DAL - Delta Air Lines: Continuing Sell Thesis

2024-01-14 21:16:00 ET

Summary

- Delta Air Lines' management team has revised its earnings outlook, signaling a potential slowdown in travel demand due to worsening macroeconomic conditions.

- Consumer loan delinquency rates and personal savings rates have worsened, indicating that the average US consumer's financial situation is getting tighter.

- The airline industry is cyclical, and the minor reduction in Delta Air Lines' profit forecast suggests that the industry may be facing a slower travel demand.

Introduction

In my previous article , I had a sell rating on Delta Air Lines ( DAL ). At the time, I believed the potential macroeconomic headwinds were getting stronger, which could ultimately impact Delta Air Lines. Not only were consumers' financial health starting to show signs of weakness through disposable personal income and loan delinquency data, but the unemployment data were starting to show a slow uptrend. Thus, as travel is one of the first discretionary spending consumers forego in times of economic hardship or an expectation of relatively worse economic conditions, I had a sell rating on Delta Air Lines. Today, I continue to stand by these arguments. In fact, I believe my thesis became more compelling. Not only has numerous economic data further suggest a potential slowdown in travel demand due to the macroeconomic conditions slowing, but Delta Air Lines' management team has finally revised its earnings outlook in response to these conditions. Therefore, I continue to believe Delta Air Lines is a sell.

Macroeconomic Conditions

It has been about four months since my initial sell thesis on Delta Air Lines, and since then, macroeconomic conditions have worsened.

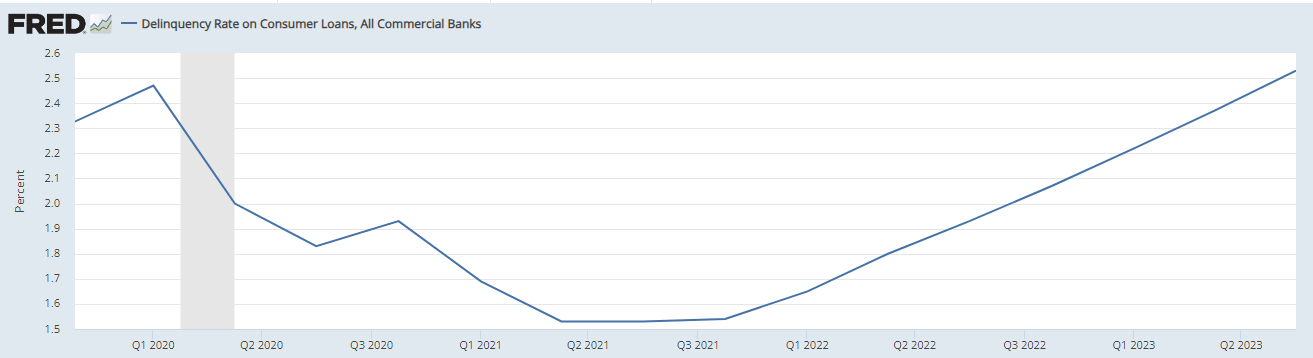

Starting with the delinquency rate on consumer loan data, from 2023Q2 delinquency rate of 2.37% , the consumer loan delinquency increased about 6.75% quarter-over-quarter to 2.53% as the chart below shows. Further, the increase in consumer loan delinquencies has been an ongoing problem since the peak of the pandemic with no clear signs of slowing potentially indicating that the consumers' financial situation could continue to worsen going forward. This claim is supported by the rate at which the delinquency rates are increasing. From 2023Q1 to 2023Q2, the delinquency rate increased to about 6.76%, nearly identical to the rate increase from 2023Q2 to 2023Q3. Thus, the rate at which delinquency is increasing suggests that the current trend will likely be ongoing.

