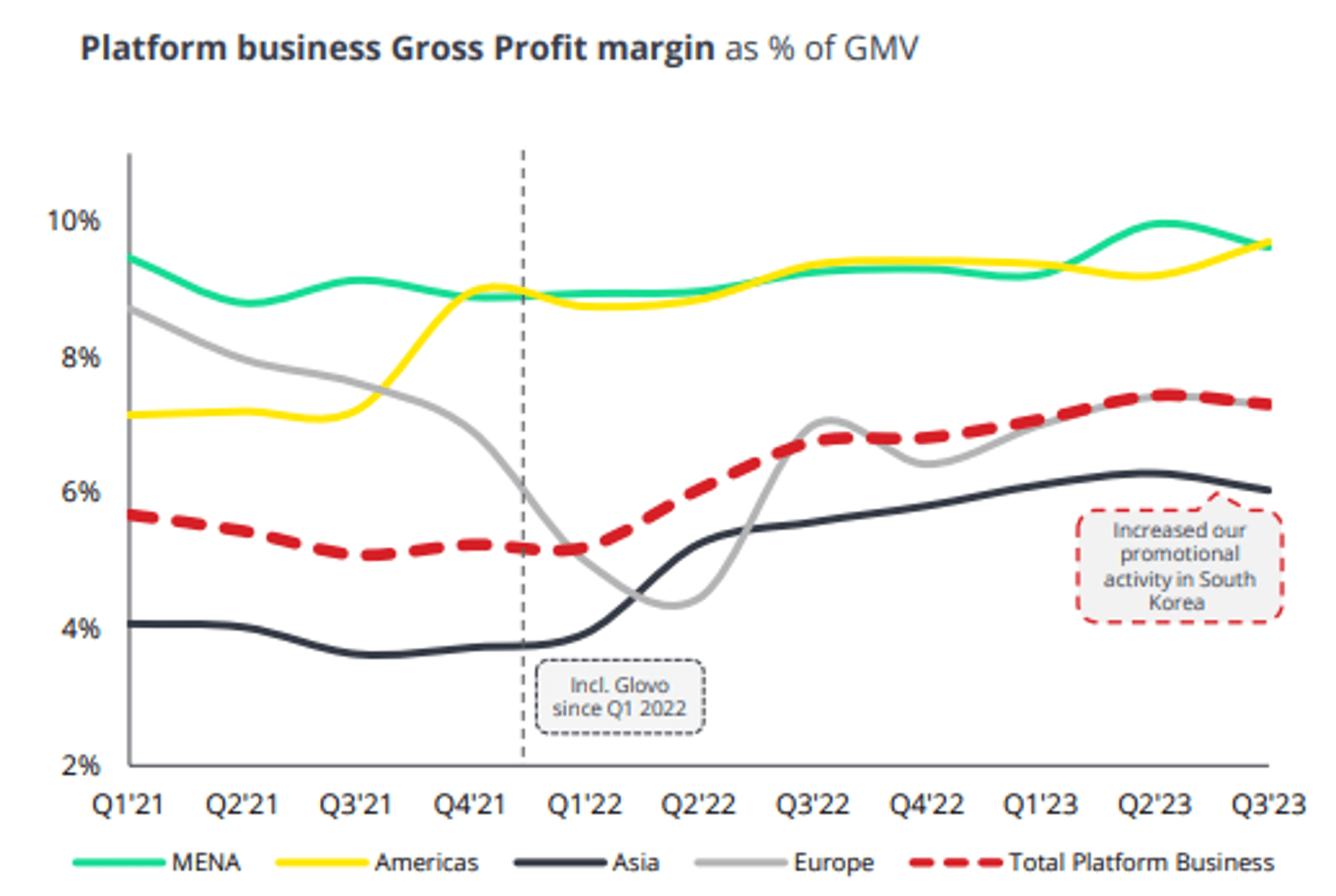

As the following illustrates, the company’s GM% progress has stalled for a number of quarters, regardless of maturity and scale, suggesting progress is not easily delivered any longer.

{kind=link}

Balance sheet & Cash Flows

As previously touched on, Delivery Hero is flush with cash, allowing it to service its current interest burden, which represents ~4% of revenue. The company is unlikely to imminently need cash, with M&A activity slowing and losses declining.

