DELHY - Delivery Hero: The Mayhem Is Over Clear Road To Profitability

Summary

- Delivery Hero is a company managing food delivery platforms. Technology investor Prosus owns 25% of the company.

- Delivery Hero's recent trading update contained strong growth numbers considering hard comps.

- The company's EBITDA margin has increased rapidly, and so cash burn is set to decrease significantly going forward.

- Dilution and liquidity risks have lowered significantly.

- The market has priced in significant revenue growth and margin expansion, but the company is probably set to deliver on that and more.

Delivery Hero ( DLVHF ) published their Q4 2022 trading update last week. In the beginning of 2022 I wrote about Delivery Hero; while it seemed 'undervalued' at the time, the company was under significant dilution risks.

At the time, Delivery Hero stock had just experienced a huge decline from €130 to €28 in a couple of months, losing billions of market capitalization and creating a lot of drama around the company. Now a year later DH seems to be in a much better position.

The bull case

Let me shortly reiterate the bull case on Delivery Hero. Delivery Hero manages food delivery platforms across the globe. The company is particularly highly exposed to emerging markets (South Korea is a huge position) through countries in Asia, Middle East, Europe and the Americas. Generally speaking, these countries are considerably underpenetrated in terms of food delivery and are likely set to have relatively high economic growth rates; a golden combination for high revenue growth rates to come. Food delivery platforms embody highly attractive economics; the three-party network with restaurants, drivers and consumers is difficult to break. Particularly, the largest platform in a country can acquire customers at a significantly lower CAC due to efficient marketing investments. Recreating the network of restaurants and to a lesser extent drivers is not an easy task either. Delivery Hero's high historical growth rates (66% constant currency GMV growth in 2021) are partially a consequence of that.

One big reason for the significant stock decline last year was management's bad capital allocation:

- I do continue to be critical of the Glovo acquisition of DH; while I see the growth potential in Eastern Europe the company is facing significant regulatory backlash in Spain. Spain and Italy made up nearly a majority of Glovo's GMV in the beginning of 2022 and particularly Spain is Glovo's strongest position.

- Also, consider the investment in Deliveroo ( DROOF ) - that currently has a negative enterprise value. Last year, Delivery Hero acquired a significant stake in Deliveroo. Deliveroo is under significant competitive pressure from Just Eat Takeaway (JTKWY) and Uber (UBER) Eats; it is clear that the CEO of Just Eat Takeaway wants to conquer the UK and London. Deliveroo is the market leader in London and Italy (where Just Eat is a close second) - but it does not have the financial means to sustain those positions in my opinion. The stock price reflects that. Just adding a quote from the JET CEO from Q4 2021 call:

" We are going to invest whatever is necessary to make sure that we are going to be by far the market leader in London." Jitse Groen , CEO of Just Eat Takeaway

Management needs to have a better capital allocation strategy going forward. I am optimistic about that.

One of the largest technology investors in the world, Prosus ( PROSY ) owns 25% of Delivery Hero. This puts more reputation under the investment case of Delivery Hero. Prosus is optimistic about food delivery as a long term investment and clearly they see Delivery Hero as one of the best investment vehicles to benefit.