{kind=link}

St. Louis Federal Reserve

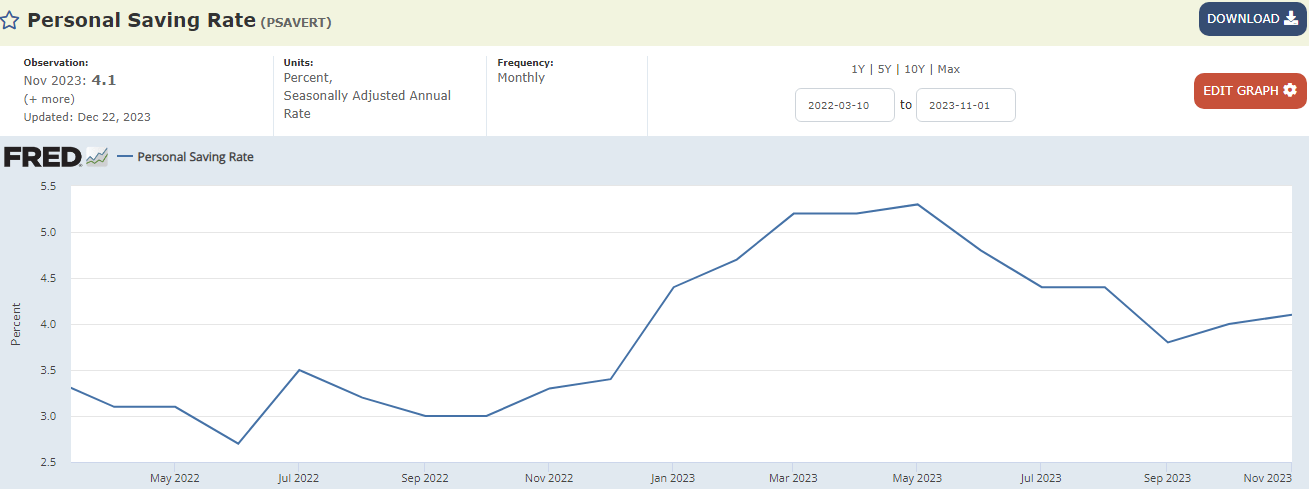

Further, the personal savings rate has also worsened since my previous article. As the chart below shows, the personal savings rate has declined about 7% from August 2023 to November 2023.

{kind=link}

St. Louis Federal Reserve

Overall, I believe it is fairly evident that the average US consumer's financial situation is getting tighter, and because it is the case that consumers tend to cut discretionary spending in times of economic hardship, I believe Delta Air Lines will continue to see a headwind for the foreseeable future.

CPI data supports this argument. On January 11th, 2024, the US Bureau of Labor Statistics released the December 2023 CPI data . The year-over-year airline fares declined by 9.4% and increased by 1% month-over-month. Investors, in my opinion, should focus more on the year-over-year data as December travel is busier than November travel, which is likely the reason for a month-over-month airfare increase. Thus, as reflected by the airfare, the demand environment does not seem to be positive for Delta Air Lines.

Delta Air Lines Earnings Report

On January 12th, 2024, Delta Air Lines released the 2023Q4 earnings report. The fourth quarter operations were positive. The company reported a revenue of $14.2 billion and an operating income of $1.3 billion with a margin of 9.3%. The strong results allowed the company to reduce debt and finance lease obligations by $361 million. However, the company's initial guidance for 2024 came in below the market expectation. The market was expecting the company to report over $7 per share in earnings, but the company is guiding for $6 to 7 per share in earnings, which would mean that the bottom-line expansion will be minimal in 2024.

One may point out that the 2023Q4 results and 2024 outlook, while not as strong as before, continue to be positive as the company is still expecting to report strong earnings while paying down debt. Although this argument is true, I believe it also could be short-sighted. The airline industry is extremely cyclical, and the macroeconomic data has been pointing toward a slowdown in the economy for the past several quarters. Despite these developments in the economy, the airline industry including Delta has continued to tout record demand and strong future demand. These commentaries have likely allowed the investors to think that the airline industry will continue to flourish even as there are some minor slowdowns in the economy as the world post-pandemic is far different from pre-pandemic times. In other words, investors likely believed the airline industry's short-term demand forecast while thinking the cyclicality of the industry was a thing of the past. And, when Delta Air Lines finally reduced this growth expectation, although minor, gave a reality check to the market. The airline industry is still cyclical. If there is some trouble brewing in the economy whether it is extreme or just a minor slowdown, the airline industry will inevitably be affected. Therefore, I viewed the minor expectation change to Delta Air Lines' bottom line forecast to be symbolic and significant. Airline's future expectations for demand are finally coming in line with the macroeconomic data, which could just be the beginning of a slower travel demand.

Risk to Thesis

Along with the macroeconomic condition, I am expecting Delta Air Lines and the airline industry to see some form of a slowdown in demand. Thus, my thesis heavily relies on the macroeconomic conditions to worsen leading to the reduced travel demand. However, if it is the case that the macroeconomic conditions today are already in a trough and are reaching a soft landing, my negative outlooks could be in peril. If there is no meaningful slowdown in the economy, it is likely for the airline industry to continue flourishing with no hiccups to demand. Further, while it is true that numerous economic data are pointing towards a weakening consumer financial health, some data including the unemployment rate continue to show strength, which could continue to support the economy.

Summary

Delta Air Lines' 2023Q4 earnings report was both symbolic and significant. For the past few quarters, the macroeconomic data has been pointing toward a slowing travel demand, yet the airline industry including Delta has touted strong demand saying that they do not see any slowdowns. Thus, there were discrepancies and high hopes from investors that the post-pandemic travel industry could be less cyclical than in the past. However, during the 2023Q4 earnings call, Delta Air Lines' management team reduced the profit forecast signaling that the airline is not expected to continue its strong growth in 2024, which could be the first signal of the slowing demand. Therefore, I believe my sell thesis became stronger leading to a continued sell rating.

For further details see:

Delta Air Lines: Continuing Sell Thesis