Outlook

{kind=link}

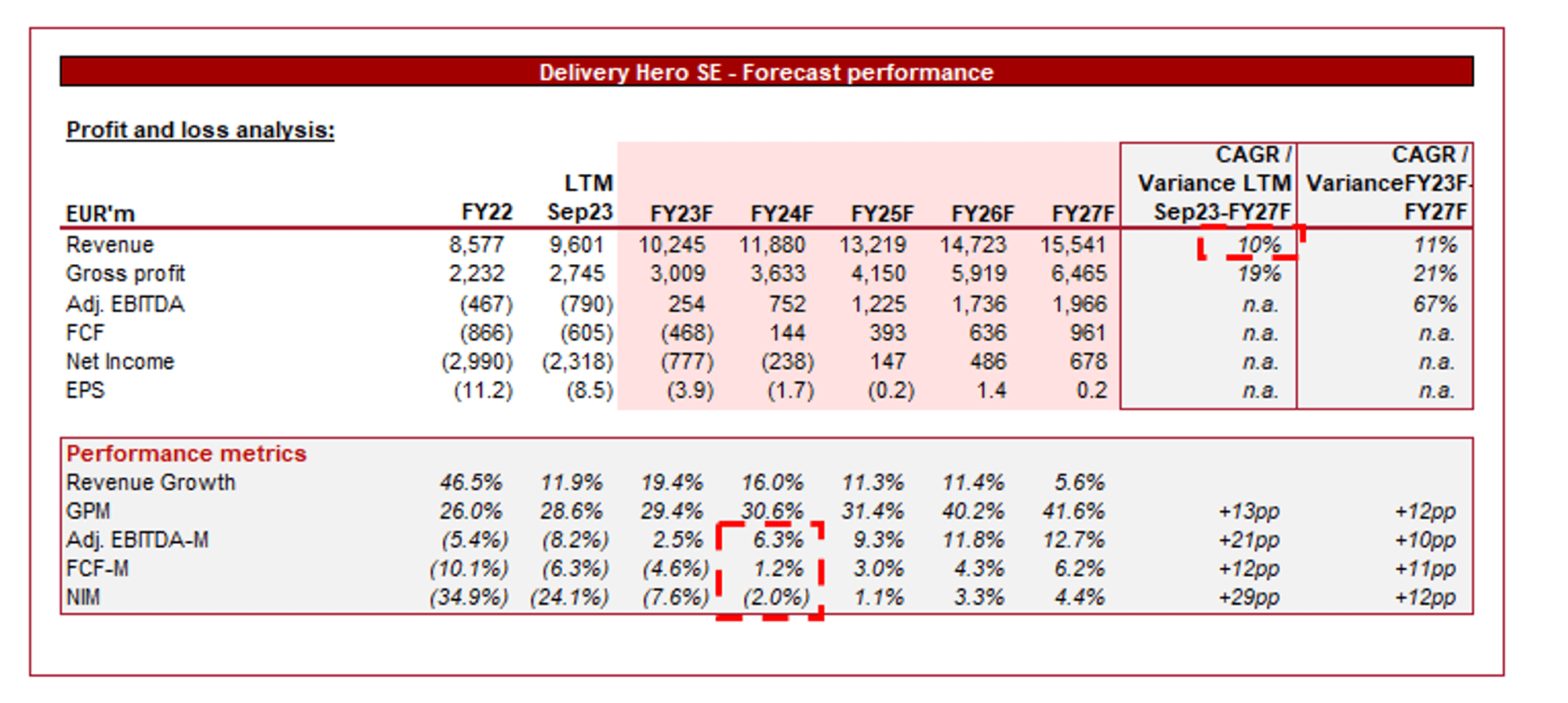

Presented above is Wall Street's consensus view on the coming years.

Analysts are forecasting a step-down in growth in the coming 5 years (+10% CAGR), alongside gradual margin improvement. We believe these forecasts to be on the opportunistic side, primarily due to the concerns we have raised. An acceleration is possible post-FY26F, following softening competition, but we are not overly supportive of +12% growth before then.

Beats and Misses

{kind=link}

In recent quarters, Delivery Hero has consistently missed estimates, which is following downward revisions. This reflects the significance of the slowdown.