Market shares

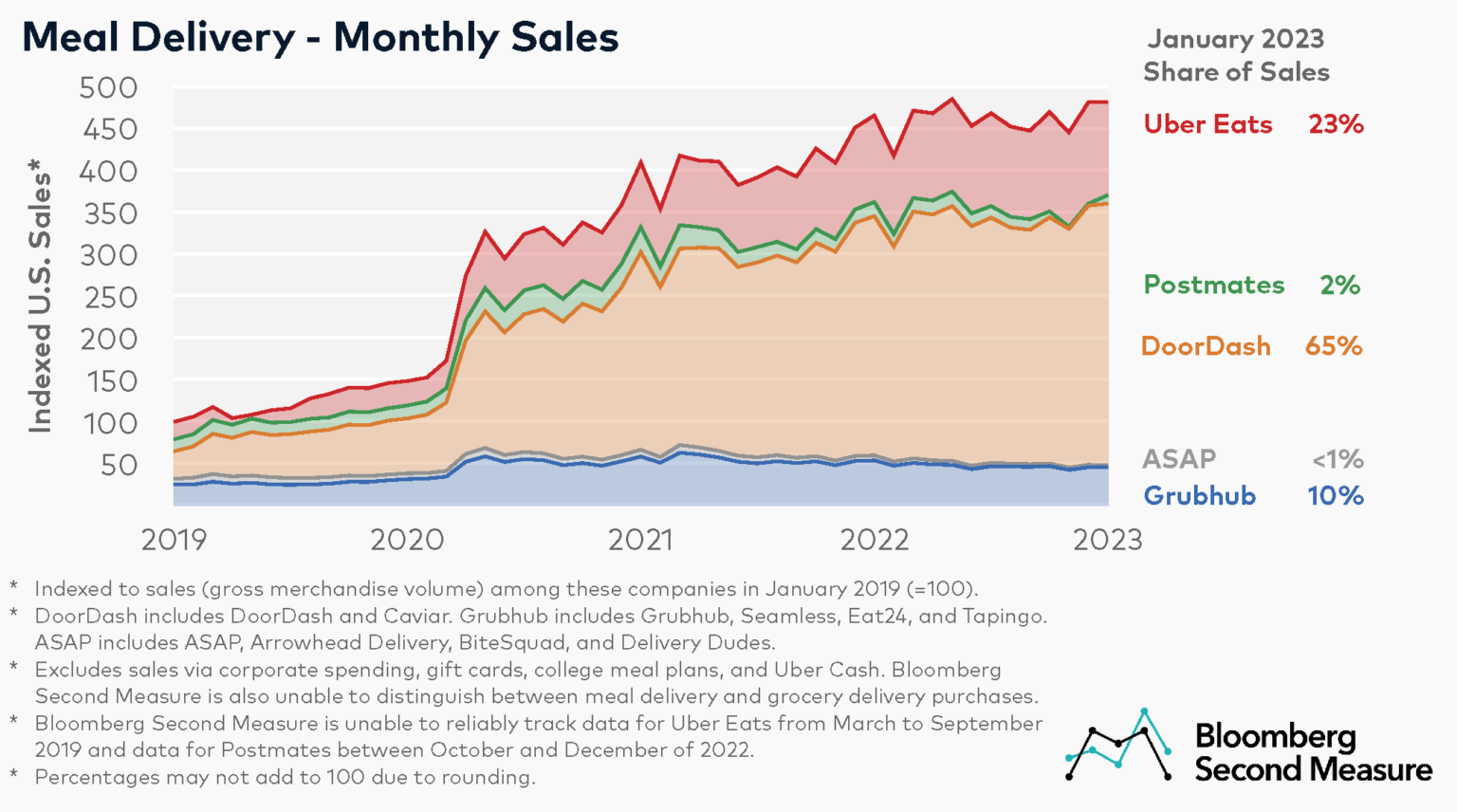

Delivery Hero generally operates market leading or competitive number 1 position in most of its markets. 51 % market share in the Philippines in May 2022, 64% market share in Hong Kong, 54% market share in Spain (with significant regulatory backlash) and a strong market leading position in South Korea. Management stated in the recent call market share is expanding in 'nearly all countries'.

Bloomberg Second Measure (Bloomberg Second Measure)

{kind=link}

In Asia its biggest competitors are Uber and Grab ( GRAB ). Both Uber and Grab are food delivery and ride hailing platforms. These platforms are able to sell food delivery benefits and ride hailing benefits in one subscription. I am not optimistic about the value proposition of combining food delivery and ride hailing benefits in one subscription. In the US DoorDash ( DASH ) has significantly outgrown Uber Eats in recent years and become the clear market leader in most areas. In Brazil, Uber also lost massively to iFood - of which Just Eat Takeaway recently sold its 33% stake to Prosus. Brazil is Uber's highest penetrated market in terms of weekly active users for its ride hailing service. Yet it left the food delivery market at the start of 2022 due to iFood's dominance.

I do not see these ride hailing competitors with food delivery platforms as posing a significant risk to DH's story - particularly considering DH's leading position in most of its markets.

Uber Investor Relations Day (Uber Investor Relations Day)

{kind=link}

Results

FY2022 results from Delivery Hero came out strong. GMV of the group grew by 17.5% in 2022 with growth slowing down in Q4 2022 to 8.8%. Probably a significant portion of this driven by AOV expansion so no outlook on order growth. Particularly noticeable is the growth at the MENA and Europe businesses, these businesses grew their GMV by 18% and 19%, respectively, from Q1 2021 to Q1 2022, while the Americas and Asia segments saw practically no growth. These are actually very good results in a quarter with very difficult comps: energy crisis, economic uncertainty and eased lockdowns. The strong performance across the board strengthens the case for reasonably strong growth at Delivery Hero going forward into the next years.