Peer analysis

{kind=link}

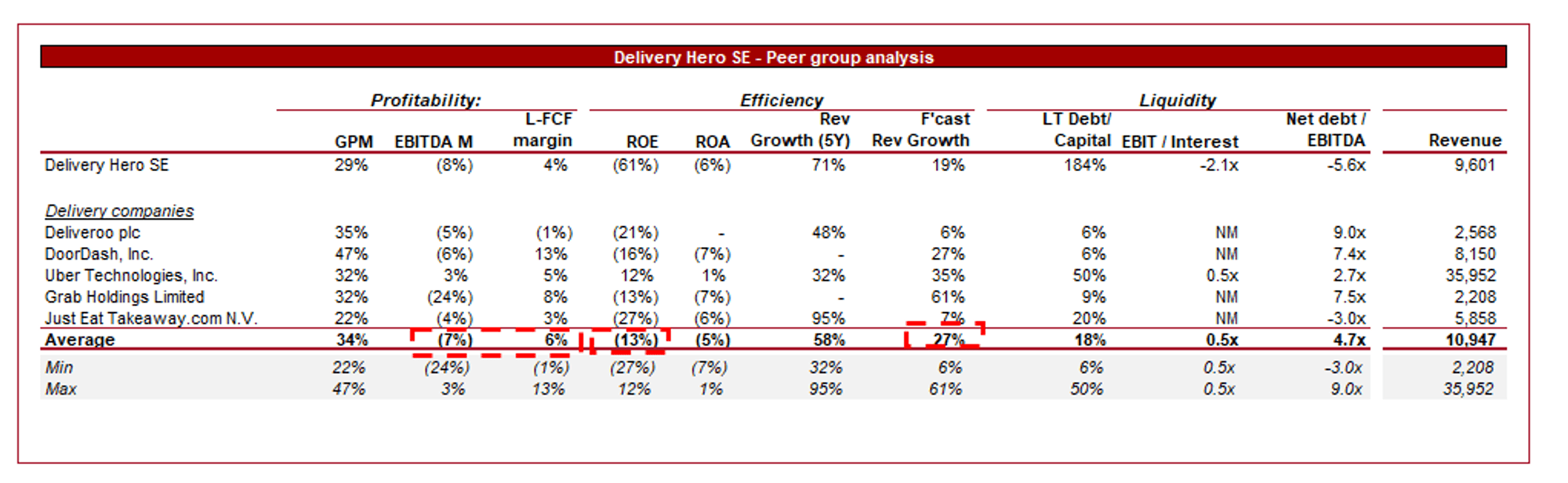

Presented above is a comparison of Delivery Hero to a cohort of its directly comparable peers (Deliveroo, Just Eat, DoorDash ( DASH ), Uber ( UBER ), and Grab ( GRAB ).

The company’s EBITDA-M margin is broadly consistent with its peers, although is notably above Deliveroo ( OTCPK:DROOF ) and Just Eat ( OTCPK:JTKWY ), the most comparable of the cohort. This implies slightly better progress by its peers, although clearly not noticeably so.

Further, The company’s ROE is significantly higher than all of its peers, reflecting substantial investment to achieve its current position. This will be far more important at a later stage, but if not a positive reflection of capital allocation.

Finally, Delivery Hero’s growth has been comparable to its peers, particularly when considering M&A (Which Deliveroo for example has been less active in). Looking ahead, Delivery Hero is expected to outperform both Deliveroo and Just Eat.