The group increased profitability massively, with the adj EBITDA margin sitting at -0.3% in Q4 2022 from Q4 2021. Annualized we are talking about a €1.34 billion improvement in adj EBITDA in just one year. This really shows how profitability in food delivery is very much in control of the company's management. A slowdown in marketing spend and increased focus on logistical efficiency / value-adding orders can easily add a billion in adj EBITDA in a year's time.

Considering the company burned €1.2 billion in ttm 2022, this recent margin expansion looks set to significantly lower cash burn going forward.

The company is guiding for adj EBITDA margin to expand to 1% of GMV by H2 2022. Annualized with 15% GMV growth, this is approximately €500 million in adj EBITDA at H2 2022. On this discussion, we have to wonder whether Delivery Hero will be returning vast amounts of EBITDA in the coming years. Listening to the call, management clearly states they believe many of their markets are underpenetrated and provide attractive reinvesting opportunities. I think we have to expect management to increase profitability to a level that takes away any significant liquidity and dilution risks, but not further.

Advertising

Delivery Hero is optimistic about the traction in advertising. It is attractive that quick commerce and restaurants can spend an extra buck on advertising to get more attention for their offering, but I think the CEO of Just Eat Takeaway had a relevant point about that:

'I do want to caution on the optimism because I see a lot of people write about advertisement, et cetera. It's not that these restaurants have so much money to play around with, right? I mean it's still a marginal okay, I want to be higher than my neighbor sort of thing. You should not expect all of a sudden the commission revenue to double as a result of that. And I see sometimes very optimistic views on this in the analyst reports. ' ~Jitse Groen, Q4 2022 Trading Update Call JET

The attractiveness of advertising revenues is that it obviously is a software margin revenue. Excluding marketing cost we are talking 90+% adj EBITDA here depending per company. If Delivery Hero can make advertising revenues 10% of long-term revenues at a 50% adj EBITDA margin that is an extra €500 million in adj EBITDA at this year's revenue. But with 20% CAGR growth rates in the coming years (which are likely) I can easily see advertising contribute a billion in adj EBITDA in a couple of years.

It makes me wonder; what the difference is between advertising and the marketplace. In both cases, restaurants pay a software margin fee to get customers to order food on a platform. If the platform has a moat and has the most customers, that is a sustainable revenue stream. Why is advertising hip and marketplace outdated? Frankly, I see very little difference except that marketplace restaurants operate their own delivery fleet, but that is a more relevant discussion in a Just Eat Takeaway article.

Valuation

Delivery Hero continues to be significantly leveraged with a net debt of €2.6 million and a total debt of €5.7 million (cash at €3 billion). On February 13, 2023, the company raised a convertible bond with a 3.5%-4% interest rate. The company should be able to pay that interest rate easily across its debt.

With a stock price of €42.10 the market cap sits at €10.8 billion and the enterprise value at €13.4 billion

Below you can see a simple model with a 20% CAGR for GMV from 2023 to 2028 and a adj EBITDA margin of 3% at 2028. With an enterprise value of €13.4 billion, this models implies 3.3 times current EV / 2028 adjusted EBITDA. Maybe before that the shareholders get some cash flows from 2025 to 2027. Paying 3.3 times adj EBITDA for 2028 is not incredibly attractive (with a 50% adj EBITDA to FCF conversion that is 6.6 times FCF), and so clearly adj EBITDA margins or/and revenue growth rates have to be a bit higher. I think DH could pull that off with significant probability of success. Particularly the margins. Increasing adj EBITDA margins to 5% or 6% - which is actually pretty realistic - paints a very different picture (1-1.5 times adj EBITDA becoming 2-3 times FCF). The stock still prices in significant pessimism. Considering recent margin expansion it is likely DH can achieve that mature state with little dilution and bond raises from now on.

Also, if you look at financials of Grubhub and Just Eat in 2017 and 2018 the EBITDA to FCF conversation rate becomes more like 80-90% in a mature state; as these businesses are very capital efficient and require little capex in a mature form. With those conversation ratios a 20% CAGR and 6% adj EBITDA margins leads to free cash flows of approximately €7 billion by 2028.

Estimates for Delivery Hero coming years (Author)

{kind=link}

Conclusion

Delivery Hero is well-positioned to benefit from the adoption of food delivery in emerging markets, while the stock may seem expensive at first glance, excellent operational performance and capital allocation can lead to a significant increase in the stock price.

For further details see:

Delivery Hero: The Mayhem Is Over, Clear Road To Profitability