Valuation

{kind=link}

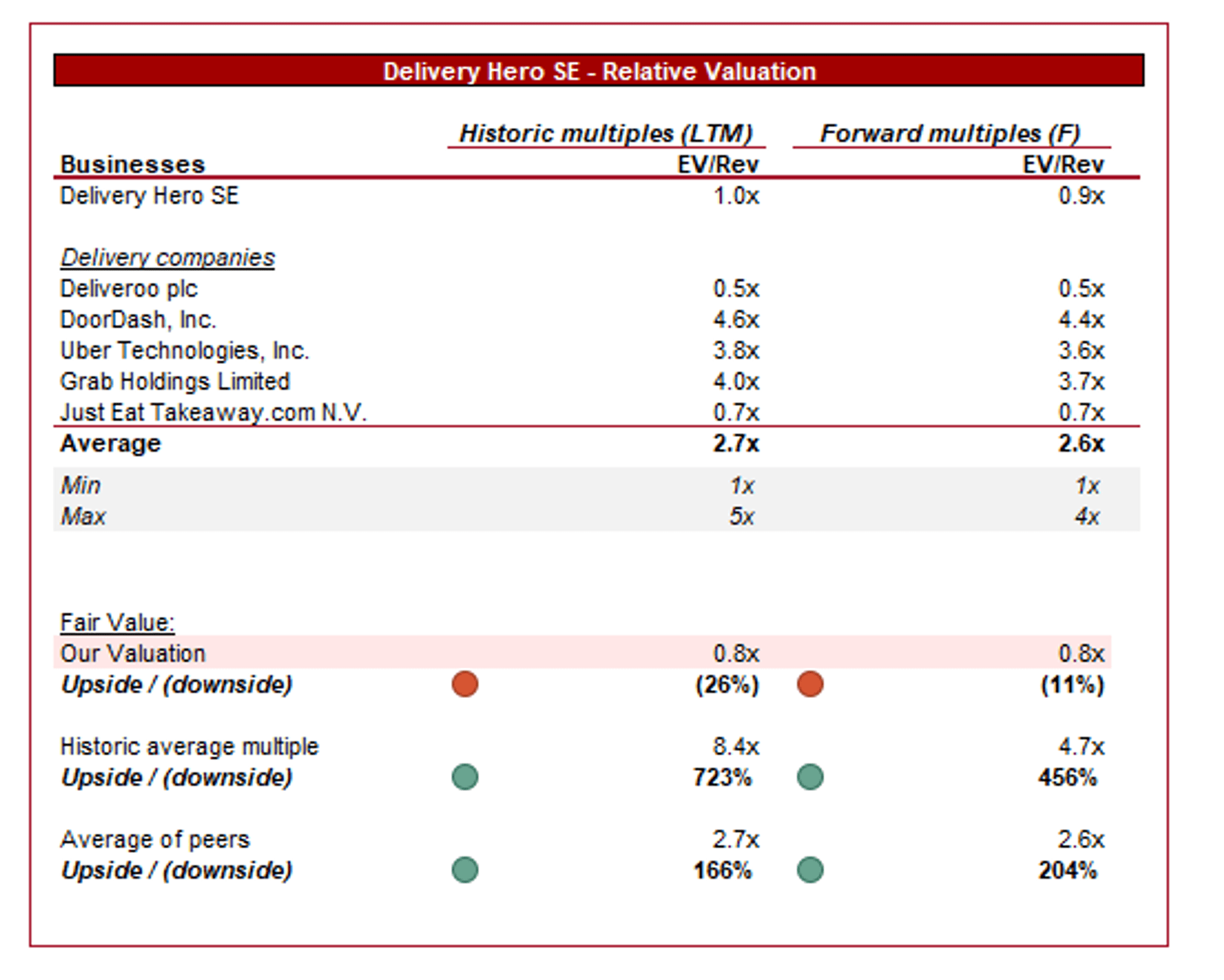

Delivery Hero is currently trading at 1x LTM Revenue and 0.9x NTM Revenue. This is a discount to its historical average.

Given the limited commercial and financial development, a discount is undeniably warranted. To trade at ~1x Revenue, markets are still pricing in reasonable progress, although to an overall profitability of ~HSD. We do believe this is possible, although will likely require over 5 years to deliver and significant execution risk.

{kind=link}

Delivery Hero is currently trading at a deep discount to its peers, primarily due to Uber and Grab, one of which is profitable already and the other is growing extremely quickly. When excluded, Delivery Hero is at a premium of ~40% on an LTM basis and ~29% on a NTM basis.

We believe Delivery Hero’s fair value is currently a ~25% premium to Deliveroo and Just Eat, primarily due to its commercial position. As discussed, the industry needs to fundamentally change, and we believe it will be a case of “Survival of the fittest”. For this reason, we consider certain weaknesses to be offset by its strong cash position and market share.

Even with said premium, we still see downside risk at Delivery Hero’s current valuation. With a difficult 2024 and broader 3Y period ahead, as growth normalizes and execution is observed through margin appreciation, we believe the industry is still far from attractive.

Key risks with our thesis

The key risk to our thesis, and fundamental view of the industry, is margin progression. If Delivery Hero can deliver a better-than-expected increase, its share price will respond positively.

Final thoughts

We have been highly critical of this industry and remain so, seeing limited progress and attractive earnings in the future. Delivery Hero continues to execute on margin improvement but is seeing the inevitable negative impact on its top-line, with issues in Asia only acting to compound its progress.

We do think it has staying power in Europe and Asia, which implies the potential for upside, but in its current position, we maintain our sell rating.

For further details see:

Delivery Hero: Further Pain Ahead Before Any Hope Of Upside